Private Equity Capital Briefing Monthly Insights and Intelligence on PE Trends

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Listing of PSERS' Investment Managers, Advisors, and Partnerships

Pennsylvania Public School Employees’ Retirement System Roster of Investment Managers, Advisors, and Consultants As of March 31, 2015 List of PSERS’ Internally Managed Investment Portfolios • Bloomberg Commodity Index Overlay • Gold Fund • LIBOR-Plus Short-Term Investment Pool • MSCI All Country World Index ex. US • MSCI Emerging Markets Equity Index • Risk Parity • Premium Assistance • Private Debt Internal Program • Private Equity Internal Program • Real Estate Internal Program • S&P 400 Index • S&P 500 Index • S&P 600 Index • Short-Term Investment Pool • Treasury Inflation Protection Securities • U.S. Core Plus Fixed Income • U.S. Long Term Treasuries List of PSERS’ External Investment Managers, Advisors, and Consultants Absolute Return Managers • Aeolus Capital Management Ltd. • AllianceBernstein, LP • Apollo Aviation Holdings Limited • Black River Asset Management, LLC • BlackRock Financial Management, Inc. • Brevan Howard Asset Management, LLP • Bridgewater Associates, LP • Brigade Capital Management • Capula Investment Management, LLP • Caspian Capital, LP • Ellis Lake Capital, LLC • Nephila Capital, Ltd. • Oceanwood Capital Management, Ltd. • Pacific Investment Management Company • Perry Capital, LLC U.S. Equity Managers • AH Lisanti Capital Growth, LLC Pennsylvania Public School Employees’ Retirement System Page 1 Publicly-Traded Real Estate Securities Advisors • Security Capital Research & Management, Inc. Non-U.S. Equity Managers • Acadian Asset Management, LLC • Baillie Gifford Overseas Ltd. • BlackRock Financial Management, Inc. • Marathon Asset Management Limited • Oberweis Asset Management, Inc. • QS Batterymarch Financial Management, Inc. • Pyramis Global Advisors • Wasatch Advisors, Inc. Commodity Managers • Black River Asset Management, LLC • Credit Suisse Asset Management, LLC • Gresham Investment Management, LLC • Pacific Investment Management Company • Wellington Management Company, LLP Global Fixed Income Managers U.S. Core Plus Fixed Income Managers • BlackRock Financial Management, Inc. -

Preqin Research Report Fig

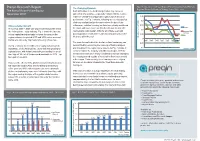

Preqin Research Report Fig. 3 Comparison of Private Equity Performance by Fund Primary The Changing Dynamic Regional Focus for Funds of Vintage Years 1995 - 2007 The Rise of Asian Private Equity Such diffi culties in the fundraising market may come as November 2010 somewhat of a surprise – especially considering the relative resilience of Asia-focused private equity funds in terms of 0.25 performance. As Fig. 3 shows, following an extended period 0.2 of strong median fund performance since the turn of the Unprecedented Growth millennium, vehicles focusing on Asia have clearly weathered 0.15 the storm with more success than their European and US Europe The period 2003 – 2008 saw unprecedented growth within 0.1 the Asian private equity industry. Fig. 1 shows the increase counterparts, with median IRRs for all vintage years still Asia and Rest of World posting positive results while funds focusing primarily on the 0.05 in total capital raised annually by funds focusing on the US region between the period 2003 and 2008, when a record West are still in the red. IRR Median Net-to-LP 0 $91bn was raised by 194 funds achieving a fi nal close. 1995 1997 1999 2001 2003 2005 2007 The main factors behind the decline in Asia fundraising can -0.05 As Fig. 2 shows, the record level of capital raised saw the be identifi ed by examining the make-up of fund managers -0.1 Vintage Year importance of the Asian private equity industry growing on and investors in the region more closely. As Fig. -

VP for VC and PE.Indd

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION A guide to Venture PhilAnthroPy for Venture Capital and Private Equity investors Ashley Metz CummingS and Lisa Hehenberger JUNE 2011 2 A guidE to Venture Philanthropy for Venture Capital and Private Equity investors LETTER fROM SERgE RAICHER 4 Part 2: PE firms’ VP engAgement 20 ContentS Executive Summary 6 VC/PE firms and Philanthropy PART 1: Introduction 12 Models of engagement in VP Purpose of the document Model 1: directly support Social Purpose Organisations Essence and Role of Venture Philanthropy Model 2: Invest in or co-invest with a VP Organisation Venture Philanthropy and Venture Capital/Private Equity Model 3: found or co-found a VP Organisation Published by the European Venture Philanthropy Association This edition June 2011 Copyright © 2011 EVPA Email : [email protected] Website : www.evpa.eu.com Creative Commons Attribution-Noncommercial-No derivative Works 3.0 You are free to share – to copy, distribute, display, and perform the work – under the following conditions: Attribution: You must attribute the work as A gUIdE TO VENTURE PHILANTHROPY fOR VENTURE CAPITAL ANd PRIVATE EqUITY INVESTORS Copyright © 2011 EVPA. Non commercial: You may not use this work for commercial purposes. No derivative Works: You may not alter, transform or build upon this work. for any reuse or distribution, you must make clear to others the licence terms of this work. ISbN 0-9553659-8-8 Authors: Ashley Metz Cummings and dr Lisa Hehenberger Typeset in Myriad design and typesetting by: Transform, 115b Warwick Street, Leamington Spa CV32 4qz, UK Printed and bound by: drukkerij Atlanta, diestsebaan 39, 3290 Schaffen-diest, belgium This book is printed on fSC approved paper. -

Private Equity 05.23.12

This document is being provided for the exclusive use of SABRINA WILLMER at BLOOMBERG/ NEWSROOM: NEW YORK 05.23.12 Private Equity www.bloombergbriefs.com BRIEF NEWS, ANALYSIS AND COMMENTARY CVC Joins Firms Seeking Boom-Era Size Funds QUOTE OF THE WEEK BY SABRINA WILLMER CVC Capital Partners Ltd. hopes its next European buyout fund will nearly match its predecessor, a 10.75 billion euro ($13.6 billion) fund that closed in 2009, according to two “I think it would be helpful people familiar with the situation. That will make it one of the largest private equity funds if Putin stopped wandering currently seeking capital. One person said that CVC European Equity Partners VI LP will likely aim to raise 10 around bare-chested.” billion euros. The firm hasn’t yet sent out marketing materials. Two people said they expect it to do so — Janusz Heath, managing director of in the second half. Mary Zimmerman, an outside spokeswoman for CVC Capital, declined Capital Dynamics, speaking at the EMPEA to comment. conference on how Russia might help its reputation and attract more private equity The London-based firm would join only a few other firms that have closed or are try- investment. See page 4 ing to raise new funds of similar size to the mega funds raised during the buyout boom. Leonard Green & Partners’s sixth fund is expected to close shortly on more than $6 billion, more than the $5.3 billion its last fund closed on in 2007. Advent International MEETING TO WATCH Corp. is targeting 7 billion euros for its seventh fund, larger than its last fund, and War- burg Pincus LLC has a $12 billion target on Warburg Pincus Private Equity XI LP, the NEW JERSEY STATE INVESTMENT same goal as its predecessor. -

ANNUAL REVIEW 2017 Land of the Giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus

ANNUAL REVIEW 2017 Land of the giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus Ares Management is honored to be recognized as Lender of the Year in North America for the fourth consecutive year as well as Lender of the Year in Europe Lender of the year in Europe Ares Management, L.P. (NYSE: ARES) is a leading global alternative asset manager with approximately $106 billion of AUM1 and offices throughout the United States, Europe, Asia and Australia. With more than $70 billion in AUM1 and approximately 235 investment professionals, the Ares Credit Group is one of the largest global alternative credit managers across the non-investment grade credit universe. Ares is also one of the largest direct lenders to the U.S. and European middle markets, operating out of twelve office locations in both geographies. Note: As of December 31, 2017. The performance, awards/ratings noted herein may relate only to selected funds/strategies and may not be representative of any client’s given experience and should not be viewed as indicative of Ares’ past performance or its funds’ future performance. 1. AUM amounts include funds managed by Ivy Hill Asset Management, L.P., a wholly owned portfolio company of Ares Capital Corporation and a registered investment adviser. learn more at: www.aresmgmt.com | www.arescapitalcorp.com The battle of the brands the US market on page 80, advisor Hamilton TOBY MITCHENALL Lane said it had received a record number EDITOR'S of private placement memoranda in 2017 – ISSN 1474–8800 LETTER MARCH 2018 around 800 – and that this, combined with Senior Editor, Private Equity faster fundraising processes, has made it dif- Toby Mitchenall, Tel: +44 207 566 5447 [email protected] ficult to some investors to make considered Special Projects Editor decisions. -

The Private Equity Review the Private Equity Review

The Private Equity Review The Private Equity Review Fourth Edition Editor Stephen L Ritchie Law Business Research The Private Equity Review The Private Equity Review Reproduced with permission from Law Business Research Ltd. This article was first published in The Private Equity Review - Edition 4 (published in March 2015 – editor Stephen L Ritchie). For further information please email [email protected] The Private Equity Review Fourth Edition Editor Stephen L Ritchie Law Business Research Ltd PUBLISHER Gideon Roberton BUSINESS DEVELOPMENT MANAGER Nick Barette SENIOR ACCOUNT MANAGERS Katherine Jablonowska, Thomas Lee ACCOUNT MANAGER Felicity Bown PUBLISHING COORDINATOR Lucy Brewer MARKETING ASSISTANT Dominique Destrée EDITORIAL COORDINATOR Shani Bans HEAD OF PRODUCTION Adam Myers PRODUCTION EDITOR Anne Borthwick SUBEDITOR Janina Godowska MANAGING DIRECTOR Richard Davey Published in the United Kingdom by Law Business Research Ltd, London 87 Lancaster Road, London, W11 1QQ, UK © 2015 Law Business Research Ltd www.TheLawReviews.co.uk No photocopying: copyright licences do not apply. The information provided in this publication is general and may not apply in a specific situation, nor does it necessarily represent the views of authors’ firms or their clients. Legal advice should always be sought before taking any legal action based on the information provided. The publishers accept no responsibility for any acts or omissions contained herein. Although the information provided is accurate as of March 2015, be advised that this is -

PEI June2020 PEI300.Pdf

Cover story 20 Private Equity International • June 2020 Cover story Better capitalised than ever Page 22 The Top 10 over the decade Page 24 A decade that changed PE Page 27 LPs share dealmaking burden Page 28 Testing the value creation story Page 30 Investing responsibly Page 32 The state of private credit Page 34 Industry sweet spots Page 36 A liquid asset class Page 38 The PEI 300 by the numbers Page 40 June 2020 • Private Equity International 21 Cover story An industry better capitalised than ever With almost $2trn raised between them in the last five years, this year’s PEI 300 are armed and ready for the post-coronavirus rebuild, writes Isobel Markham nnual fundraising mega-funds ahead of the competition. crisis it’s better to be backed by a pri- figures go some way And Blackstone isn’t the only firm to vate equity firm, particularly and to towards painting a up the ante. The top 10 is around $30 the extent that it is able and prepared picture of just how billion larger than last year’s, the top to support these companies, which of much capital is in the 50 has broken the $1 trillion mark for course we are,” he says. hands of private equi- the first time, and the entire PEI 300 “The businesses that we own at Aty managers, but the ebbs and flows of has amassed $1.988 trillion. That’s the Blackstone that are directly affected the fundraising cycle often leave that same as Italy’s GDP. Firms now need by the pandemic, [such as] Merlin, picture incomplete. -

Charles Hayes

Charles Hayes Co-head of Financial Sponsors Group and Partner Corporate and M&A He is universally viewed as a rising talent in the context of high-end private equity deals. Some of the firm's most significant financial sponsor clients benefit from his 'fantastic' expertise. Chambers 2020 Primary practice Corporate and M&A 01/10/2021 Charles Hayes | Freshfields Bruckhaus Deringer About Charles Hayes <p><strong>Charles is global co-head of our financial sponsors group.</strong> <strong>He specialises in high-profile and complex acquisitions, carve-outs, take-privates and exits for some of the world’s largest financial sponsors.</strong></p> <p>Charles is sought after by clients who value his technical and commercial excellence on a full range of financial sponsor deal types. He works across sectors, specialising in financial services, media and healthcare. He has also advised on a number of high-profile sports investments.</p> <p>His client base covers global private equity houses, pension funds, sovereign wealth funds and corporates. Having spent time on secondment with Goldman Sachs and in Freshfields’ MENA offices, Charles has a thorough understanding of the needs of our global financial sponsor clients.</p> <p>Charles speaks English, French and German.</p> Recent work <ul> <li>Advising <strong>CVC Capital Partners </strong>on its participation with Fédération de Internationale Volleyball (“FIVB”) and partnership in Volleyball World.</li> <li>Advising <strong>GIC </strong>on an investment made -

Private Equity-Style Investing in Public Markets

Private Equity-Style Investing in Public Markets I had the pleasure of speaking with Adrian Warner, chief investment officer of Sydney-based Avenir Capital a few years ago. Adrian shared his insights into public equity investing with a private equity mindset. In doing so, Adrian drew upon more than two decades of experience as a private equity investor in the U.S. and Australia. The following transcript has been edited for space and clarity. John Mihaljevic, MOI Global: Adrian Warner has a background in private equity and was highly successful in that field prior to starting Sydney, Australia-based Avenir Capital, a value-oriented investment firm in public markets. Adrian, tell us about your path and what motivated you to make the switch from private to public equity. Adrian Warner, Avenir Capital: I’ve spent close to 20 years in the private equity industry, both in Australia and in the US. I started out in the early 1990s after spending some years at Bain & Co in consulting. I finished my education in the 1980s, when the efficient market hypothesis was at its peak. I did a First-Class Honors degree in finance, having it drilled into me very firmly that public markets were efficient, and there was no way to effectively beat them over the long term. With that backdrop, I sought otherwise to apply investing in markets I felt were less efficient. Private equity in the early 1990s was such a place. It was still a fairly small and under-the-radar industry, and there were great opportunities there to hunt down businesses available for much less than I felt they were worth. -

OPERF Private Equity Portfolio

Oregon Public Employees Retirement Fund Private Equity Portfolio As of December 31, 2019 ($ in millions) Vintage Capital Total Capital Total Capital Fair Market Total Value Partnership IRR2 Year Commitment Contributed Distributed Value Multiple 1,2 2000 2000 Riverside Capital Appreciation Fund $50.0 $45.7 $80.4 $0.0 1.80x 19.1% 2003 2003 Riverside Capital Appreciation Fund $75.0 $80.7 $157.2 $0.0 2.06x 17.2% 2012 A&M Capital Partners $100.0 $68.8 $82.9 $50.2 2.16x 28.8% 2018 A&M Capital Partners Europe I $151.5 $17.9 $0.0 $13.4 0.75x NM 2018 A&M Capital Partners II $200.0 $33.5 $0.0 $32.9 0.98x NM 2016 ACON Equity Partners IV $112.5 $58.9 $7.7 $42.4 0.83x ‐10.8% 2019 Advent Global Technology $50.0 $0.0 $0.0 ($0.6) 0.00x NM 2019 Advent International GPE IX $100.0 $11.5 $0.0 $10.4 0.91x NM 2008 Advent International GPE VI A $100.0 $100.0 $195.2 $15.8 2.11x 16.8% 2012 Advent International GPE VII C $50.0 $47.1 $45.7 $39.7 1.82x 15.7% 2015 Advent Latin American Private Equity Fund VI C $75.0 $56.8 $15.0 $61.4 1.35x 17.3% 2019 Advent Latin American Private Equity Fund VII $100.0 $0.0 $0.0 $0.0 0.00x NM 2018 AEP IV OPERS Co‐Investments $37.5 $21.5 $0.0 $24.9 1.15x NM 2006 Affinity Asia Pacific Fund III $100.0 $95.3 $124.6 $10.9 1.42x 9.0% 2007 Apax Europe VII $199.5 $220.7 $273.6 $6.0 1.29x 4.5% 2016 Apax IX $250.0 $231.0 $6.6 $317.6 1.42x NM 2012 Apax VIII‐B $150.4 $158.8 $149.7 $115.5 1.70x 14.9% 2018 Apollo Investment Fund IX $480.0 $88.4 $0.9 $77.8 0.89x NM 2006 Apollo Investment Fund VI $200.0 $257.4 $385.2 $3.8 1.69x 8.7% 2008 Apollo -

![[Title Goes Here]](https://docslib.b-cdn.net/cover/7730/title-goes-here-1067730.webp)

[Title Goes Here]

CVC CAPITAL PARTNERS ACQUIRES SISAL GROUP S.P.A.FROM PERMIRA, APAX AND CLESSIDRA Milan – 30 May 2016 – CVC Capital Partners announced today that funds advised by CVC Capital Partners (“CVC”) have agreed to acquire a 100% equity stake in Italian gaming and payments operator, Sisal Group S.p.A. (“Sisal”), from funds advised by Apax Partners, Permira and Clessidra. The value of the transaction, which is expected to close by the end of September, was €1.0bn. Headquartered in Milan, Sisal is a leading operator in the Italian gaming market and the number one provider of payments services. Established in 1946, Sisal was the first Italian company to operate in the gaming sector as a Government Licensee. Through its capillary network of 45,000 points of sale, the company offers the public in excess of 500 payment services. Sisal employs about 2000 people. CVC has a strong track record in the gaming industry through its strategic investments in Sky Bet (UK), Tipico (Germany) as well as its previous investment in William Hill. Giampiero Mazza, Partner and Head of CVC’s Italian team, said: “We are very pleased to have the opportunity to invest in Sisal. The Company is a well diversified entertainment business with a historical brand in Italy and strong market positions across gaming, lotteries, betting and convenience payments. Under its previous shareholders and the management team led by Emilio Petrone, Sisal was able to grow and reshape its business perimeter thorough a period of difficult macro conditions and regulatory uncertainty. Sisal today is ideally positioned to capture growth in a number of areas. -

THE INSTITUTE for QUANTITATIVE RESEARCH in FINANCE® Volume 8

® "The Q - Group" THE INSTITUTE FOR QUANTITATIVE RESEARCH ® IN FINANCE Founded 1966 -- Over 50 years of Research and Seminars Devoted to the State-of-the-Art in Investment Technology Summary of Proceedings Volume 8 2011 - 2015 ALL RIGHTS RESERVED. NO PART OF THIS PUBLICATION MAY BE REPRODUCED, STORED IN A RETRIEVAL SYSTEM, OR TRANSMITTED, IN ANY FORM OR BY ANY MEANS ELECTRONIC, MECHANICAL, PHOTOCOPYING, RECORDING OR OTHERWISE, WITHOUT THE PRIOR WRITTEN PERMISSION OF THE PUBLISHER AND COPYRIGHT OWNER. Published by The Institute for Quantitative Research in Finance, P.O. Box 6194, Church Street Station, New York, NY 10249.6194 Copyright 2017 by The Institute for Quantitative Research in Finance, P.O. Box 6194, Church Street Station, New York, NY 10249.6194 Printed in The United States of America PREFACE TO VOLUME 8 iv TABLE OF CONTENTS PREFACE TO VOLUME 8 ........................................................................................................ iv Active Asset Management – Alpha .............................................................................................. 1 1. Cross-Firm Information Flows (Spring 2015) 1 Anna Scherbina, Bernd Schlusche 2. Dissecting Factors (Spring 2014) 2 Juhani Linnainmaa 3. The Surprising “Alpha” From Malkiel’s Monkey And Upside-Down Strategies (Fall 2013) 4 Jason Hsu 4. Will My Risk Parity Strategy Outperform? Lisa R Goldberg (Spring 2012) 5 Lisa Goldberg Active Asset Management – Mutual Fund Performance .......................................................... 7 5. Target Date Funds (Fall 2015) 7 Ned Elton, Marty Gruber 6. Patient Capital Outperformance (Spring 2015) 8 Martijn Cremers 7. Do Funds Make More When They Trade More? (Spring 2015) 10 Robert Stambaugh 8. A Sharper Ratio: A General Measure For Ranking Investment Risks (Spring 2015) 11 Kent Smetters 9. Scale And Skill In Active Management (Spring 2014) 13 Lubos Pastor 10.