Annual Plan 2009-2010

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PAKISTAN SERVICES LIMITED LIST of SHAREHOLDERS/BENEFICIAL OWNERS S

PAKISTAN SERVICES LIMITED LIST OF SHAREHOLDERS/BENEFICIAL OWNERS s. No. Folio No. Name of Shareholder Father Name Address Nationality Occupation CNIC NO. Category No. of Shares 1 14 SECRETARY, P.I.A P.I.A. CORPORATION PIA BUILDING KARACHI AIRPORT KARACHI PAKISTANI OTHER OTHERS 172,913 2 15 PRESIDENT OF PAKISTAN PRESIDENTS SECRETARIAT RAWALPINDI PAKISTANI OTHER OTHERS 336,535 3 16 MAHMUD A. HAROON HAROON HOUSE DR. ZIAUDDIN AHMAD ROAD KARACHI-2 PAKISTANI OTHER INDIVIDUALS 40 4 17 SAID A. HAROON HAROON HOUSE DR. ZIAUDDIN AHMAD ROAD KARACHI-2 PAKISTANI OTHER INDIVIDUALS 27 5 23 S.A. SHAKOOR PASHA S/O AL-HAJ S. KARIM BAKSH A-502, BLOCK-3 GULSHAN-E-IQBAL KARACHI PAKISTANI OTHER INDIVIDUALS 67 6 24 ZAFAR MOHAMMAD KHAN 55, MUSLIMABAD M.A. JINNAH ROAD KARACHI-5 PAKISTANI OTHER INDIVIDUALS 67 7 26 HAJIANI HAWA BAI W/O HAJI HASHIM 1119/3, HUSSAINABAD FEDERAL B AREA KARACHI-38 PAKISTANI OTHER INDIVIDUALS 2 8 29 KHAWAJA ABDUL RASHEED S/O MR. ABDUL HAMID C/O CONTINENTAL CYCLE AND MOTOR COMPANY 425, DR. ZIAUDDIN AHMED ROAD, KARACHI. PAKISTANI OTHER INDIVIDUALS 272 9 34 AVARI BYRAMJI DINSHAW S/O MR.BYRAMJI BEACH LUXURY HOTEL NEW QUEENS ROAD KARACHI PAKISTANI OTHER INDIVIDUALS 3,751 10 36 SAFDAR IQBAL PURI S/O MR. M. SHARIF PURI 59-C-2 GULBERG III LAHORE PAKISTANI OTHER INDIVIDUALS 3,716 11 40 NUZHAT JAMILA QAYUM W/O MR. M.A. QAYYUM 229-2A, BLOCK-2 (AL-FATIMA) P.E.C.H. SOCIETY KARACHI-75400 PAKISTANI OTHER INDIVIDUALS 597 12 49 U.B.L. (SYED SIBTE RAZA NAQVI) A/C SYED SIBTE RAZA NAQVI JUBILEE INSURANCE HOUSE I.I. -

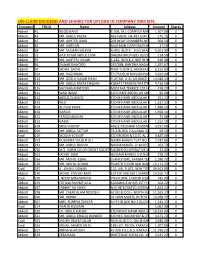

Un-Claim Dividend and Shares for Upload in Company Web Site

UN-CLAIM DIVIDEND AND SHARES FOR UPLOAD IN COMPANY WEB SITE. Company FOLIO Name Address Amount Shares Abbott 41 BILQIS BANO C-306, M.L.COMPLEX MIRZA KHALEEJ1,507.00 BEG ROAD,0 PARSI COLONY KARACHI Abbott 43 MR. ABDUL RAZAK RUFI VIEW, JM-497,FLAT NO-103175.75 JIGGAR MOORADABADI0 ROAD NEAR ALLAMA IQBAL LIBRARY KARACHI-74800 Abbott 47 MR. AKHTER JAMIL 203 INSAF CHAMBERS NEAR PICTURE600.50 HOUSE0 M.A.JINNAH ROAD KARACHI Abbott 62 MR. HAROON RAHEMAN CORPORATION 26 COCHINWALA27.50 0 MARKET KARACHI Abbott 68 MR. SALMAN SALEEM A-450, BLOCK - 3 GULSHAN-E-IQBAL6,503.00 KARACHI.0 Abbott 72 HAJI TAYUB ABDUL LATIF DHEDHI BROTHERS 20/21 GORDHANDAS714.50 MARKET0 KARACHI Abbott 95 MR. AKHTER HUSAIN C-182, BLOCK-C NORTH NAZIMABAD616.00 KARACHI0 Abbott 96 ZAINAB DAWOOD 267/268, BANTWA NAGAR LIAQUATABAD1,397.67 KARACHI-190 267/268, BANTWA NAGAR LIAQUATABAD KARACHI-19 Abbott 97 MOHD. SADIQ FIRST FLOOR 2, MADINA MANZIL6,155.83 RAMTLA ROAD0 ARAMBAG KARACHI Abbott 104 MR. RIAZUDDIN 7/173 DELHI MUSLIM HOUSING4,262.00 SOCIETY SHAHEED-E-MILLAT0 OFF SIRAJUDULLAH ROAD KARACHI. Abbott 126 MR. AZIZUL HASAN KHAN FLAT NO. A-31 ALLIANCE PARADISE14,040.44 APARTMENT0 PHASE-I, II-C/1 NAGAN CHORANGI, NORTH KARACHI KARACHI. Abbott 131 MR. ABDUL RAZAK HASSAN KISMAT TRADERS THATTAI COMPOUND4,716.50 KARACHI-74000.0 Abbott 135 SAYVARA KHATOON MUSTAFA TERRECE 1ST FLOOR BEHIND778.27 TOOSO0 SNACK BAR BAHADURABAD KARACHI. Abbott 141 WASI IMAM C/O HANIF ABDULLAH MOTIWALA95.00 MUSTUFA0 TERRECE IST FLOOR BEHIND UBL BAHUDARABAD BRANCH BAHEDURABAD KARACHI Abbott 142 ABDUL QUDDOS C/O M HANIF ABDULLAH MOTIWALA252.22 MUSTUFA0 TERRECE 1ST FLOOR BEHIND UBL BAHEDURABAD BRANCH BAHDURABAD KARACHI. -

Punjab Tourism for Economic Growth Final Report Consortium for Development Policy Research

Punjab Tourism for Economic Growth Final Report Consortium for Development Policy Research ABSTRACT This report documents the technical support provided by the Design Team, deployed by CDPR, and covers the recommendations for institutional and regulatory reforms as well as a proposed private sector participation framework for tourism sector in Punjab, in the context of religious tourism, to stimulate investment and economic growth. Pakistan: Cultural and Heritage Tourism Project ---------------------- (Back of the title page) ---------------------- This page is intentionally left blank. 2 Consortium for Development Policy Research Pakistan: Cultural and Heritage Tourism Project TABLE OF CONTENTS LIST OF ACRONYMS & ABBREVIATIONS 56 LIST OF FIGURES 78 LIST OF TABLES 89 LIST OF BOXES 910 ACKNOWLEDGMENTS 1011 EXECUTIVE SUMMARY 1112 1 BACKGROUND AND CONTEXT 1819 1.1 INTRODUCTION 1819 1.2 PAKISTAN’S TOURISM SECTOR 1819 1.3 TRAVEL AND TOURISM COMPETITIVENESS 2324 1.4 ECONOMIC POTENTIAL OF TOURISM SECTOR 2526 1.4.1 INTERNATIONAL TOURISM 2526 1.4.2 DOMESTIC TOURISM 2627 1.5 ECONOMIC POTENTIAL HERITAGE / RELIGIOUS TOURISM 2728 1.5.1 SIKH TOURISM - A CASE STUDY 2930 1.5.2 BUDDHIST TOURISM - A CASE STUDY 3536 1.6 DEVELOPING TOURISM - KEY ISSUES & CHALLENGES 3738 1.6.1 CHALLENGES FACED BY TOURISM SECTOR IN PUNJAB 3738 1.6.2 CHALLENGES SPECIFIC TO HERITAGE TOURISM 3940 2 EXISTING INSTITUTIONAL ARRANGEMENTS & REGULATORY FRAMEWORK FOR TOURISM SECTOR 4344 2.1 CURRENT INSTITUTIONAL ARRANGEMENTS 4344 2.1.1 YOUTH AFFAIRS, SPORTS, ARCHAEOLOGY AND TOURISM -

Teaching Guide 3.Pdf

3 Teaching Guide We Learn Social Studies Musarrat Haidery 1 contents Contents Pages Introduction ................................................................................................... iv Unit 1 Our world ............................................................................................2 Unit 2 Earth, the living planet ......................................................................12 Unit 3 Natural resources ..............................................................................20 Unit 4 Making the world a better place .......................................................26 Unit 5 Then and now ...................................................................................40 Unit 6 Our culture ........................................................................................46 Unit 7 The world of maps ............................................................................50 Worksheets ..................................................................................................54 Answer key ..................................................................................................63 Additional questions ....................................................................................69 Introduction Introduction This teaching guide is a valuable asset to the teacher of We Learn Social Studies Book 3. It offers step-by-step guidance about how to use the student’s book so that maximum benefit is passed on to students. At the same time, it makes your work easy. Social studies -

Classification: 8U1.66

Author wise Bibliography Classification: 8u1.66, 1 Articles on Iqbal. - N M: N M, (8U1.66V3EngEng/ART) 2 Cuttings on Iqbaliyat. - Unknown: 0. (8U1.66V3EngEng/CUT-I) 3 Iqbal Millat No Hudikaawan. A. S. Noniwala(Tr.). - Unknown: 0. (8U1.66A71GujGuj/NON-I) 4 Aspects of Iqbal: A Collection of Selected Papers Read on the Occasion of the Iqbal Day Celebrations on the 9th January, 1938. - Lahore: Qaumi Kutab Khana, 1938. (8U1.66R3EngEng/ASP-I) 5 Iqbal: Spiritual Father of Pakistan. - Islamabad: Ministary of Education, Government of Pakistan, 1949. (8U1.66O3EngEng/PAK-I) 6 Iqbal Studies. Ziaul Islam(Ed.). - Lahore: Bazm-e-Iqbal, 1950. (8U1.66O3EngEng/IQB-Z) 7 Illustrated Weekly of Pakistan. 11:29(Iqbal Number - April 1950).Yusuf Afghan (Ed.). - Karachi: Pakistan Herald, 1950. (8U1.66V2Eng/ILL-Y) 8 Iqbal Day 1951. - Rome: Pakistan Embassey, 1951. (8U1.66R3ItaIta/IQB-P) 9 Iqbal Bazm-e-Iqbal. 1:1(July 1952).Sharif, M. M. (Ed.). Bazm-e-Iqbal, 1952. (8U1.66V13/IQB) 10 Iqbal as Thinker: Eight Essays. - Lahore: 1952. (8U1.66O1EngEng/IQB) 11 Iqbal Bazm-e-Iqbal. 1:3(Jan 1953).Sharif, M. M. (Ed.). Bazm-e-Iqbal, 1953. (8U1.66V13/IQB) 12 Iqbal Bazm-e-Iqbal. 2:1(July 1953).Sharif, M. M. (Ed.). - Lahore: Bazm-e-Iqbal, 1953. (8U1.66V13/IQB) 13 Pakistan Today. 1:1(Iqbal No. April 21, 1953).The High Commissioner for Pakistan, India (Ed.). - Delhi: High Commissioner for Pakistan India, 1953. (8U1.66V2Eng/PAK-H) 14 Iqbal Bazm-e-Iqbal. 2:3(Jan 1954).Sharif, M. M. (Ed.). Bazm-e-Iqbal, 1954. (8U1.66V13/IQB) 15 Iqbal Bazm-e-Iqbal. -

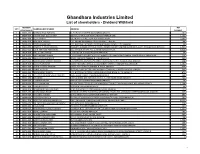

List of Shareholder-Dividend Withheld

Ghandhara Industries Limited List of shareholders - Dividend Withheld MEMBER NET SR # SHAREHOLDER'S NAME ADDRESS FOLIO PAR ID PAYABLE 1 00002-000 MISBAHUDDIN FAROOQI D-151 BLOCK-B NORTH NAZIMABADKARACHI. 461 2 00004-000 FARHAT AFZA BEGUM MST. 166 ABU BAKR BLOCK NEW GARDEN TOWN,LAHORE 1,302 3 00005-000 ALLAH RAKHA 135-MUMTAZ STREETGARHI SHAHOO,LAHORE. 3,293 4 00006-000 AKHTAR A. PERVEZ C/O. AMERICAN EXPRESS CO.87 THE MALL, LAHORE. 180 5 00008-000 DOST MUHAMMAD C/O. NATIONAL MOTORS LIMITEDHUB CHAUKI ROAD, S.I.T.E.KARACHI. 46 6 00010-000 JOSEPH F.P. MASCARENHAS MISQUITA GARDEN CATHOLIC COOP.HOUSING SOCIETY LIMITED BLOCK NO.A-3,OFF: RANDLE ROAD KARACHI. 1,544 7 00013-000 JOHN ANTHONY FERNANDES A-6, ANTHONIAN APT. NO. 1,ADAM ROAD,KARACHI. 5,004 8 00014-000 RIAZ UL HAQ HAMID C-103, BLOCK-XI, FEDERAL.B.AREAKARACHI. 69 9 00015-000 SAIED AHMAD SHAIKH C/O.COMMODORE (RETD) M. RAZI AHMED71/II, KHAYABAN-E-BAHRIA, PHASE-VD.H.A. KARACHI-46. 214 10 00016-000 GHULAM QAMAR KURD 292/8, AZIZABAD FEDERAL B. AREA,KARACHI. 129 11 00017-000 MUHAMMAD QAMAR HUSSAIN C/O.NATIONAL MOTORS LTD.HUB CHAUKI ROAD, S.I.T.E.,P.O.BOX-2706, KARACHI. 218 12 00018-000 AZMAT NAWAZISH AZMAT MOTORS LIMITED, SC-43,CHANDNI CHOWK, STADIUM ROAD,KARACHI. 1,585 13 00021-000 MIRZA HUSSAIN KASHANI HOUSE NO.R-1083/16,FEDERAL B. AREA, KARACHI 434 14 00023-000 RAHAT HUSSAIN PLOT NO.R-483, SECTOR 14-B,SHADMAN TOWN NO.2, NORTH KARACHI,KARACHI. -

S. No. Folio No. Security Holder Name Father's/Husband's Name Address

Askari Bank Limited List of Shareholders without / invalid CNIC # as of 31-12-2019 S. Folio No. Security Holder Name Father's/Husband's Name Address No. of No. Securities 1 9 MR. MOHAMMAD SAEED KHAN S/O MR. MOHAMMAD WAZIR KHAN 65, SCHOOL ROAD, F-7/4, ISLAMABAD. 336 2 10 MR. SHAHID HAFIZ AZMI S/O MR. MOHD ABDUL HAFEEZ 17/1 6TH GIZRI LANE, DEFENCE HOUSING AUTHORITY, PHASE-4, KARACHI. 3,280 3 15 MR. SALEEM MIAN S/O MURTUZA MIAN 344/7, ROSHAN MANSION, THATHAI COMPOUND, M.A. JINNAH ROAD, KARACHI. 439 4 21 MS. HINA SHEHZAD MR. HAMID HUSSAIN C/O MUHAMMAD ASIF THE BUREWALA TEXTILE MILLS LTD 1ST FLOOR, DAWOOD CENTRE, M.T. KHAN ROAD, P.O. 10426, KARACHI. 470 5 42 MR. M. RAFIQUE S/O A. RAHIM B.R.1/27, 1ST FLOOR, JAFFRY CHOWK, KHARADHAR, KARACHI. 9,382 6 49 MR. JAN MOHAMMED S/O GHULAM QADDIR KHAN H.NO. M.B.6-1728/733, RASHIDABAD, BILDIA TOWN, MAHAJIR CAMP, KARACHI. 557 7 55 MR. RAFIQ UR REHMAN S/O MOHD NASRULLAH KHAN PSIB PRIVATE LIMITED, 17-B, PAK CHAMBERS, WEST WHARF ROAD, KARACHI. 305 8 57 MR. MUHAMMAD SHUAIB AKHUNZADA S/O FAZAL-I-MAHMOOD 262, SHAMI ROAD, PESHAWAR CANTT. 1,919 9 64 MR. TAUHEED JAN S/O ABDUR REHMAN KHAN ROOM NO.435, BLOCK-A, PAK SECRETARIAT, ISLAMABAD. 8,530 10 66 MS. NAUREEN FAROOQ KHAN SARDAR M. FAROOQ IBRAHIM 90, MARGALA ROAD, F-8/2, ISLAMABAD. 5,945 11 67 MR. ERSHAD AHMED JAN S/O KH. -

2.2. Broad Fiscal Implications of the 7Th NFC Award

87101 Public Disclosure Authorized Public Disclosure Authorized Fiscal Implications of the 18th Amendment: The Outlook for Provincial Finances Aisha Ghaus Pasha Public Disclosure Authorized World Bank Policy Paper Series on Pakistan PK 02/12 November 2011 Public Disclosure Authorized The Outlook for Provincial Finances 2011 The Policy Research Working Paper Series disseminates the findings of work in progress to encourage the exchange of ideas about development issues. An objective of the series is to get the findings out quickly, even if the presentations are less than fully polished. The papers carry the names of the authors and should be cited accordingly. The findings, interpretations, and conclusions expressed in this paper are entirely those of the authors. They do not necessarily represent the views of the International Bank for Reconstruction and Development / World Bank and its affiliated organizations, or those of the Executive Directors of the World Bank or the governments they represent. 2 The Outlook for Provincial Finances 2011 Fiscal Implications of the 18th Amendment: The Outlook for Provincial Finances Aisha Ghaus Pasha I would like to acknowledge the kind cooperation shown by a number of federal and provincial officials. Also, I thank Jose R. Lopez Claix and Hanid Mukhtar for their continuous guidance and support and all the participants at the World Bank workshop on the 18th Amendment held last June for their useful comments. 3 The Outlook for Provincial Finances 2011 ACRONYMS ADP Annual Development Programme AIT Agricultural -

Mlcf List of Shareholders As 30-09-2020 (Without CNIC)

Maple Leaf Cement Factory Limited Shareholders without CNIC Numbers as on 30-09-2020 Sr.No. Folio/CDC A/C# Share-holder's Name Address No of Shares 1 33 NIGHAT BANO L-428 SECTOR NO.4 NORTH KARACHI KARACHI 512 MRS. KULSUM BAI B-10, U.K. APPARTMENT, PHASE-I, GULSHAN-I-IQBAL, KARACHI. 44 2 35 AISHA ALI MOHAMMAD FLAT NO.4-B, MADINA MANSION, 4TH FLOOR, PLOT G.K. 2/14, 90 3 44 MOOSA STREET, KHARADAR, KARACHI. 4 49 ZAFER IQBAL BATT J.M 138/139 B-303 M.L HEIGHTS SOLDIER BAZAR KARACHI 110 5 84 MUHAMMAD ASIF KHAN 19/C BLOCK-6 P.E.C.H.S. KARACHI 1,188 6 85 SHAKIL AHMED 4/403 SHAH FAISAL COLONY KARACHI-25 196 7 117 MOHAMMAD ARSHID 19-HOOR CENTRE, NEAR CITY COURTS, KARACHI. 132 8 134 HAJRA BEGUM A541 BLOCK N NORTH NAZIMABAD KARACHI 132 9 137 SHAHID YAR KHAN 46-HASAN COLONY, NAZIMABAD, KARACHI. 44 MOHAMMAD IQBAL FLAT # A-15, AL-MUJAHID APARTMENT, 3RD FLOOR, MILLWALA 360 10 155 STREET, GARDEN WEST, KARACHI RAMZAN ALI C/O HASAN ALI BOOK DEPO, QASIER ZAINAB, NEAR BARA IMAM 148 11 234 BARA, KHARADHAR, KARACHI-74000. 12 244 NAJMA BR 1/40 FLAT NO.3 2ND FLOOR KHARADAR KARACHI 396 13 274 MUHAMMAD IBRAHIM 17-MOHAMMAD AFZAL BLDG. JINNAH STREET KARACHI 44 KANIZ FATIMA USMAN AHMED & CO. DADA CHAMBERS M.A JINNAH ROAD NEAR 16 14 285 M/W TOWER KARACHI A RAZZAK SR 9/43 MOHAMMADI MANSION 4TH FLOOR J.RAM STREET PAK 148 15 304 CHOWK KARACHI MOHAMMAD AYUB 92-B/II, SOUTH CIRCULAR AVENUE, DEFENCE, PHASE-II, KARACHI. -

Psdp 2010-2011

WATER & POWER DIVISION (WATER SECTOR) 0.823109275 (Million Rupees) Sl. Name, Location & Status of the Estimated Cost Expenditure Throw- Allocation for 2010-11 Allocation for 2011-12 Allocation for 2012-13 No Scheme Total Foreign upto June forward as on Foreign Loan Rupee Total Total Foreign Total Foreign Loan 2010 01-7-10 Loan Loan 1 2 3 4 5 6 7 8 9 10 11 12 13 On-going Schemes 1 Raising of Mangla Dam including 62553.000 0.000 78535.030 0.000 0.000 2469.328 2469.328 2469.328 0.000 0.000 0.000 resettlement 2 Mirani Dam 5861.000 0.000 4993.980 867.020 0.000 82.311 82.311 82.311 0.000 0.000 0.000 3 Sabakzai Dam Project 1960.820 0.000 1588.990 371.830 0.000 82.311 82.311 82.311 0.000 0.000 0.000 4 Satpara Multipurpose Dam 4480.020 554.680 2545.715 1934.305 0.000 164.622 164.622 164.622 0.000 200.000 0.000 5 Gomal Zam Dam 12829.000 4964.000 5431.380 7397.620 0.000 823.109 823.109 823.109 0.000 3000.000 0.000 6 Greater Thal Canal (Phase - I) 30467.000 0.000 8652.440 21814.560 0.000 200.000 200.000 740.798 0.000 1500.000 0.000 7 Kachhi Canal (Phase - I) 31204.000 0.000 23589.180 7614.820 0.000 2263.551 2263.551 2263.551 0.000 4000.000 0.000 8 Rainee Canal (Phase - I) 18861.580 0.000 8930.960 9930.620 0.000 1810.840 1810.840 1810.840 0.000 3000.000 0.000 9 Lower Indus Right Bank Irrigation & 14707.000 0.000 11783.080 2923.920 0.000 658.487 658.487 658.487 0.000 400.000 0.000 Drainage, Sindh 10 Balochistan Effluent Disposal into RBOD. -

Psdp 2009-2010

WATER & POWER DIVISION (WATER SECTOR) (Million Rupees) Sl. Name, Location & Status of the Estimated Cost Expenditure Throw- Allocation for 2009-10 No Scheme Total Foreign upto June forward as on Foreign Rupee Total Loan 2009 01-7-09 Loan 1 2 3 4 5 6 7 8 9 On-going Schemes 1 Raising of Mangla Dam including 101384.330 0.000 62204.003 39180.327 0.000 12000.000 12000.000 resettlement 2 Mirani Dam 5811.000 0.000 5247.260 563.740 0.000 313.740 313.740 3 Sabakzai Dam 2005.545 0.000 1488.990 516.555 0.000 280.000 280.000 4 Satpara Multipurpose Dam 4805.975 195.786 2193.998 2611.977 0.000 50.000 50.000 5 Gomal Zam Dam 12829.000 4964.000 2951.922 9877.078 0.000 2000.000 2000.000 6 Greater Thal Canal (Phase - I) 30467.109 0.000 7176.962 23290.147 0.000 1000.000 1000.000 7 Kachhi Canal (Phase - I) 31204.000 0.000 18625.016 12578.984 0.000 4000.000 4000.000 8 Rainee Canal (Phase - I) 18862.000 0.000 5051.287 13810.713 0.000 2000.000 2000.000 9 Lower Indus Right Bank Irrigation & 14707.143 0.000 10819.677 3887.466 0.000 1500.000 1500.000 Drainage, Sindh 10 Balochistan Effluent Disposal into RBOD. 6535.970 0.000 2548.353 3987.617 0.000 800.000 800.000 (RBOD-III) 11 Feasibility Studies of Dams (Naulong, 378.468 0.000 191.485 186.983 0.000 60.000 60.000 Hingol), Balochistan 12 Land and Water Monitoring / Evaluation 427.000 0.000 0.000 427.000 0.000 40.000 40.000 of Indus Plains (SMO) 13 Construction of IRSA Office building, 38.250 0.000 28.250 10.000 0.000 10.000 10.000 Islamabad 14 Revamping/Rehabilitation of Irrigation & 16796.000 0.000 8850.000 7946.000 -

ADP 2013-14, a Scheme to Provide “KIDS ROOMS” in 1000-Primary Schools Which Will Continue During This Financial Year As Well

GOVERNMENT OF THE PUNJAB MTDF 2013-16 DEVELOPMENT PROGRAMME 2013-14 Annual Development Programme 2013‐14 Abstract (Million Rs.) Page No Sector Type Capital Revenue Total F. Aid Total New 28,639.882 40,763.400 69,403.282 0.000 69,403.282 Social Sectors Ongoing 7,118.140 12,332.578 19,450.718 1,941.000 21,391.718 Total 35,758.022 53,095.978 88,854.000 1,941.000 90,795.000 New 7.000 14,774.000 14,781.000 0.000 14,781.000 School Education Ongoing 24.965 694.035 719.000 0.000 719.000 Total 31.965 15,468.035 15,500.000 0.000 15,500.000 New 2,428.000 979.000 3,407.000 0.000 3,407.000 Higher Education Ongoing 2,443.294 819.706 3,263.000 0.000 3,263.000 Total 4,871.294 1,798.706 6,670.000 0.000 6,670.000 New 732.546 172.454 905.000 0.000 905.000 Special Education Ongoing 171.824 63.176 235.000 0.000 235.000 Total 904.370 235.630 1,140.000 0.000 1,140.000 New 0.000 605.000 605.000 0.000 605.000 Literacy Ongoing 0.000 1,000.000 1,000.000 0.000 1,000.000 Total 0.000 1,605.000 1,605.000 0.000 1,605.000 New 1,332.000 0.000 1,332.000 0.000 1,332.000 Sports & Youth Ongoing 623.000 20.000 643.000 0.000 643.000 Affairs Total 1,955.000 20.000 1,975.000 0.000 1,975.000 New 1,715.151 6,592.547 8,307.698 0.000 8,307.698 Health & Family Ongoing 3,784.006 4,908.296 8,692.302 0.000 8,692.302 Planinig Total 5,499.157 11,500.843 17,000.000 0.000 17,000.000 New 0.000 8,056.500 8,056.500 0.000 8,056.500 Water Supply & Ongoing 0.000 2,811.500 2,811.500 0.000 2,811.500 Sanitation Total 0.000 10,868.000 10,868.000 0.000 10,868.000 New 728.185 1,033.899 1,762.084 0.000