Piper Jaffray Software Activity Update November 2016

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sabre Corporation Annual Report 2019

Sabre Corporation Annual Report 2019 Form 10-K (NASDAQ:SABR) Published: February 15th, 2019 PDF generated by stocklight.com UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2018 or ¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Sabre Corporation (Exact name of registrant as specified in its charter) Delaware 001-36422 20-8647322 (State or other jurisdiction (Commission File Number) (I.R.S. Employer of incorporation or organization) Identification No.) 3150 Sabre Drive Southlake, TX 76092 (Address, including zip code, of principal executive offices) (682) 605-1000 (Registrant's telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: Common Stock, $0.01 par value The NASDAQ Stock Market LLC (Title of class) (Name of exchange on which registered) Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No ¨ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Answer of Defendants Sabre Corporation and Sabre Glbl Inc

Case 1:19-cv-01548-LPS Document 22 Filed 09/10/19 Page 1 of 35 PageID #: 61 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF DELAWARE ) UNITED STATES OF AMERICA, ) ) Plaintiff, ) ) v. ) Civil Action No. 19-cv-01548-LPS ) SABRE CORPORATION, ) SABRE GLBL INC., ) FARELOGIX, INC., and ) SANDLER CAPITAL PARTNERS V, L.P., ) ) Defendants. ) ) ANSWER OF DEFENDANTS SABRE CORPORATION AND SABRE GLBL INC. Defendants Sabre Corporation and Sabre GLBL Inc. (together, “Sabre”) by and through their undersigned counsel, answer as follows the allegations of the Complaint filed on August 20, 2019 (the “Complaint”), by the United States (“Plaintiff”). Except for those allegations expressly admitted herein, Sabre denies each and every allegation in the Complaint. Except as noted herein, Sabre lacks knowledge or information sufficient to form a belief as to the truth of the allegations regarding statements made in internal documents by Farelogix, Inc. (“Farelogix”), or any other allegations regarding non-public statements, commercial plans, or intentions of companies other than Sabre’s. Sabre expressly denies that Plaintiff is entitled to the relief requested or any other relief. Sabre reserves the right to amend this Answer. PRELIMINARY STATEMENT Plaintiff claims that Sabre’s acquisition of Farelogix (the “Acquisition”) is “a dominant firm’s attempt to eliminate a disruptive competitor.” Nothing could be further from the truth. Case 1:19-cv-01548-LPS Document 22 Filed 09/10/19 Page 2 of 35 PageID #: 62 First, Sabre is not dominant. It is one of three major global distribution systems (“GDSs”) in the world. In fact, it is not even the largest GDS in the world—Amadeus is the leading global GDS, and Sabre competes against it, Travelport and others to serve both airline and travel agency customers. -

Benjamin M. Weadon Senior Associate

Benjamin M. Weadon Senior Associate 704.444.1082 [email protected] Charlotte | Bank of America Plaza, 101 South Tryon Street, Suite 4000 | Charlotte, NC 28280-4000 Ben Weadon is a senior associate with Alston & Bird’s Corporate & Business Transactions Group. He advises private equity firms and their portfolio companies from coast to coast on leveraged buyouts, growth equity investments, merger and acquisition transactions, and general corporate matters. Ben has advised on deals in various industries, including software, semiconductor, telecommunications, and fleet management. Ben received his J.D., with high honors, from the University of North Carolina School of Law, where he was elected to the Order of the Coif. In law school, Ben was the executive editor of the North Carolina Banking Institute Journal. Ben received a B.A. in history, cum laude, from Duke University. Representative Experience Represented CommScope Holding Company Inc. in its $7.4 billion acquisition of ARRIS International plc. Represented The Carlyle Group in its $7.4 billion acquisition of Veritas, an information management system provider, from Symantec Corporation. Represented CommScope Holding Company Inc. in its $3 billion acquisition of TE Connectivity’s telecom, enterprise, and wireless businesses. Represented an entity controlled by The Carlyle Group in the acquisition of the Compute business of MACOM Technology Solutions and related joint venture with Oracle Corporation. Represented The Carlyle Group in its investment in ProKarma, a high-growth IT services firm. Represented Ridgemont Equity Partners in its acquisition of Munch’s Supply, a leading wholesale distributor of heating, ventilation, and air conditioning (HVAC) equipment. Represented Ridgemont Equity Partners in its acquisition of Dickinson Fleet Services, a technology-enabled service provider in the vehicle fleet maintenance industry. -

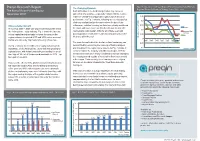

Preqin Research Report Fig

Preqin Research Report Fig. 3 Comparison of Private Equity Performance by Fund Primary The Changing Dynamic Regional Focus for Funds of Vintage Years 1995 - 2007 The Rise of Asian Private Equity Such diffi culties in the fundraising market may come as November 2010 somewhat of a surprise – especially considering the relative resilience of Asia-focused private equity funds in terms of 0.25 performance. As Fig. 3 shows, following an extended period 0.2 of strong median fund performance since the turn of the Unprecedented Growth millennium, vehicles focusing on Asia have clearly weathered 0.15 the storm with more success than their European and US Europe The period 2003 – 2008 saw unprecedented growth within 0.1 the Asian private equity industry. Fig. 1 shows the increase counterparts, with median IRRs for all vintage years still Asia and Rest of World posting positive results while funds focusing primarily on the 0.05 in total capital raised annually by funds focusing on the US region between the period 2003 and 2008, when a record West are still in the red. IRR Median Net-to-LP 0 $91bn was raised by 194 funds achieving a fi nal close. 1995 1997 1999 2001 2003 2005 2007 The main factors behind the decline in Asia fundraising can -0.05 As Fig. 2 shows, the record level of capital raised saw the be identifi ed by examining the make-up of fund managers -0.1 Vintage Year importance of the Asian private equity industry growing on and investors in the region more closely. As Fig. -

TRS Contracted Investment Managers

TRS INVESTMENT RELATIONSHIPS AS OF DECEMBER 2020 Global Public Equity (Global Income continued) Acadian Asset Management NXT Capital Management AQR Capital Management Oaktree Capital Management Arrowstreet Capital Pacific Investment Management Company Axiom International Investors Pemberton Capital Advisors Dimensional Fund Advisors PGIM Emerald Advisers Proterra Investment Partners Grandeur Peak Global Advisors Riverstone Credit Partners JP Morgan Asset Management Solar Capital Partners LSV Asset Management Taplin, Canida & Habacht/BMO Northern Trust Investments Taurus Funds Management RhumbLine Advisers TCW Asset Management Company Strategic Global Advisors TerraCotta T. Rowe Price Associates Varde Partners Wasatch Advisors Real Assets Transition Managers Barings Real Estate Advisers The Blackstone Group Citigroup Global Markets Brookfield Asset Management Loop Capital The Carlyle Group Macquarie Capital CB Richard Ellis Northern Trust Investments Dyal Capital Penserra Exeter Property Group Fortress Investment Group Global Income Gaw Capital Partners AllianceBernstein Heitman Real Estate Investment Management Apollo Global Management INVESCO Real Estate Beach Point Capital Management LaSalle Investment Management Blantyre Capital Ltd. Lion Industrial Trust Cerberus Capital Management Lone Star Dignari Capital Partners LPC Realty Advisors Dolan McEniry Capital Management Macquarie Group Limited DoubleLine Capital Madison International Realty Edelweiss Niam Franklin Advisers Oak Street Real Estate Capital Garcia Hamilton & Associates -

DENVER CAPITAL MATRIX Funding Sources for Entrepreneurs and Small Business

DENVER CAPITAL MATRIX Funding sources for entrepreneurs and small business. Introduction The Denver Office of Economic Development is pleased to release this fifth annual edition of the Denver Capital Matrix. This publication is designed as a tool to assist business owners and entrepreneurs with discovering the myriad of capital sources in and around the Mile High City. As a strategic initiative of the Denver Office of Economic Development’s JumpStart strategic plan, the Denver Capital Matrix provides a comprehensive directory of financing Definitions sources, from traditional bank lending, to venture capital firms, private Venture Capital – Venture capital is capital provided by investors to small businesses and start-up firms that demonstrate possible high- equity firms, angel investors, mezzanine sources and more. growth opportunities. Venture capital investments have a potential for considerable loss or profit and are generally designated for new and Small businesses provide the greatest opportunity for job creation speculative enterprises that seek to generate a return through a potential today. Yet, a lack of needed financing often prevents businesses from initial public offering or sale of the company. implementing expansion plans and adding payroll. Through this updated resource, we’re striving to help connect businesses to start-up Angel Investor – An angel investor is a high net worth individual active in and expansion capital so that they can thrive in Denver. venture financing, typically participating at an early stage of growth. Private Equity – Private equity is an individual or consortium of investors and funds that make investments directly into private companies or initiate buyouts of public companies. Private equity is ownership in private companies that is not listed or traded on public exchanges. -

Before the FEDERAL COMMUNICATIONS COMMISSION Washington, D.C

Before the FEDERAL COMMUNICATIONS COMMISSION Washington, D.C. 20554 In the Matter ofthe Application of SinglePipe Communications, Inc., Transferor, ALEC, Inc., Licensee ... ., --, and Integrated Broadband Services, LLC, Transferee For grant of authority pursuant to Section 214 ofthe Communications Act of 1934, as amended, and Section 63.04 ofthe Commission's Rules to Transfer Control of ALEC, Inc. I. INTRODUCTION A. Summary ofTransaction SinglePipe Communications, Inc. ("SinglePipe" or "Transferor"), ALEC, Inc. ("ALEC" or "Licensee") and Integrated Broadband Services, LLC ("IBBS" or "Transferee") (collectively, "Applicants"), through their undersigned l:ounsel and pursuant to Section 214 of the Communications Act, as amended l and Section 63.04 of the Commission's rules,2 respectfully request Commission approval to transfer control of Li>:ensee to Transferee. Licensee is a non- dominant carrier holding blanket domestic 214 authorization from the Commission to provide interstate telecommunications services under Section 63.01 ofthe Commission's ruIes.3 1 47 U.S.C. § 214. 2 47 C.F.R. § 63.04. 3 47 C.F.R. § 63.01. 1 DWT 14804192v2 0102461.QODOOl B. Request for Streamlined Processing Applicants respectfully submit that this application is eligible for presumptive streamlined processing under Section 63.03(b)(l)(ii) of the Commission's rules because the Transferee is not a telecommunications provider. 4 II. DESCRIPTION OF THE APPLICANTS A. Transferor and Licensee SinglePipe is a Kentucky corporation with its principal place of business at 11492 Bluegrass Parkway, Louisville, KY 40299, and is the direct, 100% parent of ALEC. SinglePipe is not a regulated telecommunications entity in any state, and has no subsidiaries, other than ALEC, that are regulated telecommunications entities. -

Venture Capital & Private Equity Canadian Market Overview

VC & PE CANADIAN MARKET OVERVIEW // 2017 CONTENTS PARTICIPATING DATA CONTRIBUTORS ............................................................................... 3 PRIVATE EQUITY CANADIAN MARKET OVERVIEW ...................................................... 17 PRIVATE EQUITY HIGHLIGHTS .................................................................................................................................... 18 FOREWORD ......................................................................................................................................4 PRIVATE EQUITY HEAT MAP // BUYOUT & ADD-ON DEALS ONLY ............................................... 19 VENTURE CAPITAL CANADIAN MARKET OVERVIEW .................................................... 5 PRIVATE EQUITY HEAT MAP // ALL PE DEALS ............................................................................................. 20 VENTURE CAPITAL HIGHLIGHTS ................................................................................................................................ 6 QUARTER-OVER-QUARTER PE INVESTMENT ACTIVITY ....................................................................... 21 VENTURE CAPITAL HEAT MAP ..................................................................................................................................... 7 TOP DISCLOSED CANADIAN PE DEALS OVER $500M ............................................................................ 22 QUARTER-OVER-QUARTER VC INVESTMENT ACTIVITY ........................................................................ -

Sabre Corporation (Exact Name of Registrant As Specified in Its Charter)

' UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C. 20549 FORM 10-K ~ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2018 or • TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Sabre Corporation (Exact name of registrant as specified in its charter) Delaware 001-36422 20-8647322 (State or other jurisdiction (Commission File Number) (I.R.S. Employer of Incorporation or organization) Identification No.) 3150 Sabre Drive Southlake, TX 76092 (Address, including zip code, ofprinc ipal executive offices) (682) 605-1000 (Registrant's telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: Common Stock, $0.01 par value The NASDAQ Stock Market LLC (Title of class) (Name of exchange on which registered ) Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrantis a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes l!I No • Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act Yes • No l!I Indicate by check mark whether the registrant (1) has fi led all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

PEI Investor Relations, Marketing & Communications Forum 2019

June 19-20 | Convene, 730 Third Ave | New York Attendee list A.P. Moller Capital Bain Capital C-Bridge Capital Partners FTV Capital ACME Capital Banner Real Estate Group CCMP Capital Advisors Further Capital Partners Actis Barings Centerbridge Partners GCM Grosvenor Advent International Basis Investment Group Cerberus Capital Management General Atlantic AE Industrial Partners Battery Ventures Charlesbank Capital Partners General Catalyst Partners AEA Investors BBH Capital Partners The Chauncey F. Lufkin III Gennx360 AEW Capital Management BC Partners Foundation Genstar Capital AIMA The Beach Company The City of New York, Finance Global Infrastructure Partners Alcentra Berkshire Partners Civitas Capital Grain Management Alcion Ventures Bernhard Capital Partners Coller Capital Gryphon Investors Allianz Capital Partners Bicknell Family Holding Cornell Capital GTCR Altor Equity Partners Company Court Square Capital Partners Halstatt American Securities Bison Crescent Capital Group Hamilton Lane AMP Capital BKM Capital Partners CRV Hammes Angelo Gordon Blackstone Cypress Real Estate Advisors Hammond, Kennedy, Whitney Antares Capital Blue Heron Asset Managment Denham Capital & Co Apollo Global Management Blue Water Energy Duff & Phelps Hancock Capital Management ARC Financial Corp Bridge Investment Group Dyal Capital Partners Harvard Management Company ArcLight Capital Partners BroadVail Capital Edelman HCI Equity Partners Argosy Capital Brook Venture Partners EnCap Investments HGGC Arroyo Energy Investment Brookfield Asset Management EQT Partners -

ANNUAL REVIEW 2017 Land of the Giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus

ANNUAL REVIEW 2017 Land of the giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus Ares Management is honored to be recognized as Lender of the Year in North America for the fourth consecutive year as well as Lender of the Year in Europe Lender of the year in Europe Ares Management, L.P. (NYSE: ARES) is a leading global alternative asset manager with approximately $106 billion of AUM1 and offices throughout the United States, Europe, Asia and Australia. With more than $70 billion in AUM1 and approximately 235 investment professionals, the Ares Credit Group is one of the largest global alternative credit managers across the non-investment grade credit universe. Ares is also one of the largest direct lenders to the U.S. and European middle markets, operating out of twelve office locations in both geographies. Note: As of December 31, 2017. The performance, awards/ratings noted herein may relate only to selected funds/strategies and may not be representative of any client’s given experience and should not be viewed as indicative of Ares’ past performance or its funds’ future performance. 1. AUM amounts include funds managed by Ivy Hill Asset Management, L.P., a wholly owned portfolio company of Ares Capital Corporation and a registered investment adviser. learn more at: www.aresmgmt.com | www.arescapitalcorp.com The battle of the brands the US market on page 80, advisor Hamilton TOBY MITCHENALL Lane said it had received a record number EDITOR'S of private placement memoranda in 2017 – ISSN 1474–8800 LETTER MARCH 2018 around 800 – and that this, combined with Senior Editor, Private Equity faster fundraising processes, has made it dif- Toby Mitchenall, Tel: +44 207 566 5447 [email protected] ficult to some investors to make considered Special Projects Editor decisions. -

PEI June2020 PEI300.Pdf

Cover story 20 Private Equity International • June 2020 Cover story Better capitalised than ever Page 22 The Top 10 over the decade Page 24 A decade that changed PE Page 27 LPs share dealmaking burden Page 28 Testing the value creation story Page 30 Investing responsibly Page 32 The state of private credit Page 34 Industry sweet spots Page 36 A liquid asset class Page 38 The PEI 300 by the numbers Page 40 June 2020 • Private Equity International 21 Cover story An industry better capitalised than ever With almost $2trn raised between them in the last five years, this year’s PEI 300 are armed and ready for the post-coronavirus rebuild, writes Isobel Markham nnual fundraising mega-funds ahead of the competition. crisis it’s better to be backed by a pri- figures go some way And Blackstone isn’t the only firm to vate equity firm, particularly and to towards painting a up the ante. The top 10 is around $30 the extent that it is able and prepared picture of just how billion larger than last year’s, the top to support these companies, which of much capital is in the 50 has broken the $1 trillion mark for course we are,” he says. hands of private equi- the first time, and the entire PEI 300 “The businesses that we own at Aty managers, but the ebbs and flows of has amassed $1.988 trillion. That’s the Blackstone that are directly affected the fundraising cycle often leave that same as Italy’s GDP. Firms now need by the pandemic, [such as] Merlin, picture incomplete.