Atos Reference Document 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Digital Transformation: Creating New Business Models Where Digital

IBM Global Business Services Strategy and Transformation Executive Report IBM Institute for Business Value Digital transformation Creating new business models where digital meets physical IBM Institute for Business Value IBM Global Business Services, through the IBM Institute for Business Value, develops fact-based strategic insights for senior executives around critical public and private sector issues. This executive report is based on an in-depth study by the Institute’s research team. It is part of an ongoing commitment by IBM Global Business Services to provide analysis and viewpoints that help companies realize business value. You may contact the authors or send an e-mail to [email protected] for more information. Additional studies from the IBM Institute for Business Value can be found at ibm.com/iibv Introduction By Saul J. Berman and Ragna Bell Individuals and businesses alike are embracing the digital revolution. Social networks and digital devices are being used to engage government, businesses and civil society, as well as friends and family. People are using mobile, interactive tools to determine who to trust, where to go and what to buy. At the same time, businesses are undertaking their own digital transformations, rethinking what customers value most and creating operating models that take advantage of what’s newly possible for competitive differentiation. The challenge for business is how fast and how far to go on the path to digital transformation. The new digital age Business leaders have long used information technology to In every industry, business leaders realize customer expecta- improve productivity and efficiency, reach new markets and tions have created tremendous pressure to change the way they optimize supply chains. -

2014 Registration Document Annual Financial Report Contents

2014 REGISTRATION DOCUMENT ANNUAL FINANCIAL REPORT CONTENTS 1 4 Presentation of the Company Financial Information 129 and its activities 5 4.1 Analysis on Capgemini 2014 Group consolidated 1.1 Milestones in the Group’s history and its values 6 results AFR 130 1.2 The Group’s activities 8 4.2 Consolidated accounts AFR 136 1.3 Main Group subsidiaries and simplified 4.3 Comments on the Cap Gemini S.A. Financial organization chart 13 Statements AFR 195 1.4 The market and the competitive environment 15 4.4 Cap Gemini S.A. financial statements AFR 197 1.5 2014, a year of strong growth 17 4.5 Other financial and accounting information AFR 221 1.6 The Group’s investment policy, financing policy and market risks AFR 25 1.7 Risk analysis AFR 26 5 CAP GEMINI and its shareholders 223 2 5.1 Cap Gemini S.A. Share Capital AFR 224 5.2 Cap Gemini S.A. and the stock market 229 Corporate governance 5.3 Current ownership structure 233 and Internal control 33 5.4 Share buyback program AFR 235 2.1 Organization and activities of the Board of Directors AFR 35 6 2.2 General organization of the Group AFR 54 2.3 Compensation of executive corporate officers AFR 58 2.4 Internal control and risk management Report of the Board of Directors procedures AFR 70 and draft resolutions 2.5 Statutory Auditors’ report prepared in accordance with Article L.225-235 of the French Commercial of the Combined Shareholders’ Code on the report prepared by the Chairman Meeting of May 6, 2015 237 of the Board of Directors AFR 79 6.1 Resolutions presented at the Ordinary Shareholders’ -

Carbon Footprint & Energy Transition Report

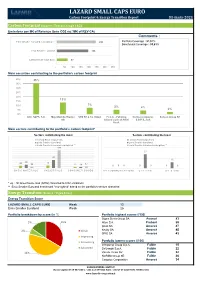

LAZARD SMALL CAPS EURO Carbon Footprint & Energy Transition Report 31-mars-2021 Carbon Footprint (Source : Trucost, scope 1&2) Emissions per M€ of Revenue (tons CO2 éq.*/M€ of REV CA) Comments : Emix Smaller Euroland reweighted ** 242 Portfolio Coverage : 97,51% Benchmark Coverage : 93,61% Emix Smaller Euroland 196 Lazard Small Caps Euro 67 - 50 100 150 200 250 300 350 Main securities contributing to the portfolio's carbon footprint 40% 35% 35% 30% 25% 20% 13% 15% 10% 7% 5% 4% 5% 2% 0% Altri, SGPS, S.A. Mayr-Melnhof Karton STO SE & Co. KGaA F.I.L.A. - Fabbrica Corticeira Amorim, Surteco Group SE AG Italiana Lapis ed Affini S.G.P.S., S.A. S.p.A. Main sectors contributing to the portfolio's carbon footprint* Sectors contributing the most Sectors contributing the least Lazard Small Caps Euro Lazard Small Caps Euro Emix Smaller Euroland Emix Smaller Euroland Emix Smaller Euroland reweighted ** Emix Smaller Euroland reweighted ** 193 27 87 12 35 28 24 13 17 12 11 00 0 0 0 0 0 BASIC MATERIALS INDUSTRIALS CONSUMER GOODS TELECOMMUNICATIONS UTILITIES OIL & GAS * eq. : All Greenhouse Gas (GHG) converted to CO2 emissions ** Emix Smaller Euroland benchmark "reweighted" based on the portfolio's sectors allocation Energy Transition (Source : Vigeo Eiris) Energy Transition Score LAZARD SMALL CAPS EURO Weak 13 Emix Smaller Euroland Weak 25 Portfolio breakdown by score (in %) Portfolio highest scores (/100) Sopra Steria Group SA Avancé 83 5% 10% Alten S.A. Probant 59 Ipsos SA Amorcé 47 2% Weak Nexity SA Amorcé 45 SPIE SA Amorcé 43 Improving Portfolio lowest scores (/100) Convincing Interpump Group S.p.A. -

What Is the Value of a Company?

ibm corporate responsibility report ibm corporate What is the value of a company? ibm corporate responsibility report 2002 www.ibm.com/ibm/responsibility/ This report is also available at This report about this report This report combines and expands upon IBM’s previous reporting on corporate philanthropy, diversity, employee well-being and environ- mental programs. The document describes these and other programs and provides data for 2002. Where appropriate, five years of data have been included to demonstrate trends and provide year-to-year comparisons. Environmental and selected financial data include that for IBM and its controlled subsidiary companies, which in general are majority owned. Other data is that of IBM. We have included information on the areas of corporate responsibility we believe are the most relevant and meaningful with regard to IBM’s global activities. Among the references used in preparing this report are the Global Reporting Initiative (GRI) Sustainability Reporting Guidelines, the corporate social responsibility surveys of a number of external organizations, and questions we are often asked by customers and other stakeholders. We view this report as a valuable tool for maintaining dialogue with a variety of interested parties, including our employees, customers, investors, neighbors and regulators. We also realize we cannot address all the interests of all groups in a single document. For additional information, questions or comments on the report, call (800) IBM-4YOU or, outside the United States, (404) 238-1234. Additional information about IBM and its business performance may be found in the company’s annual report, available on the Internet at www.ibm.com/annualreport/2002/index_home.htm. -

Why Companies Outsource "Buying" Services Is an Increasingly Viable Option

Outsourcing: The U.S. Business Revolution Spring 1997 Copyright © Michael F. Corbett & Associates, Ltd., 1997 Customer Confidential. Reproduction in whole or in part is strictly prohibited. Outsourcing: The U.S. Business Revolution Published by: Michael F. Corbett & Associates, Ltd. Lexington Park, East Bldg. Suite A 255 Route 55 LaGrangeville, NY 12540 (845) 452-0600 (845) 452-6988 (fax) Email: [email protected] Copyright Ó Michael F. Corbett & Associates, Ltd. 1997 All rights reserved. Michael F. Corbett & Associates reports are limited publications containing valuable management information provided to a select group of customers in response to orders and our customers acknowledge when ordering that the reports are for our customer’s own internal use only and not for general publication or disclosure to third parties. This report may not be copied or given, lent or resold to third parties without written permission nor may its contents be disclosed to non-customers without written permission. Information is believed to be reliable but cannot be guaranteed to be correct or complete. Copyright © Michael F. Corbett & Associates, Ltd., 1997 2 Customer Confidential. Reproduction in whole or in part is strictly prohibited. Table of Contents SECTION 1: OUTSOURCING: BACKGROUND, DEFINITIONS & DECISION FACTORS 5 OUTSOURCING DEFINED 5 TRADITIONAL ORGANIZATIONAL STRUCTURES 6 OUTSOURCING’S EMERGENCE AS A POWERFUL MANAGEMENT TOOL 7 DRIVING FACTORS 12 OUTSOURCING AS A “MAKE VERSUS BUY” DECISION 12 TOP TEN REASONS COMPANIES OUTSOURCE 17 TYPES OF SERVICES OUTSOURCED AND SELECTED CASE STUDIES 21 THE OUTSOURCING CONTINUUM 21 CLEANING 21 FOOD SERVICES 23 COPY CENTERS 23 MAILROOM OPERATIONS 24 PAYROLL 25 FACILITY MANAGEMENT 25 HUMAN RESOURCES 27 TRANSPORTATION & LOGISTICS 28 INFORMATION TECHNOLOGY 30 MARKETING & SALES 36 FINANCE 37 THE OUTSOURCING PROCESS 39 STRATEGIC ANALYSIS 39 IDENTIFYING BEST CANDIDATES 39 DEFINING REQUIREMENTS 40 SELECTING PROVIDER(S) 41 TRANSITIONING THE OPERATION 41 MANAGING THE RELATIONSHIP 42 Copyright © Michael F. -

Siemens Company History Phase8

New paths in a time of crisis 1989–2006 The years from 1989 to 2006 confronted the company with challenges unlike any before – including the first comprehensive reform of the corporate organization, the launch of the Ten- Point Program, and the compliance crisis – that compelled its chief players to make fundamental changes. 1989 was a year of profound changes, not just for Germany and global politics, but for Siemens. Twenty years after the company’s last major organizational reform, there was a need for action. Siemens AG had outgrown the structure that had been laid out back in 1966 and 1969. Where revenues in fiscal 1969 had been 12.7 billion deutschmarks, by 1986 they had risen to 51.4 billion. The number of business units had grown to eight by the end of the 1980s. Karlheinz Kaske, CEO from 1981 to 1992, aimed to improve "mo- bility, effectiveness and competitiveness," with an organizational structure that took due account of the company's changing envi- ronment – the technological paradigm shift from mechanical de- vices to electronics and microelectronics, the growth of interna- tional business, a greatly expanded worldwide customer base, and ever-intensifying competition. So top management first of all set up a more effective administrative structure. The eight former business units were rearranged into 15 new, leaner units, two operating Groups with their own legal form, and two independ- ent Divisions. Each was responsible for its own profits and value chain – from development through production to sales – and each was managed by three Group Executive Managers. Top management, which formerly included more than 30 people, was © Siemens Historical Institute 2017 1/4 siemens.com/history cut by a third. -

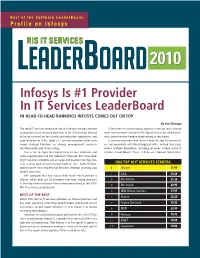

Infosys Is #1 Provider in IT Services Leaderboard in Head-To-Head Rankings Infosys Comes out on Top

Best of the Software LeaderBoard: Profile on Infosys RIS IT SERVICES Leaderboard 2010 Infosys Is #1 Provider In IT Services LeaderBoard IN HEAD-TO-HEAD RANKINGS INFOSYS COMES OUT ON TOP By Joe Skorupa The retail IT services landscape has shifted over the past decade Of the three lists where Infosys appears in the top spot it should as providers have elevated their role in the IT hierarchy. Instead come as no surprise that one is the Top-10 master list, which is the of being counted on for simple cost-reduction capabilities and only comprehensive head-to-head ranking in the report. augmentation of skills, today’s IT services providers offer such IT services providers that make it onto the Top-10 master list major strategic functions as change management, business are not specialists with finely targeted skills. Instead they excel transformation and IT consulting. across multiple disciplines, including all seven Criteria in the IT This is not to imply that competency in cost reduction and Services LeaderBoard. These Criteria are: Domain Experience, skills augmentation are not important. They are. But many lead- ing IT services providers are so large and diverse that they pos- 2010 TOP 10 IT SERVICES LEADERS sess a deep pool of talent found nowhere else, both off-shore and on-shore, that retailers tap for both strategic planning and 1 Infosys 31.80 project execution. 2 JDA 31.68 One company that has successfully made this transition is Infosys, which beat out 32 providers that have strong practices 3 Accenture 31.34 in the retail industry to earn the number one ranking in the 2010 4 Microsoft 28.92 RIS IT Services LeaderBoard. -

IBM Global Services: a Brief History

IBM Global Services: A Brief History IBM Corporate Archives May 2002 2405SH01 2 OVERVIEW Background In 1991 IBM was a $64.8 billion company, of which less than $6 billion was derived from non-maintenance services. Ten short years later, the business of information technology (IT) services alone generated more than 40 percent of IBM’s $86 billion in sales and had become the single largest source of revenue in IBM’s portfolio. How did that happen? It was partly the result of old-fashioned hard work and serious commitment: growing customer by customer; building disciplined management and financial systems; and investing to hire and train experts in everything from IT consulting to systems architecture and Web services. IBM used its financial strength to fund the expensive push into outsourcing, and the company placed informed bets on the future in areas such as IT utility services (“e-business on demand”) and hosted storage. But most important, the success of IBM Global Services came from something very simple: a clear understanding of customers’ needs. IBM saw that technology and business were converging to create something new and challenging for every kind of enterprise. And IBM had the deep experience in both areas to help its customers bring them together most effectively. The following pages offer a brief look at the history and growth of the organization that is today IBM’s top revenue generator. Definitions What are “services?” In the IT world, that broad term has encompassed dozens of offerings and meanings, including consulting, custom programming, systems integration (designing, building and installing complex information systems), systems operations (in which a vendor runs part or all of a company’s information systems), business innovation services (such as supply chain management), strategic outsourcing, application management services, integrated technology services (such as business recovery), networking services, learning services, security services, storage services and wireless services. -

Tech Procurement in the UK Justice Sector

Tech Procurement in the UK Justice Sector December 2020 Trusted Insight on Government Contracts and Spend Trusted by suppliers, the public sector, and the media — Corporate Government Media 550+ Press citations since Jan 2019 “Serious-minded business data provider Tussell” Matthew Vincent 22nd September 2018 2 | Trends and Opportunities in the Justice Sector We transform open data into useful data – so you don’t have to — Open data Third party data Useful data Use cases CONTRACT DATA Public Sector Aggregate Get better value from TED (EU) suppliers Companies House Contracts Finder (UK), Sell2Wales, PCS Match Digital Marketplace Suppliers Normalise Win government Circa 70 local portals contracts Cleanse SPEND DATA Moody’s Analytics 6800+ Central Gov’t, Press Local Gov’t & NHS Machine Scrutinise public bodies learn spending 3 | Trends and Opportunities in the Justice Sector Total data coverage: Justice — Spend Contracts Q1 2016 – Q2 2020 Q1 2015 – Q3 2020 864,000 invoices 7,000 contracts £28bn spend value £17bn contract value 43 buyers 100 buyers 31,000 suppliers 2,600 suppliers 4 | Trends and Opportunities in the Justice Sector Questions Tussell will answer — 1. How big is the market? 2. What’s the breakdown by sub-sector? 3. Can new entrants break through? 4. Has demand recovered from Covid? 5. How can I position my firm for future rebids? 5 | Procurement in the UK EdTech market Technology spend in the justice sector in the five years from 2016-2020 was £3bn in total, an average of £597m per annum Spend data £728M £710M Average: £597M £578M -

Family Businesses in Germany and the United States Since

Family Businesses in Germany and the United States since Industrialisation A Long-Term Historical Study Family Businesses in Germany and the United States since Industrialisation – A Long-Term Historical Study Industrialisation since States – A Long-Term the United and Businesses Germany in Family Publication details Published by: Stiftung Familienunternehmen Prinzregentenstraße 50 80538 Munich Germany Tel.: +49 (0) 89 / 12 76 400 02 Fax: +49 (0) 89 / 12 76 400 09 E-mail: [email protected] www.familienunternehmen.de Prepared by: Institut für Wirtschafts- und Sozialgeschichte Platz der Göttinger Sieben 5 37073 Göttingen Germany Univ.-Prof. Dr. Hartmut Berghoff Privatdozent Dr. Ingo Köhler © Stiftung Familienunternehmen, Munich 2019 Cover image: bibi57 | istock, Sasin Tipchai | shutterstock Reproduction is permitted provided the source is quoted ISBN: 978-3-942467-73-5 Quotation (full acknowledgement): Stiftung Familienunternehmen (eds.): Family Businesses in Germany and the United States since Indus- trialisation – A Long-Term Historical Study, by Prof. Dr. Hartmut Berghoff and PD Dr. Ingo Köhler, Munich 2019, www.familienunternehmen.de II Contents Summary of main results ........................................................................................................V A. Introduction. Current observations and historical questions ..............................................1 B. Long-term trends. Structural and institutional change ...................................................13 C. Inheritance law and the preservation -

C-Lab Jahresbericht 2011 C-Lab Annual Report 2011

JAHRESBERICHT ANNUAL REPORT 2011 C-LAB JAHRESBERICHT 2011 C-LAB ANNUAL REPORT 2011 Im C-LAB – Cooperative Computing & Communication Laboratory – arbeiten Mitarbeiter und Mitarbeiterinnen der Universität Paderborn und der Atos IT Solutions and Services GmbH (Siemens IT Solutions and Services GmbH bis 30.6.2011) an gemeinsamen Forschungs- und Entwick- lungsprojekten erfolgreich zusammen. Die Kooperation wurde 1985 von der Nixdorf Computer AG (nun Atos IT Solutions and Services GmbH) und der Universität Pader- born im Einvernehmen mit dem Land Nordrhein-Westfa- len gegründet. C-LAB’s Cooperative Computing & Communication Lab- oratory successfully brings together employees from Pa- derborn University and from Atos IT Solutions and Serv- ices GmbH (Siemens IT Solutions and Services GmbH until June 30, 2011) in a series of joint research and de- velopment projects. The cooperation was initiated in 1985 by Nixdorf Computer AG (now Atos IT Solutions and Serv- ices GmbH) and by Paderborn University with the support of the North Rhine-Westphalia regional government. Dr. Wolfgang Kern Atos IT Solutions and Services GmbH Prof. Dr. Franz Josef Rammig Universität Paderborn C-LAB Fürstenallee 11 D-33102 Paderborn www.c-lab.de INHALTSVERZEICHNIS CONTENTS VORWORT 5 PREFACE . AUSGEWÄHLTE PROJEKTE 11 SELECTED PROJECTS . KONZEPTE FÜR EIN COMMUNITY-BASIERTES WISSENSMANAGEMENT IM ENTERPRISE 2.0 CONCEPTS FOR A COMMUNITY-BASED KNOWLEDGE MANAGEMENT IN ENTERPRISE 2.0 . 11 OSAMI OSAMI . 19 PROJEKTÜBERSICHTEN 26 PROJECT OVERVIEW . NUTZERPROZESSE AM BEISPIEL DES PROJEKTES MARION USER PROCESSES AS ILLUSTRATED BY THE MARION PROJECT . 26 CYBER-PHYSICAL SYSTEMS CYBER-PHYSICAL SYSTEMS . 28 ORGANIC COMPUTING ORGANIC COMPUTING . 30 OPTICAL ENGINEERING OPTICAL ENGINEERING . 32 ELECTRIC MOBILITY SIMULATION SUITE ELECTRIC MOBILITY SIMULATION SUITE . -

USER GROUP »Governance, Risk, Compliance in Der IT« 14

USER GROUP »Governance, Risk, Compliance in der IT« 14. Arbeitstreffen Leipzig, 26./27. April 2018 THEMENSCHWERPUNKT „Governance, Risk & Control von IT-Sourcing und Cloud Computing: Anforde- rungen, Herausforderungen und Lösungsansätze“ FACHLICHE LEITUNG Prof. Dr. Nils Urbach Universität Bayreuth MITGLIEDER DER USER GROUP MEDIENPARTNER ORGANISATORISCHES TERMIN 26./27. April 2018 ANSPRECHPARTNER Yvonne Weißflog Seite | 2 T +49 341 98988-422 F +49 341 98988-9444 E [email protected] VERANSTALTUNGSORT Alte Essig-Manufactur Paul-Gruner-Straße 44 | 04107 Leipzig T +49 341 2 67 80 I www.michaelis-leipzig.de/de/alte-essig- manufactur/ ABENDVERANSTALTUNG Weinwirtschaft Leipzig Thomaskirchhof 13/14 | 04109 Leipzig T +49 341 49614606 I www.weinwirtschaft-leipzig.de HOTEL Eine Auswahl an Übernachtungsmöglichkeiten finden Sie unter: www.softwareforen.de/hotelempfehlungen Bitte nutzen Sie die Buchungscodes des jeweiligen Hotels, um auf die vergünstigten Konditionen der Leipziger Foren zuzugreifen. User Group »Governance, Risk, Compliance in der IT« www.softwareforen.de/it-governance RÜCKBLICK ARBEITSTREFFEN 13. Arbeitstreffen – 23./24. November 2017 Policies vs. Geschäftsziele: IT-GRC im Spannungsfeld von Effektivität und angemessener Regelungstiefe Seite | 3 12. Arbeitstreffen – 04./05. Mai 2017 Tools & Co: Automatisierung von IT-GRC - Wie bitte? Anforderungen, Möglichkeiten & Erfahrungsberichte 11. Arbeitstreffen – 10./ 11. November 2016 IT-Konsumerisierung, Cloud Computing und Schatten-IT: Neue Anforde- rungen an das GRC im Zeitalter der Digitalisierung? 10. Arbeitstreffen – 21./22. April 2016 Flexibilität vs. Kontrolle: Erfahrungen und Best Practices aus den aktuellen Anforderungen an die IT-Compliance 9. Arbeitstreffen – 26./ 27. November 2015 SIEM – Schluss mit dem Unwissen über die Gefahr? 8. Arbeitstreffen – 5./6. Mai 2015 Management und Controlling von IT-Risiken 7.