A Banking Heritage Group Mission Values

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The State of the Deal and Deloitte Queensland Index

The State of the Deal and Deloitte Queensland Index March 2021 – Queensland Index Exceeds $100 billion THE STATE OF THE DEAL | March 2021 – Queensland Index Exceeds $100 billion Contents Executive Summary 1 Then & Now – Investment Landscape 3 Then & Now – Deloitte Queensland Index 4 Queensland Economic Update 7 The Deloitte Queensland Index Q1 2021 8 Contacts 11 Sources 12 ii THE STATE OF THE DEAL | March 2021 – Queensland Index Exceeds $100 billion Executive Summary Following the significant rebound in the second half of 2020, companies in the Deloitte Queensland Index exceeded $100 billion at 31 March 2021, the highest month end market capitalisation on record for the State. Deloitte Queensland Index S&P/ASX All Ordinaries Companies in the Deloitte return in Q1 2021 return in Q1 2021 Queensland Index 3.5% 2.4% 169 at 31 March 2021 10.6% in Q4 2020 14.0% in Q4 2020 173 at 31 December 2020 90 companies increased Market capitalisation as at Mar-21 market capitalisation (53%) 66 companies decreased market $101.6b capitalisation (39%) 12 no movement (7%) $97.2b as at Dec-20 $18.5b as at Sep-02 5 delistings 1 listing (1%) Announced QLD M&A Disclosed value of announced transactions in Q1 2021 QLD M&A transactions in Q1 2021 64 $1.9b 92 in Q4 2020 $3.3b in Q4 2020 1 THE STATE OF THE DEAL | March 2021 – Queensland Index Exceeds $100 billion The Deloitte Queensland Index increased by 3.5% in Q1 2021 Queensland M&A more broadly remains strong with with total market capitalisation increasing to $101.6b at 64 transactions announced in Q1 2021 including: Mar-21, the highest month end value on record for the State. -

Industry Associations & ASX Companies

Industry Associations, ASX Companies, Shareholder Interests and Lobbying CONTENTS About the Authors ........................................................................................................................ 3 ACCR ............................................................................................................................................ 3 About ISS-caer ............................................................................................................................. 3 About the Report .......................................................................................................................... 4 Foreword ...................................................................................................................................... 4 Introduction .................................................................................................................................. 5 Report Structure .......................................................................................................................... 6 PART 1 - Background ................................................................................................................... 8 What is an Industry Association? .............................................................................................. 8 Advantages and Disadvantages of Belonging to an Industry Association ........................... 10 Australian Legislation and Regulations Covering Industry Associations ............................. 11 -

Socially Conscious Australian Equity Holdings

Socially Conscious Australian Equity Holdings As at 30 June 2021 Country of Company domicile Weight COMMONWEALTH BANK OF AUSTRALIA AUSTRALIA 10.56% CSL LTD AUSTRALIA 8.46% AUST AND NZ BANKING GROUP AUSTRALIA 5.68% NATIONAL AUSTRALIA BANK LTD AUSTRALIA 5.32% WESTPAC BANKING CORP AUSTRALIA 5.08% TELSTRA CORP LTD AUSTRALIA 3.31% WOOLWORTHS GROUP LTD AUSTRALIA 2.93% FORTESCUE METALS GROUP LTD AUSTRALIA 2.80% TRANSURBAN GROUP AUSTRALIA 2.55% GOODMAN GROUP AUSTRALIA 2.34% WESFARMERS LTD AUSTRALIA 2.29% BRAMBLES LTD AUSTRALIA 1.85% COLES GROUP LTD AUSTRALIA 1.80% SUNCORP GROUP LTD AUSTRALIA 1.62% MACQUARIE GROUP LTD AUSTRALIA 1.54% JAMES HARDIE INDUSTRIES IRELAND 1.51% NEWCREST MINING LTD AUSTRALIA 1.45% SONIC HEALTHCARE LTD AUSTRALIA 1.44% MIRVAC GROUP AUSTRALIA 1.43% MAGELLAN FINANCIAL GROUP LTD AUSTRALIA 1.13% STOCKLAND AUSTRALIA 1.11% DEXUS AUSTRALIA 1.11% COMPUTERSHARE LTD AUSTRALIA 1.09% AMCOR PLC AUSTRALIA 1.02% ILUKA RESOURCES LTD AUSTRALIA 1.01% XERO LTD NEW ZEALAND 0.97% WISETECH GLOBAL LTD AUSTRALIA 0.92% SEEK LTD AUSTRALIA 0.88% SYDNEY AIRPORT AUSTRALIA 0.83% NINE ENTERTAINMENT CO HOLDINGS LIMITED AUSTRALIA 0.82% EAGERS AUTOMOTIVE LTD AUSTRALIA 0.82% RELIANCE WORLDWIDE CORP LTD UNITED STATES 0.80% SANDFIRE RESOURCES LTD AUSTRALIA 0.79% AFTERPAY LTD AUSTRALIA 0.79% CHARTER HALL GROUP AUSTRALIA 0.79% SCENTRE GROUP AUSTRALIA 0.79% ORORA LTD AUSTRALIA 0.75% ANSELL LTD AUSTRALIA 0.75% OZ MINERALS LTD AUSTRALIA 0.74% IGO LTD AUSTRALIA 0.71% GPT GROUP AUSTRALIA 0.69% Issued by Aware Super Pty Ltd (ABN 11 118 202 672, AFSL 293340) the trustee of Aware Super (ABN 53 226 460 365). -

Natwest Markets Plc

Information Memorandum 5 March 2020 NatWest Markets Plc (incorporated in Scotland with limited liability under the Companies Act 1948 to 1980, registered number SC090312) A$5,000,000,000 Debt Issuance Programme Arranger & Dealer National Australia Bank Limited Dealers Australia and New Zealand Banking Group Limited Commonwealth Bank of Australia Mizuho Securities Asia Limited NatWest Markets Plc The Toronto-Dominion Bank Westpac Banking Corporation Contents Important notices 1 1. Programme summary 4 2. Information about NatWest Markets Plc 9 3. UK Bank Resolution Regime 10 4. Selling restrictions 11 5. Summary of certain taxation matters 15 6. Other important matters 17 7. Conditions of the Notes 19 8. Form of Pricing Supplement 39 9. Glossary 44 Directory 47 42015475_33 Important notices This Information Memorandum The distribution and use of this Information Memorandum, including any Issue Materials, and the This Information Memorandum relates to a debt offer or sale of Notes may be restricted by law in certain issuance programme (“ Programme ”) established by jurisdictions and intending purchasers and other NatWest Markets Plc (the “Issuer ”), under which it may investors should inform themselves about them and issue Notes from time to time. It has been prepared by, observe any such restrictions. and is issued with the authority of, the Issuer. In particular: The Issuer is neither a bank nor an authorised deposit- taking institution which is authorised under the this Information Memorandum is not a prospectus Australian Banking Act and nor is it supervised by the or other disclosure document for the purposes of the Australian Prudential Regulation Authority. The Notes Corporations Act. -

Australian Equities Lending Margins Effective 21 April 2021

Australian Equities Lending Margins Effective 21 April 2021 Stock ASX Margin Stock ASX Margin Stock ASX Margin Code Rate Code Rate Code Rate A2B Australia A2B 40% AusNet Services AST 70% Costa Group Holdings CGC 60% The A2 Milk Company A2M 65% ASX ASX 75% Challenger Financial Australian Agricultural Company AAC 55% AUB Group AUB 50% Services Group CGF 70% Adelaide Brighton ABC 70% Australian United Challenger Capital Notes CGFPA 60% Abacus Property Group ABP 60% Investment Company AUI 70% Challenger Capital Notes 2 CGFPB 60% Audinate Group AD8 40% Aventus Retail Property Group AVN 50% Challenger Capital Notes 3 CGFPC 60% Adairs ADH 40% Alumina AWC 70% Charter Hall Group CHC 70% APN Industria REIT ADI 40% Accent Group AX1 40% Champion Iron CIA 50% Australian Ethical Amaysim Australia AYS 40% Cimic Group CIM 70% Investment Limited AEF 40% Aurizon Holdings AZJ 75% Carlton Investments CIN 50% Australian Foundation Bapcor BAP 60% Centuria Industrial REIT CIP 60% Investment Company AFI 75% Baby Bunting Group BBN 40% Collins Foods CKF 50% Ainsworth Game Technology AGI 40% Bendigo & Adelaide Bank BEN 70% Class CL1 40% AGL Energy AGL 75% Bendigo & Adelaide Bank BENHB 65% Clean Teq Holdings CLQ 40% AGL Energy USFDS AGLHA 75% Bendigo & Adelaide Bank CPS BENPE 65% Clover Corporation CLV 40% Automotive Holdings Group AHG 55% Bendigo & Adelaide Bank CPS BENPF 65% Charter Hall Long Wale REIT CLW 60% Asaleo Care AHY 50% Bendigo & Adelaide Bank CPS BENPG 65% Centuria Metropolitan REIT CMA 50% Auckland International Airport AIA 70% Bell Financial Group -

FTSE World Asia Pacific

2 FTSE Russell Publications 19 August 2021 FTSE World Asia Pacific Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) a2 Milk 0.04 NEW Asustek Computer Inc 0.1 TAIWAN Cheil Worldwide 0.02 KOREA ZEALAND ASX 0.12 AUSTRALIA Cheng Shin Rubber Industry 0.03 TAIWAN AAC Technologies Holdings 0.05 HONG KONG Atlas Arteria 0.05 AUSTRALIA Chiba Bank 0.04 JAPAN ABC-Mart 0.02 JAPAN AU Optronics 0.08 TAIWAN Chicony Electronics 0.02 TAIWAN Accton Technology 0.07 TAIWAN Auckland International Airport 0.06 NEW China Airlines 0.02 TAIWAN Acer 0.03 TAIWAN ZEALAND China Development Financial Holdings 0.07 TAIWAN Acom 0.02 JAPAN Aurizon Holdings 0.05 AUSTRALIA China Life Insurance 0.02 TAIWAN Activia Properties 0.03 JAPAN Ausnet Services 0.03 AUSTRALIA China Motor 0.01 TAIWAN ADBRI 0.01 AUSTRALIA Australia & New Zealand Banking Group 0.64 AUSTRALIA China Steel 0.19 TAIWAN Advance Residence Investment 0.05 JAPAN Axiata Group Bhd 0.04 MALAYSIA China Travel International Investment <0.005 HONG KONG ADVANCED INFO SERVICE 0.06 THAILAND Azbil Corp. 0.06 JAPAN Hong Kong Advantech 0.05 TAIWAN B.Grimm Power 0.01 THAILAND Chow Tai Fook Jewellery Group 0.04 HONG KONG Advantest Corp 0.19 JAPAN Bandai Namco Holdings 0.14 JAPAN Chubu Elec Power 0.09 JAPAN Aeon 0.2 JAPAN Bangkok Bank (F) 0.02 THAILAND Chugai Seiyaku 0.27 JAPAN AEON Financial Service 0.01 JAPAN Bangkok Bank PCL (NVDR) 0.01 THAILAND Chugoku Bank 0.01 JAPAN Aeon Mall 0.02 JAPAN Bangkok Dusit Medical Services PCL 0.07 THAILAND Chugoku Electric Power 0.03 JAPAN Afterpay Touch Group 0.21 AUSTRALIA Bangkok Expressway and Metro 0.02 THAILAND Chunghwa Telecom 0.17 TAIWAN AGC 0.08 JAPAN Bangkok Life Assurance PCL 0.01 THAILAND CIMB Group Holdings 0.08 MALAYSIA AGL Energy 0.04 AUSTRALIA Bank of East Asia 0.03 HONG KONG CIMIC Group 0.01 AUSTRALIA AIA Group Ltd. -

Bank of Queensland Submission to RBA: EFTPOS and Visa Debit

Bank of Queensland Submission to RBA EFTPOS and Visa Debit Consultation Document April 2005 Contents 1. Executive Summary 2. EFTPOS Interchange Fees 2.1 The Case for Zero EFTPOS Interchange Fees 2.2 RBA’s Draft EFTPOS Interchange Fee Standard 2.3 Potential Impact of the Reforms on Product Pricing 3. Visa Debit Reforms 3.1 The ‘Honour All Cards’ Rule 3.2 Visa Debit – Transparency 4. EFTPOS Access 5. Conclusion 1. Executive Summary It is a matter of history that the differing reform processes adopted for credit card interchange and for EFTPOS interchange has resulted in the implementation of these reforms becoming “out of step”. All the benefits from the disconnect between these reforms have fallen on the side of the retailers. In designating the EFTPOS system, we believed that the Reserve Bank would move to redress this situation and place the EFTPOS reforms back on track, as such we embraced designation as a positive development. Clearly, the self-regulatory industry EFTPOS reforms were aimed at achieving concurrent interchange fee reform between EFTPOS and Credit Cards but were required to follow an onerous and uncertain regulatory approval process. The uncertainty of the process was highlighted by the Australian Competition Tribunal (ACT) decision in 2004 to overturn the successful Authorisation Application determination made by the Australian Competition and Consumer Commission (ACCC) in relation to Zero EFTPOS Interchange Fees. For the record, Bank of Queensland supports the views expressed by the Reserve Bank1 in the Consultation Document in relation to the ACT findings. Throughout the whole Payments System reform process, the financial services industry has been characterised as being generally opposed to reform, when clearly this has not been the case. -

Trevor Hart Banking in a New World: the Beginnings of ANZ Bank

Trevor Hart Banking in a new world: the beginnings of ANZ Bank Proceedings of the ICOMON meetings, held in conjunction with the ICOM Conference, Melbourne (Australia, 10-16 October, 1998), ed. by Peter Lane and John Sharples. Melbourne, Numismatic Association of Australia, Inc, 2000. 117 p. (NAA Special publication, 2). (English). pp. 39-46 Downloaded from: www.icomon.org BANKING IN A NEW WORLD THE BEGINNINGS OF ANZ BANK By Trevor Hart ANZ Bank, Melbourne, Australia For its first twenty-nine years proposed to the Government in Australia had no bank. The British England, the formation of "The New settlement of Australia began in South Wales Loan Bank" based on 1788, but Australia's first bank, the the bank at the Cape of Good Hope. Bank of New South Wales, did not In 1812 the government refused open until 1817. his proposal. Macquarie accepted this refusal but was still convinced of Australia was founded as a the need for a bank in the colony.4 In self-supporting penal colony and 1816 he acted again, this time monetary arrangements were ad hoc. "convening a meeting of the A local currency of small private magistrates, principal merchants and promissory notes grew up in gentlemen of Sydney ... at which my conjunction with the circulation of favourite measure of a bank was Government Store receipts. This led brought forward."5 Macquarie issued to a dual monetary standard in a 'charter' for seven years to the which 'currency' came to mean directors of the new bank (which "money of purely local was later disallowed by the British acceptability" and 'sterling' meant Government) and on 8 April 1817 "any form of money .. -

Pp43-45 6.3-Oliver

THE FINANCIAL SERVICES FORUM Retail Banking BANK TO THE FUTURE The high street banks have alienated many of their customers in their search for efficiency, depersonalising the whole experience with offshore call centres and centralised lending decisions. Malcolm Oliver looks at how two relative newcomers to the UK retail banking scene are reviving the old concept of real bank managers and personal service. The future of retail banking is a self-evidently important The key to success is often not the development of theme, and indeed one that The Financial Services Forum the ideas themselves but having the confidence (and addresses each year in the slightly broader context of its perhaps the commercial and professional courage) to Future of Retail Financial Services conferences. stand out and not dismiss them, like most of the herd, But between the positive idea and the delivered reality as passé or inappropriate to the needs of twenty-first- can fall a huge shadow. If speakers really have cracked century customers. As Allan Leighton said recently, in the problem in a way that will deliver lasting customer his new book on leadership, “the biggest challenge to satisfaction and regulatory approval and sustainable senior management is being able to listen effectively to profitability, why on earth would they want to give their those below who know what will and will not work”. secrets away to commercial rivals? Just reflect on how many financial services companies The Forum largely avoids this problem by its in the last decade or so have put in place new strategies membership formula, which means that most presenters to relocate call centres overseas, or to close local will already have built informal relationships with most of branches, or to withdraw free ATMs, or to restrict opening the audience, and will therefore feel that they are talking hours – only to have to perform an embarrassing volte- amongst friends rather than competitors. -

How Mpos Helps Food Trucks Keep up with Modern Customers

FEBRUARY 2019 How mPOS Helps Food Trucks Keep Up With Modern Customers How mPOS solutions Fiserv to acquire First Data How mPOS helps drive food truck supermarkets compete (News and Trends) vendors’ businesses (Deep Dive) 7 (Feature Story) 11 16 mPOS Tracker™ © 2019 PYMNTS.com All Rights Reserved TABLEOFCONTENTS 03 07 11 What’s Inside Feature Story News and Trends Customers demand smooth cross- Nhon Ma, co-founder and co-owner The latest mPOS industry headlines channel experiences, providers of Belgian waffle company Zinneken’s, push mPOS solutions in cash-scarce and Frank Sacchetti, CEO of Frosty Ice societies and First Data will be Cream, discuss the mPOS features that acquired power their food truck operations 16 23 181 Deep Dive Scorecard About Faced with fierce eTailer competition, The results are in. See the top Information on PYMNTS.com supermarkets are turning to customer- scorers and a provider directory and Mobeewave facing scan-and-go-apps or equipping featuring 314 players in the space, employees with handheld devices to including four additions. make purchasing more convenient and win new business ACKNOWLEDGMENT The mPOS Tracker™ was done in collaboration with Mobeewave, and PYMNTS is grateful for the company’s support and insight. PYMNTS.com retains full editorial control over the findings presented, as well as the methodology and data analysis. mPOS Tracker™ © 2019 PYMNTS.com All Rights Reserved February 2019 | 2 WHAT’S INSIDE Whether in store or online, catering to modern consumers means providing them with a unified retail experience. Consumers want to smoothly transition from online shopping to browsing a physical retail store, and 56 percent say they would be more likely to patronize a store that offered them a shared cart across channels. -

Lousada Family Tree M Esther Lamego 1708 –20.10.1744 D of Aaron Lamego of Jamaica Uncle Isaac Lamego 1685 –9.1.1767 M …

Emanuel Baruh Lousada Lousada Family Tree m Esther Lamego 1708 –20.10.1744 d of Aaron Lamego of Jamaica Uncle Isaac Lamego 1685 –9.1.1767 m … Jacob Baruh Lousada d1752 Rebecca Baruh Lousada Abigail Baruh Lousada Rachel Baruh Lousada Aaron Lousada m12.1743 Abigail Lamego m Joseph Aguilar d before 1752 m … Almoyda m Rodrigues Lopes m Rachel d of Daniel Abigail Lamego 12.11.1723 – Jacob Sarah Lamego m Rebecca Lamego m Esther Lamego 12.11.1723 – 16.3.1790 d of Mendes da Costa 16.3.1790 m12.1743 Jacob Lamego Jacob Lopes Torres Isaac Mendes da Costa 1737 – 1799 Uncle Isaac Lamego Isaac Aguilar Esther Almoyda Rachel Almoyda Abigail Almoyda Baruh Lousada d 1752 m Abraham de Mattos Daniel Baruh Lousada Emanuel Baruh Mocatta 1730 –1800 Isaac David Rebecca Sarah d14.10.1769 m Rachel Lousada m Esther for children see Jacob Torres Torres Torres m Torres Isaac Baruh Lousada Emanuel Baruh Esther Lousada b2.1818 Daniel Baruh Lousada Rebecca m 2 David Lopes Pereira Rachel Lousada Lousada 1748 –1831 Lousada Baruh Lousada m 1 1748 –30.5.1831 m 6.3.1771 Lousada m m Emanuel Baruh son of Aaron Lousada Lousada 1771 Baron d’Aguilar 1748 – 30.5.1831 Abraham for children see Rachel Judith 8.5.1747 –19.11.1821 Rebecca Ximenes Lousada b1807 son of and Rachel Mendes son of Diego Lopes m Daniel Baruh Aguilar d of Diego Lopes Pereira Aaron Lousada da Costa Pereira Lousada d 14.10.1769 Clare Lousada m Jacob Daniel Aaron Isaac Duke de Baron d’Aguilar son of Aaron Lousada David Ximenes Lousada Lousada Lousada Lousada 1783 for children see Emanuel –15.9.1857 m Lydia Lousada -

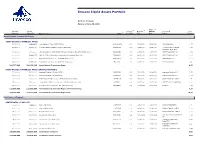

Invesco Liquid Assets Portfolio

Invesco Liquid Assets Portfolio Portfolio Holdings Data as of June 30, 2021 4 2 3 Final Principal Market 1 Coupon/ Maturity Maturity Associated % of Amount Value ($) Name of Issue CUSIP Yield (%) Date Date Issuer Portfolio Asset Backed Commercial Paper ASSET-BACKED COMMERCIAL PAPER 25,000,000 24,998,958 Ionic Capital III Trust (CEP-UBS AG) 46220WUG9 0.13 07/16/2021 07/16/2021 UBS GROUP AG 1.27 37,777,000 37,774,140 Lexington Parker Capital Company (Multi-CEP) 52953AUV5 0.15 07/29/2021 07/29/2021 Lexington Parker Capital 1.93 Company (Multi-CEP) 10,500,000 10,500,000 LMA Americas LLC (CEP-Credit Agricole Corporate & Investment Bank S.A.) 53944QXR6 0.05 10/25/2021 10/25/2021 CREDIT AGRICOLE SA 0.54 40,000,000 39,992,272 LMA SA (CEP-Credit Agricole Corporate & Investment Bank S.A.) 53944QW30 0.24 09/03/2021 09/03/2021 CREDIT AGRICOLE SA 2.04 20,000,000 20,000,000 Ridgefield Funding Co. LLC (CEP-BNP Paribas S.A.) 76582JW26 0.14 09/02/2021 09/02/2021 BNP PARIBAS SA 1.02 55,000,000 54,964,250 Ridgefield Funding Co. LLC (CEP-BNP Paribas S.A.) 76582JY81 0.14 11/08/2021 11/08/2021 BNP PARIBAS SA 2.80 188,277,000 188,229,620 Asset-Backed Commercial Paper 9.60 ASSET-BACKED COMMERCIAL PAPER (INTEREST BEARING) 50,000,000 50,000,000 Anglesea Funding LLC (Multi-CEP) 0347M5VG1 0.17 07/01/2021 08/04/2021 Anglesea Funding LLC 2.55 25,000,000 25,000,000 Anglesea Funding LLC (Multi-CEP) 0347M5VL0 0.17 07/01/2021 08/04/2021 Anglesea Funding LLC 1.27 10,000,000 10,000,000 Bedford Row Funding Corp.