JP Yearbook 2020.Indd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Outdoor Club Japan (OCJ) 国際 アウトドア・クラブ・ジャパン Events

Outdoor Club Japan (OCJ) 国際 アウトドア・クラブ・ジャパン Events Norikuradake Super Downhill 10 March Friday to 12 March Monday If you are not satisfied ski & snowboard in ski area. You can skiing from summit. Norikuradake(3026m)is one of hundred best mountain in Japan. This time is good condition of backcountry ski season. Go up to the summit of Norikuradake by walk from the top of last lift(2000m). Climb about 5 hours and down to bottom lift(1500m) about 50 min. (Deta of last time) Transport: Train from Shinjuku to Matsumoto and Taxi from Matsumoto to Norikura-kogen. Return : Bus from Norikura-kogen to Sinshimashima and train to Shinjuku. Meeting Time & Place : 19:30 Shijuku st. platform 5 car no.1 for super Azusa15 Cost : About Yen30000 Train Shinjuku to matsumoto Yen6200(ow) but should buy 4coupon ticket each coupon Yen4190 or You can buy discount ticket shop in town price is similar. (price is non-reserve seat) Taxi about Yen13000 we will share. Return bus Yen1300 and local train Yen680. Inn Yen14000+tax 2 overnight 2 breakfast 1 dinner (no dinner Friday) Japanese room and hot spring! Necessary equipment : Skiers & Telemarkers need a nylon mohair skin. Snowboarders need snowshoes. Crampons(over 8point!) Clothes: Gore-tex jacket and pants, fleece, hut, musk, gloves, sunglasses, headlamp, thermos, lunch, sunscreen If you do not go up to the summit, you can enjoy the ski area and hot springs. 1 day lift pass Yen4000 Limit : 12persons (priority is downhill from summit) In Japanese : 026m)の頂上からの滑降です。 ゲレンデスキーに物足りないスキーヤー、スノーボーダー向き。 山スキーにいいシーズンですが、天気次第なので一応土、日と2日間の時間をとりました。 -

Symbol of Peace and Restoration Statue of “Kanaderu Otome” (A Girl Playing Guitar)

Community Information Paper Vol.33 December 2015 Issued by Azabu Regional City Office Edited by The Azabu Editing Office 5-16-45 Roppongi, Minato City, Tokyo 106-8515 Tel: 03-5114-8812 Fax: 03-3583-3782 Please contact Minato Call (City Information Service) for inquiries regarding Residents’ Life Support. Tel: 03-5472-3710 A community information paper created and edited by Azabu residents Fascinated by Artistic Azabu ⑦ Symbol of Peace and Restoration Statue of “Kanaderu Otome” (A Girl Playing Guitar) Shin Hongo (1905 – 1980) He was a leading sculptor of representational sculptures in Japan after the war, and a pio- neer of monumental statues and field sculp- tures. He was born and grew up in Sapporo. After graduating from the Craftworks and Sculpture Division, the Craft and Design De- partment of Koto Kogei Gakkou (tertiary insti- tution for crafts, presently the Department of Technology in Chiba University) in 1928, he studied under the great sculptor Kotaro Taka- mura. His representative works include a sculpture of a group of students who died in the war called “Kike Wadatsumi no Koe” (1950), the sculpture “Arashi no naka no Boshizo” (Mother and Child in a Storm) (1953), and more. (Pictures provided by Hongo Shin Memorial Museum of Sculpture, Sapporo) The coffee shop “Almond”, a famous都営地下鉄大江戸線 meeting 麻布十番駅 spot on a corner of the Roppongi Cross- ing, opened in 1964. Since 1954, 10 years before Almond was established, a statue of a 麻布十番大通り girl playing guitar has stood at the side of the crossing.東 京 メ トImmediately ロ 南 北 線 after the war, this Bronze Statue “Kanaderu Otome” by Shin Hongo statue, called “Kanaderu Otome,”きみちゃん像 was sculpted by Shin Hongo as a symbol of peace パ テ ィ オ 通 り パティオ and restoration. -

List of Certified Facilities (Cooking)

List of certified facilities (Cooking) Prefectures Name of Facility Category Municipalities name Location name Kasumigaseki restaurant Tokyo Chiyoda-ku Second floor,Tokyo-club Building,3-2-6,Kasumigaseki,Chiyoda-ku Second floor,Sakura terrace,Iidabashi Grand Bloom,2-10- ALOHA TABLE iidabashi restaurant Tokyo Chiyoda-ku 2,Fujimi,Chiyoda-ku The Peninsula Tokyo hotel Tokyo Chiyoda-ku 1-8-1 Yurakucho, Chiyoda-ku banquet kitchen The Peninsula Tokyo hotel Tokyo Chiyoda-ku 24th floor, The Peninsula Tokyo,1-8-1 Yurakucho, Chiyoda-ku Peter The Peninsula Tokyo hotel Tokyo Chiyoda-ku Boutique & Café First basement, The Peninsula Tokyo,1-8-1 Yurakucho, Chiyoda-ku The Peninsula Tokyo hotel Tokyo Chiyoda-ku Second floor, The Peninsula Tokyo,1-8-1 Yurakucho, Chiyoda-ku Hei Fung Terrace The Peninsula Tokyo hotel Tokyo Chiyoda-ku First floor, The Peninsula Tokyo,1-8-1 Yurakucho, Chiyoda-ku The Lobby 1-1-1,Uchisaiwai-cho,Chiyoda-ku TORAYA Imperial Hotel Store restaurant Tokyo Chiyoda-ku (Imperial Hotel of Tokyo,Main Building,Basement floor) mihashi First basement, First Avenu Tokyo Station,1-9-1 marunouchi, restaurant Tokyo Chiyoda-ku (First Avenu Tokyo Station Store) Chiyoda-ku PALACE HOTEL TOKYO(Hot hotel Tokyo Chiyoda-ku 1-1-1 Marunouchi, Chiyoda-ku Kitchen,Cold Kitchen) PALACE HOTEL TOKYO(Preparation) hotel Tokyo Chiyoda-ku 1-1-1 Marunouchi, Chiyoda-ku LE PORC DE VERSAILLES restaurant Tokyo Chiyoda-ku First~3rd floor, Florence Kudan, 1-2-7, Kudankita, Chiyoda-ku Kudanshita 8th floor, Yodobashi Akiba Building, 1-1, Kanda-hanaoka-cho, Grand Breton Café -

A 5 Day Tokyo Itinerary

What To Do In Tokyo - A 5 Day Tokyo Itinerary by NERD NOMADS NerdNomads.com Tokyo has been on our bucket list for many years, and when we nally booked tickets to Japan we planned to stay ve days in Tokyo thinking this would be more than enough. But we fell head over heels in love with this metropolitan city, and ended up spending weeks exploring this strange and fascinating place! Tokyo has it all – all sorts of excellent and corky museums, grand temples, atmospheric shrines and lovely zen gardens. It is a city lled with Japanese history, but also modern, futuristic neo sci- streetscapes that make you feel like you’re a part of the Blade Runner movie. Tokyo’s 38 million inhabitants are equally proud of its ancient history and culture, as they are of its ultra-modern technology and architecture. Tokyo has a neighborhood for everyone, and it sure has something for you. Here we have put together a ve-day Tokyo itinerary with all the best things to do in Tokyo. If you don’t have ve days, then feel free to cherry pick your favorite days and things to see and do, and create your own two or three day Tokyo itinerary. Here is our five day Tokyo Itinerary! We hope you like it! Maria & Espen Nerdnomads.com Day 1 – Meiji-jingu Shrine, shopping and Japanese pop culture Areas: Harajuku – Omotesando – Shibuya The public train, subway, and metro systems in Tokyo are superb! They take you all over Tokyo in a blink, with a net of connected stations all over the city. -

1. 1.1 February 1.2 Conducte 2. 2.1 Between Their Ide 3. 3.1 Will Act 3.2

ISTF/1-IP/1 27/02/12 International Civil Aviation Organization FIRST MEETING OF IONOSPHERIC STUDIES TAKS FORCE (ISTF/1) 27-29 February 2012, Tokayo, Japan MEETING BULLETIN 1. Schedule of meeting 1.1 The opening session of the meeting will be held at 0930 hours on Monday, 27 February 2012 at the Mita Kaigisho, (Mita Conference Hall), Tokyo, Japan. 1.2 The technical tour to Electronic Navigation Research Institute (ENRI) will be conducted from 1000 to 1200 hours on Wednesday, 29 February 2012. 2. Registration of participants 2.1 Participants are requested to register at the Registration Desk of the Mita Kaigisho between 0915 - 0930 hours on the opening day of the meeting. Participants are also requested to wear their identification badge all the time inside the Mita Kaigisho. 3. Officers and Secretariat concerned with the meeting 3.1 Mr. Sujan K. Saraswati, Regional Officer CNS of the ICAO Asia and Pacific Office will act as Secretary of the meeting. His contact address is as follows: Mr. Sujan K. Saraswati, Regional Officer CNS Tel: +66 (2) 537 8189 to 97 Ext. 155 Fax: +66 (2) 537 8199 E-mail: [email protected] 3.2 The daily meeting service is the responsibility of Dr. Susumu Saito. Dr. Saito will provide secretarial support. The contact address is as follows: Dr. Susumu Saito, Senior Researcher, CNS Department Electronic Navigation Research Institute (ENRI) Tel: +81 422 413 191 Fax: +81 422 413 199 E-mail: [email protected] 4. Meeting documents for distribution 4.1 Participants wishing to make presentations or present papers for distribution during the meeting are requested to submit electronic copies to the Secretariat as early as possible, and preferably no later than 13 Febrruary 2012 at the following email addresses: [email protected] and cc: [email protected] ISTF/1-IP/1 -2- 27/02/12 5. -

Sunshine City Prince Hotel

November 2018 Sunshine City Prince Hotel Announcing the birth of a hotel floor for all fans of Japan’s subculture, including those from other countries, in Tokyo’s Ikebukuro district! Opening of a concept floor in April 2019 (tentative) In April 2019 (tentative), Sunshine City Prince Hotel (3-1-5 Higashi-Ikebukuro, Toshima-ku, Tokyo; Tsuyoshi Okumura, General Manager) will open a new floor taking Japanese subculture as its theme. This concept floor will be designed to motivate trips to Japan by overseas fans of Japanese anime, manga, and other elements of Japanese subculture, and make their stay at the hotel even more fun. Located on the 25th floor of the hotel, the concept floor will consist of four common-use areas and 20 concept rooms , and have features differing from hotel floors having only rooms for guests. Taking “a dream-come-true experience of a stay surrounded by things you love” as its watchword, this floor will be designed especially for guests from other countries who love anime, manga, and other elements of Japanese subculture. It will make their stay a dream-like one unlike anything they have experienced before. Instead of having the same contents throughout the year, the floor will change the tie-up contents in step with the going needs and with the right timing, for use by a wider circle of fans. Common-use area: event space Common-use area: library space Twin room A (conceptual depi ction) (conceptual depiction) (conceptual depiction) Together with the Shinjuku and Shibuya districts, the Ikebukuro district of Tokyo’s Toshima Ward, in which our hotel is situated, is one of the three major subcenters of Tokyo. -

Former House of the Ishimaru Family “L'assemblee HIROO”

Community Information Paper No.42 February 2018 Translated/Issued by Azabu Regional City Office Edited by the Azabu Editing Office 5-16-45 Roppongi, Minato City, Tokyo, 106-8515 Tel: 03-5114-8812 (Rep.) Fax: 03-3583-3782 Please contact Minato Call for inquiries regarding Residents’ Life Support. Tel: 03-5472-3710 A community information paper created and edited by people who live in Azabu. Fascinated by Artistic Azabu ⑮ A Mansion Preserved and Protected in the Azabu Area Former House of the Ishimaru Family “l’Assemblee HIROO” l’Assemblee HIROO Area of the premises: 542.1m2 (About 167.3 tsubo), Building floor space: 314.8m2 (About 97.2 tsubo) Do you know about this mansion quietly nestled along the Teppo-zaka alleyway slope in Minami Azabu? It turned 95 years old in 2017, but still has all the fascinating and elegant appearance it had when it was first built. This luxurious mansion was built for the late Mr. Sukezaburo In what was formerly a bedroom, there are several elements Ishimaru, upon his return from London in 1922. In the fol- of Japanese style, including sliding doors and tokonoma (al- lowing year, 1923, the Great Kanto Earthquake struck this cove). However, all of this is matched harmoniously with the area. Fortunately, this building was not seriously damaged. Western-style fireplace, also designed in consideration of the family’s lifestyle. On the premises, there are three of the zelkova trees that are over 300 years old. There is a story that relates how, during The stone pillar in the dining room, the handrail of the stairs, the Great Tokyo Air Raid in 1945, those living in the neigh- and the beams in the student room on the top floor remain borhood poured water over this cypress tree to protect the unchanged and fully functional, the same as they have always Some earthquake reinforcement has been carried out for the building, and the stones forming the pillar are the same as tree. -

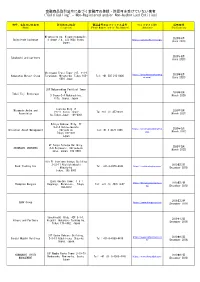

金融商品取引法令に基づく金融庁の登録・許認可を受けていない業者 ("Cold Calling" - Non-Registered And/Or Non-Authorized Entities)

金融商品取引法令に基づく金融庁の登録・許認可を受けていない業者 ("Cold Calling" - Non-Registered and/or Non-Authorized Entities) 商号、名称又は氏名等 所在地又は住所 電話番号又はファックス番号 ウェブサイトURL 掲載時期 (Name) (Location) (Phone Number and/or Fax Number) (Website) (Publication) Miyakojima-ku, Higashinodamachi, 2020年6月 SwissTrade Exchange 4-chōme−7−4, 534-0024 Osaka, https://swisstrade.exchange/ (June 2020) Japan 2020年6月 Takahashi and partners (June 2020) Shiroyama Trust Tower 21F, 4-3-1 https://www.hamamatsumerg 2020年6月 Hamamatsu Merger Group Toranomon, Minato-ku, Tokyo 105- Tel: +81 505 213 0406 er.com/ (June 2020) 0001 Japan 28F Nakanoshima Festival Tower W. 2020年3月 Tokai Fuji Brokerage 3 Chome-2-4 Nakanoshima. (March 2020) Kita. Osaka. Japan Toshida Bldg 7F Miyamoto Asuka and 2020年3月 1-6-11 Ginza, Chuo- Tel:+81 (3) 45720321 Associates (March 2021) ku,Tokyo,Japan. 104-0061 Hibiya Kokusai Bldg, 7F 2-2-3 Uchisaiwaicho https://universalassetmgmt.c 2020年3月 Universal Asset Management Chiyoda-ku Tel:+81 3 4578 1998 om/ (March 2022) Tokyo 100-0011 Japan 9F Tokyu Yotsuya Building, 2020年3月 SHINBASHI VENTURES 6-6 Kojimachi, Chiyoda-ku (March 2023) Tokyo, Japan, 102-0083 9th Fl Onarimon Odakyu Building 3-23-11 Nishishinbashi 2019年12月 Rock Trading Inc Tel: +81-3-4579-0344 https://rocktradinginc.com/ Minato-ku (December 2019) Tokyo, 105-0003 Izumi Garden Tower, 1-6-1 https://thompsonmergers.co 2019年12月 Thompson Mergers Roppongi, Minato-ku, Tokyo, Tel: +81 (3) 4578 0657 m/ (December 2019) 106-6012 2019年12月 SBAV Group https://www.sbavgroup.com (December 2019) Sunshine60 Bldg. 42F 3-1-1, 2019年12月 Hikaro and Partners Higashi-ikebukuro Toshima-ku, (December 2019) Tokyo 170-6042, Japan 31F Osaka Kokusai Building, https://www.smhpartners.co 2019年12月 Sendai Mubuki Holdings 2-3-13 Azuchi-cho, Chuo-ku, Tel: +81-6-4560-4410 m/ (December 2019) Osaka, Japan. -

TOKYO TRAIN & SUBWAY MAP JR Yamanote

JR Yamanote Hibiya line TOKYO TRAIN & SUBWAY MAP Ginza line Chiyoda line © Tokyo Pocket Guide Tozai line JR Takasaka Kana JR Saikyo Line Koma line Marunouchi line mecho Otsuka Sugamo gome Hanzomon line Tabata Namboku line Ikebukuro Yurakucho line Shin- Hon- Mita Line line A Otsuka Koma Nishi-Nippori Oedo line Meijiro Sengoku gome Higashi Shinjuku line Takada Zoshigaya Ikebukuro Fukutoshin line nobaba Todai Hakusan Mae JR Joban Asakusa Nippori Line Waseda Sendagi Gokokuji Nishi Myogadani Iriya Tawara Shin Waseda Nezu machi Okubo Uguisu Seibu Kagurazaka dani Inaricho JR Shinjuku Edo- Hongo Chuo gawa San- Ueno bashi Kasuga chome Naka- Line Higashi Wakamatsu Okachimachi Shinjuku Kawada Ushigome Yushima Yanagicho Korakuen Shin-Okachi Ushigome machi Kagurazaka B Shinjuku Shinjuku Ueno Hirokoji Okachimachi San-chome Akebono- Keio bashi Line Iidabashi Suehirocho Suido- Shin Gyoen- Ocha Odakyu mae Bashi Ocha nomizu JR Line Yotsuya Ichigaya no AkihabaraSobu Sanchome mizu Line Sendagaya Kodemmacho Yoyogi Yotsuya Kojimachi Kudanshita Shinano- Ogawa machi Ogawa Kanda Hanzomon Jinbucho machi Kokuritsu Ningyo Kita Awajicho -cho Sando Kyogijo Naga Takebashi tacho Mitsu koshi Harajuku Mae Aoyama Imperial Otemachi C Meiji- Itchome Kokkai Jingumae Akasaka Gijido Palace Nihonbashi mae Inoka- Mitsuke Sakura Kaya Niju- bacho shira Gaien damon bashi bacho Tameike mae Tokyo Line mae Sanno Akasaka Kasumi Shibuya Hibiya gaseki Kyobashi Roppongi Yurakucho Omotesando Nogizaka Ichome Daikan Toranomon Takaracho yama Uchi- saiwai- Hachi Ebisu Hiroo Roppongi Kamiyacho -

MANGA⇔TOKYO (Venue: La Villette, Paris, France)

2018.7.5 Press Release: Opening Announcement The National Art Center, Tokyo The Japan Foundation November 29 (Thu.) – December 30 (Sun.), 2018 The National Art Center, Tokyo International Exhibition | Japonismes2018 official program MANGA⇔TOKYO (Venue: La Villette, Paris, France) Illustration by Yoh Yoshinari / Graphic design by Tsuyoshi Kusano ©Crypton Future Media, INC. www.piapro.net / ©khara / ©Naoko Takeuchi/PNP, Toei Animation / ©Osamu Akimoto, Atelier Beedama/SHUEISHA / ©SOTSU, SUNRISE / ©TOHO CO., LTD. The National Art Center, Tokyo and the Japan Foundation are pleased to announce that the "MANGA ⇔ TOKYO" exhibition will be held at La Villette in Paris, France from November 29, 2018 (Thursday). Japan's manga, animation, games, SFX films (tokusatsu) are reflective of the social change and technological development of the city of <Tokyo>. This exhibition pursues to represent these depictions through numerous drawings, models and images. How did the characteristics of the real city inspire the direction of fiction? How did these fictions and their characters present us with a new hybrid reality, now multilayered to the real city? This exhibition does focus on Japanese manga, animation, games, and SFX films (tokusatsu), but through them it also portrays the city of <Tokyo>, already iconic in a lot of people’s mind. It hopes to delve into the meaning and possibilities for Japan’s animation, manga and its gaming culture, as they have become tourism drawcards and created what for many enthusiasts is a "sacred pilgrimage" when visiting Japan. The “MANGA⇔TOKYO” exhibition follows the first highly successful “Manga*Anime*Games from Japan” exhibition held at the National Art Center, Tokyo in 2015, and is one of the official programs of “Japonismes 2018: les âmes en résonance”, an extensive cultural season to showcase the unrevealed beauty of Japanese culture in France. -

Guideline for Community Development

Peripheral Area of Tamachi Station West Exit/Fudanotsuji Crossing Guideline for Community Development February 2013 Minato City The community, from Edo to Tokyo, continues creating a future where comfortable and active living blends in with bustling streets, bringing splendid harmony Greetings, The peripheral area of Tamachi Station West Exit/Fudanotsuji Crossing (hereinafter referred to as “the District”) used to be an area with a place called “Fudanotsuji” where there was a place to post a notice board called “kosatsuba,” and functioned as the main entrance of Edo City. In this area, there was also a kurayashiki (warehouse-residence) of Satsuma domain where Ta- kamori Saigo and Kaishu Katsu had an interview for negotiating the bloodless surrender of Edo Castle. As time goes by after the Edo Period, the District and its surrounding areas have experienced various changes in the community; firstly, a number of educational and academic institutions were built, factories which supported the living of the residents were built afterwards, and now the community has become a business-oriented area. In the meantime, we have a great city- scape with rich greenery on the hilltop of Takanawa, as well as a bustling shopping street full of vitality. The District, along with the peripheral area of Tamachi Station East Exit, is designated as a national “Area to be Emergently Developed for Specified City Reproduction,” and expected to form a new hub district where a variety of functions are integrated in order to strengthen Tokyo’s global competitiveness. Taking this opportunity to promote future reconstruction in Minato City, we have prepared the “Peripheral area of Tamachi Station West/Fudanotsuji Crossing Guideline for Community De- velopment” as a manual in order to solve problems and to develop a comfortable and attractive community. -

THE WESTIN TOKYO Sakura Map

THE WESTIN TOKYO Sakura Map 1 Meguro River 2 Yoyogi Park Take the JR Yamanote Line from Ebisu Station to Take the JR Yamanote Line from Ebisu Station to Meguro Station (3 minutes). 5 minutes' walk from Harajuku Station (5 minutes). 3 minutes' walk from Meguro Station. Harajuku Station. Along both sides of the river banks spanning Atop the vast lawn, you will find cherry trees 4km, you will find 800 Somei Yoshino cherries in full bloom. This is a popular cherry in bloom. At night, they are illuminated. blossom viewing location. Ueno 4 Yamanote Line Sobu Line Kudanshita Hanzomon Line 7 Shinjyuk3ugyoen 3 Shinjyuku Gyoen National Park 4 Ueno Onshi Park Take the JR Yamanote Line from Ebisu Station to Shinjuku Take the JR Yamanote Line from Ebisu Station to Shinjyuku Station. From Shinjuku Station, board the Tokyo Metro Ueno Station (30 minutes). 2 minutes' walk from the Marunouchi Line and take it to Shinjuku-gyoenmae Station (3 Ueno Park exit of Ueno Station. minutes). 5 minutes' walk from Shinjuku-gyoenmae Station. The main road through the park features Enjoy 1,300 cherry trees of 65 varieties 1,200 cherry trees, making it one of the Marunouchi Line 6 outbloom. foremost destinations in Tokyo. Roppongi 5 Tokyo Midtown Harajyuku Shinanomachi 2 Take the Tokyo Metro Hibiya Line from Ebisu Station to Roppongi Station (6 minutes). 6 minutes' walk from Roppongi Station. 5 When in full bloom, sakura street is turned to sakura tunnel. At night, their illuminated blossoms create a bewitching mood. Hibiya Line 8 6 Meiji Jingu Gaien Ebisu Hamamatsucho Take the JR Yamanote Line from Ebisu Station to Yoyogi Station (8 minutes).