Industrial Potential Survey Report Palakkad District 2014

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

To Read / Download the Order

WWW.LIVELAW.IN IN THE HIGH COURT OF KERALA AT ERNAKULAM PRESENT THE HONOURABLE MR. JUSTICE K.HARIPAL WEDNESDAY, THE 14TH DAY OF JULY 2021 / 23RD ASHADHA, 1943 BAIL APPL. NO. 3850 OF 2021 CRIME NO.26/2020 OF EE & ANSS, MALAPPURAM PETITIONERS/ACCUSED: 1 MIDHUN AGED 30 YEARS,SON OF PURUSHAN, KOCHUPARAMBIL HOUSE, PANAYIKULAM, ALANGAD P O, ERNAKULAM DISTRICT, PIN 683502 2 SUJITH P U AGED 30 YEARS, SON OF UNNI,PUTHANVEETIL, EDAYAR P O, ERNAKULAM DISTRICT, PIN 686662 BY ADV K.NIRMALAN RESPONDENTS/STATE: 1 STATE OF KERALA STATE OF KERALA, REPRESENTED BY THE PUBLIC PROSECUTOR, HIGH COURT OF KERALA, HIGH COURT P O, ERNAKULAM 682 031 ERNAKULAM, PIN - 682031 2 INSPECTOR OF EXCISE INSPECTOR OF EXCISE, ENFORCEMENT AND ANTI NARCOTIC SQUAD, MALAPPURAM, REPRESENTED BY THE PUBLIC PROSECUTOR, HIGH COURT OF KERALA, HIGH COURT P O, ERNAKULAM BY PUBLIC PROSECUTOR SMT.SRREJA V. THIS BAIL APPLICATION HAVING COME UP FOR ADMISSION ON 5.07.2021,ALONG WITH CRL.M.C.NOS.2712/2021 AND 2901/2021, THE COURT ON 14.07.2021 DELIVERED THE FOLLOWING: WWW.LIVELAW.IN CRL.M.C.2712 & 2901 OF 2021 & BAIL APPL.NO.3850 OF 2021 -2- IN THE HIGH COURT OF KERALA AT ERNAKULAM PRESENT THE HONOURABLE MR. JUSTICE K.HARIPAL WEDNESDAY, THE 14TH DAY OF JULY 2021 / 23RD ASHADHA, 1943 CRL.MC NO. 2712 OF 2021 CRIME NO.26/2020 OF EE & ANSS, MALAPPURAM PETITIONERS/ACCUSED 2 & 3: 1 MIDHUN AGED 30 YEARS S/O PURUSHAN, KOCHUPARAMBIL HOUSE, PANAYIKKULAM, ALANGADE P.O.ERNAKULAM DISTRICT-680 502. 2 SUJITH P.U, AGED 30 YEARS S/O UNNI, PUTHANVEETIL, EDAYAR P.O.ERNAKULAM DISTRICT- 686 662. -

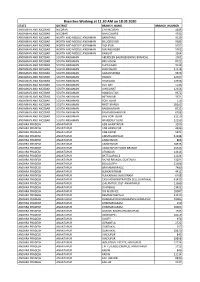

Payment Locations - Muthoot

Payment Locations - Muthoot District Region Br.Code Branch Name Branch Address Branch Town Name Postel Code Branch Contact Number Royale Arcade Building, Kochalummoodu, ALLEPPEY KOZHENCHERY 4365 Kochalummoodu Mavelikkara 690570 +91-479-2358277 Kallimel P.O, Mavelikkara, Alappuzha District S. Devi building, kizhakkenada, puliyoor p.o, ALLEPPEY THIRUVALLA 4180 PULIYOOR chenganur, alappuzha dist, pin – 689510, CHENGANUR 689510 0479-2464433 kerala Kizhakkethalekal Building, Opp.Malankkara CHENGANNUR - ALLEPPEY THIRUVALLA 3777 Catholic Church, Mc Road,Chengannur, CHENGANNUR - HOSPITAL ROAD 689121 0479-2457077 HOSPITAL ROAD Alleppey Dist, Pin Code - 689121 Muthoot Finance Ltd, Akeril Puthenparambil ALLEPPEY THIRUVALLA 2672 MELPADAM MELPADAM 689627 479-2318545 Building ;Melpadam;Pincode- 689627 Kochumadam Building,Near Ksrtc Bus Stand, ALLEPPEY THIRUVALLA 2219 MAVELIKARA KSRTC MAVELIKARA KSRTC 689101 0469-2342656 Mavelikara-6890101 Thattarethu Buldg,Karakkad P.O,Chengannur, ALLEPPEY THIRUVALLA 1837 KARAKKAD KARAKKAD 689504 0479-2422687 Pin-689504 Kalluvilayil Bulg, Ennakkad P.O Alleppy,Pin- ALLEPPEY THIRUVALLA 1481 ENNAKKAD ENNAKKAD 689624 0479-2466886 689624 Himagiri Complex,Kallumala,Thekke Junction, ALLEPPEY THIRUVALLA 1228 KALLUMALA KALLUMALA 690101 0479-2344449 Mavelikkara-690101 CHERUKOLE Anugraha Complex, Near Subhananda ALLEPPEY THIRUVALLA 846 CHERUKOLE MAVELIKARA 690104 04793295897 MAVELIKARA Ashramam, Cherukole,Mavelikara, 690104 Oondamparampil O V Chacko Memorial ALLEPPEY THIRUVALLA 668 THIRUVANVANDOOR THIRUVANVANDOOR 689109 0479-2429349 -

Accused Persons Arrested in Palakkad District from 28.03.2021To03.04.2021

Accused Persons arrested in Palakkad district from 28.03.2021to03.04.2021 Name of Name of the Name of the Place at Date & Arresting Court at Sl. Name of the Age & Cr. No & Sec Police father of Address of Accused which Time of Officer, which No. Accused Sex of Law Station Accused Arrested Arrest Rank & accused Designation produced 1 2 3 4 5 6 7 8 9 10 11 Chirakkad colony, produced 319/2021 U/S Sreejith, SI of Sanmughesh Kannan 33/m Kunnathurmeedu, South PS 30/3/2021 South PS before the 379 IPC Police 1 Palakkad Court 318/2021 U/S Chelambathu house, Sreejith, SI bail from Jayakrishnan Rajan 43/m 15 ( C) of South PS 28/3/21 South PS Pandarakavu, of Police station Abakri Act 2 Palakkad 318/2021 U/S Mangangam house, Sreejith, SI bail from Ramadas Ponnu 32/m 15 ( C) of South PS 28/3/21 South PS Pandarakavu, of Police station Abakri Act 3 Palakkad 318/2021 U/S Mangangam house, Sreejith, SI bail from Prajith Ramankutty 32/m 15 ( C) of South PS 28/3/21 South PS Pandarakavu, of Police station Abakri Act 4 Palakkad 320/2021 U/S Noorani, Vithunni, Sreejith, SI bail from Rajamani 25/m 279, 185 MV South PS 30/3/2021 South PS Palakkad of Police station 5 Santhosh Act Cherumkulam 323/21 U/s 15 Sreejith, SI bail from Mohanan 28/m house, Ganesagiri, ( C) of Abkari South PS 31/3/2021 South PS of Police court 6 Sham mohan Shoaranur act 323/21 U/s 15 Sreejith, SI bail from Balakrishnan 31/m Vilayankad house, ( C) of Abkari South PS 31/3/21 South PS of Police court 7 Viswambharan Parali, Ottapalam act 324/2021 u/s Sreejith, SI bail from Sajerali 28/m 118 € -

Name of District : Palakkad Phone Numbers PS Contact LAC Name of Polling Station Name of BLO in Charge Designation Office Address NO

Palakad District BLO Name of District : Palakkad Phone Numbers PS Contact LAC Name of Polling Station Name of BLO in charge Designation Office address NO. Address office Residence Mobile Gokulam Thottazhiyam Basic School ,Kumbidi sreejith V.C.., Jr Health PHC Kumbidi 9947641618 49 1 (East) Inspector Gokulam Thottazhiyam Basic School sreejith V.C.., Jr Health PHC Kumbidi 9947641619 49 2 ,Kumbidi(West) Inspector Govt. Harigan welfare Lower Primary school Kala N.C. JPHN, PHC Kumbidi 9446411388 49 3 ,Puramathilsseri Govt.Lower Primary school ,Melazhiyam Satheesan HM GLPS Malamakkavu 2254104 49 4 District institution for Education and training Vasudevan Agri Asst Anakkara Krishi Bhavan 928890801 49 5 Aided juniour Basic school,Ummathoor Ameer LPSA AJBS Ummathur 9846010975 49 6 Govt.Lower Primary school ,Nayyur Karthikeyan V.E.O Anakkara 2253308 49 7 Govt.Basic Lower primary school,Koodallur Sujatha LPSA GBLS koodallur 49 8 Aided Juniour Basic school,Koodallur(West Part) Sheeja , JPHN P.H.C kumbidi 994611138 49 9 Govt.upper primary school ,Koodallur(West Part) Vijayalakshmi JPHN P.H.C Kumbidi 9946882369 49 10 Govt.upper primary school ,Koodallur(East Part) Vijayalakshmi JPHN P.H.C Kumbidi 9946882370 49 11 Govt.Lower Primary School,Malamakkavu(east Abdul Hameed LPSA GLPS Malamakkavu 49 12 part) Govt.Lower Primary School.Malamakkavu(west Abdul Hameed LPSA GLPS Malamakkavu 49 13 part) Moydeenkutty Memmorial Juniour basic Jayan Agri Asst Krishi bhavan 9846329807 49 14 School,Vellalur(southnorth building) Kuamaranellur Moydeenkutty Memmorial Juniour -

Vadanamkurussi Rob Sia Draft Report English

SOCIAL IMPACT ASSESSMENT STUDY DRAFT REPORT LAND ACQUISITION FOR THE CONSTRUCTION OF RAILWAY OVER BRIDGE AT VADANAMKURISSI IN ONGALLUR VILLAGE, PALAKKAD DISTRICT Requiring Body ROADS AND DEVELOPMENT CORPORATION OF KERALA LTD (A Government of Keral Undertaking) Mahakavi Vailoppilli Roiad Palarivattam, Kochi – 682025 Phone: 0484-2338205 SIA Unit Rajagiri College of Social Sciences Rajagiri P.O Kalamassery Pin: 683104 Ph: 0484 2911330 – 332/2550785 [email protected] www.rajagirioutreach.org 16.05.2019 SIA - Land Acquisition for Construction of Railway Over Bridge at Vadanamkurissi in Palakkad District. CONTENTS CHAPTER 1 - EXECUTIVE SUMMARY 1.1 Project and public purpose 1.2 Location 1.3 Size and attributes of land acquisition 1.4 Alternatives considered 1.5 Social impacts 1.6 Mitigation measures CHAPTER 2 - DETAILED PROJECT DESCRIPTION 2.1 Background of the project, including developers background and governance/ management structure 2.2 Rationale for project including how the project fits the public purpose criteria listed in the Act 2.3 Details of project size, location, capacity, outputs, production targets, costs and risks 2.4 Examination of alternatives 2.5 Phases of the project construction 2.6 Core design features and size and type of facilities 2.7 Need for ancillary infrastructural facilities 2.8 Work force requirements (temporary and permanent) 2.9 Details of social impact assessment/ environment impact assessment if already conducted and any technical feasibility reports 2.10 Applicable legislations and policies CHAPTER 3 –TEAM COMPOSITION APPROACH, METHODOLOGY AND SCHEDULE OF THE SOCIAL IMPACT ASSESSMENT 3.1 List of all team members with qualification 3.2 Description and rationale for the methodology and tools used to collect information for the social impact assessment 3.3 Sampling methodology used 3.4 Overview of information/ data sources used 3.5 Schedule of consultations with key stakeholders and brief description of public hearings conducted SIA - Land Acquisition for Construction of Railway Over Bridge at Vadanamkurissi in Palakkad District. -

Social Exclusion of Ravuthar Community: a Case Study

International Journal of Science and Research (IJSR) ISSN: 2319-7064 ResearchGate Impact Factor (2018): 0.28 | SJIF (2018): 7.426 Social Exclusion of Ravuthar Community: A Case Study Mohammed Rishad K P M.Phil Scholar, Gandhigram Rural Institute (Deemed to be University) Centre for Applied research Dindigul, Tamil Nadu, India Abstract: India, the world’s largest democracy, has a multi-cultural rash that has numerous religious communities. According to the 2011 census, 79.8 percent are practicing Hinduism and 14.2 percent are adheres to Islam, while the remaining 6 percent are other religions. According to Rizvi and Roy (1984), Indian Muslims are not a homogeneous community as it appears in the general perception Muslims are divided based on different religious ideologies, caste differentiation and customary practices. Among the different Muslim communities, Ravuthar is one of the Muslim communities from the South Indian States of Tamil Nadu and Kerala who are socially excluded at a wider. The etymology of the word suggests ‘ravath’ means ‘warriors’. But in reality, the Ravuthar community is facing high discrimination among the Muslim community. The present study is focused on how the Ravuthar community is excluded or discriminated among the Muslim community at Thiruvegappura Panchayat, Palakkad District, and Kerala by using descriptive research design. The researcher has employed an interview guide and case study. From the case studies, the relevant information was collected by the researcher. In the community, they were facing various issues such as stigma discrimination based on their linguistic and spatial. Their representation in any religious or social positions is very less. -

Branches Working at 11.30 AM on 18.05.2020

Branches Working at 11.30 AM on 18.05.2020 STATE DISTRICT BRANCH_NAME BRANCH_NUMBER ANDAMAN AND NICOBAR NICOBAR CAR NICOBAR 4645 ANDAMAN AND NICOBAR NICOBAR NAN COWRIE 4933 ANDAMAN AND NICOBAR NORTH AND MIDDLE ANDAMAN BARATANG 9139 ANDAMAN AND NICOBAR NORTH AND MIDDLE ANDAMAN BILLIGROUND 9385 ANDAMAN AND NICOBAR NORTH AND MIDDLE ANDAMAN DIGLIPUR 5752 ANDAMAN AND NICOBAR NORTH AND MIDDLE ANDAMAN MAYABUNDER 5902 ANDAMAN AND NICOBAR NORTH AND MIDDLE ANDAMAN RANGAT 1564 ANDAMAN AND NICOBAR SOUTH ANDAMAN ABERDEEN BAZAR(EVENING BRANCH) 2001 ANDAMAN AND NICOBAR SOUTH ANDAMAN BRICHGUNJ 8722 ANDAMAN AND NICOBAR SOUTH ANDAMAN CHOULDARI 9138 ANDAMAN AND NICOBAR SOUTH ANDAMAN DOLLYGUNJ 17178 ANDAMAN AND NICOBAR SOUTH ANDAMAN GARACHARMA 9670 ANDAMAN AND NICOBAR SOUTH ANDAMAN HADDO 12357 ANDAMAN AND NICOBAR SOUTH ANDAMAN HAVELOCK 12358 ANDAMAN AND NICOBAR SOUTH ANDAMAN HUT BAY 5543 ANDAMAN AND NICOBAR SOUTH ANDAMAN JUNGLIHAT 12356 ANDAMAN AND NICOBAR SOUTH ANDAMAN MANGLUTAN 9672 ANDAMAN AND NICOBAR SOUTH ANDAMAN MITHAKARI 9671 ANDAMAN AND NICOBAR SOUTH ANDAMAN PORT BLAIR 156 ANDAMAN AND NICOBAR SOUTH ANDAMAN PROTHRAPUR 18262 ANDAMAN AND NICOBAR SOUTH ANDAMAN RAKSHAVIHAR 8721 ANDAMAN AND NICOBAR SOUTH ANDAMAN RAMAKRISHNAPUR 6288 ANDAMAN AND NICOBAR SOUTH ANDAMAN SME PORT BLAIR 61250 ANDAMAN AND NICOBAR SOUTH ANDAMAN WIMBERLY GUNJ 12359 ANDHRA PRADESH ANANTAPUR ADB ANANTAPUR 3200 ANDHRA PRADESH ANANTAPUR ADB HINDUPUR 4696 ANDHRA PRADESH ANANTAPUR ADB KADIRI 5871 ANDHRA PRADESH ANANTAPUR AMMAVARIPALLE 61398 ANDHRA PRADESH ANANTAPUR ANANTAPUR 806 ANDHRA -

Sl. No Branch Name Branch Code Category U/Su/R Ural

ANNEXURE-A LIST OF BRANCHES UNDER BRANCHES UNDER RBO-IV,PALAKKAD BRANCH U/SU/R SL. NO BRANCH NAME CODE CATEGORY URAL REGION Area(in sqft) 1 RBO 4 PALAKKAD 14923 C Urban 3721 RBO 4 Palakkad 2 PALGHAT A D B 1660 C Urban 5803 RBO 4 Palakkad 3 T B ROAD, PALAKKAD 70177 C Urban 7513 CHITTOOR TOWN, Semi RBO 4 Palakkad 4 PALAKKAD 70178 C Urban 5860 Semi RBO 4 Palakkad 5 MANKARA 2237 C Urban 2000 RBO 4 Palakkad 6 OLAVAKKOT 2245 C Urban 4000 RBO 4 Palakkad 7 CIVIL STATION PALGHAT 4925 C Urban 2000 Semi RBO 4 Palakkad 8 SSI KANJIKODE 6640 C Urban 2360 Semi RBO 4 Palakkad 9 KERALASSERY 7624 C Urban 2000 Semi RBO 4 Palakkad 10 PUDUPPARIYARAM 8245 C Urban 2317 RBO 4 Palakkad 11 PALGHAT TOWN 8658 C Urban 2851 MERCY COLLEGE RBO 4 Palakkad 12 CAMPUS 9157 C Urban 2340 Semi RBO 4 Palakkad 13 CHITTOOR 10706 C Urban 1900 Semi RBO 4 Palakkad 14 MUTHALAMADA 11928 C Urban 1935 RBO 4 Palakkad 15 KUNNATHURMEDU 12861 C Urban 1925 RBO 4 Palakkad 16 VADAKKANTHARA 12862 C Urban 2146 RBO 4 Palakkad 17 VICTORIA COLLEGE 12886 C Urban 1587 RBO 4 Palakkad 18 MEENAKSHIPURAM 12888 C Rural 1450 RBO 4 Palakkad 19 NRI PALAKKAD 14465 C Urban 2879 Semi RBO 4 Palakkad 20 KONGAD 14966 C Urban 1985 RBO 4 Palakkad 21 MALAMPUZHA ROAD 16078 C Urban 2619 RBO 4 Palakkad 22 MARUTHARODE 16079 C Urban 2853 Semi RBO 4 Palakkad 23 KODUVAYUR TOWN 17032 C Urban 2158 Semi RBO 4 Palakkad 24 NEMMARA 17034 C Urban 2676 Semi RBO 4 Palakkad 25 KOLLENGODE 18319 C Urban 2990 Semi RBO 4 Palakkad 26 ELAPPULLY 18677 C Urban 617 RBO 4 Palakkad 27 SEKHARIPURAM 18974 C Urban 1750 RBO 4 Palakkad 28 sbiINTOUCH -

Accused Persons Arrested in Palakkad District from 08.11.2015 to 14.11.2015

Accused Persons arrested in Palakkad district from 08.11.2015 to 14.11.2015 Name of the Name of Name of the Place at Date & Court at Sl. Name of the Age & Cr. No & Sec Police Arresting father of Address of Accused which Time of which No. Accused Sex of Law Station Officer, Rank Accused Arrested Arrest accused & Designation produced 1 2 3 4 5 6 7 8 9 10 11 Crime No. 1579/15 U/s Erattukulam, Kannadi, Shiju Ebraham 1 Vinesh Neelakandan 36 Town South 08.11.2015 143, 147, 341, Town South Bail by Police Palakkad SI of Police 323, 294 (b), r/w 149 IPC Crime No. Pazhampalliyil House, 1602/15 U/s Koppakeyam PO, 10/11/2015 Prasanth Kumar 2 Santhosh Thankachan PP 27 IMA Junction 118 (e) of KP Town South Bail by Police Chennpara, at 23.55 hrs Addl SI of Police Act and 185 of Mundakayam, Idukki MV Act Kurakkampotta, Crime No. Vijayan @ Ramesh Addl. 3 Sahadevan 35 Erattakulam, Chittur, Sub Jail Chittur ########## 1574/15 U/s Town South Remanded Robert Vijayan SI of Police Palakkad 379 IPC Karthika Nivas, AR Crime No. Balasubraman Nair Colony, KSRTC Link 1605/15 U/s 15 Shiju Ebraham 4 Muthuswamy 47 ########## Town South Bail by Police ian Kunnathurmedu, Road (C ) of Abkari SI of Police Palakkad Act 1817/15 U/s Perumthuruthi house, Rajappan C SI Bailed by 5 Rahul Ramachandran 21 Male Sakunthala JN ########## 279, 3(1) r/w Traffic P.S Dhoni, Palakkad of Police police 181 MV Act Valathottil veedu, 1814/15 U/s Rajappan C SI Bailed by 6 Usman Chekkutty molla 54 Male Kalladikkode, Traffic p.s ########## Traffic P.S 279, 337 IPC of Police police Palakkad Chimbalakkode, -

35/1 Vallapuzha Village, Pattambi Taluk, Palakkad District, Kerala Quarry Area: 0.7099 Ha (70.99 Ares) Non Forest - Private Land

APPLICATION FOR ENVIRONMENTAL CLEARANCE FOR GRANITE BUILDING STONE QUARRY PROJECT (As per EIA Notification 2006 and amendments thereof) Form-IM, PFR & EMP Proponent/Applicant SRI. K. SUKUMARAN President OTTAPPALAM TALUK KARINKAL QUARRY OPERATORS INDUSTRIAL CO-OPERATIVE SOCIETY LIMITED Vadanamkurussi Palakkad District (D), Kerala – 679121 Email ID: [email protected] Phone No: 9846 883 731, 9846 959 618 Site at Re. Survey No. : 35/1 Vallapuzha Village, Pattambi Taluk, Palakkad District, Kerala Quarry Area: 0.7099 Ha (70.99 Ares) Non Forest - Private Land Prepared by Hareesh G. Thampy 905-D, Sankarnagar, Kaimanam P. O., Thiruvananthapuram, Kerala RQP/BNG/296/2013/A Mobile : 9387 838 782 1 TABLE OF CONTENTS Sl. No. DESCRIPTION Page No. I FORM – IM 4-7 II CHECKLIST FOR MINING PROJECTS 8-19 III QUESTIONNAIRE FOR MINING PROJECTS 20-22 IV PRE-FEASIBILITY REPORT 23-41 1. Executive Summary 24 2. Introduction of the Project 26 3. Project Description 29 4. Site Analysis 34 5. Planning Brief 36 6. Proposed Infrastructures 38 7. Rehabilitation & Resettlement (R & R) Plan 40 8. Project Schedule & Cost Estimates 40 9. Analysis of the Proposal (Final Recommentation) 41 V ENVIRONMENTAL MANAGEMENT PLAN & CSR 42-65 1. Introduction of the Project/Proponent 43 2. Details of the Project 43 3. Baseline Environment 47 4. Environmental Management Plan 50 5. Safety in Blasting 56 6. Mine Closure Plan 56 7. Risk Assessment 58 8. Disaster Management Plan 59 9. Occupational Health & Safety 60 10. Environmental Monitoring Program 61 11. Social (Corporate) Responsibilty 64 12. Conslusion 65 2 Sl. No. DESCRIPTION Page No. ANNEXURE 1. -

Palakkad PALAKKAD

Palakkad PALAKKAD / / / s Category in s s e e Final e Y which Y Reason for Y ( ( ( Decision in 9 his/her 9 Final 9 1 1 appeal 1 - - house is - Decision 6 3 1 - - (Increased - 0 included in 1 (Recommen 1 3 3 relief 3 ) ) ) Sl Name of disaster Ration Card the Rebuild ded by the Relief Assistance e e o o o e r Taluk Village r amount/Red r N N N o No. affected Number App ( If not o Technically Paid or Not Paid o f f f uced relief e e in the e Competent b b b amount/No d Rebuild App d Authority/A d e e e l l change in a Database fill a ny other m e e i relief p p the column a reason) l p p amount) C A as `Nil' ) A 1 2 3 4 5 6 7 8 9 10 11 12 1 Palakkad Akathethara T M SURENDREN 1946162682 yes Paid 2 Palakkad Akathethara DEVU 1946022862 yes Paid 3 Palakkad Akathethara PRASAD K 1946022923 yes Paid 4 Palakkad Akathethara MANIYAPPAN R 1946022878 yes Paid 5 Palakkad Akathethara SHOBHANA P 1946021881 yes Paid Not Paid 6 Palakkad Akathethara Seetha 1946022739 yes Duplication 7 Palakkad Akathethara SEETHA 1946022739 yes Paid 8 Palakkad Akathethara KRISHNAVENI K 1946158835 yes Paid 9 Palakkad Akathethara kamalam 1946022988 yes Paid 10 Palakkad Akathethara PRIYA R 1946132777 yes Paid 11 Palakkad Akathethara CHELLAMMA 1946022421 yes Paid Page 1 Palakkad 12 Palakkad Akathethara Chandrika k 1946022576 yes Paid 13 Palakkad Akathethara RAJANI C 1946134568 yes Paid KRISHNAMOORT 14 Palakkad Akathethara 1946022713 yes Paid HY N 15 Palakkad Akathethara Prema 1946023035 yes Paid 16 Palakkad Akathethara PUSHPALATHA 1946022763 yes Paid 17 Palakkad Akathethara KANNAMMA -

Kiifb Newsletter Kiifb Newsletter

KIIFB NEWSLETTER Vol 1. Issue 12.1 Defining the Future Our Chairman Shri. Pinarayi Vijayan Hon. Chief Minister Approved Projects as on 28/11/2018 Our Vice Chairman Dr. T M Thomas Isaac Hon. Minister for Finance Smt. Anie Jula Thomas, Joint Fund Manager, KIIFB handing over the first series of Pravasi Chitty Bond Certificates to Smt. M. T. Sujatha, AGM NRI Business Centre, KSFE Ltd. From the CEO’s desk.......... 4. The technicalities involved to release a Chital number, should the client be unable The highlight of the last fortnight was the auction held for the online chits for NRIs on 23rd to successfully effect the subscription in November 2018. In this issue, we would like to favour of another prospective client. trace the journey that has led to this wonderful 5. Registering the Chit with the live system of achievement. the Registration Department (CORAL) 6. Conversion of the money realized through The whole process was watched with chits into Bonds issued by KIIFB eagerness and enthusiasm by our Honourable Minister Dr. Thomas Isaac in a press meet at 7. A Financial Payment System for put Thiruvananthapuram. The Chairman, KSFE options periodically from the Bonds Shri. Peelipose Thomas and Sri. Purushothaman, issued by KIIFB so that KSFE can pay their Managing Director, KSFE were present with him commitments to Chit customers in time. along with several senior Board Members of 8. Integration of the subscription modules KSFE. There was considerable excitement in with systems of Exchange Houses the air. As our entire team watched with bated 9. Online processing for different types of breath, Ajeesh of UAE made history and became Securities the first auction winner in the lot.