General Growth Properties 2013 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

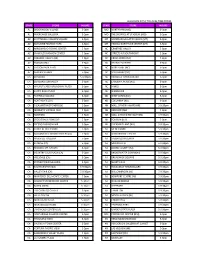

Prom 2018 Event Store List 1.17.18

State City Mall/Shopping Center Name Address AK Anchorage 5th Avenue Mall-Sur 406 W 5th Ave AL Birmingham Tutwiler Farm 5060 Pinnacle Sq AL Dothan Wiregrass Commons 900 Commons Dr Ste 900 AL Hoover Riverchase Galleria 2300 Riverchase Galleria AL Mobile Bel Air Mall 3400 Bell Air Mall AL Montgomery Eastdale Mall 1236 Eastdale Mall AL Prattville High Point Town Ctr 550 Pinnacle Pl AL Spanish Fort Spanish Fort Twn Ctr 22500 Town Center Ave AL Tuscaloosa University Mall 1701 Macfarland Blvd E AR Fayetteville Nw Arkansas Mall 4201 N Shiloh Dr AR Fort Smith Central Mall 5111 Rogers Ave AR Jonesboro Mall @ Turtle Creek 3000 E Highland Dr Ste 516 AR North Little Rock Mc Cain Shopg Cntr 3929 Mccain Blvd Ste 500 AR Rogers Pinnacle Hlls Promde 2202 Bellview Rd AR Russellville Valley Park Center 3057 E Main AZ Casa Grande Promnde@ Casa Grande 1041 N Promenade Pkwy AZ Flagstaff Flagstaff Mall 4600 N Us Hwy 89 AZ Glendale Arrowhead Towne Center 7750 W Arrowhead Towne Center AZ Goodyear Palm Valley Cornerst 13333 W Mcdowell Rd AZ Lake Havasu City Shops @ Lake Havasu 5651 Hwy 95 N AZ Mesa Superst'N Springs Ml 6525 E Southern Ave AZ Phoenix Paradise Valley Mall 4510 E Cactus Rd AZ Tucson Tucson Mall 4530 N Oracle Rd AZ Tucson El Con Shpg Cntr 3501 E Broadway AZ Tucson Tucson Spectrum 5265 S Calle Santa Cruz AZ Yuma Yuma Palms S/C 1375 S Yuma Palms Pkwy CA Antioch Orchard @Slatten Rch 4951 Slatten Ranch Rd CA Arcadia Westfld Santa Anita 400 S Baldwin Ave CA Bakersfield Valley Plaza 2501 Ming Ave CA Brea Brea Mall 400 Brea Mall CA Carlsbad Shoppes At Carlsbad -

Alabama Arizona Arkansas California Riverchase Galleria | Hoover, AL

While we are all eager to get back to business as soon as possible, the timing of our reopening plans is subject to federal, state and local regulations, so projected reopening dates are subject to change. Reopening plans and policies will adhere to federal, state, and local regulations and guidance, and be informed by industry best practices, which will vary based on location and other circumstances. Last Updated: May 27, 2020 Open Properties with Restrictions Alabama Arizona Arkansas California Riverchase Galleria | Hoover, AL Park Place | Tucson, AZ Pinnacle Hills Promenade | Rogers, AR Chula Vista Center | Chula Vista, CA The Shoppes at Bel Air | Mobile, AL The Mall at Sierra Vista | Sierra Vista, AZ Fig Garden Village | Fresno, CA Tucson Mall | Tucson, AZ Galleria at Tyler | Riverside, CA Mt. Shasta Mall | Redding, CA Otay Ranch Town Center | Chula Vista, CA Promenade Temecula | Temecula, CA The Shoppes at Carlsbad | Carlsbad, CA Valley Plaza Mall | Bakersfield, CA Victoria Gardens | Rancho Cucamonga, CA Colorado Connecticut Florida Georgia Park Meadows | Lone Tree, CO Brass Mill Center | Waterbury, CT Altamonte Mall | Altamonte Springs, FL Augusta Mall | Augusta, GA The Shoppes at Buckland Hills | Manchester, CT Coastland Center | Naples, FL Cumberland Mall | Atlanta, GA The Shops at Somerset Square | Glastonbury, CT Governor's Square | Tallahassee, FL North Point Mall | Alpharetta, GA The SoNo Collection | Norwalk, CT Lakeland Square Mall | Lakeland, FL Oglethorpe Mall | Savannah, GA Mizner Park | Boca Raton, FL Peachtree Mall | -

State Storeno Mall Name Store Type 2015 Sales 2014 Sales Variance

Variance State StoreNo Mall Name Store Type 2015 Sales 2014 Sales Inc/(Dec) % Inc/(Dec) TX 83 NorthPark Center In-Line 1,472,766.00 1,363,984.00 108,782.00 7.98% SC 135 Coastal Grand Mall In-Line 1,151,631.67 1,113,877.31 37,754.36 3.39% TX 20 Barton Creek Square Shopping Center In-Line 1,096,658.41 1,083,499.33 13,159.08 1.21% CA 8 Westfield Valencia Town Center In-Line 1,071,022.26 1,087,795.83 (16,773.57) -1.54% TX 19 Baybrook Mall In-Line 1,025,120.43 1,055,953.79 (30,833.36) -2.92% AZ 125 Park Place Mall In-Line 950,664.23 946,527.12 4,137.11 0.44% TN 48 Wolfchase Galleria In-Line 923,588.32 867,012.22 56,576.10 6.53% TX 55 Stonebriar Centre In-Line 876,800.55 815,558.37 61,242.18 7.51% CA 126 Westfield Galleria at Roseville In-Line 869,168.30 754,757.11 114,411.19 15.16% CO 167 Cherry Creek Shopping Center In-Line 868,959.85 835,887.13 33,072.72 3.96% CO 61 Park Meadows Center In-Line 831,157.07 800,397.91 30,759.16 3.84% AZ 28 Arrowhead Towne Center In-Line 771,406.64 656,746.72 114,659.92 17.46% CA 39 Westfield University Towne Center In-Line 738,949.33 573,464.00 165,485.33 28.86% CA 35 The Promenade at Temecula In-Line 733,268.27 666,557.65 66,710.62 10.01% KY 78 Mall St. -

Brookfield Property REIT Inc. (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (MARK ONE) ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2018 or o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to COMMISSION FILE NUMBER 1-34948 Brookfield Property REIT Inc. (Exact name of registrant as specified in its charter) Delaware 27-2963337 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification Number) 250 Vesey Street, 15th Floor, New York, NY 10281-1023 (Address of principal executive offices) (Zip Code) (212) 417-7000 (Registrant's telephone number, including area code) Securities Registered Pursuant to Section 12(b) of the Act: Title of Each Class A Stock: Name of Each Exchange on Which Registered: Class A Stock, $.01 par value NASDAQ Global Select Market Securities Registered Pursuant to Section 12(g) of the Act: 6.375% Series A Cumulative Redeemable Preferred Stock Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Alderwood Altamonte Mall Apache Mall Augusta Mall Baybrook Mall

Official Rules - New Year Fitness Resolution Sweepstakes NO PURCHASE NECESSARY TO ENTER OR WIN. This promotion is not administered by, sponsored, endorsed, or associated with Facebook or Instagram. This Sweepstakes is solely sponsored by General Growth Services, Inc. (“GGSI” or "Sponsor"), it is a national Sweepstakes marketeD at each of the Participating Malls (“Participating Malls”) referenceD-below. DATES: Enter once between January 15, 2018 3:00 PM CST and February 9, 2018 11:59 PM CST (“Promotional Period”). Limit one entry per person. ENTRY: Visit a Participating Mall’s Facebook (“FB”) page, and look for the Sweepstakes message we post and answer the questions on our timeline. ELIGIBILITY: The Sweepstakes is open to legal residents of the 50 United States or D.C., age 18 or older. Employees and officers of GGSI and their respectiVe parent and subsidiary companies and affiliates are not eligible to enter or win. Immediate family members and household members of such indiViduals are also not eligible to enter or win. "Immediate family members" shall mean parents, step-parents, legal guardians, children, step-children, siblings, step-siblings, or spouses. "Household members" shall mean those people who share the same residence at least three months a year. PRIZE/WINNER SELECTION/ODDS: Winner will be selected in a random drawing. The odds of winning depend on the total number of entries receiVed nationally. One Grand Prize winner to receiVe a $100 GGP Gift Card. CLAIMING PRIZE: Winner will be notified (“Win Notification”) Via FB by the Sponsor and will haVe 4 days after the Win Notification to contact the Sponsor. -

Case 20-13076-BLS Doc 67 Filed 12/07/20 Page 1 of 14

Case 20-13076-BLS Doc 67 Filed 12/07/20 Page 1 of 14 IN THE UNITED STATES BANKRUPTCY COURT FOR THE DISTRICT OF DELAWARE ------------------------------------------------------------ x : In re: : Chapter 11 : Case No. 20-13076 (BLS) FRANCESCA’S HOLDINGS CORPORATION, : et al.,1 : Joint Administration Requested : Debtors. : Re: D.I. 8 ------------------------------------------------------------ x SUPPLEMENTAL DECLARATION OF SHERYL BETANCE IN SUPPORT OF THE DEBTORS’ APPLICATION FOR ENTRY OF AN ORDER AUTHORIZING THE RETENTION AND EMPLOYMENT OF STRETTO AS CLAIMS AND NOTICING AGENT, NUNC PRO TUNC TO THE PETITION DATE Pursuant to 28 U.S.C.§ 1746, I, Sheryl Betance, declare under penalty of perjury that the following is true and correct to the best of my knowledge, information, and belief: 1. I am a Senior Managing Director of Corporate Restructuring at Stretto, a chapter 11 administrative services firm with offices at 410 Exchange, Ste. 100, Irvine, CA 92602. Except as otherwise noted, I have personal knowledge of the matters set forth herein, and if called and sworn as a witness, I could and would testify competently thereto. 2. On December 3, 2020, the Debtors filed the Debtors’ Application for Entry of an Order Authorizing the Retention and Employment of Stretto as Claims and Noticing Agent, Nunc Pro Tunc to the Petition Date [D.I. 8] (the “Application”),2 and the Declaration of Sheryl Betance in Support of the Debtors’ Application for Entry of an Order Authorizing the Retention and 1 The Debtors in these cases, along with the last four digits of each Debtor’s federal tax identification number, are Francesca’s Holdings Corporation (4704), Francesca’s LLC (2500), Francesca’s Collections, Inc. -

Brookfield Properties' Retail Group Overview

Retail Overview Brookfield Properties’ Retail Group Overview We are Great Gathering Places. We embrace our cultural core values of Humility, Attitude, Do The Right Thing, H Together and Own It. HUMILITY Brookfield Properties’ retail group is a company focused A ATTITUDE exclusively on managing, leasing, and redeveloping high- quality retail properties throughout the United States. D DO THE RIGHT THING T TOGETHER O HEADQUARTERS CHICAGO OWN IT RETAIL PROPERTIES 160+ STATES 42 INLINE & FREESTANDING GLA 68 MILLION SQ FT TOTAL RETAIL GLA 145 MILLION SQ FT PROFORMA EQUITY MARKET CAP $20 BILLION PROFORMA ENTERPRISE VALUE $40 BILLION Portfolio Map 2 7 1 4 3 5 3 6 2 1 2 1 1 2 1 3 3 3 1 1 2 4 1 2 1 3 2 1 1 10 4 2 5 1 4 10 2 3 3 1 48 91 6 5 6 2 7 6 4 5 11 7 4 1 1 1 2 2 2 5 7 1 2 1 2 1 1 1 1 6 1 3 5 3 4 15 19 2 14 11 1 1 3 2 1 2 1 1 3 6 2 1 3 4 18 2 17 3 1 2 1 3 2 2 5 3 6 8 2 1 12 9 7 5 1 4 3 1 2 1 2 16 3 4 13 3 1 2 6 1 7 9 1 10 5 4 2 1 4 6 11 5 3 6 2 Portfolio Properties 1 2 3 3 3 1 7 4 Offices 13 12 2 Atlanta, GA 7 3 1 1 Chicago, IL Baltimore, MD 8 5 2 Dallas, TX 4 Los Angeles, CA 6 New York, NY 8 2 9 5 Property Listings by State ALABAMA 7 The Oaks Mall • Gainesville 3 The Mall in Columbia • Columbia (Baltimore) 9 Brookfield Place • Manhattan WASHINGTON 8 Pembroke Lakes Mall • Pembroke Pines 4 Mondawmin Mall • Baltimore 10 Manhattan West • Manhattan 1 Riverchase Galleria • Hoover (Birmingham) 1 Alderwood • Lynnwood (Seattle) 5 Towson Town Center • Towson (Baltimore) 11 Staten Island Mall • Staten Island 2 The Shoppes at Bel Air • Mobile (Fort Lauderdale) -

TURFWAY COMMONS 2, 730 SF - 2,800 SF Retail Space Available Florence, Kentucky Excess Space Also Available

TURFWAY COMMONS 2, 730 SF - 2,800 SF Retail Space Available Florence, Kentucky Excess Space Also Available 1 Northgate Mall LOCATION 2 Tri-County Mall 3 Kenwood Towne Centre 4999 Houston Road | Florence, Kentucky 41042 4 Florence Mall 71 5 Eastgate Mall 275 2 75 1 HIGHLIGHTS 275 3 • 2,730 SF - 2,800 SF Retail Space Available 275 74 71 • Excess Space Also Available 5 • Just off I-75/71 with great visibility and ample parking 471 275 • Anchored by Michael’s Arts & Crafts, Guitar Center and Half Price Books 275 75 • Defy Extreme Air Sports “COMING SOON” 71 SITE 4 • Shadow anchored by Sam’s Club • Major retailers in the market include Walmart Supercenter, Kohl’s, Best Buy, Dick’s Sporting Goods, Target, PetSmart, Christmas Tree Shops, At Home, DEMOGRAPHICS Home Depot, Lowe’s, and Meijer • Population of 146,198 in 5 miles with AHI of $84,050 2019 Estimate 1 Mile 3 Miles 5 Miles Population 2,961 58,536 146,198 Households 1,204 24,354 57,908 TRAFFIC COUNTS Average HH Income $54,582 $67,053 $84,050 Daytime Employees 10,587 48,869 94,971 Turfway Road: 15,485 VPD I-71/75: 176,192 VPD CONTACT ANCHOR ASSOCIATES Owned and Managed by: Marianne Holewski • [email protected] 3825 Edwards Road, Suite 630 Cincinnati, OH 45209 Amy Holter • [email protected] 513.784.1106 Office Phone • 513.784.1106 Website • www.anchor-associates.com Florence, Kentucky Florence, COMMONS TURFWAY Unit # Suite Sq. Ft. Tenant 1 4951 2,100 GameStop 2 4971 1,820 Mariner Financial 3 4975 2,730 AVAILABLE 4 4979 1,330 UV Spa Nails 5 4981 4,570 CiCi's Pizza 6 4987 1,400 Wild Birds Unlimited 7 4989 2,800 AVAILABLE 8 4995/A 1,050 America's Best Contacts & Eyeglasses 9 4995/B 2,800 America's Best Contacts & Eyeglasses 10 4997 1,400 Advance-U-Cash 11 4999/100 33,148 Defy Extreme Air Sports 12 4999/200 24,000 Michaels 13 4999/300 15,087 Guitar Center 14 4999/400 11,236 Half Price Books 19,600 SF 16,000 SF 12 11 13 14 67891 0 9 8 7 7 56 4 3 12 The information herein is not guaranteed. -

Alabama Arizona Arkansas California Riverchase Galleria

While we are all eager to get back to business as soon as possible, the timing of our reopening plans is subject to federal, state and local regulations, so projected reopening dates are subject to change. Reopening plans and policies will adhere to federal, state, and local regulations and guidance, and be informed by industry best practices, which will vary based on location and other circumstances. Last Updated: July 20, 2020 Open Properties with Restrictions Alabama Arizona Arkansas California Riverchase Galleria | Hoover, AL Park Place | Tucson, AZ Pinnacle Hills Promenade | Rogers, AR Bayshore Mall | Eureka, CA The Shoppes at Bel Air | Mobile, AL The Mall at Sierra Vista | Sierra Vista, AZ Chula Vista Center | Chula Vista, CA Tucson Mall | Tucson, AZ Fig Garden Village | Fresno, CA Mt. Shasta Mall | Redding, CA Otay Ranch Town Center | Chula Vista, CA Valley Plaza Mall | Bakersfield, CA Victoria Gardens | Rancho Cucamonga, CA Colorado Connecticut Delaware Florida Park Meadows | Lone Tree, CO Brass Mill Center | Waterbury, CT Christiana Mall | Newark, DE Altamonte Mall | Altamonte Springs, FL Southwest Plaza | Littleton, CO The Shoppes at Buckland Hills | Manchester, CT Coastland Center | Naples, FL The Shops at Somerset Square | Glastonbury, CT Governor's Square | Tallahassee, FL The SoNo Collection | Norwalk, CT Lakeland Square Mall | Lakeland, FL Mizner Park | Boca Raton, FL The Oaks Mall | Gainesville, FL Pembroke Lakes Mall | Pembroke Pines, FL Shops at Merrick Park | Coral Gables, FL Georgia Hawaii Idaho Illinois Augusta Mall -

2Q17 Columbia Retail Market Report

2Q17: Columbia Retail Market Report Grocers In, Big Box Retailers Out VACANCY The Columbia retail market stayed steady between the close of 2016 and the close of the second quarter, with vacancy 5.3% creeping from 5.1% to 5.3%. Net absorption this quarter Rates crept upwards from 5.1% in 4Q16 was negative 18,174 square feet (SF), compared to a positive 306,581 SF at the close of the fourth quarter 2016. NAI Avant Director of Retail Services Patrick Palmer, CCIM attributes the negative net absorption to big box retailers NET ABSORPTION closing their doors, making more vacant space available in the market. For example, this quarter, HH Gregg closed its doors -18,174 SF and moved out of ±30,396 SF at Village at Sandhill Forum 306,581 SF in 4Q16 Center, in addition to vacating the chain’s ±69,023 SF location on Bower Parkway. But the Columbia retail market remains steady and strong. Average rental rates rose from $11.06 SF at the close of 2016, AVERAGE RENTAL RATE to $11.42 SF at the close of the second quarter 2017. The Central Business District continues to own the highest rental $11.42 rate at $19.38 SF. Up from $11.06 in 4Q16 The highlights for the Columbia retail market in the second quarter of 2017 center around major grocery store openings and announcements. VACANCY: MALLS Impact of E-Commerce: Columbia is no exception to the nationwide 13.6% reality of big box retailers closing their doors. The only building type that saw Nearly every major department store, including decreased vacancy in 2Q17 Macy’s, Kohl’s, Walmart, and Sears, have closed hundreds of stores due to the rise of e-commerce. -

State Store Hours State Store Hours Al Brookwood

ALL HOURS APPLY TO LOCAL TIME ZONES STATE STORE HOURS STATE STORE HOURS AL BROOKWOOD VILLAGE 5-9pm MO NORTHPARK (MO) 5-9pm AL RIVERCHASE GALLERIA 5-9pm MO THE SHOPPES AT STADIUM (MO) 5-9pm AZ SCOTTSDALE FASHION SQUARE 5-9pm MT BOZEMAN GALLATIN VALLEY (MT) 5-9pm AZ BILTMORE FASHION PARK 5-9pm MT HELENA NORTHSIDE CENTER (MT) 5-9pm AZ ARROWHEAD TOWNE CENTER 5-9pm NC CRABTREE VALLEY 5-9pm AZ CHANDLER FASHION CENTER 5-9pm NC STREETS AT SOUTHPOINT 5-9pm AZ PARADISE VALLEY (AZ) 5-9pm NC CROSS CREEK (NC) 5-9pm AZ TUCSON MALL 5-9pm NC FRIENDLY CENTER 5-9pm AZ TUCSON PARK PLACE 5-9pm NC NORTHLAKE (NC) 5-9pm AZ SANTAN VILLAGE 5-9pm NC SOUTHPARK (NC) 5-9pm CA CONCORD 5-9:30pm NC TRIANGLE TOWN CENTER 5-9pm CA CONCORD SUNVALLEY 5-9pm NC CAROLINA PLACE (NC) 5-9pm CA WALNUT CREEK BROADWAY PLAZA 5-9pm NC HANES 5-9pm CA SANTA ROSA PLAZA 5-9pm NC WENDOVER 5-9pm CA FAIRFIELD SOLANO 5-9pm ND WEST ACRES (ND) 5-9pm CA NORTHGATE (CA) 5-9pm ND COLUMBIA (ND) 5-9pm CA PLEASANTON STONERIDGE 5-9pm NH MALL OF NEW HAMPSHIRE 5-9:30pm CA MODESTO VINTAGE FAIR 5-9pm NH BEDFORD (NH) 5-9pm CA NEWPARK 5-9pm NH MALL AT ROCKINGHAM PARK 5-9:30pm CA STOCKTON SHERWOOD 5-9pm NH FOX RUN (NH) 5-9pm CA FRESNO FASHION FAIR 5-9pm NH PHEASANT LANE (NH) 5-9:30pm CA SHOPS AT RIVER PARK 5-9pm NJ MENLO PARK 5-9:30pm CA SACRAMENTO DOWNTOWN PLAZA 5-9pm NJ WOODBRIDGE CENTER 5-9:30pm CA ROSEVILLE GALLERIA 5-9pm NJ FREEHOLD RACEWAY 5-9:30pm CA SUNRISE (CA) 5-9pm NJ MONMOUTH 5-9:30pm CA REDDING MT. -

Alabama Arizona Arkansas California Riverchase Galleria | Hoover

While we are all eager to get back to business as soon as possible, the timing of our reopening plans is subject to federal, state and local regulations, so projected reopening dates are subject to change. Reopening plans and policies will adhere to federal, state, and local regulations and guidance, and be informed by industry best practices, which will vary based on location and other circumstances. Last Updated: May 21, 2020 Open Properties with Restrictions Alabama Arizona Arkansas California Riverchase Galleria | Hoover, AL Park Place | Tucson, AZ Pinnacle Hills Promenade | Rogers, AR Chula Vista Center | Chula Vista, CA The Shoppes at Bel Air | Mobile, AL The Mall at Sierra Vista | Sierra Vista, AZ Fig Garden Village | Fresno, CA Tucson Mall | Tucson, AZ Mt. Shasta Mall | Redding, CA Otay Ranch Town Center | Chula Vista, CA Victoria Gardens | Rancho Cucamonga, CA Connecticut Florida Georgia Hawaii Brass Mill Center | Waterbury, CT Altamonte Mall | Altamonte Springs, FL Augusta Mall | Augusta, GA Ala Moana Center | Honolulu, HI The Shoppes at Buckland Hills | Manchester, CT Coastland Center | Naples, FL Cumberland Mall | Atlanta, GA Prince Kuhio Plaza | Hilo, HI The Shops at Somerset Square | Glastonbury, CT Governor's Square | Tallahassee, FL North Point Mall | Alpharetta, GA Whalers Village | Lahaina, HI The SoNo Collection | Norwalk, CT Lakeland Square Mall | Lakeland, FL Oglethorpe Mall | Savannah, GA Mizner Park | Boca Raton, FL Peachtree Mall | Columbua, GA The Oaks Mall | Gainesville, FL Perimeter Mall | Atlanta, GA Pembroke Lakes Mall | Pembroke Pines, FL Shoppes at River Crossing | Macon, GA Shops at Merrick Park | Coral Gables, FL Idaho Indiana Iowa Kentucky Boise Towne Square | Boise, ID Glenbrook Square | Fort Wayne, IN Coral Ridge Mall | Coralville, IA Florence Mall | Florence, KY Grand Teton Mall | Idaho Falls, ID Jordan Creek Town Center | West Des Moines, IA Greenwood Mall | Bowling Green, KY Silver Lake Mall | Coeur d'Alene, ID Mall St.