View Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Swale Borough Council

SWALE BOROUGH COUNCIL Project: RETAIL STUDY 2010: Bulky and DIY Goods Addendum Latest Revision: 20/05/2011 - DRAFT Study area population by zone Zone 2010 2015 2020 2025 1 39,501 40,410 41,418 42,595 2 12,888 13,185 13,514 13,897 3 46,052 47,112 48,287 49,659 4 11,242 11,501 11,788 12,123 5 19,162 19,603 20,092 20,663 6 5,340 5,463 5,599 5,758 TOTAL 134,185 137,274 140,698 144,695 Sources/notes for frontispiece 1. 2010 population for each zone from Pitney Bowes Business Insight Area Profile Report (6 July 2010) 2. Growth in population based on growth rates implied by scenarioKent County 3 of Council 6 scenarios population prepared forecasts by Research for Swale & Intelligence, Borough - South Kent CouEastntyPlan Council Strategy (16- Septemberbased Forecasts 2010). (September The KCC projections 2009) Total are Population based on SwaleForecasts. Borough Available: Counciil's 'Option 1' for newhttps://shareweb.kent.gov.uk/Documents/facts homes which assumes an additional 13,503-and dwellings-figures/sep between-forecasts 2006-sep-2031-09 -usingweb.pdf a phasing Access provideddate: 12 byOctober SBC 2010 OTHER COMPARISON GOODS Table 3.1 Expenditure per capita (£) Zone 2007 2010 2015 2020 2025 1 2,062 2,162 2,592 3,124 3,764 2 2,356 2,470 2,962 3,569 4,301 3 2,164 2,269 2,721 3,278 3,950 4 2,336 2,449 2,937 3,539 4,264 5 2,194 2,300 2,758 3,324 4,005 6 2,347 2,460 2,951 3,555 4,284 Sources/notes for Table 3.1 1. -

Download Our Operating and Portfolio Review

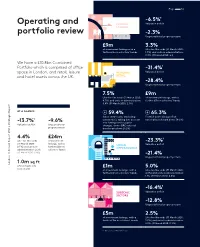

Page 36 -6.5%1 Operating and CENTRAL Valuation deficit LONDON portfolio review -2.3% Ungeared total property return £9m 3.3% of investment lettings with a Like-for-like voids (31 March 2020: further £1m in solicitors’ hands 1.3%) and units in administration: 0.3% (31 March 2020: nil) We have a £10.8bn Combined Portfolio which is comprised of office -31.4%1 space in London, and retail, leisure REGIONAL Valuation deficit and hotel assets across the UK. RETAIL -28.4% Ungeared total property return 7.5% £9m Like-for-like voids (31 March 2020: of investment lettings, with a 4.7%) and units in administration: further £7m in solicitors’ hands 5.8% (31 March 2020: 2.1%) AT A GLANCE 59.4% 65.3% Same centre sales (excluding Footfall down (ShopperTrak ¹ automotive), taking into account national benchmark down 58.2%) -13.7% -9.6% new lettings and occupier Valuation deficit Ungeared total changes, down (BRC national » Strategic Report property return benchmark down 29.2%) 4.4% £24m Like-for-like voids of investment -23.3%1 (31 March 2020: lettings, with a URBAN Valuation deficit 2.5%) and units in further £12m in OPPORTUNITIES administration: 2.2% solicitors’ hands (31 March 2020: 0.8%) -21.4% Ungeared total property return 1.0m sq ft Landsec // AnnualLandsec Report // 2021 of developments £1m 5.0% now on site of investment lettings, with a Like-for-like voids (31 March 2020: further £1m in solicitors’ hands 4.8%) and units in administration: 1.1% (31 March 2020: 0.4%) -16.4%1 SUBSCALE Valuation deficit SECTORS -12.8% Ungeared total property return £5m 2.5% of investment lettings, with a Like-for-like voids (31 March 2020: further £3m in solicitors’ hands 2.0%) and units in administration: 2.9% (31 March 2020: 0.9%) 1. -

Regeneration and Economic Development Policy Overview and Scrutiny Committee

KENT COUNTY COUNCIL REGENERATION AND ECONOMIC DEVELOPMENT POLICY OVERVIEW AND SCRUTINY COMMITTEE MINUTES of a meeting of the Regeneration and Economic Development Policy Overview and Scrutiny Committee held in the Council Chamber, Sessions House, County Hall, Maidstone on Wednesday, 17 November 2010. PRESENT: Mr M C Dance (Chairman), Mr I S Chittenden (Vice-Chairman), Mr A R Chell, Mr K A Ferrin, MBE, Mr P J Homewood, Mrs J P Law, Mr K H Pugh, Mrs J A Rook, Mr K Smith, Mr M V Snelling and Mrs E M Tweed ALSO PRESENT: Mr K G Lynes, Mr M J Whiting and Mr M A Wickham IN ATTENDANCE: Mr D Cockburn (Executive Director, Strategy, Economic Development & ICT), Mr N Smith (Head of Development Investment), Mr M Bodkin (Head of Urban Regeneration), Mrs T Bruton (Head of Regeneration Projects) and Miss T Grayell (Democratic Services Officer) UNRESTRICTED ITEMS 45. Minutes of the meeting held on 23 September 2010 (Item A3) RESOLVED that the Minutes of the meeting held on 23 September 2010 are correctly recorded and that they be signed by the Chairman. 46. Update on District Visits (Item B1) Mr M J Whiting, Member for Swale Central, was present for this item and spoke on it with the permission of the Chairman. Mr M Bodkin, Head of Urban Regeneration, Mrs T Bruton, Head of Regeneration Projects, Mr P Campion, Development Contributions Manager, Mrs H Coleman, Economic Development Manager, Mr R Hancock, Regeneration and Projects Manager, Mr D Hughes, Regeneration and Projects Manager, Mr I Lewis, Growth Areas Manager, and Mr K Mackenney, Regeneration and Projects Manager, were in attendance for this item. -

Seele Project Map London

projects in london Current and completed seele-projects, you may visit in and around London. Madame Toussauds 01 36 37 41 Royal Albert Hall 39 40 42 Victoria & Albert Museum 13 British Museum 12 Buckingham Palace 38 Houses of Parliament 11 27 31 34 16 07 08 02 21 46 23 14 Westminster Abbey 17 26 28 22 06 09 18 15 19 25 29 32 London Eye 03 20 24 St Paul's Cathedral 33 43 30 44 Imperial War Museum 05 Tower of London 35 45 04 10 projects in london Current and completed seele-projects, you may visit in and around London. 01 Hendon Quadrangle (university) 10 Wimbledon No. 1 Court (tennis stadium) 19 Unilever House (office building) 28 19 – 31 Moorgate (office building) 36 intu Watford (shopping centre) 45 Cutty Sark (museum) steel-and-glass roof, lift enclosure, post-and-beam construction, atrium, glass fibre construction, unitised façade made out of steel-and-glass gridshell roof steel-and-glass enclosure of the gallery and staircase balustrades balustrades, door systems glazed west façade, roofing stone, glass and aluminium www.watford-shopping.co.uk hull www.mdx.ac.uk www.wimbledon.com www.unilever.com reception open to the public Watford High Street (Train) www.rmg.co.uk/cutty-sark Hendon Central Wimbledon Park reception open to the public Moorgate / Bank 210 Queen St, Watford Cutty Sark The Burroughs Church Rd, Wimbledon City Thameslink 19 – 31 Moorgate King William Walk / Greenwich se-austria / 2005 se-austria / 2019 seele GmbH / 2007 100 Victoria Embankment se-austria / 2002 se-austria / 2018 se-austria / 2012 02 Westfield (shopping -

Archaeological Evaluation Report Westwood Cross, Thanet Kent

Archaeology South-East ASE Archaeological Evaluation Report Westwood Cross, Thanet Kent NGR: TR 36455 67441 Planning Ref: F/TH/12/0781 ASE Project No: 6729 Site Code: TWE14 ASE Report No: 2014159 OASIS id: archaeol6-179227 Catherine Douglas Archaeological Evaluation Report Westwood Cross, Thanet Kent NGR: TR 36455 67441 Planning Ref: F/TH/12/0781 ASE Project No: 6729 Site Code: TWE14 ASE Report No: 2014159 OASIS id: archaeol6-179227 Catherine Douglas With contributions by Anna Doherty and Karine Le Hégarat Illustrations by Justin Russell May 2014 Archaeology South-East Units 1 & 2 2 Chapel Place Portslade East Sussex BN41 1DR Tel: 01273 426830 Fax: 01273 420866 Email: [email protected] Archaeology South-East Eval: Westwood Cross, Thanet, Kent ASE Report No: 2014159 Abstract Archaeology South-East was commissioned by CgMs Ltd, to undertake an archaeological evaluation by trial trenching on land at Westwood Cross, Thanet, Kent. Five trenches were excavated. A single undated post hole containing a piece of struck flint was identified in Trench 2, and a sherd of medieval pottery was retrieved from the topsoil in Trench 5. Some degree of modern truncation was identified in Trench 1, but the paucity of archaeology in the other trenches and the survival of an intact subsoil horizon suggest a lack of past activity on the site. © Archaeology South-East UCL i Archaeology South-East Eval: Westwood Cross, Thanet, Kent ASE Report No: 2014159 CONTENTS 1.0 Introduction 2.0 Archaeological Background 3.0 Archaeological Methodology 4.0 Results 5.0 The Finds -

Limited and Guild Realisations Limited (Formerly Republic (Retail) Limited) - Both in Administration (Together ‘The Companies’)

Ernst & Young LLP 1 Bridgewater Place, Water Lane Leeds LS11 5QR T el: 0113 298 2200 Fax: 0113 298 2201 www.ey.com/uk TO ALL KNOWN CREDITORS 8 April 2013 Ref: RHK/JPS/TRJ/AE/PCF11.1 Direct line: 0113 298 2496 Direct fax: 0113 298 2206 Email: [email protected] Dear Sirs Republic (UK) Limited and Guild Realisations Limited (formerly Republic (Retail) Limited) - both in Administration (together ‘the Companies’) Further to my appointment as Joint Administrator of the Companies, I attach a copy of my statement of proposals in accordance with paragraph 49 of Schedule B1 to the Insolvency Act 1986. As you will note from the proposals, there is no prospect of any funds becoming available to unsecured creditors of either of the Companies other than by virtue of the prescribed part. As a consequence, I do not propose to summon meetings of creditors. If, however, creditors whose debts amount to at least 10% of total debts of either of the Companies make a request in the prescribed form within 8 business days of these proposals being sent out, a meeting will be held in that company. Copies of the prescribed form (Form 2.21B) are enclosed in case you wish to request a meeting. I would draw your attention to the provisions of Rule 2.37 of the Insolvency Rules 1986 which provide that if a meeting is requested, it will only be held if the expenses of summoning and holding such a meeting are paid by the creditor or creditors making the request and if security is first deposited with me for payment. -

Web List.Xlsx

WELSH STORE CLOSURES Store Address CLOSE DATE Aberdare The Works, 2 & 3 Commercial Street, Aberdare, CF44 7RW Closed from Sunday 20th December Abergavenny TheWorks.co.uk, Unit 3, Cibi Shopping Centre, Abergavenny, NP7 5AJ Closed from Sunday 20th December Aberystwyth The Works, 35 Terrace Road, Aberystwyth, SY23 2AE Closed from Sunday 20th December Bangor The Works, 241 High Street, Bangor, LL57 1PA Closed from Sunday 20th December Barry The Works, Unit 4, 110-118 Holton Road, Barry, CF63 4HH Closed from Sunday 20th December Brecon TheWorks.co.uk, Unit 14/15, Bethel Square Shopping Centre, Brecon, LD3 7JP Closed from Sunday 20th December Bridgend TheWorks.co.uk, 22 Adare Street, Bridgend, CF31 1EJ Closed from Sunday 20th December Bridgend Outlet TheWorks.co.uk, Unit 86a, Welsh Designer Village, Pen-Y-Cae, Bridgend, CF32 9SU Closed from Sunday 20th December Caernarfon The Works, 11 Pool Street, Caernarfon, LL55 2AD Closed from Sunday 20th December Caerphilly TheWorks.co.uk, Unit 8, Castle Court Shopping Centre, Caerphilly, CF83 1NU Closed from Sunday 20th December Cardiff Queens Street The Works, 16 Queens Street, Cardiff, CF10 2BU Closed from Sunday 20th December Cardigan The Works, 7 / 8 High Street, Cardigan, SA43 1HJ Closed from Sunday 20th December Carmarthen The Works, 11 Pool Street, Caernarfon, LL55 2AD Closed from Sunday 20th December Colwyn Bay The Works, 11 Bay View Centre, Sea View Road, Colwyn Bay, LL29 8DG Closed from Sunday 20th December Cwmbran TheWorks.co.uk, 2-4 The Parade, Cwmbran Shopping Centre, Cwmbran, NP44 1PT Closed -

Loyola University New Orleans Study Abroad

For further information contact: University of East London International Office Tel: +44 (0)20 8223 3333 Email: [email protected] Visit: uel.ac.uk/international Docklands Campus University Way London E16 2RD uel.ac.uk/international Study Abroad uel.ac.uk/international Contents Page 1 Contents Page 2 – 3 Welcome Page 4 – 5 Life in London Page 6 – 9 Docklands Campus Page 10 – 11 Docklands Page 12 – 15 Stratford Campus Page 16 – 17 Stratford Page 18 – 19 London Map Page 20 – 21 Life at UEL Page 23 Study Abroad Options Page 25 – 27 Academic School Profiles Page 28 – 29 Practicalities Page 30 – 31 Accommodation Page 32 Module Choices ©2011 University of East London Welcome This is an exciting time for UEL, and especially for our students. With 2012 on the horizon there is an unprecedented buzz about East London. Alongside a major regeneration programme for the region, UEL has also been transformed. Our £170 million campus development programme has brought a range of new facilities, from 24/7 multimedia libraries and state-of-the-art clinics,to purpose-built student accommodation and, for 2011, a major new sports complex. That is why I am passionate about our potential to deliver outstanding opportunities to all of our students. Opportunities for learning, for achieving, and for building the basis for your future career success. With our unique location, our record of excellence in teaching and research, the dynamism and diversity provided by our multinational student community and our outstanding graduate employment record, UEL is a university with energy and vision. I hope you’ll like what you see in this guide and that you will want to become part of our thriving community. -

Sustainability Report 2017

Sustainability Report 2017 Making our experience count Progress Commitments Sustainability Complete Existing commitment (retained) On track Existing commitment (extended) performance Incomplete New commitment at a glance Our commitments and progress to date Creating jobs and opportunities Community employment Fairness Diversity Health, safety and security Commitment Commitment Commitment Commitment Help a total of 1,200 Ensure the working environments Make measurable improvements Maintain an exceptional standard disadvantaged people we control are fair and ensure that to the profile – in terms of gender, of health, safety and security secure jobs by 2020 everyone who is working on our ethnicity and disability – of our in all the working environments behalf – within an environment we employee mix we control Progress control – is paid at least the Living Wage by 2020 Progress Progress Employment secured for 962 people from Progress Participant in the National Chaired the Health in disadvantaged backgrounds Equality Standard assessment Construction Leadership Group Accreditation received from the process. Set specific diversity and launched Mates in Mind Living Wage Foundation metrics to be achieved by 2020 mental health programme Efficient use of natural resources Carbon Renewable energy Energy Waste Commitment Commitment Commitment Commitment Reduce carbon intensity (kgCO2/ Continue to procure 100% Reduce energy intensity (kWh/ Send zero waste to landfill with m2) by 40% by 2030 compared to renewable electricity across m2) by 40% by 2030 -

West India Quay 1901

WEST INDIA QUAY NEAR CANARY WHARF • E14 WEST INDIA QUAY NEAR CANARY WHARF • E14 This bright two bedroom duplex apartment facing South and West is located on the nineteenth and twentieth floors of a striking modern development and provides breath taking views towards London and the City skyline. There is one secure parking space. Master bedroom with en suite • 2nd bedroom with en suite reception room • kitchen • guest WC • concierge • private parking Guide price: £1,499,995 Tenure: Leasehold Local authority: London Borough of Tower Hamlets These particulars are intended only as a guide and must not be relied upon as statements of fact. Your attention is drawn to the Important Notice on the last page of the text. Description of Property A superbly presented duplex apartment extending to 206.7 sq m ﴾2,225 sq ft﴿. Entered via an entrance hall with a guest WC, the apartment offers a substantial South and West facing reception room with a dining area which benefits from having a double height ceiling and providing sensational far reaching views towards the iconic City skyline from floor to ceiling windows. The modern open‐ plan kitchen offers integrated appliances and a breakfast bar. There are stairs leading to an upper landing which is ideal for use as a study area, which in turn gives access to both bedrooms. The master bedroom suite extends to 37 ft in length providing ample space and has a dressing area with fitted wardrobes and access to an ensuite bathroom. The generous second bedroom also benefits from fitted wardrobes and access to an ensuite bathroom. -

34 Bus Time Schedule & Line Route

34 bus time schedule & line map 34 Birchington-On-Sea View In Website Mode The 34 bus line (Birchington-On-Sea) has 6 routes. For regular weekdays, their operation hours are: (1) Birchington-On-Sea: 8:20 PM - 9:20 PM (2) Margate: 5:18 AM - 2:03 PM (3) Margate: 6:57 AM (4) Minnis Bay: 6:30 AM - 5:48 PM (5) Ramsgate: 5:58 AM - 6:07 PM (6) Westwood: 6:51 PM Use the Moovit App to ƒnd the closest 34 bus station near you and ƒnd out when is the next 34 bus arriving. Direction: Birchington-On-Sea 34 bus Time Schedule 16 stops Birchington-On-Sea Route Timetable: VIEW LINE SCHEDULE Sunday Not Operational Monday 8:20 PM - 9:20 PM Cecil Square, Margate Cecil Square, Margate Tuesday 8:20 PM - 9:20 PM Marine Terrace, Margate Wednesday 8:20 PM - 9:20 PM Hall by the Sea Road, Margate Thursday 8:20 PM - 9:20 PM Nayland Rock, Westbrook Friday 8:20 PM - 9:20 PM Albert Road, Margate Saturday 8:20 PM - 9:20 PM Royal Sea Bathing, Westbrook 77 Canterbury Road, Margate Waverley Road, Garlinge 34 bus Info The Hussar, Garlinge Direction: Birchington-On-Sea 221 Canterbury Road, Margate Stops: 16 Trip Duration: 14 min St James' Park Road, Garlinge Line Summary: Cecil Square, Margate, Marine 218 Canterbury Road, Margate Terrace, Margate, Nayland Rock, Westbrook, Royal Sea Bathing, Westbrook, Waverley Road, Garlinge, Walmer Castle, Westgate-On-Sea The Hussar, Garlinge, St James' Park Road, Garlinge, Canterbury Road, Margate Walmer Castle, Westgate-On-Sea, Library, Westgate- On-Sea, Domneva Road, Westgate-On-Sea, Hengist Library, Westgate-On-Sea Road, Birchington-On-Sea, -

Leisure Savills

SAVILLS PROPERTY MANAGEMENT LEISURE savills.co.uk 3 SAVILLS PROPERTY MANAGEMENT: LEISURE INTRODUCTION We are Savills Leisure Property Management, the UK’s leading leisure property management service provider. Acting for a range of landlords, our portfolio comprises premier indoor and outdoor leisure schemes throughout the UK, including centres, parks and out of town retail. We provide leisure-specific property management services, from core functions through to consultancy and place shaping initiatives. We act as an extension to our clients’ team; onboarding objectives, addressing challenges, offering guidance and presenting solutions to compliment the overall strategy. LEISURE-SPECIFIC SERVICE DELIVERY We believe that leisure-focused property management is fundamental to the success of a scheme and its stakeholders. We have developed specialised, sector-specific capabilities such as service charge benchmarking, tenant compliance audits, footfall reporting, customer journey and tenant trade analysis, and waste management and environmental reporting. Furthermore, we understand the importance of occupier relations. We have long-term working relationships with key national leisure tenants, maintained through active relationship management and engagement. WE GO FURTHER THAN MOST Our expertise in leisure property management transcends functional service delivery. We work with the end user front of mind to ensure our clients’ spaces are best in class. We use and develop the latest technologies to understand performance metrics to aid decision-making