Final Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2019 Tanzania in Figures

2019 Tanzania in Figures The United Republic of Tanzania 2019 TANZANIA IN FIGURES National Bureau of Statistics Dodoma June 2020 H. E. Dr. John Pombe Joseph Magufuli President of the United Republic of Tanzania “Statistics are very vital in the development of any country particularly when they are of good quality since they enable government to understand the needs of its people, set goals and formulate development programmes and monitor their implementation” H.E. Dr. John Pombe Joseph Magufuli the President of the United Republic of Tanzania at the foundation stone-laying ceremony for the new NBS offices in Dodoma December, 2017. What is the importance of statistics in your daily life? “Statistical information is very important as it helps a person to do things in an organizational way with greater precision unlike when one does not have. In my business, for example, statistics help me know where I can get raw materials, get to know the number of my customers and help me prepare products accordingly. Indeed, the numbers show the trend of my business which allows me to predict the future. My customers are both locals and foreigners who yearly visit the region. In June every year, I gather information from various institutions which receive foreign visitors here in Dodoma. With estimated number of visitors in hand, it gives me ample time to prepare products for my clients’ satisfaction. In terms of my daily life, Statistics help me in understanding my daily household needs hence make proper expenditures.” Mr. Kulwa James Zimba, Artist, Sixth street Dodoma.”. What is the importance of statistics in your daily life? “Statistical Data is useful for development at family as well as national level because without statistics one cannot plan and implement development plans properly. -

Spatial Uncertainties in Fluoride Levels and Health Risks in Endemic Fluorotic

Groundwater for Sustainable Development 14 (2021) 100618 Contents lists available at ScienceDirect Groundwater for Sustainable Development journal homepage: www.elsevier.com/locate/gsd Research paper Spatial uncertainties in fluoridelevels and health risks in endemic fluorotic regions of northern Tanzania Julian Ijumulana a,b,c,*, Fanuel Ligate a,b,d, Regina Irunde a,b,e, Prosun Bhattacharya a,g, Jyoti Prakash Maity f, Arslan Ahmad g,h,i, Felix Mtalo b a KTH-International Groundwater Arsenic Research Group, Department of Sustainable Development, Environmental Science and Engineering, KTH Royal Institute of Technology, Teknikringen 10B, SE-100 44 Stockholm, Sweden b Department of Water Resources Engineering, College of Engineering and Technology, University of Dar Es Salaam, Dar Es Salaam, Tanzania c Department of Transportation and Geotechnical Engineering, College of Engineering and Technology, University of Dar Es Salaam, Dar Es Salaam, Tanzania d Department of Chemistry, Mkwawa College of Education, University of Dar Es Salaam, Tanzania e Department of Chemistry, College of Natural and Applied Sciences, University of Dar Es Salaam, Tanzania f Department of Earth and Environmental Sciences, National Chung Cheng University, 168 University Road, Min-Hsiung, Chiayi County, 62102, Taiwan g KWR Water Cycle Research Institute, Groningenhaven 7, 3433 PE Nieuwegein, The Netherlands h SIBELCO Ankerpoort NV, Op de Bos 300, 6223 EP Maastricht, the Netherlands i Department of Environmental Technology, Wageningen University and Research (WUR), Wageningen, The Netherlands ARTICLE INFO ABSTRACT Keywords: Spatial uncertainty caused by large-scale variation in fluoride(F ) occurrence remains a setback for water supply Groundwater authorities in the F belts of the world. It is estimated that approximately 80 million people in the East African Fluoride contamination Rift Valley (EARV) regions and volcanic areas exhibit a wide variety of fluorosissymptoms due to drinking water Probability kriging with F‾ concentrations higher than 1.5 mg/L (WHO guideline limit). -

Dissemination Meeting Held in Arusha, Tanzania (10 December 2019)

REPORT OF THE WILLOWS IMPACT EVALUATION (WIE) DISSEMINATION MEETING HELD IN ARUSHA, TANZANIA (10 DECEMBER 2019) PI: Prof. Sia Msuya Kilimanjaro Christian Medical Center P.O. Box 3010 Moshi, Tanzania Tel: +255- 2754379 E-mail: [email protected] 1 Table of contents 1.0. Background .............................................................................................................................. 3 2.0. Meeting Participants ................................................................................................................ 3 3.0. Meeting Presentations .............................................................................................................. 4 4.0. Discussion and Meeting Recommendations ............................................................................ 6 5.0. Closing Remarks ...................................................................................................................... 9 6.0. Conclusions ............................................................................. Error! Bookmark not defined. 7.0. Acknowledgements ............................................................................................................... 12 8.0. Appendices .............................................................................. Error! Bookmark not defined. 2 1.0. Background The Willows Impact Evaluation project (hereafter WIE is a collaborative evaluation programme between (Kilimanjaro Christian Medical University College (hereafter KCMUCo) and the Harvard T.H Chan School -

Classification of Chagga Agroforestry Homegardens And

CLASSIFICATION OF CHAGGA AGROFORESTRY HOMEGARDENS AND THEIR CONTRIBUTIONS TO FOOD, INCOME AND WOOD ENERGY TO COMMUNITIES OF ROMBO DISTRICT, TANZANIA JIMSON MBWIGA A DISSSERTATION SUBMITTED IN PARTIAL FULFILMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF SCIENCE IN MANAGEMENT OF NATURAL RESOURCES FOR SUSTAINABLE AGRICULTURE OF SOKOINE UNIVER SITY OF AGRICULTURE. MOROGORO, TANZANIA. 2016 ii ABSTRACT The present study was carried out in 2014 in Rombo District, Kilimanjaro, Tanzania, in order to classify Chagga agroforestry homegardens and establish their relative contributions to food, income and wood energy to the local communities. The study methodology included random selection of four divisions, one ward from each division, one village from each ward and 30 households per village forming a total sample of 120 households. A social survey was subsequently carried out using questionnaires employed to household heads and checklists of probe questions for key informants. Data were analyzed using the Statistical Package for Social Sciences (SPSS) version 16.0 and Microsoft Excel Programs. Analysis of Variance (ANOVA) was performed to compare means between and within treatments and the Least Significant Difference (LSD) was used to separate the significantly differing means. Results indicated that all five renewable natural resource components of woody perennials, herbaceous crops, animals, insects and aquatic life-forms were present in the Chagga agroforestry homegardens which were in various interactions broadly classified into nine agroforestry systems with the Agrosilvopastoral system being the most widely spread and the Agroaquosilvicultural, Agroaquosilvopastoral, Aposilvopastoral and Silvopastoral systems being, in that order, the least spread throughout the district. Spatial arrangements of components were the most common arrangement forming agroforestry technologies like boundary planting, mixed intercropping and live fences. -

Revisiting the Rural-Urban Linkages in East Africa: Continuity Or Breakdown in the Spatial Model of Rural Development? the Case of the Kilimanjaro Region in Tanzania

Belgeo Revue belge de géographie 1 | 2020 Miscellaneous Revisiting the rural-urban linkages in East Africa: Continuity or breakdown in the spatial model of rural development? The case of the Kilimanjaro region in Tanzania Bernard Charlery de la Masselière, François Bart, Bénédicte Thibaud and Rémi Benos Electronic version URL: http://journals.openedition.org/belgeo/38669 DOI: 10.4000/belgeo.38669 ISSN: 2294-9135 Publisher: National Committee of Geography of Belgium, Société Royale Belge de Géographie Electronic reference Bernard Charlery de la Masselière, François Bart, Bénédicte Thibaud and Rémi Benos, “Revisiting the rural-urban linkages in East Africa: Continuity or breakdown in the spatial model of rural development?”, Belgeo [Online], 1 | 2020, Online since 27 May 2020, connection on 20 January 2021. URL: http://journals.openedition.org/belgeo/38669 ; DOI: https://doi.org/10.4000/belgeo.38669 This text was automatically generated on 20 January 2021. Belgeo est mis à disposition selon les termes de la licence Creative Commons Attribution 4.0 International. Revisiting the rural-urban linkages in East Africa: Continuity or breakdown i... 1 Revisiting the rural-urban linkages in East Africa: Continuity or breakdown in the spatial model of rural development? The case of the Kilimanjaro region in Tanzania Bernard Charlery de la Masselière, François Bart, Bénédicte Thibaud and Rémi Benos AUTHOR'S NOTE This paper is a result of some extensive research carried out under the European programme RurbanAfrica (www.rurbanafrica.ku.dk) coordinated by the university of Copenhagen. Introduction 1 In Africa, agriculture transformation and rural livelihood diversification on one side, rapid growth of the urban system on another side are the general indices of the emergence of a new model of development. -

Basic Demographic and Socio-Economic Profile

The United Republic of Tanzania Basic Demographic and Socio-Economic Profile National Bureau of Statistics Ministry of Finance Dar es Salaam and Office of Chief Government Statistician Ministry of State, President ‟s Office, State House and Good Governance Zanzibar April, 2014 UNITED REPUBLIC OF TANZANIA, ADMINISTRATIVE BOUNDARIES Basic Demographic and Socio-Economic Profile Foreword The 2012 Population and Housing Census (PHC) for the United Republic of Tanzania was carried out on the 26th August, 2012. This was the fifth Census after the Union of Tanganyika and Zanzibar in 1964. Other censuses were carried out in 1967, 1978, 1988 and 2002. The 2012 PHC, like previous censuses, will contribute to the improvement of quality of life of Tanzanians through the provision of current and reliable data for policy formulation, development planning and service delivery as well as for monitoring and evaluating national and international development frameworks. The 2012 PHC is unique as the collected information will be used in monitoring and evaluating the Development Vision 2025 for Tanzania Mainland and Zanzibar Development Vision 2020, Five Year Development Plan 2011/12–2015/16, National Strategy for Growth and Reduction of Poverty (NSGRP) commonly known as MKUKUTA and Zanzibar Strategy for Growth and Reduction of Poverty (ZSGRP) commonly known as MKUZA. The Census will also provide information for the evaluation of the Millennium Development Goals (MDGs) in 2015. The Poverty Monitoring Master Plan, which is the monitoring tool for NSGRP and ZSGRP, mapped out core indicators for poverty monitoring against the sequence of surveys, with the 2012 PHC being one of them. Several of these core indicators for poverty monitoring are measured directly from the 2012 PHC. -

The Copyright of This Thesis Vests in the Author. No Quotation from It Or Information Derived from It Is to Be Published Without Full Acknowledgement of the Source

The copyright of this thesis vests in the author. No quotation from it or information derived from it is to be published without full acknowledgement of the source. The thesis is to be used for private study or non- commercial research purposes only. Published by the University of Cape Town (UCT) in terms of the non-exclusive license granted to UCT by the author. University of Cape Town i ESTABLISHMENT OF A COMPREHENSIVE SURVEILLANCE SYSTEM FOR ACUTE PESTICIDE POISONING IN TANZANIA Elikana Eliona Lekei LKXELI001 SUBMITTED TO THE UNIVERSITY OF CAPE TOWN In fulfillment of the requirements for the degree DOCTOR OF PHILOSOPHY Faculty Health Sciences UNIVERSITY OF CAPE TOWN Date of submission: 27th August 2012 Supervisor: Prof. Leslie London School ofy Public of Health Cape & Family Medicine Town Faculty of Health Sciences Anzio Road, Observatory 7925 South Africa E mail: [email protected] Tel: 27 21 4066524 Universit Co Supervisor: Dr Aiwerasia V Ngowi Muhimbili University of Health and Allied Sciences (MUHAS) School of Public Health and Social Sciences Department of Environmental and Occupational Health P O Box 65015 Dar es Salaam, Tanzania Tel: 255 2150302-6 Ext. 236; Fax: 255 22 2150465 i ii DECLARATION I, Elikana Eliona Lekei, hereby declare that the work on which this dissertation/thesis is based is my original work (except where acknowledgements indicate otherwise) and that neither the whole work nor any part of it has been, is being, or is to be submitted for another degree in this or any other university. I empower the university to reproduce for the purpose of research either the whole or any portion of the contents in any manner whatsoever. -

The Pastoralists' Resilience and Innovative Adaptation Strategies On

International Journal of Environment and Bioenergy, 2017, 12(1): 47-61 International Journal of Environment and Bioenergy ISSN: 2165-8951 Journal homepage: www.ModernScientificPress.com/Journals/IJEE.aspx Florida, USA Article The Pastoralists’ Resilience and Innovative Adaptation Strategies on Impacts of Climate Change in Rangelands of Longido District, Tanzania Laurent Joseph1*and Abiud Kaswamila2 1Department of Management Science, Faculty of Economics and Management Science, Institute of Finance Management, Box 2372, Mwanza, Tanzania 2Department of Geography and Environmental Studies, University of Dodoma, P.O. Box 395, Dodoma, Tanzania *Author to whom correspondence should be addressed; E-Mail: [email protected]; Article history: Received 3 March 2017, Revised 3 April 2017, Accepted 10 April 2017, Published 14 April 2017. Abstract: The study investigated pastoralists’ resilience and innovative adaptation strategies to the impacts of climate change in Longido district. Data were collected using several methods including household survey, Focus Group Discussion, interviews and field visits. The results indicate that pastoralist’s resilience and adaptation strategies varied from one village to another. The major strategies were migration, construction and use of water reservoirs, use of traditional weather forecasting techniques, regulation of livestock reproduction, and use of by-laws. Keywords: Pastoralists, resilience, innovative adaptation strategies, climate change rangelands, Longido District. 1. Introduction Climate is a vital aspect for the survival of animals and plants all over the world but the change of its characteristics in terms of temperature increase and rain shortage, disturbs the whole ecosystem, Copyright © 2017 by Modern Scientific Press Company, Florida, USA Int. J. Environ. Bioener. 2017, 12(1) : 47-61 48 especially for pastoralists and farmers who directly depend on natural resources for their survival (Waugh, 2009). -

Pangani Basin: a Situation Analysis

Pangani Basin: A Situation Analysis IUCN Eastern Africa Programme 2003 i Published by: Copyright: © 2003 International Union for Conservation of Nature and Natural Resources This publication may be produced in whole or part and in any form for education or non-profit uses, without special permission from the copyright holder, provided acknowledgement of the source is made. IUCN would appreciate receiving a copy of any publication which uses this publication as a source. No use of this publication may be made for resale or other commercial purpose without the prior written permission of IUCN. Citation: IUCN Eastern Africa Programme, 2003. The Pangani River Basin: A Situation Analysis, xvi + 104pp. ISBN: 2-8317-0760-9 Design and layout: Gordon O. Arara Printed by: ScanHouse Press Ltd. Photo 1: The summit of Mount Kilimanjaro; Photo 2: Forest stand at 1 Shire Njoro; Photo 3: Gate controlling the release of water into irrigation furrows; Photo 4: Children swimming in an irrigation 3 4 reservoir; Photo 5: Sisal plantations; Photo 6: Irrigated rice scheme; 2 Photo 7: Water gauging station at Chemka Spring; Photo 8: Vandalized gate controlling the release of water into irrigation furrows; Photo 9: 5 Dam wall at Nyumba ya Mungu Reservoir (color changes mark the declining water levels); Photo 10: A vendor sells water from a borehole 6 9 10 Photos 1, 3, 5, 6, 8, 9 copyright 2003 Kelly West; Photos 2, 7 7 8 copyright 2002 Kim Geheb; Photos 4, 10 copyright 2003 Ger Bergkamp. Available from: IUCN- EARO Publications Service Unit, P. O. Box 68200 - 00200, Nairobi, Kenya; Telephone ++ 254 20 890605-12; Fax ++ 254 20 890615; E-mail: [email protected] The designations of geographical entities in this book, and the presentation of the material, do not imply the expression of any opinion whatsoever on the part of the participating organiza- tions concerning the legal status of any country, territory, or area, or of its authorities, or con- cerning the delimitation of its frontiers or boundaries. -

Arumeru District Catherine W

Conservation agriculture as practised in Tanzania Conservation agriculture in Africa series Series editors Bernard Triomphe Josef Kienzle Martin Bwalya Soren Damgaard-Larsen Titles Conservation agriculture as practised in Ghana Philip Boahen, Benjamin Addo Dartey, Genevieve Delali Dogbe, E. Asare Boadi, Bernard Triomphe, Soren Daamgard-Larsen, John Ashburner Conservation agriculture: a Uganda case study Paul Nyende, Anthony Nyakuni, John Peter Opio, Wilfred Odogola Conservation agriculture in Zambia: a case study of Southern Province Frédéric Baudron, Herbert M. Mwanza, Bernard Triomphe, Martin Bwalya Conservation agriculture as practised in Kenya: two case studies Pascal Kaumbutho, Josef Kienzle, editors Laikipia District Tom Apina, Paul Wamai, Philip Mwangi Siaya District Philip K. Mwangi, Kennedy O. Okelo, Tom Apina Conservation agriculture as practised in Tanzania: three case studies Richard Shetto, Marietha Owenya, editors Arumeru District Catherine W. Maguzu, Dominick E. Ringo, Wilfred Mariki, Marietha Owenya, Flora Kola, Charles Leseyo Karatu District Dominick E. Ringo, Catherine W. Maguzu, Wilfred Mariki, Marietha Owenya, Njumbo, Frank Swai Mbeya District Saidi Mkomwa, Ahaz Mussei, Remmy Mwakimbwala, Ndabhemeye Mulengera, Elimpaa Kiranga Conservation agriculture as practised in Tanzania: three case studies Richard Shetto, Marietha Owenya, editors Arumeru District Karatu District Mbeya District Publishers African Conservation Tillage Network (ACT) PO Box 14733, Westlands Nairobi 00800, Kenya tel and fax: +254 20 445 1391 website: -

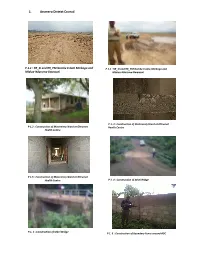

1. Arumeru District Council

1. Arumeru District Council P.1.1 : RR_SI and RR_PM Gombe Estate Mmbogo and P 1.1 : RR_SI and RR_PM Gombe Estate‐Mmbogo and Mlalua‐Nduruma‐Bwawani Mlalua‐Nduruma‐Bwawani P 1. 3 : Construction of Materninty Ward at Oltrumet P 1.2 : Construction of Materninty Ward at Oltrumet Health Centre Health Centre P 1.5 : Construction of Materninty Ward at Oltrumet Health Centre P 1. 4 : Construction of Sekei Bridge P.1. 5 : Construction of Sekei Bridge P 1. 6 : Construction of Boundary Fence around ADC 2. BAHI DISTRICT COUNCIL P 2.1: Aditors at contractor's site office reviewing P2.2: Uncompacted fill and poor concrete drawings workmanship on Kongogo Dam P 2.3: Un‐cemented Riprap at Kongogo Dam P 2.4: Poorly trimmed borrow pit at Kongogo P 2.5: Auditors checking dimensions compliance at Bahi DC P 2.6: Completed Kigwe Mnadani Drift Servant Quarters P 2.7: Auditors confirming a borehole at Mchito P 2.8: Auditors discussing with village leader at Borehole Mundemu on the way forward - dry borehole 3. Bukoba District Council P. 3.1: Cracks can be seen on the floor and walls of a newly constructed Agricultural Centre at Kikomelo P. 3.2: A newly constructed small bridge P 3.3: Oversize, dirty, sand stone coarse aggregates used for bridges/box culverts along Kalebe- Nyakibimbili road P 3.4: A bridge whose width was increased a day after casting without engineer’s approval along Kalebe- Nyakibimbili road 4. Geita District Council P 4.1: Poorly constructed pavement at the New Geita Bus Stand P 4.2: An auditor and PE Technician carrying out P 4.3: Well constructed headwalls and wingwalls and measurements at the New Geita Bus Stand poorly compacted approaches along Geita Town – Katoma Area Roads P 4.4 Poor workmanship on constructed headwall P 4.5 One of the existing “Bridges” along Sungusira and wing walls along Sungusira – Nyakaduha Road Road 5. -

Operation Bootstrap Africa Dignity Fall 2016 New Nurses for Tanzania!

Operation Bootstrap Africa Dignity Fall 2016 New Nurses for Tanzania! The first students have graduated from the new Arusha Lutheran Medical Centre School of Nursing in Arusha, Tanzania. This school was the dream of many and your gifts made it a reality! Each one of these young people had the cost of their training reduced by a $1,000 annual OBA scholarship. These new nurses will provide patient care in hospitals, dispensaries and clinics across Tanzania, helping to meet the critical shortage of nurses in the country. Arusha Lutheran Medical Centre School of Nursing First Graduation - August 20, 2016 What a wonderful and blessed day we had on the very first graduation of our ALMC School of Nursing. It was an amazing and historic event as the first graduation included three separate classes. The festivities were honored by our Bishop, Rev. Solomon Massangwa, serving as guest of honor. Dr. Kibira, the director of the ALMC Training Centre, welcomed the crowd and Prof. Jacobson shared the history of the dream and the miracles of the school coming into being. There were three classes; the first class of 19 which had begun in March of 2014, the second class of 22 which started in September of 2014, and a third class which undertook a one-year course in Community Health Technician training and graduated 37 students. The complete set of exam results was only available for the first class who had an amazing success rate of 99.9% in the exams! While we wait for national comparisons to arrive, we are confident that we will be one of the top nursing schools in the country.