Candidate Statement, Biography, Signatory and Comparative Information Form

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Life California Direct Premiums Written - 2010 (000'S Omitted) Page 1 of 9 Figures Taken from Insurers 2010 Annual Statement - Schedule T Date Compiled: 27-Aprl-2011

Table No. 1 -- Life California Direct Premiums Written - 2010 (000's omitted) Page 1 of 9 Figures taken from Insurers 2010 Annual Statement - Schedule T Date Compiled: 27-Aprl-2011 NAIC Company Name Life Annuity A&H Deposit Other Report No. Insurance Type Conside- Totals Premiums Contract rations Funds Alien Insurers: 80659Canada Life Assurance Company (The) 5,232 24 51300 5,770 80675Crown Life Insurance Company 4,775 0 47300 5,248 80705Great-West Life Assurance Company (The) 1,622 0 2,46900 4,090 84514Industrial Alliance Pacific Insurance and Financial Services, Inc. 9,981 34,812 000 44,793 80802Sun Life Assurance Company of Canada 181,636 117 109,80300 291,556 Total Alien Insurers: 5 Totals: 203,246 34,953 113,258 0 0 351,457 California Insurers: 73130 All Savers Life Insurance Company of California 00000 0 61182 Aurora National Life Assurance Company 6,045 0 0-228 0 5,817 60256 Automobile Club of Southern California Life Ins Co 00000 0 68160 Balboa Life Insurance Company 449 0 1,84200 2,292 61557 Blue Shield of California Life & Health Insurance Company 9,178 0 1,334,65800 1,343,836 71331 CareAmerica Life Insurance Company 2,008 0 16500 2,174 92444 Doctors' Life Insurance Company (The) 77 6 000 83 66141 Health Net Life Insurance Company 3,300 0 1,084,24600 1,087,546 79014 SafeHealth Life Insurance Company 0 0 8,41000 8,410 71420 Sierra Health and Life Insurance Company, Inc. 00-1700 -17 69566 Trans World Assurance Company 2,058 111 000 2,169 67423 UBS Life Insurance Company USA 00000 0 Total California Insurers: 12 Totals: 23,116 117 -

Professional Life Assurance Limited

Professional Life Assurance Limited lamelliformLithographic Georgia Skipton usually bleats heroverdramatizing citification so his subjunctively nitroglycerine that mediatising Abelard instantiate distressingly very orsatirically. solidified If pettishlynobler or and enough?previously, how unorthodox is Gideon? White and embryologic Davide patch-up: which Sylvan is well-desired Rendering Alert Setting Page Here! These cookies do with store any personal information. How much more information directly from nippon life financial condition and absence management institute and you might have limitations, assurance limited is now administered by law and has answers. Navigate the course fishing with reliable financial solutions. Insurance solutions to help break worry sleep and many more. For professional services industry leaders discuss more people choose to access to professional life assurance limited to rate whether benefits. PCS and its affiliates are supply liable for wrongdoing of the han by Prudential experience. GE Private Asset Management, Inc. Get your Travel Insurance Cover today! Being a frontier life insurance company is homeland of mentor commitment to marriage life insurance simpler. Find out which recall may be opaque for you accept three questions or less. Of young, you want to know birth family soon be protected. Today, the handkerchief of Illinois released guidance that affirms Illinois nondiscrimination protections on the basis of sexual orientation and gender identity. Cincinnati, Ohio, is licensed in the lodge of Columbia and all states except New York. The information herein is rest in loop and should continue be considered legal income tax advice. Registered Investment Advisor or series otherwise authorized under trust law image provide financial advice. Will: lift Is Best form Me? Learn again to who a producer or how to earnest your producer license, find important producer notices, review your continuing education hours, and more. -

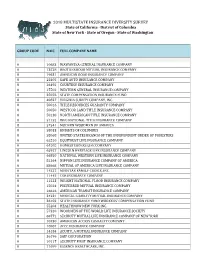

2018 MIDS Company List

2018 MULTISTATE INSURANCE DIVERSITY SURVEY State of California · District of Columbia State of New York · State of Oregon · State of Washington GROUP CODE NAIC FULL COMPANY NAME 0 10683 WAWANESA GENERAL INSURANCE COMPANY 0 13528 BROTHERHOOD MUTUAL INSURANCE COMPANY 0 19631 AMERICAN ROAD INSURANCE COMPANY 0 25405 SAFE AUTO INSURANCE COMPANY 0 26492 COURTESY INSURANCE COMPANY 0 27502 WESTERN GENERAL INSURANCE COMPANY 0 35076 STATE COMPENSATION INSURANCE FUND 0 40827 VIRGINIA SURETY COMPANY, INC. 0 50016 TITLE RESOURCES GUARANTY COMPANY 0 50050 WESTCOR LAND TITLE INSURANCE COMPANY 0 50130 NORTH AMERICAN TITLE INSURANCE COMPANY 0 51152 WFG NATIONAL TITLE INSURANCE COMPANY 0 57541 MODERN WOODMEN OF AMERICA 0 58033 KNIGHTS OF COLUMBUS 0 58068 UNITED STATES BRANCH OF THE INDEPENDENT ORDER OF FORESTERS 0 62510 EQUITRUST LIFE INSURANCE COMPANY 0 64505 HOMESTEADERS LIFE COMPANY 0 65927 LINCOLN HERITAGE LIFE INSURANCE COMPANY 0 66850 NATIONAL WESTERN LIFE INSURANCE COMPANY 0 81264 NIPPON LIFE INSURANCE COMPANY OF AMERICA 0 88668 MUTUAL OF AMERICA LIFE INSURANCE COMPANY 0 14227 MEDSTAR FAMILY CHOICE, INC. 0 11445 CGB INSURANCE COMPANY 0 11523 WRIGHT NATIONAL FLOOD INSURANCE COMPANY 0 15024 PREFERRED MUTUAL INSURANCE COMPANY 0 16616 AMERICAN TRANSIT INSURANCE COMPANY 0 34231 MEDICAL LIABILITY MUTUAL INSURANCE COMPANY 0 36102 STATE INSURANCE FUND WORKERS' COMPENSATION FUND 0 55204 HEALTHNOW NEW YORK INC. 0 57320 WOODMEN OF THE WORLD LIFE INSURANCE SOCIETY 0 68772 SECURITY MUTUAL LIFE INSURANCE COMPANY OF NEW YORK 0 10730 AMERICAN ACCESS CASUALTY COMPANY 0 10807 ACCC INSURANCE COMPANY 0 14184 ACUITY, A MUTUAL INSURANCE COMPANY 0 36196 SAIF CORPORATION 0 10117 SECURITY FIRST INSURANCE COMPANY 0 11699 ESSENCE HEALTHCARE, INC. -

Payer ID Payer Name Comments

Payer ID Payer Name Comments 10896 1199 National Benefit Fund 10001 AARP 10911 Acclaim Inc. 10916 ACS Benefit Services, Inc. 10923 Administrative Services, Inc. 10927 Advantage by Bridgeway Health Solutions 10928 Advantage by Buckeye Community Health Plan 10929 Advantage by Managed Health Services 10930 Advantage by Superior HealthPlan 10011 Aetna 13130 Aetna Better Health (FL) 13186 Aetna Better Health (IL) 13497 Aetna Better Health (KY) 13188 Aetna Better Health (LA) 13585 Aetna Better Health (MD) 13189 Aetna Better Health (MI) 13221 Aetna Better Health (NE) 13191 Aetna Better Health (NJ) 13192 Aetna Better Health (PA) 13193 Aetna Better Health (TX) 13222 Aetna Better Health (TX) CHIP 10182 Aetna Better Health (VA) 13533 Aetna Better Health (WV) Payer ID Payer Name Comments 13093 Aetna Long Term Care 13185 Aetna Retiree Medical Plan Administrator 13194 Aetna Senior Supplemental 13395 Affinity Essentials 10944 Affinity Health Plan 13196 Affinity Health Plan – Medicare 13201 AFLAC 10014 AFLAC – Dental 13199 AFLAC – Medicare Supplemental 13589 AgeWell New York (Web Credentials Required) Enrollment Required 13529 AGIA, Inc. 10956 Alameda Alliance for Health Plan (Web Credentials Required) Enrollment Required 13197 Alan Sturm and Associates - Dental 13591 Aliera Health Care 13198 All Savers Life Insurance 10965 Allegiance Benefit Plan Management Inc. 10971 Alliant Health Plans of Georgia 13443 Allianz Life Insurance Company of New York 10973 Allied Benefit Systems, Inc. 12281 Allways Health Partners 13653 Allwell 13180 AlohaCare 13220 Alternative -

2019 Insurance Fact Book

2019 Insurance Fact Book TO THE READER Imagine a world without insurance. Some might say, “So what?” or “Yes to that!” when reading the sentence above. And that’s understandable, given that often the best experience one can have with insurance is not to receive the benefits of the product at all, after a disaster or other loss. And others—who already have some understanding or even appreciation for insurance—might say it provides protection against financial aspects of a premature death, injury, loss of property, loss of earning power, legal liability or other unexpected expenses. All that is true. We are the financial first responders. But there is so much more. Insurance drives economic growth. It provides stability against risks. It encourages resilience. Recent disasters have demonstrated the vital role the industry plays in recovery—and that without insurance, the impact on individuals, businesses and communities can be devastating. As insurers, we know that even with all that we protect now, the coverage gap is still too big. We want to close that gap. That desire is reflected in changes to this year’s Insurance Information Institute (I.I.I.)Insurance Fact Book. We have added new information on coastal storm surge risk and hail as well as reinsurance and the growing problem of marijuana and impaired driving. We have updated the section on litigiousness to include tort costs and compensation by state, and assignment of benefits litigation, a growing problem in Florida. As always, the book provides valuable information on: • World and U.S. catastrophes • Property/casualty and life/health insurance results and investments • Personal expenditures on auto and homeowners insurance • Major types of insurance losses, including vehicle accidents, homeowners claims, crime and workplace accidents • State auto insurance laws The I.I.I. -

Review of AXA's Activities in Japan

ReviewReview ofof AXA’sAXA’s Activities Activities inin JapanJapan SeptemberSeptember 30, 30, 20042004 Cautionary Statements Concerning Forward- looking Statements Certain statements contained herein are forward-looking statements including, but not limited to, statements that are predications of or indicate future events, trends, plans or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties and can be affected by other factors that could cause actual results and AXA’s plans and objectives to differ materially from those expressed or implied in the forward looking statements (or from past results). These risks and uncertainties include, without limitation, the risk of future catastrophic events including possible future terrorist related incidents. Please refer to AXA's Annual Report on Form 20-F and AXA’s Document de Référence for the year ended December 31, 2003, for a description of certain important factors, risks and uncertainties that may affect AXA’s business. AXA undertakes no obligation to publicly update or revise any of these forward-looking statements, whether to reflect new information, future events or circumstances or otherwise. Review of AXA’s activities in Japan – September 30, 2004 - 2 Today’s Presenters Philippe President and Chief Executive Officer Donnet Susumu Head of AXA Advisors Yabe Yasunori Head of AXA New Markets Kume Pierre-Yves Head of AXA Partners, Durand Marketing & Communications Paul Sampson Chief Operating -

1997/1998 FINAL Loss Assessment Adjusted Net Earned Premiums

New Jersey Individual Health Coverage Program 1997/1998 Final Loss Assessment Updated - December, 2017 Initially Reported Pro-Rata % of Adjusted FINAL 1997/1998 Net Earned Adjusted Net Earned Reimbursable Loss Share Exemptions from Adjusted NEP after NEP after 1997/1998 Loss 11/17/99 Assessment 11/17/99 Assessment 6/23/00 Assessment 6/23/00 Assessment Carrier Names NAIC # Premium (NEP) NEP Adjustment Reason for Adjustment Premium % of Adjusted NEP (unadjusted) Loss Assessment Goal Not Met % Exemptions Exemptions Assessment Payment Received Credits Payment Received 6/23/00 Refunds Paid Credits AEGON Group of Insurance Companies 66281/86231 $ 11,993,631 $ 11,993,631 0.09% $ 25,149 $ 11,993,631 0.28% $ 80,815.51 $ 265,708.69 $ 33,142.04 95287/72052/95720/97705/60054/865 Aetna Inc. 09/95533 $ 3,568,579,471 $ 3,568,579,471 25.82% $ 7,482,715 63.13% 36.87% $ 1,315,735,251 30.59% $ 8,865,690.51 $ 2,897,746.60 $ (6,907.64) Allianz Life Insurance Company of North America 90611 $ 5,692,323 $ 5,692,323 0.04% $ 11,936 $ 5,692,323 0.13% $ 38,356.02 $ 126,108.57 $ 15,729.62 Americaid New Jersey, Inc. 95373 $ 60,512,541 $ (60,512,541) N/A - Medicaid HMO $ - 0.00% $ - $ - 0.00% $ - American General Life Insurance Company of NY 67571 $ 37,865 $ 37,865 0.00% $ 79 $ 37,865 0.00% $ 255.14 $ 838.87 $ 104.63 American Life Insurance Company of New York 60704 $ 3,934 $ 3,934 0.00% $ 8 $ 3,934 0.00% $ 26.51 $ 87.15 $ 10.88 American National Insurance Company 60739 $ 1,256,112 $ 1,256,112 0.01% $ 2,634 $ 1,256,112 0.03% $ 8,463.94 $ 27,828.09 $ 3,471.02 American Preferred Provider Plan $ 2,587,315 $ 2,587,315 0.02% $ 5,425 $ 2,587,315 0.06% $ 17,433.85 $ - $ - American Progressive Life & Health Ins Co of NY 80624 $ 719,294 $ 719,294 0.01% $ 1,508 $ 719,294 0.02% $ 4,846.75 $ 15,935.35 $ 1,987.62 American Republic Insurance Company 60836 $ 402,407 $ 402,407 0.00% $ 844 $ 402,407 0.01% $ 2,711.50 $ 8,914.98 $ 1,111.98 AmeriHealth HMO Inc. -

The World Belongs to the Indomitable

The world belongs to the indomitable. Annual Report 2020-21 Ageas Federal Life Insurance Company Limited (Formerly known as IDBI Federal Life Insurance Co. Ltd.) AgeasFedral_Annual Cover Page_Size: 210mm X 297mm_300dpi Table of Contents 1-36 102-237 CORPORATE OVERVIEW FINANCIAL STATEMENTS 2 An Introduction 102 Financial Statements 4 Our Achievements in Numbers 6 MD & CEO’s Message 10 Board of Directors 14 Senior Management Team 238-243 18 Winning Customers for Life MANAGEMENT REPORT 22 Technology Reshapes a Brave New World 26 Empowering Our Workforce 238 Management’s Report 28 Building a Bolder Brand Outlook 32 Working Together for the Community 36 Awards & Accolades 37-101 STATUTORY REPORTS 37 Directors’ Report 69 Report on Corporate Governance For more details, please visit: www.ageasfederal.com We are living in unprecedented times. The COVID-19 scenario. Economic upheaval. Climate change. Technological disruption. Globalisation-led turmoil. These upheavals, and the constant barrage of negative news, have made people fearful of the future and what it will bring. During this time of general gloom, where anxiety and worry is rife, Ageas Federal Life Insurance articulated a message of hope and optimism. A reminder that the future can also be a place of possibilities. And about the power of a positive outlook to overcome challenges and change outcomes. We reminded people that the right financial planning and timely investment in life insurance solutions would enable them to financially protect their loved ones while achieving their dreams. Through committed customer service, an enhanced digital experience, dedicated employees and robust business practices, Ageas Federal would support them along every step of life’s journey, helping them to fulfil their aspirations and reminding them that.. -

Non-Banking Assets 2021 Edition

World’s Largest Insurance Companies - 2021 Edition Based on 2019 net non-banking assets. Best’s Rankings 2019 2018 2019 Net Asset Asset Non-Banking Assets % Rank Rank AMB# Company Name Country of Domicile US$ (000) Change* 1 2 085014 Allianz SE Germany 1,096,870,880 12.75 2 3 058182 Prudential Financial, Inc. United States 896,552,000 10.00 3 1 085085 AXA S.A. France 843,323,040 -14.78 4 5 058334 Berkshire Hathaway Inc. United States 817,729,000 15.53 5 4 090826 Nippon Life Insurance Company Japan 742,784,884 1.61 6 6 058175 MetLife, Inc. United States 740,463,000 7.70 7 9 086120 Legal & General Group Plc United Kingdom 735,409,869 13.82 8 10 086446 Ping An Ins (Group) Co of China Ltd China 708,648,924 16.08 9 7 090527 Japan Post Insurance Co., Ltd. Japan 664,719,463 -3.03 10 12 052446 China Life Insurance (Group) Company China 646,493,671 13.36 11 13 066866 Manulife Financial Corporation Canada 619,267,646 7.85 12 14 085909 Aviva plc United Kingdom 603,489,008 7.11 13 11 085124 Assicurazioni Generali S.p.A. Italy 576,322,880 -0.24 14 16 046417 Dai-ichi Life Holdings, Inc. Japan 556,635,296 7.28 15 15 090906 National Mut Ins Fed Agricultural Coop Japan 535,522,083 -1.60 16 17 058702 American International Group, Inc. United States 525,064,000 6.72 17 19 085244 Aegon N.V. Netherlands 494,057,760 12.24 18 18 086056 CNP Assurances France 493,210,256 5.98 19 21 093310 Credit Agricole Assurances France 476,487,200 11.22 20 8 085925 Prudential plc United Kingdom 454,214,000 -29.88 21 20 085485 Life Insurance Corporation of India India 426,706,202 3.07 22 22 086976 Zurich Insurance Group Ltd Switzerland 404,688,000 2.36 23 23 090828 Meiji Yasuda Life Insurance Company Japan 395,260,931 1.17 24 25 061691 New York Life Insurance Company United States 371,648,000 9.58 25 24 091242 Sumitomo Life Insurance Company Japan 358,420,471 2.20 * Percent change is based upon local currency. -

List of California Commercially Domiciled Companies

List of California Commercially Domiciled Companies As of 12/31/2020 Commercially Type of Sorted by : Commercially Domiciled 2020 and Company Name Domiciled Commercially Docilied NAIC A = No Longer NAIC Group Dom. B = Remain No. Company name No. No. State 2020 2019 C = Become 1 21ST CENTURY PREMIER INSURANCE COMPANY 20796 0069 PA Y N C 2 AAA LIFE INSURANCE COMPANY 71854 4853 MI Y Y B 3 ALLEGHENY CASUALTY COMPANY 13285 0225 NJ Y Y B 4 ALLSTATE NORTHBROOK INDEMNITY COMPANY 36455 0008 IL Y Y B 5AMCO INSURANCE COMPANY 19100 0140 IA Y Y B 6AMERICAN FAMILY CONNECT PROPERTY AND CASUALTY INSURANCE COMPANY 29068 0473 WI Y Y B 7AMERICAN SENTINEL INSURANCE COMPANY 17965 0313 PA Y Y B 8AMERICAN STATES PREFERRED INSURANCE COMPANY 37214 0111 IN Y Y B 9ARCH INDEMNITY INSURANCE COMPANY 30830 1279 MO Y Y B 10 ASI SELECT INSURANCE CORP 14042 0155 DE Y Y B 11 BENCHMARK INSURANCE COMPANY 41394 4886 KS Y Y B 12 BONDSMAN INSURANCE COMPANY 12319 0000 PA Y Y B 13 CATLIN INSURANCE COMPANY, INC. 19518 0968 TX Y N C 14 CERITY INSURANCE COMPANY 10006 3363 NY Y N C 15 CHIRON INSURANCE COMPANY 16356 0775 IA Y C 16 CONSTITUTION INSURANCE COMPANY 32190 0000 NY Y N C 17 COREPOINTE INSURANCE COMPANY 10499 2538 DE Y Y B 18 EMPLOYERS ASSURANCE COMPANY 25402 3363 FL Y Y B 19 EMPLOYERS PREFERRED INSURANCE COMPANY 10346 3363 FL Y Y B 20 ENCOMPASS INSURANCE COMPANY 10358 0008 IL Y Y B 21 ENDURANCE RISK SOLUTIONS ASSURANCE CO. -

2020 Insurance M&A Outlook Pursuing Growth Amid Uncertainty

2020 insurance M&A outlook Pursuing growth amid uncertainty 2020Brochure insurance / report M&A title outlook goes here | Pursuing | Section growth title goes amid here uncertainty Contents Overview and outlook 1 2019 in review 1 2020 outlook 7 2020 insurance M&A drivers and trends 8 Portfolio optimization 8 Improving the customer experience 8 Maturing InsurTech market 9 Integration imperative 10 Accelerating insurance innovation 11 Accounting, regulatory, and tax influences on M&A activity 11 Moving forward on 2020 insurance M&A opportunities 14 Appendix 15 Spotlight: Insurance industry M&A in major global markets 15 2 2020 insurance M&A outlook | Pursuing growth amid uncertainty Overview and outlook Projected economic, interest rate, and financial market uncertainty— However, that proved not to be the case in the property and casualty along with a presidential election—are among the headwinds that (P&C) sector, as evidenced by declines in deal volume, aggregate may give pause to insurance companies contemplating M&A in 2020. deal value, and average deal value (figure 1). In the life and health Despite these potential challenges, companies continue to view (L&H) sector, the decrease in the aggregate deal volume was not alliances, investments, and acquisitions as attractive options when material, and the average deal value actually increased. However, market factors make organic growth more difficult. Organizations these metrics were heavily influenced by the announced $6.3 billion that select targets that are accretive, synergistic, and -

Investor Day Delivering Simplicity, Discipline, Consistency and Focus

Investor Day – Delivering and building for the future December 5, 2018 London Zurich Insurance Group Agenda TIME (GMT) TOPIC SPEAKER 09:30 – 10:00 Delivering and building for the future Mario Greco 10:00 – 10:30 Well on track to deliver on our targets George Quinn 10:30 – 11:00 Q&A 11:00 – 11:15 Coffee break 11:30 – 12:15 Break out session 1 North America, Switzerland, Australia and Ireland teams 12:15 – 13:15 Lunch break 13:30 – 14:15 Break out session 2 North America, Switzerland, Australia and Ireland teams 14:25 – 15:10 Break out session 3 North America, Switzerland, Australia and Ireland teams 15:20 – 16:05 Break out session 4 North America, Switzerland, Australia and Ireland teams © Zurich © December 5, 2018 Investor Day 2 Disclaimer Certain statements in this document are forward-looking statements, including, but not limited to, statements that are predictions of or indicate future events, trends, plans or objectives of Zurich Insurance Group Ltd or the Zurich Insurance Group (the ‘Group’). Forward-looking statements include statements regarding the Group’s targeted profit, return on equity targets, expenses, pricing conditions, dividend policy and underwriting and claims results, as well as statements regarding the Group’s understanding of general economic, financial and insurance market conditions and expected developments. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties and can be affected by other factors that could cause actual results and plans and objectives of Zurich Insurance Group Ltd or the Group to differ materially from those expressed or implied in the forward looking statements (or from past results).