Leaving Home Global Powers of Retailing 2011 Global Retail Perspectives from Deloitte

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Developing Employees As Organisational Assets

Developing Employees as Organisational Assets INTRODUCTION The Kingfisher Recruitment • The Person Specification How KMDS is evolving commercial and afterwards in key functions The Group requires from prospec- Kingfisher plc is one of Europe’s leading retailers based Management Development Scheme Investing in a trainee over ten years tive KMDS trainees: The KMDS was launched in 1995 and • a post-graduate certificate in man- around three main sectors - DIY, electrical and general involves significant cost as well as today has 172 individuals on the scheme agement studies from Templeton • excellent interpersonal skills merchandise. The company employs over 130,000 people in invest- risk. The risk includes choosing the working across the Group. All individu- College, Oxford The KMDS represents a key • enthusiasm and drive to become ment by the organisation in its human wrong type of person and equally als following the KMDS route joined in • a ‘skills tool-box’ consisting of 2,900 stores across 15 countries and has some of the best senior managers within 7-10 years assets. The scheme takes high-poten- importantly losing the person to anoth- their early 20s. Recently Kingfisher has day-release training to develop per- known retail brands in Europe, including B&Q, Castorama, • innovative approach to challenges tial graduates who want to make a er organisation during the training recognised that there are benefits in sonal skills Comet, Darty, BUT, Woolworths and Superdrug among opening up the process to existing high- career in retail, and provides them with process. For this reason, Kingfisher • the ability to analyse and make • a ‘buddy’ who is already on the others. -

QUEST Integration

Pharmacy Name Address City State Zip Phone No Hours24 County Longs Drug Store 1330 Pali Hwy Honolulu Hi 968132230 8085365542 Y Honolulu Longs Drug Store 555 Kilauea Ave Hilo Hi 967203011 8089359075 Y Hawaii Shiigi Drug Co., Inc. 333 Kilauea Ave Ste 109 Hilo Hi 967203013 8089350001 N Hawaii Don Quijote Drugs 801 Kaheka St Honolulu Hi 968143725 8089736661 N Honolulu Longs Drug Store 1088 Bishop St Ste 113 Honolulu Hi 968133109 8085365706 N Honolulu Longs Drug Store 4211 Waialae Ave Honolulu Hi 968165319 8087320782 N Honolulu Longs Drug Store 1620 N School St Honolulu Hi 968171844 8088410724 Y Honolulu The Queens Medical Center Phcy 1301 Punchbowl St Honolulu Hi 968132402 8085474238 Y Honolulu Molokai Drugs Inc 28 Kamoi Street Ste 100 Kaunakakai Hi 967480000 8085535790 N Maui Longs Drug Store 850 Kamehameha Hwy Ste 107 Pearl City Hi 967822682 8084554555 Y Honolulu Longs Drug Store 46-047 Kamehameha Hwy Ste C Kaneohe Hi 967443736 8082354551 Y Honolulu Longs Drug Store 1450 Ala Moana Blvd Ste 2004 Honolulu Hi 968144671 8089494010 N Honolulu Westside Pharmacy 1-3845 Kaumualii Highway Hanapepe Hi 96716 8083355342 N Kauai Times Pharmacy 1425 Liliha St Honolulu Hi 968173522 8085225078 N Honolulu Longs Drug Store 70 E Kaahumanu Ave Kahului Hi 967322176 8088770068 N Maui Longs Drug Store 98-1005 Moanalua Rd Spc 400 Aiea Hi 967014775 8084880958 N Honolulu Longs Drug Store 609 Kailua Rd Kailua Hi 967342839 8082619794 N Honolulu Queens Pob I Pharmacy 1380 Lusitana St Honolulu Hi 968132449 8085474745 N Honolulu Longs Drug Store 2750 Woodlawn Dr Honolulu Hi 968221841 8089882151 N Honolulu Aiea Medical Pharmacy 99-128 Aiea Heights Dr Ste 103 Aiea Hi 967013916 8088405680 N Honolulu Longs Drug Store 3221 Waialae Ave Honolulu Hi 968165842 8087352811 Y Honolulu Plaza Pharmacy 321 N Kuakini St Ste 105 Honolulu Hi 968172375 8085479440 N Honolulu Pharmacare No. -

Don Quijote - Kaheka 801 KAHEKA STREET, HONOLULU, HAWAII 96814

FOR LEASE > FOOD COURT SPACE Don Quijote - Kaheka 801 KAHEKA STREET, HONOLULU, HAWAII 96814 Food Court Space for lease The food court is situated in the premier hub of commerce in the The space is located in the Don Quijote food court, which includes a Ala Moana area, just 5 minutes delightful array of local and Asian cuisines. The foot court provides walking distance to Ala Moana strong co-tenant synergies and ample outdoor seating for customers. Center, Ross Dress for Less, Walmart and Sam’s Club. Property Information Available Space: Space 14 (430 SF) Kapiolani Blvd Base Rent: Negotiable Kalakaua Ave Operating Expenses: $1.83 PSF/Mo Term: 3 - 5 years Features & Benefits: > Great visibility > Excellent foot traffic > The largest Asian grocery store on Oahu WAIKIKI MARIA SU (S) COLLIERS INTERNATIONAL | Hawaii Retail Services Division 220 S. King Street, Suite 1800 808 524 2666 Honolulu, Hawaii 96813 www.colliers.com/hawaii [email protected] This document has been prepared by Colliers International for advertising and general information only. Colliers International makes no guarantees, representations or warranties of any kind, expressed or implied, regarding the information including, but not limited to, warranties of content, accuracy and reliability. Any interested party should undertake their own inquiries as to the accuracy of the information. Colliers International excludes unequivocally all inferred or implied terms, conditions and warranties arising out of this document and excludes all liability for loss and damages arising there from. This publication is the copyrighted property of Colliers International and/or its licensor(s). ©2020. All rights reserved.. -

Die Antwort Auf Das Discountmodell

R Die Antwort auf das Discountmodell Ein neues Geschäftsmodell für den Lebensmitteleinzelhandel? Projekt XI August 2005 Eine Studie im Auftrag von The Coca-Cola Retailing Research Council Europe durchgeführt von McKinsey & Company Der Auftraggeber / Die Verfasser The Coca-Cola Retailing Research Council, Europe The Coca-Cola Retailing Research Council, Europe (CCRRCE) hat sich zur Aufgabe gemacht, den Lebensmitteleinzelhandel und das damit verbundene System der Warenverteilung in Europa besser zu verstehen. Er konzentriert sich darauf, wichtige Themen und Probleme zu erkennen und gezielt zu untersuchen. Die gewonnenen Erkenntnisse werden ggf. in einem geeigneten Forum präsentiert, damit die Informationen voll dazu genutzt werden können, die Warenverteilung des Lebensmitteleinzelhandels weiterzuentwickeln und effektiver zu gestalten. McKinsey & Company McKinsey & Company ist eine Managementberatung, die führenden Unternehmen und Organisationen hilft, ihre Performance durch entscheidende, nachhaltige und substanzielle Verbesserungen zu steigern. Über die letzten sieben Jahrzehnte hat die Firma stets an ihrem Hauptziel festgehalten: Unternehmen als vertrauenswürdigster, externer Berater zur Seite zu stehen, wenn die Unternehmensführung vor kritischen Entscheidungen steht. Mit etwa 7.800 Beratern, die sich auf 85 Niederlassungen in 44 Ländern verteilen, berät McKinsey Unternehmen über Strategie, operatives Geschäft, Organisation und Technologie. Die Firma verfügt nicht nur über umfassende Erfahrung in allen großen Branchen und Hauptfunktionsbereichen, -

Finance Project

MASTER OF SCIENCE IN FINANCE MASTERS FINAL WORK PROJECT EQUITY RESEARCH: HORNBACH BAUMARKT AG JOÃO MARIA GONÇALVES PAIVA DÓRDIO RODRIGUES SUPERVISOR: ANA ISABEL ORTEGA VENÂNCIO OCTOBER 2020 Acknowledgements This paper represents the end of a journey started in 2018 and I would like to express my sincerest gratitude to all persons involved in these 2 years of the Masters. Firstly, to Professor Ana Venâncio for the guidance, time and patience, not only during this project, but also during classes. Secondly, to my family, parents, sister and grandmother, for supporting and believing in me. And last but not least, to my friends, new and old, for the moments shared in these past 2 years. i Abstract The following project is a valuation of the company Hornbach Baumarkt AG, based on publicly available information until the 6th November 2020. It follows the format recommended by the CFA Institute. Hornbach Baumarkt AG was chosen due to the interest in wanting to explore and learn about the DIY sector and by it being the only publicly traded German company. Hornbach Baumarkt AG is a Top 10 player in the DIY Home Improvement sector in Europe. It was created in 1993 after an IPO that saw Hornbach AG being subdivided in Hornbach Holding AG (Parent Company) and Hornbach Baumarkt AG, having the original company being founded in 1877, in Landau, Germany, but only making their first IPO in 1987. Today, Hornbach Baumarkt AG is a Child company of Hornbach Holding AG. The valuation was derived from an intrinsic valuation, based on a Discounted Cash Flow (DFC) method, more specifically, through a Free Cash Flow to the Firm (FCFF) perspective. -

Graham & Doddsville

Graham & Doddsville An investment newsletter from the students of Columbia Business School Inside this issue: Issue XXII Fall 2014 Wally Weitz — Omaha Dinner P. 3 Power of Good Management 5x5x5 Student Value Investing Wally Weitz is the Founder and President of Weitz Fund P. 4 Investment Management, an Omaha-based fund manager with over $5 billion in AUM. Influenced by the value investing Wally Weitz P. 6 philosophy of Benjamin Graham and Warren Buffett, Mr. Weitz started his career as a securities analyst in New York Guy Gottfried P. 14 after earning a BA in Economics from Carleton College in 1970. He then joined Chiles, Heider, & Co. in Omaha, Columbia IIC working there for ten years before starting his own fund in Meeting Ideas P. 22 Wally Weitz (Continued on page 6) Development Capital Partners P. 26 Guy Gottfried — Editors: The Value of Capital Allocation Matt Ford MBA 2015 Guy Gottfried is the Founder and Managing Partner of Rational Investment Group, LP, a Toronto-based investment Peter Pan firm following a concentrated, risk-averse value approach. MBA 2015 Prior to founding Rational, Mr. Gottfried was an analyst at Tom Schweitzer, CFA Fairholme Capital Management. He began his career at MBA 2015 Veritas Investment Research, Canada’s largest independent equity research firm. Mr. Gottfried graduated with a BBA Brendan Dawson with Honors from the Schulich School of Business at York MBA 2016 Guy Gottfried University, where he was a President’s Scholarship recipient. Scott DeBenedett (Continued on page 14) MBA 2016 Michael Herman Development Capital Partners — MBA 2016 The Changing Landscape in Africa Visit us at: Development Capital Partners (DCP) is a New York- www.grahamanddodd.com based investment manager focused exclusively on Afri- www.csima.org can markets. -

FIC-Prop-65-Notice-Reporter.Pdf

FIC Proposition 65 Food Notice Reporter (Current as of 9/25/2021) A B C D E F G H Date Attorney Alleged Notice General Manufacturer Product of Amended/ Additional Chemical(s) 60 day Notice Link was Case /Company Concern Withdrawn Notice Detected 1 Filed Number Sprouts VeggIe RotInI; Sprouts FruIt & GraIn https://oag.ca.gov/system/fIl Sprouts Farmers Cereal Bars; Sprouts 9/24/21 2021-02369 Lead es/prop65/notIces/2021- Market, Inc. SpInach FettucIne; 02369.pdf Sprouts StraIght Cut 2 Sweet Potato FrIes Sprouts Pasta & VeggIe https://oag.ca.gov/system/fIl Sprouts Farmers 9/24/21 2021-02370 Sauce; Sprouts VeggIe Lead es/prop65/notIces/2021- Market, Inc. 3 Power Bowl 02370.pdf Dawn Anderson, LLC; https://oag.ca.gov/system/fIl 9/24/21 2021-02371 Sprouts Farmers OhI Wholesome Bars Lead es/prop65/notIces/2021- 4 Market, Inc. 02371.pdf Brad's Raw ChIps, LLC; https://oag.ca.gov/system/fIl 9/24/21 2021-02372 Sprouts Farmers Brad's Raw ChIps Lead es/prop65/notIces/2021- 5 Market, Inc. 02372.pdf Plant Snacks, LLC; Plant Snacks Vegan https://oag.ca.gov/system/fIl 9/24/21 2021-02373 Sprouts Farmers Cheddar Cassava Root Lead es/prop65/notIces/2021- 6 Market, Inc. ChIps 02373.pdf Nature's Earthly https://oag.ca.gov/system/fIl ChoIce; Global JuIces Nature's Earthly ChoIce 9/24/21 2021-02374 Lead es/prop65/notIces/2021- and FruIts, LLC; Great Day Beet Powder 02374.pdf 7 Walmart, Inc. Freeland Foods, LLC; Go Raw OrganIc https://oag.ca.gov/system/fIl 9/24/21 2021-02375 Ralphs Grocery Sprouted Sea Salt Lead es/prop65/notIces/2021- 8 Company Sunflower Seeds 02375.pdf The CarrIngton Tea https://oag.ca.gov/system/fIl CarrIngton Farms Beet 9/24/21 2021-02376 Company, LLC; Lead es/prop65/notIces/2021- Root Powder 9 Walmart, Inc. -

Recent Revisions to Japanese Tender Offer Rules: Toward Transparency and Fairness

JUNE 2007 JONES DAY COMMENTARY Recent REvisions to JApanesE Tender Offer RulEs: TOward Transparency and Fairness DEvElOpments iN ThE JApanesE economy in 1991, Japanese businesses underwent significant corporate restructuring for more than a M&A Market decade, and the number of tender offers gradually Japanese tender offer regulations were substantially increased as part of the effort to recover from the amended in December 2006 in the wake of recent deflationary economy in the late 1990s. Tender offers hostile-takeover activities in Japan. The tender offer in Japan in 2005 and 2006 numbered 50 and 68, regulations, which were first introduced in Japan in respectively. However, after the collapse of the eco- 1971, were substantially revised in 1990. These revised nomic bubble, hostile offers were almost nonexistent regulations form the basis of the current legal frame- in Japan until 2000, when a Japanese activist fund work. The additional revisions made in 2006 (the managed by Mr. Yoshiaki Murakami engaged in a “Revisions”) are intended to increase the transparency hostile offer for Shoei Co., Ltd., a real estate com- and fairness of tender offers by, for example, enhanc- pany. This was followed by hostile tender offers made ing the disclosure requirements and expanding the simultaneously for two mid-sized companies, Sotoh scope of application of the tender offer rules. Corporation and Yushiro Chemical Industry Co., Ltd., by Steel Partners Japan, a U.S.-based activist fund, in Historically, the pace of M&A activity, particularly take- December 2003. While the level of hostile offers is still overs, in Japan has been relatively slow. -

Global Powers of Retailing 2019 Contents

Global Powers of Retailing 2019 Contents Top 250 quick statistics 4 Global economic outlook 5 Top 10 highlights 8 Global Powers of Retailing Top 250 11 Geographic analysis 19 Product sector analysis 23 New entrants 27 Fastest 50 30 Study methodology and data sources 35 Endnotes 39 Contacts 41 Welcome to the 22nd edition of Global Powers of Retailing. The report identifies the 250 largest retailers around the world based on publicly available data for FY2017 (fiscal years ended through June 2018), and analyzes their performance across geographies and product sectors. It also provides a global economic outlook, looks at the 50 fastest-growing retailers, and highlights new entrants to the Top 250. Top 250 quick statistics, FY2017 Minimum retail US$4.53 US$18.1 revenue required to be trillion billion among Top 250 Aggregate Average size US$3.7 retail revenue of Top 250 of Top 250 (retail revenue) billion 5-year retail Composite 5.7% revenue growth net profit margin 5.0% Composite (CAGR from Composite year-over-year retail FY2012-201 2.3% return on assets revenue growth 3.3% Top 250 retailers with foreign 23.6% 10 operations Share of Top 250 Average number aggregate retail revenue of countries where 65.6% from foreign companies have operations retail operations Source: Deloitte Touche Tohmatsu Limited. Global Powers of Retailing 2019. Analysis of financial performance and operations for fiscal years ended through June 2018 using company annual reports, Supermarket News, Forbes America’s largest private companies and other sources. 4 Global economic outlook 5 Global Powers of Retailing 2019 | Global economic outlook The global economy is currently at a turning point. -

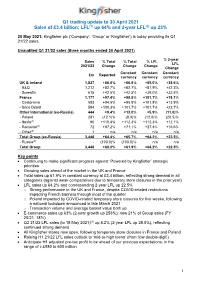

Q1 Trading Update to 30 April 2021 Sales of £3.4 Billion; LFL(1) up 64% and 2-Year LFL(2) up 23%

Q1 trading update to 30 April 2021 Sales of £3.4 billion; LFL(1) up 64% and 2-year LFL(2) up 23% 20 May 2021: Kingfisher plc (‘Company’, ‘Group’ or ‘Kingfisher’) is today providing its Q1 21/22 sales. Unaudited Q1 21/22 sales (three months ended 30 April 2021) % 2-year Sales % Total % Total % LFL LFL 2021/22 Change Change Change Change Constant Constant Constant £m Reported currency currency currency UK & Ireland 1,827 +66.8% +66.8% +65.0% +38.6% - B&Q 1,212 +82.7% +82.7% +81.9% +42.3% - Screwfix 615 +42.5% +42.5% +39.0% +32.5% France 1,177 +97.4% +98.8% +101.7% +18.1% - Castorama 583 +94.5% +95.8% +101.8% +13.9% - Brico Dépôt 594 +100.3% +101.7% +101.7% +22.7% Other International (ex-Russia) 444 +9.4% +13.0% +5.9% (11.0)% - Poland 281 (12.1)% (8.9)% (12.0)% (20.5)% - Iberia(3) 90 +110.8% +112.3% +112.3% +12.1% - Romania(4) 72 +67.2% +71.1% +27.4% +16.6% - Other(5) 1 n/a n/a n/a n/a Total Group (ex-Russia) 3,448 +64.4% +65.7% +64.2% +22.5% - Russia(6) - (100.0)% (100.0)% n/a n/a Total Group 3,448 +60.0% +61.9% +64.2% +22.5% Key points • Continuing to make significant progress against ‘Powered by Kingfisher’ strategic priorities • Growing sales ahead of the market in the UK and France • Total sales up 61.9% in constant currency at £3.4 billion, reflecting strong demand in all categories (against weak comparatives due to temporary store closures in the prior year) • LFL sales up 64.2% and corresponding 2-year LFL up 22.5% o Strong performance in the UK and France, despite COVID-related restrictions impacting French banners through most -

Screwfix Builds Bricks and Mortar Presence with 300Th Store

SCREWFIX BUILDS BRICKS AND MORTAR PRESENCE WITH 300TH STORE Trade and DIY retailer Screwfix is now even more accessible for busy tradesmen on the move across the UK, with the launch of its 300th trade counter in Birstall, West Yorkshire. Screwfix started life as a mail order catalogue-based business, but in response to customers needing to get their tools quickly and conveniently, a rapid store expansion has followed, with 60 stores being opened in 2013 alone. The national store network now gives the nation’s tradesmen, which includes builders, plumbers and electricians, as well as serious DIY-ers, greater access to tools and supplies when on the move in-between jobs. Meeting this 300th store milestone is equally significant given that Screwfix opened its very first store just eight years ago in Yeovil, Somerset. This need for a fast and easy shopping experience has been boosted by an early adoption of a multi-channel model as Screwfix chief executive Andrew Livingston explains: “It really is a case of time is money for our customers because they are busy out and about on the road, from job to job. So we’re doing all we can to help them buy the tools and accessories they need as quickly and easily as possible. As we open the doors to more and more stores across the country, we become even more convenient for our customers. This, topped with our Click & Collect technology, mobile website and smartphone apps means that customers can shop when they want and how they want. “Tradesmen rely on us for the ease and speed of online and over-the-phone ordering, but they also enjoy the store experience thanks to regular – often daily - interaction with staff, many of whom have a background in the trade.” The 300th Screwfix store will open its doors in Birstall, West Yorkshire, joining 8 other stores across West Yorkshire. -

Deloitte Studie

Global Powers of Retailing 2018 Transformative change, reinvigorated commerce Contents Top 250 quick statistics 4 Retail trends: Transformative change, reinvigorated commerce 5 Retailing through the lens of young consumers 8 A retrospective: Then and now 10 Global economic outlook 12 Top 10 highlights 16 Global Powers of Retailing Top 250 18 Geographic analysis 26 Product sector analysis 30 New entrants 33 Fastest 50 34 Study methodology and data sources 39 Endnotes 43 Contacts 47 Global Powers of Retailing identifies the 250 largest retailers around the world based on publicly available data for FY2016 (fiscal years ended through June 2017), and analyzes their performance across geographies and product sectors. It also provides a global economic outlook and looks at the 50 fastest-growing retailers and new entrants to the Top 250. This year’s report will focus on the theme of “Transformative change, reinvigorated commerce”, which looks at the latest retail trends and the future of retailing through the lens of young consumers. To mark this 21st edition, there will be a retrospective which looks at how the Top 250 has changed over the last 15 years. 3 Top 250 quick statistics, FY2016 5 year retail Composite revenue growth US$4.4 net profit margin (Compound annual growth rate CAGR trillion 3.2% from FY2011-2016) Aggregate retail revenue 4.8% of Top 250 Minimum retail Top 250 US$17.6 revenue required to be retailers with foreign billion among Top 250 operations Average size US$3.6 66.8% of Top 250 (retail revenue) billion Composite year-over-year retail 3.3% 22.5% 10 revenue growth Composite Share of Top 250 Average number return on assets aggregate retail revenue of countries with 4.1% from foreign retail operations operations per company Source: Deloitte Touche Tohmatsu Limited.