United States Securities and Exchange Commission Washington, D.C

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

View Annual Report

C O N T E N T S 1 Five Year Summary 2 Management’s Discussion and Analysis 10 Management’s Responsibility for Financial Statements 10 Report of Independent Accountants 11 Consolidated Statement of Operations 12 Consolidated Balance Sheet 13 Consolidated Statement of Cash Flows 14 Consolidated Statement of Changes in Shareowners’ Equity 15 Notes to Consolidated Financial Statements 27 Directors 28 Leadership 29 Shareowner Information Fiv e Year S U M M A R Y IN MILLIONS OF DOLLARS, EXCEPT PER SHARE AND EMPLOYEE AMOUNTS 1999 1998 1997 1996 1995 For the year Revenues $ 24,127 $ 22,809 $ 21,288 $ 19,872 $ 19,418 Research and development 1,292 1,168 1,069 1,014 865 Income from continuing operations 841 1,157 962 788 651 Net income 1,531 1,255 1,072 906 750 Earnings per share: Basic: Continuing operations 1.74 2.47 1.98 1.57 1.27 Net earnings 3.22 2.68 2.22 1.81 1.47 Diluted: Continuing operations 1.65 2.33 1.89 1.51 1.24 Net earnings 3.01 2.53 2.10 1.74 1.43 Cash dividends per common share .76 .695 .62 .55 .5125 Average number of shares of Common Stock outstanding: Basic 465.6 455.5 468.9 482.9 491.3 Diluted 506.7 494.8 507.1 517.2 519.0 Return on average common shareowners’ equity, after tax 24.6% 28.6% 24.5% 21.1% 18.6% At year end Working capital, excluding net investment in discontinued operation $ 1,412 $ 1,359 $ 1,712 $ 2,168 $ 2,065 Total assets 24,366 17,768 15,697 15,566 14,819 Long-term debt, including current portion 3,419 1,669 1,389 1,506 1,713 Total debt 4,321 2,173 1,567 1,709 1,975 Debt to total capitalization 38% 33% 28% 28% 33% Net debt (total debt less cash) 3,364 1,623 912 711 1,229 Net debt to total capitalization 32% 27% 18% 14% 23% ESOP Preferred Stock, net 449 456 450 434 398 Shareowners’ equity 7,117 4,378 4,073 4,306 4,021 Number of employees - continuing operations 148,300 134,400 130,400 123,800 119,800 UNITED TECHNOLOGIES 1 M A N A G E M E N T ’ S Discussion and Analysis Management’s Discussion and Analysis of Results of impact service and maintenance margins on installed elevators and Operations and Financial Position escalators. -

United States District Court District of Connecticut

Case 3:20-cv-01171 Document 1 Filed 08/12/20 Page 1 of 54 UNITED STATES DISTRICT COURT DISTRICT OF CONNECTICUT Geraud Darnis, David Hess, Michael Maurer, Richard Sanfrey, Civil Action No.: 3:20-cv-1171 Dino DePellegrini, Bradley Hardesty, Roy Dion, Alan Machuga, Theresa MacKinnon, Christopher Doot, David Carter and Costas Loukellis, on behalf of themselves and all others similarly situated, Plaintiffs, vs. CLASS ACTION COMPLAINT Raytheon Technologies Corporation, Carrier Global Corporation, Otis Worldwide Corporation, United Technologies Corporation Long-Term Incentive Plan, United Technologies Corporation 2018 Long-Term Incentive Compensation Plan, Carrier Global Corporation 2020 Long-Term Incentive Plan, Otis Worldwide Corporation 2020 Long-Term Incentive Plan, United Technologies Corporation Savings Restoration Plan, Carrier Global Corporation Savings Restoration Plan, Otis Worldwide Savings Restoration Plan, United Technologies Company Performance Share Unit Deferral Plan, Carrier Global Corporation LTIP Performance Share Unit Deferral Plan, Otis Worldwide Corporation LTIP Performance Share Unit Deferral Plan, United Technologies Company Deferred Compensation Plan, Carrier Global Corporation Deferred Compensation Plan, Otis Worldwide Corporation Deferred Compensation Plan, UTC Company Automatic Contribution Excess Plan, Carrier Global Corporation Company Automatic Contribution Excess Plan, Otis Worldwide Corporation Company Automatic Contribution Excess Plan, Lloyd J. Austin, III, Diane M. Bryant, John V. Faraci, Jean-Pierre Garnier, Gregory J. Hayes, Christopher J. Kearney, Ellen J. Kullman, Marshall O. Larsen, Harold McGraw, III, Robert K. Ortberg, Margaret L. O’Sullivan, Denise L. Ramos, Frederic G. Reynolds, Brian C. Rogers, David Gitlin, John J. Greisch, Charles M. Holley, Jr., Michael M. McNamara, Michael A. Todman, Virginia M. Wilson, Jeffrey H. Black, Kathy Hopinkah, Shailesh G. -

Annual Meeting of Shareowners and Proxy Statement We Offer Our Customers the Most Cutting-Edge, Sustainable Technologies

Notice of 2020 Annual Meeting of Shareowners and Proxy Statement We offer our customers the most cutting-edge, sustainable technologies. Carrier’s Infinity Controls, Carrier Transicold & Refrigeration combined with its energy-efficient Systems’ cold-chain solutions geothermal solutions, earn the are used in the preservation of food Energy Star “Most Efficient” from origin to point of sale, helping rating for geothermal products to reduce global food waste and its and are 45% more energy impact on the environment. efficient than standard heating and cooling systems. Otis’ Gen2 Switch elevator uses less electricity than most household appliances. If the power fails, the Gen2 Switch elevator continues to operate off of battery power. It also can operate on wind and solar power. Since entering into service in early Collins Aerospace’s DURACARB 2016, Pratt & Whitney’s Geared carbon brakes are providing Turbofan (“GTF”) engine customers with weight savings, and has demonstrated its ability to thereby fuel savings, and have about reduce fuel burn by 16%, reduce a 35% advantage in brake life over NOx emissions by 50% to the competing manufacturers’ material. regulatory standard and the noise footprint by 75%. Marioff’s HI-FOG water mist systems use up to 90% less water than traditional sprinkler systems. March 13, 2020 Notice of 2020 Annual Meeting of Shareowners Meeting Information DATE AND TIME: LOCATION: Your vote is very important. April 27, 2020 Ritz-Carlton Tysons Corner Please submit your proxy or 8:00 a.m. Eastern Time 1700 Tysons Boulevard voting instructions (doors open at 7:30 a.m.) McLean, VA 22102 as soon as possible. -

2020 Annual Report Swanzey, New Hampshire

2020 Annual Report Swanzey, New Hampshire Celebrating the 100th year anniversary of the 19th amendment with Women of Swanzey Contact and Meeting Information www.swanzeynh.gov Town Hall Contact Information Regular Monthly Meetings 620 Old Homestead Highway Consult the Town calendar at PO Box 10009 www.swanzeynh.gov for the most up-to-date Swanzey, New Hampshire 03446-0009 meeting information. (603) 352-7411 Board of Selectmen (603) 352-6250 (fax) Wednesday Evenings, 5:30 p.m. NH Relay TDD 1(800) 735-2964 Kenneth P. Colby Jr: 357-3499 (home) Sylvester Karasinski: 209-1776 (cell) x101 Deputy Town Clerk Bill Hutwelker: 313-3948 (cell) x102 Town Clerk x104 Sewer Commission Assistant Planning Board x105 Code Enforcement Officer 2nd & 4th Thursday, 6 p.m. x106 Finance Office Assistant x107 Town Administrator Zoning Board of Adjustment x108 Director of Planning & Economic 3rd Monday (Except Jan & Feb), 7 p.m. Development x109 Deputy Tax Collector Conservation Commission x110 Human Services Coordinator 1st Monday, 4 p.m. x111 Finance Director x112 Tax Collector/Bookkeeper Sewer Commission x114 Assessing Coordinator 1st & 3rd Wednesday, 4:30 p.m. x115 Administrative Assistant General Inquiries Economic Dev. Advisory Committee 2nd Monday, 5 p.m. Town Hall Hours Monday 9:30 a.m. to 6:00 p.m. Recreation Advisory Committee Tuesday - Thursday 8:30 a.m. to 5:00 p.m. Consult calendar Friday 7:30 a.m. to 4:00 p.m. Old Home Day Committee Emergency 911 Consult Calendar Police Department: 352-2869 Fire Department: 358-6455 Rail Trail Advisory Committee Emergency -

Otis Elevator Company (India) Limited 92, KIADB Industrial Estate Phase II, Auditors Jigani Industrial Area Anekal Taluk, Bengaluru - 560 105 M/S

CORPORATE INFORMATION Registered Ofce & Head Ofce Bankers 9th Floor, Magnus Towers, Citibank N. A. Mindspace, Link Road, Malad (West), Standard Chartered Bank Mumbai - 400 064 Maharashtra Deutsche Bank Tel: 91-22-2844 9700/ 66795151 Fax: 91-22-2844 9791 HDFC Bank Limited CIN: U29150MH1953PLC009158 Canara Bank www.otis.com Bank of America Manufacturing Facility State Bank of India Otis Elevator Company (India) Limited 92, KIADB Industrial Estate Phase II, Auditors Jigani Industrial Area Anekal Taluk, Bengaluru - 560 105 M/s. BSR & Co. LLP Chartered Accountants National Service Centre 'Sai Dhara', Block D2, Warehouse No. 3 & 4, Mumbai-Nashik Highway (NH3), Opp. R.K Petrol Pump, Cost Auditors Next to Shangrila Resort, Kuksha Village, M/s. Kishore Bhatia & Associates Bhiwandi - 421 302 Cost Accountants Dist: Thane. Regional Ofces 9th Floor, Magnus Towers, Mindspace, Link Road, Secretarial Auditors Malad (West), M/s. JSP Associates Mumbai - 400 064 Company Secretary Maharashtra Otis Elevator Company (India) Limited Victoria Park, Level 2, Block: GN, Plot no. 37/2, Sector V, Salt Lake, Kolkata - 700 091 Registrar & Share Transfer Agents st Unit Nos. 171, 172, 173 on 1 Floor, Link Intime India Pvt Ltd. nd Unit Nos. 271 and 272 on 2 Floor, C 101, 247 Park, L.B.S Marg, Aggarwal Cyber Plaza - II, Vikhroli (West), Plot No C-7, Netaji Subhash Place, Mumbai – 400 083, Maharashtra Pitampura, Delhi - 110 034 Tel.: 91-22-49186270 Otis House, MK Towers, Fax: 91-22-49186060 #27, Langford Road, Shanti Nagar, Bengaluru - 560 027 Email: [email protected] Website: www.linkintime.co.in BOARD OF DIRECTORS CONTENTS Sebi Joseph - Managing Director P. -

Otis Worldwide Cover

IPOX® PORTFOLIO HOLDING ANALYSIS 02/03/2021 To learn more, visit www.ipox.com; OTIS WORLDWIDE CORPORATION (OTIS US) Email: [email protected] Office: +1 (312) 526-3634 COMPANY DESCRIPTION Support +1 (312) 339-4114 Founded in 1853, Otis Worldwide Corporation is the world’s leading elevator and escalator manufacturing, installation and service company. Otis was acquired by United Technologies (UTC) in 1976 and was subsequently spun off in 2020 after UTC merged with Raytheon Technologies (RTX). The Farmington, CT-based company designs, manufactures, sells and installs a wide range of passenger and freight elevators, as well as escalators and moving walkways. Otis also provides maintenance, repair and modernization/upgrade services for elevators and escalators. BUSINESS MODEL Otis Worldwide generates revenue from product sales (44%) and service sales (56%). SPIN-OFF HISTORY United Technologies (now Raytheon Technologies) announced its intention to spin-off Otis in 11/26/2018. On 4/3/2020, Otis began trading as a separate public company on the NYSE through a pro-rata distribution of 0.5 shares of Otis common stock for every share of UTC common stock held at the close of business on the record date (3/19/2020). The shares opened at $43.75/share and closed the first day higher at $47.32 (▲8.16%). Otis Worldwide was included in the IPOX® 100 U.S. Portfolio (ETF: FPX) on 5/7/2020 and currently weighs ca. 0.97% of the portfolio. *Otis originally listed its common stock on the NYSE in April 1920. HISTORICAL PERFORMANCE 120% $75 Otis Worldwide IPOX® 100 U.S. -

UTC Board of Directors Approves Separation of Otis

UTC Board of Directors approves separation of Otis March 11, 2020 "When-issued" trading expected to begin on March 18, 2020 Record date for distribution of Carrier and Otis shares will be March 19, 2020 Distribution date for Carrier and Otis shares anticipated to be April 3, 2020 FARMINGTON, Conn., March 11, 2020 /PRNewswire/ -- United Technologies Corp. (NYSE: UTX) announced today that its Board of Directors approved the previously announced separations of Carrier and Otis. To effect the separations, the UTC Board of Directors declared a pro rata dividend of Carrier Global Corporation (NYSE: CARR) common stock and Otis Worldwide Corporation (NYSE: OTIS) common stock to be made effective at 12:01 a.m. EDT on April 3, 2020 to UTC's shareowners of record as of 5:00 p.m. EDT on March 19, 2020, the record date for the distribution. Each UTC shareowner will receive one (1) share of Carrier common stock and one-half (0.5) share of Otis common stock for every one (1) share of UTC common stock held on the record date. No fractional shares of Carrier or Otis will be issued in the distribution, and instead UTC shareowners will receive cash in lieu of any fractional shares. UTC shareowners will retain their shares of UTC common stock. It is expected that both Carrier and Otis will commence equity roadshows on or around mid-March 2020. Carrier's investor presentation will be available at www.Corporate.Carrier.com and Otis' investor presentation will be available at www.otis.com prior to the roadshows. Each distribution remains subject to certain conditions described in Carrier's and Otis' respective Registration Statements on Forms 10, as amended, including the Forms 10 having been declared effective by the U.S. -

OTIS WORLDWIDE CORPORATION (Exact Name of Registrant As Specified in Its Charter) ______

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 ____________________________________ FORM 10-Q ____________________________________ ☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended March 31, 2021 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission file number 001-39221 ____________________________________ OTIS WORLDWIDE CORPORATION (Exact name of registrant as specified in its charter) ____________________________________ Delaware 83-3789412 (State or other jurisdiction of incorporation) (I.R.S. Employer Identification No.) One Carrier Place, Farmington, Connecticut 06032 (Address of principal executive offices, including zip code) (860) 233-6847 (Registrant's telephone number, including area code) ____________________________________ Securities registered pursuant to Section 12(b) of the Act: Name of each exchange Title of each class Trading Symbol(s) on which registered Common Stock ($0.01 par value) OTIS New York Stock Exchange Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒. No ☐. Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). -

Industry Development Opportunities from Developing Concentrating Solar Thermal Power in Australia

Industry Development Opportunities from developing Concentrating Solar Thermal Power in Australia Authors: Giselle Rampersad and John Spoehr Research program for Australian Renewable Energy Agency (ARENA) Australian Industrial Transformation Institute April 27, 2018 Industry Development Opportunities from developing Concentrating Solar Thermal Power in Australia Australian Industrial Transformation Institute College of Business, Government and Law Flinders University of South Australia 1284 South Road Tonsley South Australia 5042 www.flinders.edu.au/aiti URL:http://www.flinders.edu.au/aiti/ CAT: AITI201801 Suggested citation: Giselle Rampersad and John Spoehr. 2018. Industry Development Opportunities from developing Concentrating Solar Thermal Power in Australia. Adelaide: Australian Industrial Transformation Institute, Flinders University of South Australia. The Australian Industrial Transformation Institute (AITI) has taken care to ensure the material presented in this report is accurate and correct. However, AITI does not guarantee and accepts no legal liability or responsibility connected to the use or interpretation of data or material contained in this report. Contents EXECUTIVE SUMMARY ................................................................................................................................ 1 ACKNOWLEDGEMENTS ............................................................................................................................... 2 ABBREVIATIONS ......................................................................................................................................... -

Financial Results

OTIS WORLDWIDE CORPORATION ANNUAL REPORT 2020 Financial results Financial results 20 Five-Year Summary 21 Management’s Discussion and Analysis of Financial Condition and Results of Operations 42 Cautionary Note Concerning Factors That May Affect Future Results 44 Management’s Report on Internal Control over Financial Reporting 45 Report of Independent Registered Public Accounting Firm 48 Consolidated Statements of Operations 49 Consolidated Statements of Comprehensive Income 50 Consolidated Balance Sheets 51 Consolidated Statements of Changes in Equity 52 Consolidated Statements of Cash Flows 53 Notes to Consolidated Financial Statements 100 Selected Quarterly Financial Data 101 Performance Graph 102 GAAP to Non-GAAP Reconciliations 19 OTIS WORLDWIDE CORPORATION ANNUAL REPORT 2020 Five-Year Summary (dollars in millions, except per share amounts; 2016 shares in millions) 2020 2019 2018 2017 (unaudited) For The Year Net sales $ 12,756 $ 13,118 $ 12,915 $ 12,323 $ 11,886 Net income1 1,056 1,267 1,210 809 1,397 Net income attributable to common shareholders1 906 1,116 1,049 636 1,197 Basic earnings per share—Net income attributable to common shareholders2 2.09 2.58 2.42 1.47 2.76 Diluted earnings per share—Net income attributable to common shareholders2 2.08 2.58 2.42 1.47 2.76 Cash dividends per common share 0.60 — — — — At December 31, Total assets 3 $ 10,710 $ 9,687 $ 9,135 $ 9,089 $ 8,584 Total debt4 5,963 39 28 18 18 1 2020 amounts include the impact of interest expense on debt, incremental standalone public company costs and non-recurring Separation- related costs. -

Rtx, Carr & Otis

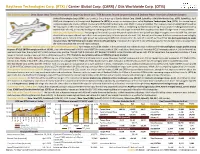

Raytheon Technologies Corp. (RTX) / Carrier Global Corp. (CARR) / Otis Worldwide Corp. (OTIS) The Edge Intelligence: Data Shows Ideal Time to Participate in Large-Cap Break-Ups / RTX Becomes Second-Largest Aviation & Defense Player Post-Spin of Industry Leaders United Technologies Corp. (UTX) is performing a 3-way break-up of Carrier Global Corp. (CARR, Spinoff) and Otis Worldwide Corp. (OTIS, Spinoff) by April 2020 and subsequently will merge with Raytheon Co. (RTN) to create an aerospace giant called Raytheon Technologies Corp. (RTX), the second largest aviation company by revenue (FY21E revenue of $78.7bn) behind Boeing Co. (BA, FY21E revenue of $113bn). The respective Spinoffs (CARR & OTIS) will be the top players in their respective spaces. Of the two Spinoff entities, OTIS is a compelling investment considering it has a market leading position (with a market share of 17%), an industry leading EBITDA margin profile (15.9%) and longer-term cash flow visibility on the back of longer-term service contracts. What Does the Spinoff Data Say? Analyzing tax-free break-ups over the past 10 years where the Spinoff was large enough to enter the S&P 500, we have identified these types of break-ups in the US are very rare (only 23 break-ups out of a total 194). Not only are they rare, but these investments can be highly profitable when entered at the right period. By examining all different periods in the life cycle of a Spinoff, we found that the best opportunity to make money in these S&P 500 listed Spins is after three months of trading. -

Raytheon Technologies Reports First Quarter 2021 Results; Sales, Adjusted EPS and Free Cash Flow Exceeded Expectations

Exhibit 99 Media Contact 860.493.4364 Investor Contact 781.522.5123 Raytheon Technologies Reports First Quarter 2021 Results; Sales, Adjusted EPS and Free Cash Flow Exceeded Expectations Raises low end of full year sales and adjusted EPS outlook; Increases share repurchase plan to at least $2 billion of shares in 2021; Increases gross merger synergies to $1.3 billion First quarter 2021 • Sales of $15.3 billion • GAAP EPS from continuing operations of $0.51, which included $0.39 of net significant and/or non- recurring charges and acquisition accounting adjustments • Adjusted EPS of $0.90 • Operating cash flow from continuing operations of $723 million; Free cash flow of $336 million • Achieved approximately $200 million of RTX synergies • Resumed share repurchase program, and repurchased $375 million of shares • Closed on the divestiture of Forcepoint for gross proceeds of $1.1 billion Raytheon Technologies updates its 2021 outlook and now anticipates the following: Outlook for full year 2021 • Sales of $63.9 - $65.4 billion, up from $63.4 - $65.4 billion • Adjusted EPS of $3.50 - $3.70, up from $3.40 - $3.70 • Share repurchases of at least $2 billion, up from $1.5 billion • Confirms free cash flow outlook of approximately $4.5 billion WALTHAM, Mass., April 27, 2021 – Raytheon Technologies Corporation (NYSE: RTX) reported first quarter 2021 results. “Raytheon Technologies delivered strong first quarter results with sales, adjusted EPS and free cash flow that were above our initial expectations, giving us the confidence to increase the low end of our sales and adjusted EPS outlook,” said Raytheon Technologies CEO Greg Hayes.