Trading Patterns Centered Around Large Institutional Purchase Events In

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Government of India Ministry of Heavy Industries and Public Enterprises Department of Public Enterprises

GOVERNMENT OF INDIA MINISTRY OF HEAVY INDUSTRIES AND PUBLIC ENTERPRISES DEPARTMENT OF PUBLIC ENTERPRISES LOK SABHA UNSTARRED QUESTION NO. 1428 TO BE ANSWERED ON THE 11th FEBRUARY, 2020 ‘Job Reservation for SCs, STs and OBCs in PSUs’ 1428. SHRI A.K.P. CHINRAJ : SHRI A. GANESHAMURTHI : Will the Minister of HEAVY INDUSTRIES AND PUBLIC ENTERPRISES be pleased to state:- (a) whether the Government is planning to revamp job reservations issue for Scheduled Castes (SCs), Scheduled Tribes (STs) and Other Backward Classes (OBCs) in State-run companies following sharp fall of employment opportunities to them consequent upon disinvestment in all the Public Sector Enterprises (PSEs); (b) if so, the details thereof; (c) whether it is true that the Department of Investment and Public Asset Management (DIPAM) is examining the issue of job reservations for SCs, STs and OBCs in State run companies following disinvestment and if so, the details thereof; (d) the total disinvestment made in various PSEs company and category-wise during the last three years along with the reasons for disinvestment; (e) the total number of SCs, STs and OBCs presently working in various PSEs company and category-wise; and (f) the total number of SCs, STs and OBCs who lost their jobs in these companies during the said period? ANSWER THE MINISTER FOR HEAVY INDUSTRIES & PUBLIC ENTERPRISES (SHRI PRAKASH JAVADEKAR) (a to d): Job reservation is available to Scheduled Castes (SCs), Scheduled Tribes (STs) and Other Backward Classes (OBCs) in Central Public Sector Enterprises (CPSEs) as per the extant Government policy. The Government follows a policy of disinvestment in CPSEs through Strategic Disinvestment and Minority Stake sale. -

Government of India Ministry of Finance Department of Investment and Public Asset Management

GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF INVESTMENT AND PUBLIC ASSET MANAGEMENT BACKGROUND MATERIAL FOR ECONOMIC EDITOR’S CONFERENCE MANDATE The mandate of the Department of Investment and Public Asset Management (DIPAM), inter-alia, includes disinvestment of Government’s shareholding in Central Public Sector Enterprises (CPSEs), matters relating to GoI’s investment in equity like capital restructuring, bonus, dividends and other related issues. DISINVESTMENT POLICY • On February, 2016, a new policy for management of Government investment in CPSEs, including disinvestment and strategic sale was approved. This was to leverage the assets of CPSEs for generation of resources for investment in new projects. This allows CPSEs to divest individual assets like land, manufacturing units etc. to release their asset value for making investment in new project. • The Department of Disinvestment (DoD) has been renamed as Department of Investment and Public Asset Management (DIPAM) with enhanced mandate of efficient management of Government investment in CPSEs by addressing issues such as capital restructuring, dividend, bonus shares etc. The approach is towards capital management from investor’s point of view. OBJECTIVES The objectives of Disinvestment Policy are: - (a) Promote people’s ownership of CPSEs to share in their prosperity through disinvestment. (b) Enables efficient management of public investment in CPSEs for accelerating economic development and augmenting Government’s resources for higher expenditure. (c) Listing of CPSEs on stock exchanges to facilitate development and deepening of capital market and spread of equity culture. (d) Raising budgetary resources for the Government. 1 COPREHENSIVE MANAGEMENT OF GOI’s INVESTMENT IN CPSEs • The Government recognizes its investment in CPSEs as an important asset for accelerating economic growth and is committed to efficient use of these resources to achieve optimum return. -

Details of Offmarket/Interdepository Debit/Credit Transactions for 50000 Or More Equity Shares in ISIN for the Period 01-Jun-2020 to 15-Jun-2020 Sr

Details of OffMarket/Interdepository debit/credit transactions for 50000 or more equity shares in ISIN for the period 01-Jun-2020 to 15-Jun-2020 Sr. No. Isin Isin_Short_Name Tran_Qty Tran_date 1 IN9002A01024 RELIANCE IND-PP EQ 266492 15-06-2020 2 IN9155A01020 TATA MOTOR-A-DVR EQ2 81364 06-06-2020 3 IN9155A01020 TATA MOTOR-A-DVR EQ2 178009 01-06-2020 4 IN9155A01020 TATA MOTOR-A-DVR EQ2 211342 15-06-2020 5 IN9155A01020 TATA MOTOR-A-DVR EQ2 239201 12-06-2020 6 IN9155A01020 TATA MOTOR-A-DVR EQ2 305800 08-06-2020 7 IN9155A01020 TATA MOTOR-A-DVR EQ2 348259 04-06-2020 8 IN9155A01020 TATA MOTOR-A-DVR EQ2 410219 05-06-2020 9 IN9155A01020 TATA MOTOR-A-DVR EQ2 520355 09-06-2020 10 IN9155A01020 TATA MOTOR-A-DVR EQ2 591155 11-06-2020 11 IN9155A01020 TATA MOTOR-A-DVR EQ2 716341 03-06-2020 12 IN9155A01020 TATA MOTOR-A-DVR EQ2 835762 13-06-2020 13 IN9155A01020 TATA MOTOR-A-DVR EQ2 1370395 10-06-2020 14 IN9155A01020 TATA MOTOR-A-DVR EQ2 2404661 02-06-2020 15 IN9175A01010 JAIN IRRIGATI EQ DVR 212299 09-06-2020 16 IN9175A01010 JAIN IRRIGATI EQ DVR 218576 11-06-2020 17 IN9274G01034 INDIABULLS VEN-PP EQ 147332 09-06-2020 18 IN9623B01058 FUTURE - EQ - DVR 2085510 09-06-2020 19 IN9623B01058 FUTURE - EQ - DVR 2085922 11-06-2020 20 INE0AEJ01013 BIRLA TYRES-EQ 56403 10-06-2020 21 INE0AEJ01013 BIRLA TYRES-EQ 68709 06-06-2020 22 INE0AEJ01013 BIRLA TYRES-EQ 107614 04-06-2020 23 INE0AEJ01013 BIRLA TYRES-EQ 115222 11-06-2020 24 INE0AEJ01013 BIRLA TYRES-EQ 2473057 15-06-2020 25 INE0AU701018 ICL ORGANIC DAIRY-EQ 78000 04-06-2020 26 INE00CX01017 MAHIP INDUSTRIES-EQ 2200000 -

List of Nodal Officer

List of Nodal Officer Designa S.No tion of Phone (With Company Name EMAIL_ID_COMPANY FIRST_NAME MIDDLE_NAME LAST_NAME Line I Line II CITY PIN Code EMAIL_ID . Nodal STD/ISD) Officer 1 VIPUL LIMITED [email protected] PUNIT BERIWALA DIRT Vipul TechSquare, Golf Course Road, Sector-43, Gurgaon 122009 01244065500 [email protected] 2 ORIENT PAPER AND INDUSTRIES LTD. [email protected] RAM PRASAD DUTTA CSEC BIRLA BUILDING, 9TH FLOOR, 9/1, R. N. MUKHERJEE ROAD KOLKATA 700001 03340823700 [email protected] COAL INDIA LIMITED, Coal Bhawan, AF-III, 3rd Floor CORE-2,Action Area-1A, 3 COAL INDIA LTD GOVT OF INDIA UNDERTAKING [email protected] MAHADEVAN VISWANATHAN CSEC Rajarhat, Kolkata 700156 03323246526 [email protected] PREMISES NO-04-MAR New Town, MULTI COMMODITY EXCHANGE OF INDIA Exchange Square, Suren Road, 4 [email protected] AJAY PURI CSEC Multi Commodity Exchange of India Limited Mumbai 400093 0226718888 [email protected] LIMITED Chakala, Andheri (East), 5 ECOPLAST LIMITED [email protected] Antony Pius Alapat CSEC Ecoplast Ltd.,4 Magan Mahal 215, Sir M.V. Road, Andheri (E) Mumbai 400069 02226833452 [email protected] 6 ECOPLAST LIMITED [email protected] Antony Pius Alapat CSEC Ecoplast Ltd.,4 Magan Mahal 215, Sir M.V. Road, Andheri (E) Mumbai 400069 02226833452 [email protected] 7 NECTAR LIFE SCIENCES LIMITED [email protected] SUKRITI SAINI CSEC NECTAR LIFESCIENCES LIMITED SCO 38-39, SECTOR 9-D CHANDIGARH 160009 01723047759 [email protected] 8 ECOPLAST LIMITED [email protected] Antony Pius Alapat CSEC Ecoplast Ltd.,4 Magan Mahal 215, Sir M.V. Road, Andheri (E) Mumbai 400069 02226833452 [email protected] 9 SMIFS CAPITAL MARKETS LTD. -

Inner 27 Quant Fund Low

Tata Quant Fund (An Open Ended Equity Scheme following quant based investing theme) As on 31st May 2020 PORTFOLIO INVESTMENT STYLE Primarily focuses on investing in equity and equity related Company name No. of Market Value % of Company name No. of Market Value % of instruments following quant based investing theme. Shares Rs. Lakhs Assets Shares Rs. Lakhs Assets INVESTMENT OBJECTIVE Equity & Equity Related Total 9103.72 94.70 Pharmaceuticals The investment objective of the scheme is to generate Auto Cipla Ltd. 52242 338.61 3.52 medium to long-term capital appreciation by investing in Hero Motocorp Ltd. 12845 303.25 3.15 Torrent Pharmaceuticals Ltd. 13914 328.73 3.42 equity and equity related instruments selected based on a Auto Ancillaries Ajanta Pharma Ltd. 19417 295.91 3.08 quantitative model (Quant Model). Motherson Sumi Systems Ltd. 382196 364.23 3.79 Syngene International Ltd. 82231 293.65 3.05 However, there is no assurance or guarantee that the Amara Raja Batteries Ltd. 53772 330.48 3.44 Cadila Healthcare Ltd. 82364 283.83 2.95 investment objective of the Scheme will be achieved. The scheme does not assure or guarantee any returns. Balkrishna Industries Ltd. 30195 325.77 3.39 Divi Laboratories Ltd. 11650 278.45 2.90 MRF Ltd. 429 253.60 2.64 Sanofi India Ltd. 3579 276.75 2.88 DATE OF ALLOTMENT Consumer Durables Abbott India Ltd. 1489 249.01 2.59 January 22, 2020 Whirlpool Of India Ltd. 12930 251.44 2.62 Pfizer Ltd. 6095 246.15 2.56 FUND MANAGER Consumer Non Durables Alkem Laboratories Ltd. -

Sharekhan Special August 31, 2021

Sharekhan Special August 31, 2021 Index Q1FY2022 Results Review Automobiles • Capital Goods • Consumer Discretionary • Consumer Goods • Infrastructure/Cement/Logistics/Building Material • IT • Oil & Gas • Pharmaceuticals • Agri Inputs and Speciality Chemical • Miscellaneous • Visit us at www.sharekhan.com For Private Circulation only Q1FY2022 Results Review In-line quarter, healthy outlook Results Review Results Summary: After ending FY2021 on a strong note, Q1FY2022 earnings of broader indices showed a promising start (Nifty/ Sensex companies’ PAT rose 100%/66% y-o-y) in the new fiscal with strong growth momentum on low base. Management commentaries on earnings outlook remained positive, on improving economic activity post second COVID-19 wave and anticipation of strong demand revival. Demand recovery and ramp-up of vaccinations look encouraging. We expect economic activity to increase in the upcoming festive season. Nifty trades at 23x and 20x EPS based on FY2022E/FY2023E EPS, at a premium to mean average. Valuation gap between large and mid-caps has shrunk, we advise investors to focus on stocks with strong earnings growth potential with reasonable valuation. High-conviction investment ideas: o Large-caps: Infosys, ICICI Bank, M&M, L&T, UltraTech, SBI, HDFC Ltd, Godrej Consumer Products, Divis Labs and Titan. o Mid-caps: NAM India, BEL, Gland Pharma, Dalmia Bharat, Laurus Labs, Max Financial Services, LTI. o Small-caps: TCI Express, Kirloskar Oil, Suprajit Engineering, Repco Home Finance, PNC Infratech, Mahindra Lifespaces, Birlasoft. After ending FY2021 on a strong note, Q1FY2022 corporate earnings of broader indices showed a promising start with continued strong growth momentum on the low base of Q1FY2021, though it was along the expected lines. -

Press Release by BP and Reliance Industries Limited

Castrol India Limited Tel: (022) 6698 4100 Technopolis Knowledge Par1<, Fax: (022) 6698 4101 Mahakali Caves Road, www.castrol.co.in ~ Castrol / Chakala, Andheri (East), Mumbai - 400 093. CIN L23200MH1979PLC021359 6 August 2019 The Secretary National Stock Exchange of India Ltd The BSE Limited Exchange Plaza Phiroze Jeejeebhoy Towers Bandra Kurla Complex Dalal Street Plot No. C/1, 'G' Block Mumbai 400 001 Bandra {East) Mumbai 400051. Scrip Code: 500870 Symbol : CASTROLIND Dear Sirs, Sub: Press Release by BP and Reliance Industries Limited BP and Reliance Industries Limited today announced that they have agreed to form a new joint venture that will include a retail service station network and aviation fuels business across India. Lubricants manufactured by Castrol India Limited will also be available across the venture's network. Attached is a press release from BP and Reliance Industries Limited to this effect. This is for your information and dissemination. Yours faithfully, For Castrol India Limited Chandana Dhar Company Secretary and Compliance Officer Encl. As above Customer Service Toll Free No.: 1800 222 100 / 1800 209 8100 0 Reliance Industries Limited press release 6 August 2019 Reliance and BP to create major world-class fuels partnership for India’s fast-growing market • Expanding partnership into fuel and convenience retailing and aviation fuels in India • Rapidly expanding the existing nationwide network of fuel retailing outlets to 5,500 • Delivering high-quality, modern service for India’s consumers, with differentiated sites, fuels, and convenience offers. BP and Reliance Industries Limited (RIL) today announced that they have agreed to form a new joint venture that will include a retail service station network and aviation fuels business across India. -

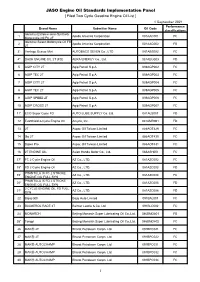

JASO Engine Oil Standards Implementation Panel

JASO Engine Oil Standards Implementation Panel [ Filed Two Cycle Gasoline Engine Oil List ] 1 September 2021 Performance Brand Name Submitter Name Oil Code classifications Idemitsu Extreme semi-Synthetic 1 Apollo America Corporation 001AAC001 FC Motorcycle Oil FC 2T Idemitsu Select Motorcycle Oil FB 2 Apollo America Corporation 001AAC002 FB 2T 3* Vantage Beaver Mini AUTOBACS SEVEN Co., LTD 081ABS002 FC 4* DASH ENGINE OIL 2T (FD) AERA ENERGY Co., Ltd. 081AEG003 FD 5 AGIP CITY 2T Agip Petroil S.p.A. 039AGP002 FC 6 AGIP TEC 2T Agip Petroil S.p.A. 039AGP003 FC 7 AGIP CITY 2T Agip Petroil S.p.A. 039AGP004 FC 8 AGIP TEC 2T Agip Petroil S.p.A. 039AGP005 FC 9 AGIP SPEED 2T Agip Petroil S.p.A. 039AGP006 FC 10 AGIP CROSS 2T Agip Petroil S.p.A. 039AGP007 FC 11* ECO Super Cycle FD AUTO LUBE SUPPLY Co. Ltd. 081ALS001 FD 12 EvoShield 2-Cycle Engine Oil Amyris, Inc. 001AMR001 FD 13 2T Aspac Oil Taiwan Limited 886AOT429 FC 14 Go 2T Aspac Oil Taiwan Limited 886AOT430 FC 15 Super Pro Aspac Oil Taiwan Limited 886AOT431 FC 16 2T ENGINE OIL Asian Honda Motor Co., Ltd. 066ASH001 FC 17* FC 2 Cycle Engine Oil AZ Co., LTD. 081AZC002 FC 18* FD 2 Cycle Engine Oil AZ Co., LTD. 081AZC003 FD PHANTULA IX FC 2 STROKE 19* AZ Co., LTD. 081AZC004 FC ENGINE OIL FULL SYN PHANTULA IX FD 2 STROKE 20* AZ Co., LTD. 081AZC005 FD ENGINE OIL FULL SYN 2 CYCLE ENGINE OIL FD FULL 21* AZ Co., LTD. 081AZC006 FD SYN 22 Bajaj GDI Bajaj Auto Limited 091BAL001 FC 23 BALMEROL RACE 2T Balmer Lawrie & Co. -

Annual Report 2015

Castrol India Limited Annual Report 2015 UNLEASHING THE POWER OF CORPORATE INFORMATION Board of Directors Bankers Mr. S. M. Datta Deutsche Bank Chairman HDFC Bank Ltd. Mr. R. Gopalakrishnan Independent Director The Hong Kong & Shanghai Banking Corporation Ltd. Mr. Uday Khanna State Bank of India Independent Director Citibank N.A. Mr. Ralph Hewins DBS Bank Ltd. Nominee Director J P Morgan Chase Bank N.A. Mr. Peter Weidner Nominee Director Registered Office Mr. Sashi Mukundan Nominee Director Technopolis Knowledge Park Mahakali Caves Road, Mr. Omer Dormen Managing Director Chakala, Andheri (East), Mumbai 400 093, INDIA. Ms. Rashmi Joshi Director - Finance (Chief Financial Officer) CIN: L23200MH1979PLC021359 Mr. Jayanta Chatterjee Telephone: 022-6698 4100 Director - Supply Chain Website: www.castrol.co.in Mr. Sandeep Deshmukh Company Secretary Registrar & Share Transfer Agents TSR Darashaw Limited Auditors Unit: Castrol India Limited 6-10, Haji Moosa Patrawala Industrial Estate, M/s. SRBC & Co. LLP 20, Dr. E. Moses Road, Mahalaxmi, Chartered Accountants Mumbai 400 011, INDIA. Telephone: 022-6656 8484 Website: [email protected] CONTENTS Financial Highlights 10 Board’s Report 13 Management Discussion & Analysis Report 44 Corporate Governance Report 55 Business Responsibility Report 68 Auditors’ Report 78 Balance Sheet 82 Statement of Profit and Loss83 Cash Flow Statement 84 Notes to Financial Statements 86 01 BOARD OF DIRECTORS Seated (l to r): Peter Weidner, Nominee Director; S. M. Datta, Chairman; R. Gopalakrishnan, Independent Director; -

Disinvestment of Psus 179. Shri Shivakumar C. Udasi: Shri

• GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF INVESTMENT AND PUBLIC ASSET MANAGEMENT LOKSABHA UNSTARRED QUESTION NO. 179 TO BE ANSWERED ON MONDAY, NOVEMBER 18, 2019 KARTIKA 27,1941 (SAKA) Disinvestment of PSUs 179. Shri Shivakumar C. Udasi: Shri Muraleedharan: Shri Rajeshbhai Chudasama: Shri Malook Nagar: Will the Minister of FINANCE be pleased to state: (a)the details of the target set by the Government / Department of Investment and Public Asset Management to raise the amount through disinvestment drive during the financial year along with the steps taken to accelerate the disinvestment process; (b)whether the Government has taken any decision on BPCL and other Public Sector Undertakings (PSUs)/ State-owned companies for disinvestment and if so, the details thereof and the reasons therefore; (c)the details of proceeds received due to disinvestment of PSUs, year-wise along with the details of PSUs where disinvestment took place, either fully or partially including the percentage of stake sold; (d)whether the PSUs sold were profit-making or loss-making and if so, the details thereof along with the number of PSUs which were converted from the stature of PSU to private and the reasons for selling profit-making PSUs; (e)the efforts made by the Government to restructure and re-finance the undertakings to revive before taking a decision of disinvestment; and (f) the details of provisions being made by the Government to tide over the loss incurred by loss-making telecom Government undertakings like BSNL, MTNL etc? -------- • ANSWER THE MINISTER OF STATE IN THE MINISTRY OF FINANCE (SHRI ANURAG SINGH THAKUR) a) The Budget target for disinvestment during 2019-20 has been set at Rs. -

Factsheet March 2016

Crosses `100 Crores* BOI AXA SHORT TERM INCOME FUND . AVERAGE MATURITY AND MODIFIED DURATION The fund is currently maintaining a Modified Duration of 0.56 and an Average Maturity of 0.90 years (as of March 31, ‘16) Hence, the fund is well positioned to take advantage of the middle segment of the yield curve where we see maximum value Why invest ASSET QUALITY in BOI AXA The fund is maintaining a judicious mix between Corporate Bonds, Money Market instruments and Government Securities This enables the fund to earn accrual income from its Corporate Bonds while also benefiting from tactical trading Short Term opportunities through G-Secs Income CREDIT QUALITY The fund is currently is 83.31% invested in G-Secs, AAA and A1+ rated instruments Fund? It is also ~2.33% invested in Unrated instruments in order to enhance the portfolio yield The fund’s portfolio yield is currently at 9.66% (as of March 31, ‘16) Refer Pg. No.3 for Product Labelling *As on 06/04/2016 Facts in Figures Monthly fund analysis and market reviews March 2016 Fund Manager’s Views The last repo rate cut by RBI appears to be one of last few rate cuts in this interest rate easing cycle. A further rate cut from here has to be driven by fall in inflation more than anything else. To explain it better, RBI has forecasted CPI inflation to be around 5% for this financial year. At the same time RBI intends to Alok Singh maintain a real positive interest rate of 1.5%-2%. -

Mf Movers & Shakers

MF MOVERS & SHAKERS MARCH 2021 DART Research Tel: +91 22 40969700 E-mail: [email protected] April 12, 2021 April 12, 2021 2 Top Five Buys & Sells Top Ten MF's March 2021 3 Top Five Buys & Sells of Top MFs for the month of March 2021 No of Shares No of Shares Highest Increase in Exposure Names Bought in Highest Decrease in Exposure (by nos of shares) Bought in (by nos of shares) March 2021 March 2021 Bharat Petroleum Corporation 4,547,448 The Indian Hotels 9,826,101 Steel Authority Of India 1,995,000 Vedanta 2,988,456 Axis MF Torrent Power 1,889,278 Tata Motors 2,574,406 Suryoday Small Finance Bank 1,887,039 EPL 2,572,954 Mahindra & Mahindra Financial Services 1,644,663 Wipro 2,226,978 Bank Of Baroda 36,590,405 Vodafone Idea 21,490,000 Steel Authority Of India 9,632,297 Vedanta 7,799,200 Birla SL MF National Aluminium 7,524,001 GMR Infrastructure 4,837,500 IDFC First Bank 3,122,875 Ashok Leyland 4,252,923 State Bank Of India 2,870,884 Bharti Airtel 3,662,791 Motherson Sumi Systems 6,769,756 Vodafone Idea 8,750,000 GAIL 3,502,259 Oil & Natural Gas Corporation 8,463,632 DSP BR MF Welspun Corp 2,559,989 Vedanta 7,199,288 ITC 2,520,668 Hindalco Industries 2,468,290 Prism Johnson 2,389,002 ICICI Prudential Life Insurance 2,343,372 Max Healthcare Institute 21,422,593 Vodafone Idea 18,830,000 Indian Railway Finance Corporation 13,939,480 Siti Networks 17,967,767 HDFC MF Oil & Natural Gas Corporation 7,327,497 Power Grid Corporation Of India 13,081,255 Varroc Engineering 6,735,218 State Bank Of India 12,478,973 Bharti Airtel 5,846,094