Private and Confidential Disclaimer

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Euroletter 1 19-3

EURO #01-2019 LETTER Internal memo of the WFIS Europe GA IN MALTA 2019 WFIS INVITATION WORKSHOP’18 SUMMER CAMP IN RUSSIA 2019 EUROCAMP 2018 EURO LETTER #01-2019 MEMBERS AUSTRIA Sezione Scout di Gela Scouts of Europa Assoraider WORLD FEDERATION Fedarazione Italiana di Scautismo Raider OF INDEPENDENT BELGIUM SG-ISG SCOUTS - EUROPE O KOSOVO CZECH REPUBLIC National Scout Center of Kosovo WFIS-Europe is a SKAUT - cesky skauting ABS LATVIA Scout organization for Svaz skautu a skautek Ceske Republik Latvijas Kristigie Skauti independent scouts. Skaut S.S.V. We meet in camps, MALTA DENMARK leadertraining and Baden Powell Scouts of Malta Baden-Powell Scouts of Denmark jamborees. ROMANIA (De Gule Speijdere i Danmark) WFIS-Europe was Asociatia Cercetasilor Traditionali din Romania created in 1999 and is an FRANCE ACT-RO organisation under Scouts de Chavagnes WFIS World-Wide. RUSSIAN FEDERATION GERMANY Every scout organisation Russian Union of Scouts Bund Europäischer St. Georgs can join WFIS-Europe if SPAIN Pfadfinderinnen und - Pfadfinder they are not member of Asociacion Scout Independiente De Madrid Bund Unabhängiger Pfadfinder another world organisation. Associació Catalana de Scouts If you want to know more CP Dreieich Grupo Scout Alpha about WFIS-Europe, Deutscher Pfadfinder Bund e.V. gegr. 1911 Asociation Juvenil Groupo Scout please contact one of the EPSG Baunach Independiente Gilwell members of the commitee. Europäischer Pfadfinderbund - Georgsritter e.V. Federation Scout de la Communidad Valenciana Freier Pfadfinderbund Asgard Scout Independientes del Principado de Asturias Freier Pfadfinderbund St.Georg Grupo Scout San Pío X Independent Scout Association COMMITTEE Asociación Grupo Scout Alcazaba Solmser Pfadfinderschaft Grupo Scout Magma 1. -

School Project Cantonian High School Fairwater Road, Fairwater, Cardiff CF5 3JR Wales

School Project Cantonian High School Fairwater Road, Fairwater, Students exchange Cardiff CF5 3JR 96/97 Wales - United Kingdom www.cantonian.cardiff.sch.uk Hakumäen koulu Comenius 96/97 Koulunpolku, 4 Comenius 97/98 39500 Ikaalinen Comenius 98/99 Finland Eurocamp 1999 (Vienna) www.ikaalinen.fi Comenius 96/97 Comenius 97/98 Comenius 98/99 Eurocamp 1999 (Vienna) Eurocamp 2000 (Bilbao) Franz Jonas Europa Hauptschule Eurocamp 2001 Deublergasse, 21 (Ikaalinen) 1210 Vienna Eurocamp 2002 (Bilbao) Austria Eurocamp 2003 (Vienna) www.europaschule.at Eurocamp 2004 (Kony) Eurocamp 2005 (Berlin) Comenius 01/02 Comenius 02/03 Comenius 03/04 Scuola Media Galileo Galilei Comenius 96/97 Via Aquileia, 1 Comenius 97/98 20021 Baranzate di Bollate (Milano) Comenius 98/99 Milan Eurocamp 1999 Italy Comenius 97/98 Students exchange Bishop Douglas High School 97/98 Hamilton Road, East Finchley Comenius 98/99 London N2 OSQ Eurocamp 1999 (Vienna) England - United Kingdom Eurocamp 2000 (Bilbao) www.bishopdouglass.barnet.sch.uk Eurocamp 2001 (Ikaalinen) Ecòle Publique de Venarsal Venarsal Comenius 98/99 France Whitmore County Junior School Comenius 98/99 Whitmore Way Comenius 99/00 Basildon Essex SS14 2TP Comenius 00/01 United Kingdom Comenius 01/02 www.whitmorejuniorschool.ik.org Escuola elementare "Italia K2" Comenius 98/99 Fiesso D'Artico Comenius 99/00 Venezia Comenius 00/01 Italia Comenius 01/02 Skola ZŠ Heyrovského Olomouc Comenius 98/99 ZŠ Heyrovského, School Project 33 779 00 Olomouc Czech Republic www.zsheyrovskeho.cz/ Students exchange Liverpool College -

Vehicle Breakdown Insurance Cover

Vehicle Breakdown Insurance Cover Insurance Product Information Document Company: This insurance is administered by Voyager Insurance Services who are authorised and regulated by the Financial Conduct Authority, FRN 305814. Registered Office: Buzzards Hall, Friars Street, Sudbury, Suffolk, CO10 2AA. Registered No: 3251845. Insurer: This insurance is provided by Call Assist Limited and underwritten by Ageas Insurance Limited. Product: Voyager European Breakdown Cover 2021/22 This Insurance Product Information Document is only intended to provide a summary of the main coverage and exclusions, and is not personalised to your specific individual needs in any way. For full and complete terms and conditions, please refer to your Policy Documentation. What is this type of insurance? This vehicle breakdown insurance cover is an insurance policy that provides roadside assistance and recovery when your vehicle unexpectedly suffers a breakdown in the Territorial Limits (UK) or Territorial Limits (EU). What is insured? What is not insured? Roadside Assistance. Any vehicle which is not listed on the Policy Schedule as Home Assist - Assistance at your registered home address or being eligible for breakdown cover. within a one-mile radius/straight line of your registered home address on the course of a trip. Storage charges unless incurred whilst we organise Nationwide Recovery on the course of a trip. repatriation from Europe (area 1, 2 or 3). European Assistance. Specialist Equipment. An electrical or mechanical failure, flat battery, accident, fire, theft, attempted theft or puncture to the vehicle, The cost of draining or removing the incorrect type of or any which immediately renders the vehicle immobilised. contaminated fuel. -

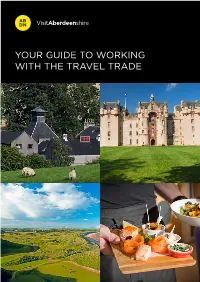

Your Guide to Working with the Travel Trade

YOUR GUIDE TO WORKING WITH THE TRAVEL TRADE CONTENTS INTRODUCTION The travel trade – intermediaries such as tour Introduction 2 operators, wholesalers, travel agents and online travel agents - play a significant role in attracting What is the 3 visitors to Aberdeen and Aberdeenshire, even Travel Trade? though consumers are increasingly organising and planning their own trips directly. Working Attracting 5 with the travel trade is an effective and valuable way of reaching larger numbers of potential International travellers in global markets. Attention Attracting visitors to your business requires Understanding Your 9 some specialist industry awareness and an Target Markets understanding of all the different kinds of travel trade activity. It’s important to know Working with the 10 how the sector works from a business point Travel Trade of view, for example, the commission system, so that tourism products can be priced Rates and Commission 13 accordingly. Developing your offer to the required standard needs an understanding of Creating a Travel 14 different travel styles, language, cultural and culinary considerations and so on. Trade Sales Kit VisitAberdeenshire runs a comprehensive Hosting 16 programme of travel trade activities which Familiarisation Visits include establishing strong relationships with key operators to attract group and Steps to working 17 independent travel to our region. with the travel trade This guide aims to provide a straightforward introduction to the opportunities available Building Relationships 17 to Aberdeen and Aberdeenshire’s tourism businesses, enabling you to grow your Next Steps? 18 business through working with the national and international travel trade. Useful Web Sites 20 KEY TAKEAWAY............... The travel trade is often thought about for the group market only, but in fact the travel trade is also used extensively for small group and individual travel. -

Travel Insurance for Residents of Eligible UK Countries (Eligible UK Countries Are Defined As: the United Kingdom, Channel Islands, Isle of Man and Gibraltar)

Travel Insurance For Residents of Eligible UK Countries (Eligible UK Countries are defined as: the United Kingdom, Channel Islands, Isle of Man and Gibraltar). Insurance Product Information Document Company: Voyager Insurance Services Ltd Product: Voyager Plus Travel Insurance 2021/22 - Standard, Prime and Black Cover Voyager Insurance Services Ltd is authorised and regulated by the Financial Conduct Authority, FRN 305814 Registered in England & Wales, Number 3251842. This insurance is underwritten by Starr International (Europe) Limited who are authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. This document provides a summary of the key information relating to this insurance policy. Complete pre-contractual and contractual information on the product is provided in the full policy documentation. The agreed sums insured are specified in your schedule. What is this type of Insurance? This travel insurance policy protects insured persons when travelling in respect of unexpected medical emergencies, personal liability and similar expenses from their travel. What is insured? What is not insured? Cancellation or Curtailment You are responsible for paying your policy excess in the including Cancellation Cover as a Result of COVID-19 event of a claim up to the amount shown in your insurance Emergency Medical Expenses policy. including Additional Travel and Accommodation Any claims for curtailment of the trip due to COVID-19. Expenses in Respect of COVID-19 Dental treatment other than to alleviate sudden pain on including Relatives Additional Expenses natural teeth. including Emergency Dental Treatment including Burial and Cremation Existing medical conditions that you haven’t told us about if required as per the “Important Conditions and Questions Hospital Stay Benefit Relating to Health & Activities”. -

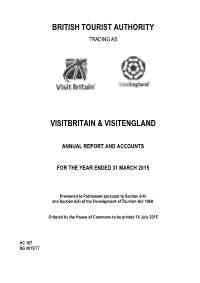

BTA Annual Report & Accounts 2014-15

BRITISH TOOURIST AUTHORITY TRADING AS VISITBRITAIN & VISITENGLAND ANNUAL REPORT AND ACCOUNTS FOR THE YEAR ENDED 31 MARCH 2015 Presented to Parliament pursuant to Section 6(4) and Section 6(6) of the Development of Tourism Act 1969. Ordered by the House of Commons to be printed 16 July 2015 HC 167 SG 2015/77 BRITISH TOURIST AUTHORITY TRADING AS VISITBRITAIN & VISITENGLAND ANNUAL REPORT AND ACCOUNTS FOR THE YEAR ENDED 31 MARCH 2015 Presented to Parliament pursuant to Section 6(4) and Section 6(6) of the Development of Tourism Act 1969. Ordered by the House of Commons to be printed 16 July 2015 HC 167 SG 2015/77 © British Tourist Authority c opyright 2015 The text of this document (this excludes, where present, the Royal Arms and all departmee ntal or agency logos) may be reproduced free of charge in any format or medium provided that it is reproduced acc urately and noot in a misleading context. The material must be acknowledged as British Tourist Authority copyright and the document tiitle specified. Where third party material has been identified, permission from the respective copyright holder must be sought. Any enquiries related to this publication should be sentt to us at VisitBritain, Sanctuary Buildings, 20 Great Smit h Street, London, SW1P 3BT. This publication is available at https://www.gov.uk/government/publications Print ISBN 9781474118972 Web ISBN 9781474118989 ID: 12051507 07/15 50442 19585 Printed on paper containing 75% recycled fibre content mminimum. Printed in the UK by the Williams Lea Group on behalf of the Controller of Her Majesty’s Stationery Office. -

Brochure Inside Pages 14/9/05 14:19 Page 1

Travel Awards Cover 14/9/05 14:09 Page 1 brochure inside pages 14/9/05 14:19 Page 1 Introduction Welcome to the 19th annual Guardian, Observer and For those whose livelihoods depend on tourism, Guardian Unlimited Travel Awards. As the longest- 2004 ended on a terrible note. The devastating running independent survey of its kind, we believe tsunami which swept through the Indian Ocean was the results published in this brochure offer a unique proof of just how fragile this industry can be. But it and fascinating insight into the tastes and also served to illustrate the regenerative power of preferences of discerning travellers today. tourism. Predictions at the time that hotels would be up and running within weeks seemed impossibly Size isn’t everything, or so they say. And once again optimistic but the cynics were proved wrong, as the results of our survey prove that, when it comes destinations like Thailand, the Maldives and Sri to choosing a holiday, our readers tend to favour the Lanka hurried to rebuild their battered infrastructure. smaller, specialist companies over the big mass market operators. The same principle applies to their The fortunes of the travel industry have always preferred destinations. If these awards were judged been particularly vulnerable to events such as purely on the number of entries, then you might natural disasters or terrorism, but the huge response expect favourites such as France and Spain to win to these awards shows that our appetite for travel is every year. Our unique scoring system ensures that as strong as ever. -

Planning Statement

Planning Design & Access Statement Amendments to extant planning permission (RR/2007/397/P as amended by later permissions) for a kitchen extension to approved conference centre, extension to existing accommodation block, amended design and location for approved accommodation blocks, toilet/shower block and tenting area, relocate approved car park, new coach passing places, provision of a range of outdoor activities including a new activity lake, creation of bunds with fencing and landscaping. PGL Pestalozzi, Ladybird Lane, Sedlescombe, Battle, TN33 0UF June 2019 Client: PGL Travel Ltd Report Title: Planning Statement Contents 1. Introduction .................................................................................................................................................................... 1 2. Need for the Proposal .................................................................................................................................................. 4 3. Site Description and Context ...................................................................................................................................... 6 4. Planning History .............................................................................................................................................................. 9 5. Proposal ........................................................................................................................................................................ 14 6. Consultation ................................................................................................................................................................ -

Eurocamp 2020, Which Will Bring Together 20 Young People from Our Twin Towns for Two Weeks of Adventure and a Creative Project

FAQ What is it? EuroCamp is an annual town council initiative, created and operated internationally, in partnership with Warwick’s twin towns. Each year EuroCamp brings four young individuals from CV34 to join groups of young people from our twin towns in France, Germany and Italy. This year, Warwick is hosting EuroCamp 2020, which will bring together 20 young people from our twin towns for two weeks of adventure and a creative project. For the past six years, EuroCamp has successfully hosted pupils from local schools and given them experience in working together with others from our twin towns on community projects, learning key skills, and aiding personal development. When is it? EuroCamp 2020 runs from Sunday 19th of July for two weeks, through to Sunday 2nd August. When is the application deadline? We close applications on Tuesday 10th March. We will then review all applications and take some forward to face-to-face meetings. Who comes to EuroCamp? Each year, some 20 young people, aged between 16 and 21, come together to form a new EuroCamp team. Warwick, and each of our twin towns, sends four young people to participate in two weeks of experiences and a collaborative community project. The EuroCamp 202 team will comprise of young individuals from Warwick, and our twin towns of Saumur (France), Verden & Havelberg (Germany), and Formigine (Italy). Where is it? EuroCamp 2020 will be headquartered at the Jockey’s Accommodation at Warwick Racecourse. Accommodation and catering for each participant is included for the two weeks. In addition to having use of the facilities at HQ, EuroCamp will deliver creative and adventure across the town with privileged access and unique (and some VIP) experiences across the town and its iconic landmarks. -

Streetfootballworld Annual Report 2012

ANNUAL REPORT 2012 Changing the world through football Intro Quote. Contents 03/ Welcome 14/ Consulting 04/ What we do 15/ Advocacy 05/ How we do it 16/ Social legacy 06/ The network 18/ Aims and achievements 08/ Network development 19/ Organisational profile 11/ Capacity development 20/ Finances Where possible, this annual report uses the Social Reporting Standard (SRS) as a guideline for reporting the activities and impact of streetfootballworld in 2012. www.social-reporting-standard.de 03 WELCOME 2012 showed us that we are heading in the right direction. MESSAGE FROM thE BOARD VOICES FROM THE NETWORK Young people are at the centre of everything we do at streetfootballworld. The organisations which form the streetfootballworld network equip their “Having come through the participants with the skills, confidence programmes myself, I have now risen and opportunities they need to to the position of Head Coach at Slum overcome the challenges they face in “It is so important for young people Soccer. A large part of that growth is their daily lives. As a worldwide coalition, to have someone to relate to when attributable to streetfootballworld and we can learn from each other and developing in life. The growth of the opportunities they have brought to develop stronger solutions together. young leaders in sports-based youth the network.” development, particularly in soccer In 2012, streetfootballworld once again which is such a powerful sport already, Homkant Surandase provided a platform to exchange best is amazing and something I’m proud to 23, Head Coach at Slum Soccer (India) practice, develop projects and share be a part of.” As a teenager, Homkant Surandase was ideas on how to increase the impact on a wandering aimlessly on the streets before global scale. -

Disappoints on Debt Repayment

25 MAY 2016 Quarterly Update COX & KINGS BUY MIDCAPS Target Price: Rs 286 Disappoints on debt repayment Cox & Kings’s (C&K) FY16 revenue at Rs 24 bn (up 6% YoY) and CMP : Rs 150 EBITDA at Rs 8.2 bn (up 1% YoY) were broadly in line with our Potential Upside : 91% expectations. PAT at Rs 539 mn (our est. Rs 2.8 bn) was affected due to goodwill write-off as a result of sale of subsidiary. However, what disappointed us was debt repayment guidance of Rs 3-5 bn not panning MARKET DATA out (due to higher capex/working capital). FY16 net debt came down to No. of Shares : 169mn Free Float : 51% Rs 22.5 bn primarily due to cash from sale of subsidiary. Market Cap : Rs25bn Management does not see deterioration in working capital but expects 52-week High / Low : Rs317 / Rs141 capex to be higher at Rs 3 bn in FY17 led by PGL expansion Avg. Daily vol. (6mth) : 497,006 shares (Rs 1.1bn); India capex at Rs 0.8 bn (largely on account of SAP Bloomberg Code : COXK IB Equity implementation); and Rs 0.7 bn towards Meininger expansion. Promoters Holding : 49% FII / DII : 34% / 3% Management guided cash of Rs 4 bn from sale of subsidiaries coupled with operating cash flow will be used to reduce debt. Q4 highlights: In a seasonally weak quarter (Q4 contributes ~10% of yearly EBITDA),C&K reported 4% decline in revenue to Rs 4.7 bn. Despite higher ad spends in domestic leisure and impact of terror attack, EBITDA (adj. -

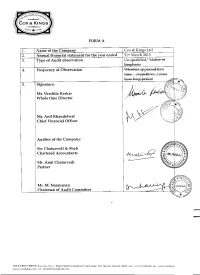

Cox & Kings Sheet 2015 Part II.Pmd

POISED FOR FUTURE GROWTH Cox & Kings Limited 75th Annual Report 2014-15 Poised For Future Growth Over the last three decades, Cox & Kings Ltd. has transformed itself from an air-ticketing agent in Mumbai into a diversified, multinational travel conglomerate with a focus on the new-age global consumer. The company nurtures a deeply entrepreneurial spirit; embracing change is in our DNA. CONTENTS Cox & Kings is today well established across 23 countries in businesses which range from experiential learning for children to flexible individual holidays and from packaged group tours to hybrid hotels. Fiscal 2014-15 was in summary a year of rejuvenation. We enhanced our dominance in existing markets, forged new partnerships to drive future growth and strengthened our Balance Sheet. If the last few years were characterised by breath-taking change, then FY15 was the year in which the transformation was complete. We look to the future with tremendous confidence and enthusiasm, anchored firmly by our roots. Business Overview 01 Financial Statements Standalone Chairman's Letter 20 Independent Auditor’s Report 98 Board of Directors 22 Financial Statements 102 Financial Highlights 24 Significant Accounting Policies 106 Corporate Information 26 Notes 108 Financial Information of Subsidiary Companies 137 Management Discussion & Analysis 27 Consolidated Statutory Reports Auditor’s Report 144 Directors' Report 41 Financial Statements 148 Report on Corporate Governance 77 Significant Accounting Policies 152 Corporate Social Responsibility Report 95 Notes 155 Annual Report 2014-15 | 01 Poised For Future Growth Over the last three decades, Cox & Kings Ltd. has transformed itself from an air-ticketing agent in Mumbai into a diversified, multinational travel conglomerate with a focus on the new-age global consumer.