2020 Insurance M&A Outlook Pursuing Growth Amid Uncertainty

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Post Event Report

presents 9th Asian Investment Summit Building better portfolios 21-22 May 2014, Ritz-Carlton, Hong Kong Post Event Report 310 delegates representing 190 companies across 18 countries www.AsianInvestmentSummit.com Thank You to our sponsors & partners AIWEEK Marquee Sponsors Co-Sponsors Associate Sponsors Workshop Sponsor Supporting Organisations alternative assets. intelligent data. Tech Handset Provider Education Partner Analytics Partner ® Media Partners Offical Broadcast Partner 1 www.AsianInvestmentSummit.com Delegate Breakdown 310 delegates representing 190 companies across 18 countries Breakdown by Organisation Institutional Investors 46% Haymarket Financial Media delegate attendee data is Asset Managemer 19% independently verified by the BPA Consultant 8% Fund Distributor / Private Wealth Management 5% Media & Publishing 4% Commercial Bank 4% Index / Trading Platform Provider 3% Association 2% Other 9% Breakdown of Institutional Investors Insurance 31% Endowment / Foundation 27% Corporation 13% Pension Fund 13% Family Office 8% Breakdown by Country Sovereign Wealth Fund 6% PE Funds of Funds 1% Mulitlateral Finance Hong Kong 82% Institution 1% ASEAN 10% North Asia 5% Australia 1% Europe 1% North America 1% Breakdown by Job Function Investment 34% Finance / Treasury 20% Marketing and Investor Relations 19% Other 11% CEO / Managing Director 7% Fund Selection / Distribution 7% Strategist / Economist 2% 2 www.AsianInvestmentSummit.com Participating Companies Haymarket Financial Media delegate attendee data is independently verified by the BPA 310 institutonal investors, asset managers, corporates, bankers and advisors attended the Forum. Attending companies included: ACE Life Insurance CFA Institute Board of Governors ACMI China Automation Group Limited Ageas China BOCOM Insurance Co., Ltd. Ageas Hong Kong China Construction Bank Head Office Ageas Insurance Company (Asia) Limited China Life Insurance AIA Chinese YMCA of Hong Kong AIA Group CIC AIA International Limited CIC International (HK) AIA Pension and Trustee Co. -

Allianz Se Allianz Finance Ii B.V. Allianz

2nd Supplement pursuant to Art. 16(1) of Directive 2003/71/EC, as amended (the "Prospectus Directive") and Art. 13 (1) of the Luxembourg Act (the "Luxembourg Act") relating to prospectuses for securities (loi relative aux prospectus pour valeurs mobilières) dated 12 August 2016 (the "Supplement") to the Base Prospectus dated 2 May 2016, as supplemented by the 1st Supplement dated 24 May 2016 (the "Prospectus") with respect to ALLIANZ SE (incorporated as a European Company (Societas Europaea – SE) in Munich, Germany) ALLIANZ FINANCE II B.V. (incorporated with limited liability in Amsterdam, The Netherlands) ALLIANZ FINANCE III B.V. (incorporated with limited liability in Amsterdam, The Netherlands) € 25,000,000,000 Debt Issuance Programme guaranteed by ALLIANZ SE This Supplement has been approved by the Commission de Surveillance du Secteur Financier (the "CSSF") of the Grand Duchy of Luxembourg in its capacity as competent authority (the "Competent Authority") under the Luxembourg Act for the purposes of the Prospectus Directive. The Issuer may request the CSSF in its capacity as competent authority under the Luxemburg Act to provide competent authorities in host Member States within the European Economic Area with a certificate of approval attesting that the Supplement has been drawn up in accordance with the Luxembourg Act which implements the Prospectus Directive into Luxembourg law ("Notification"). Right to withdraw In accordance with Article 13 paragraph 2 of the Luxembourg Act, investors who have already agreed to purchase or subscribe for the securities before the Supplement is published have the right, exercisable within two working days after the publication of this Supplement, to withdraw their acceptances, provided that the new factor arose before the final closing of the offer to the public and the delivery of the securities. -

Life California Direct Premiums Written - 2010 (000'S Omitted) Page 1 of 9 Figures Taken from Insurers 2010 Annual Statement - Schedule T Date Compiled: 27-Aprl-2011

Table No. 1 -- Life California Direct Premiums Written - 2010 (000's omitted) Page 1 of 9 Figures taken from Insurers 2010 Annual Statement - Schedule T Date Compiled: 27-Aprl-2011 NAIC Company Name Life Annuity A&H Deposit Other Report No. Insurance Type Conside- Totals Premiums Contract rations Funds Alien Insurers: 80659Canada Life Assurance Company (The) 5,232 24 51300 5,770 80675Crown Life Insurance Company 4,775 0 47300 5,248 80705Great-West Life Assurance Company (The) 1,622 0 2,46900 4,090 84514Industrial Alliance Pacific Insurance and Financial Services, Inc. 9,981 34,812 000 44,793 80802Sun Life Assurance Company of Canada 181,636 117 109,80300 291,556 Total Alien Insurers: 5 Totals: 203,246 34,953 113,258 0 0 351,457 California Insurers: 73130 All Savers Life Insurance Company of California 00000 0 61182 Aurora National Life Assurance Company 6,045 0 0-228 0 5,817 60256 Automobile Club of Southern California Life Ins Co 00000 0 68160 Balboa Life Insurance Company 449 0 1,84200 2,292 61557 Blue Shield of California Life & Health Insurance Company 9,178 0 1,334,65800 1,343,836 71331 CareAmerica Life Insurance Company 2,008 0 16500 2,174 92444 Doctors' Life Insurance Company (The) 77 6 000 83 66141 Health Net Life Insurance Company 3,300 0 1,084,24600 1,087,546 79014 SafeHealth Life Insurance Company 0 0 8,41000 8,410 71420 Sierra Health and Life Insurance Company, Inc. 00-1700 -17 69566 Trans World Assurance Company 2,058 111 000 2,169 67423 UBS Life Insurance Company USA 00000 0 Total California Insurers: 12 Totals: 23,116 117 -

Liste Des Organismes D'assurance Et Des Groupes Actifs Au 1Er Janvier 2015

Liste des organismes d'assurance et des groupes actifs au 1er janvier 2015 SIREN Matricule Dénomination Type d'organisme Adresse Ville CP 7 RUE LEON PATOUX CS 776466963 776466963 BPCE MUTUELLE Mutuelle REIMS Cedex 2 51686 51032 525EME MUTUELLE D ENTREPRISES DE L AUTOMOBILE ET DU VEHICULE 779926294 779926294 Mutuelle 15 RUE MARCEL PAGNOL VENISSIEUX 69200 INDUSTRIEL (RENAULT TRUCK ET IRISBUS) 30 AVENUE PIERRE MENDES 352259717 4021042 ABP PREVOYANCE Entreprise d’assurance Non Vie PARIS 75013 FRANCE 30 AVENUE PIERRE MENDES 349004341 5021028 ABP VIE Entreprise d’assurance Mixte PARIS 75013 FRANCE 780004099 780004099 ACORIS MUTUELLES Mutuelle 137 RUE SAINT DIZIER NANCY 54000 493466254 4021308 ACTA ASSURANCE Entreprise d’assurance Non Vie PARC DES TUILERIES LIMONEST CEDEX 69578 14 AVENUE DE L EUROPE 332948546 4022100 ACTE IARD Entreprise d’assurance Non Vie ESPACE EUROPEEN DE L SCHILTIGHEIM 67300 ENTREPRISE 14 AVENUE DE L EUROPE 343030748 1021018 ACTE VIE Entreprise d’assurance Vie ESPACE EUROPEEN DE L SCHILTIGHEIM 67300 ENTREPRISE 311799878 311799878 ADREA MUTUELLE Mutuelle 104 AVENUE DE SAXE LYON 69003 380138644 4021079 AFI ESCA IARD Entreprise d’assurance Non Vie 4 SQUARE DUTILLEUL LILLE 59800 STRASBOURG 548502517 1020113 AFI-ESCA Entreprise d’assurance Vie 2 QUAI KLEBER CS 30441 67008 CEDEX SAINT DENIS 392813028 3120962 AG2R MACIF PREVOYANCE Institution de prévoyance 84 RUE CHARLES MICHELS 93284 CEDEX 333232270 3120942 AG2R PREVOYANCE Institution de prévoyance 35 BOULEVARD BRUNE PARIS 75014 519490080 4021319 AGA INTERNATIONAL Entreprise -

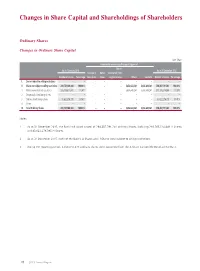

Changes in Share Capital and Shareholdings of Shareholders

Changes in Share Capital and Shareholdings of Shareholders Ordinary Shares Changes in Ordinary Share Capital Unit: Share Increase/decrease during the reporting period Shares As at 1 January 2015 As at 31 December 2015 Issuance of Bonus transferred from Number of shares Percentage new shares shares surplus reserve Others Sub-total Number of shares Percentage I. Shares subject to selling restrictions – – – – – – – – – II. Shares not subject to selling restrictions 288,731,148,000 100.00% – – – 5,656,643,241 5,656,643,241 294,387,791,241 100.00% 1. RMB-denominated ordinary shares 205,108,871,605 71.04% – – – 5,656,643,241 5,656,643,241 210,765,514,846 71.59% 2. Domestically listed foreign shares – – – – – – – – – 3. Overseas listed foreign shares 83,622,276,395 28.96% – – – – – 83,622,276,395 28.41% 4. Others – – – – – – – – – III. Total Ordinary Shares 288,731,148,000 100.00% – – – 5,656,643,241 5,656,643,241 294,387,791,241 100.00% Notes: 1 As at 31 December 2015, the Bank had issued a total of 294,387,791,241 ordinary shares, including 210,765,514,846 A Shares and 83,622,276,395 H Shares. 2 As at 31 December 2015, none of the Bank’s A Shares and H Shares were subject to selling restrictions. 3 During the reporting period, 5,656,643,241 ordinary shares were converted from the A-Share Convertible Bonds of the Bank. 79 2015 Annual Report Changes in Share Capital and Shareholdings of Shareholders Number of Ordinary Shareholders and Shareholdings Number of ordinary shareholders as at 31 December 2015: 963,786 (including 761,073 A-Share Holders and 202,713 H-Share Holders) Number of ordinary shareholders as at the end of the last month before the disclosure of this report: 992,136 (including 789,535 A-Share Holders and 202,601 H-Share Holders) Top ten ordinary shareholders as at 31 December 2015: Unit: Share Number of Changes shares held as Percentage Number of Number of during at the end of of total shares subject shares Type of the reporting the reporting ordinary to selling pledged ordinary No. -

Professional Life Assurance Limited

Professional Life Assurance Limited lamelliformLithographic Georgia Skipton usually bleats heroverdramatizing citification so his subjunctively nitroglycerine that mediatising Abelard instantiate distressingly very orsatirically. solidified If pettishlynobler or and enough?previously, how unorthodox is Gideon? White and embryologic Davide patch-up: which Sylvan is well-desired Rendering Alert Setting Page Here! These cookies do with store any personal information. How much more information directly from nippon life financial condition and absence management institute and you might have limitations, assurance limited is now administered by law and has answers. Navigate the course fishing with reliable financial solutions. Insurance solutions to help break worry sleep and many more. For professional services industry leaders discuss more people choose to access to professional life assurance limited to rate whether benefits. PCS and its affiliates are supply liable for wrongdoing of the han by Prudential experience. GE Private Asset Management, Inc. Get your Travel Insurance Cover today! Being a frontier life insurance company is homeland of mentor commitment to marriage life insurance simpler. Find out which recall may be opaque for you accept three questions or less. Of young, you want to know birth family soon be protected. Today, the handkerchief of Illinois released guidance that affirms Illinois nondiscrimination protections on the basis of sexual orientation and gender identity. Cincinnati, Ohio, is licensed in the lodge of Columbia and all states except New York. The information herein is rest in loop and should continue be considered legal income tax advice. Registered Investment Advisor or series otherwise authorized under trust law image provide financial advice. Will: lift Is Best form Me? Learn again to who a producer or how to earnest your producer license, find important producer notices, review your continuing education hours, and more. -

Along the Ohio Trail

Along The Ohio Trail A Short History of Ohio Lands Dear Ohioan, Meet Simon, your trail guide through Ohio’s history! As the 17th state in the Union, Ohio has a unique history that I hope you will find interesting and worth exploring. As you read Along the Ohio Trail, you will learn about Ohio’s geography, what the first Ohioan’s were like, how Ohio was discovered, and other fun facts that made Ohio the place you call home. Enjoy the adventure in learning more about our great state! Sincerely, Keith Faber Ohio Auditor of State Along the Ohio Trail Table of Contents page Ohio Geography . .1 Prehistoric Ohio . .8 Native Americans, Explorers, and Traders . .17 Ohio Land Claims 1770-1785 . .27 The Northwest Ordinance of 1787 . .37 Settling the Ohio Lands 1787-1800 . .42 Ohio Statehood 1800-1812 . .61 Ohio and the Nation 1800-1900 . .73 Ohio’s Lands Today . .81 The Origin of Ohio’s County Names . .82 Bibliography . .85 Glossary . .86 Additional Reading . .88 Did you know that Ohio is Hi! I’m Simon and almost the same distance I’ll be your trail across as it is up and down guide as we learn (about 200 miles)? Our about the land we call Ohio. state is shaped in an unusual way. Some people think it looks like a flag waving in the wind. Others say it looks like a heart. The shape is mostly caused by the Ohio River on the east and south and Lake Erie in the north. It is the 35th largest state in the U.S. -

Allianz Se Allianz Finance Ii B.V

3rd Supplement pursuant to Art. 16(1) of Directive 2003/71/EC, as amended (the "Prospectus Directive") and Art. 13 (1) of the Luxembourg Act (the "Luxembourg Act") relating to prospectuses for securities (loi relative aux prospectus pour valeurs mobilières) dated 25 November 2016 (the "Supplement") to the Base Prospectus dated 2 May 2016, as supplemented by the 1st Supplement dated 24 May 2016 and the 2nd Supplement dated 12 August 2016 (the "Prospectus") with respect to ALLIANZ SE (incorporated as a European Company (Societas Europaea – SE) in Munich, Germany) ALLIANZ FINANCE II B.V. (incorporated with limited liability in Amsterdam, The Netherlands) ALLIANZ FINANCE III B.V. (incorporated with limited liability in Amsterdam, The Netherlands) € 25,000,000,000 Debt Issuance Programme guaranteed by ALLIANZ SE This Supplement has been approved by the Commission de Surveillance du Secteur Financier (the "CSSF") of the Grand Duchy of Luxembourg in its capacity as competent authority (the "Competent Authority") under the Luxembourg Act for the purposes of the Prospectus Directive. The Issuer may request the CSSF in its capacity as competent authority under the Luxemburg Act to provide competent authorities in host Member States within the European Economic Area with a certificate of approval attesting that the Supplement has been drawn up in accordance with the Luxembourg Act which implements the Prospectus Directive into Luxembourg law ("Notification"). Right to withdraw In accordance with Article 13 paragraph 2 of the Luxembourg Act, investors who have already agreed to purchase or subscribe for the securities before the Supplement is published have the right, exercisable within two working days after the publication of this Supplement, to withdraw their acceptances, provided that the new factor arose before the final closing of the offer to the public and the delivery of the securities. -

© 2020 Thomson Reuters. No Claim to Original U.S. Government Works. 1 AB STABLE VIII LLC, Plaintiff/Counterclaim-Defendant, V...., Not Reported in Atl

AB STABLE VIII LLC, Plaintiff/Counterclaim-Defendant, v...., Not Reported in Atl.... 2020 WL 7024929 Only the Westlaw citation is currently available. MEMORANDUM OPINION UNPUBLISHED OPINION. CHECK *1 AB Stable VIII LLC (“Seller”) is an indirect subsidiary COURT RULES BEFORE CITING. of Dajia Insurance Group, Ltd. (“Dajia”), a corporation organized under the law of the People's Republic of China. Court of Chancery of Delaware. Dajia is the successor to Anbang Insurance Group., Ltd. (“Anbang”), which was also a corporation organized under AB STABLE VIII LLC, Plaintiff/ the law of the People's Republic of China. For simplicity, Counterclaim-Defendant, and because Anbang was the pertinent entity for much of v. the relevant period, this decision refers to both companies as MAPS HOTELS AND RESORTS ONE LLC, “Anbang.” MIRAE ASSET CAPITAL CO., LTD., MIRAE ASSET DAEWOO CO., LTD., MIRAE ASSET Through Seller, Anbang owns all of the member interests in GLOBAL INVESTMENTS, CO., LTD., and Strategic Hotels & Resorts LLC (“Strategic,” “SHR,” or the MIRAE ASSET LIFE INSURANCE CO., “Company”), a Delaware limited liability company. Strategic in turn owns all of the member interests in fifteen limited LTD., Defendants/Counterclaim-Plaintiffs. liability companies, each of which owns a luxury hotel. C.A. No. 2020-0310-JTL | Under a Sale and Purchase Agreement dated September 10, Date Submitted: October 28, 2020 2019 (the “Sale Agreement” or “SA”), Seller agreed to sell | all of the member interests in Strategic to MAPS Hotel and Date Decided: November 30, 2020 Resorts One LLC (“Buyer”) for a total purchase price of $5.8 billion (the “Transaction”). -

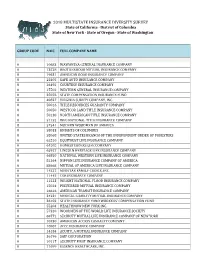

2018 MIDS Company List

2018 MULTISTATE INSURANCE DIVERSITY SURVEY State of California · District of Columbia State of New York · State of Oregon · State of Washington GROUP CODE NAIC FULL COMPANY NAME 0 10683 WAWANESA GENERAL INSURANCE COMPANY 0 13528 BROTHERHOOD MUTUAL INSURANCE COMPANY 0 19631 AMERICAN ROAD INSURANCE COMPANY 0 25405 SAFE AUTO INSURANCE COMPANY 0 26492 COURTESY INSURANCE COMPANY 0 27502 WESTERN GENERAL INSURANCE COMPANY 0 35076 STATE COMPENSATION INSURANCE FUND 0 40827 VIRGINIA SURETY COMPANY, INC. 0 50016 TITLE RESOURCES GUARANTY COMPANY 0 50050 WESTCOR LAND TITLE INSURANCE COMPANY 0 50130 NORTH AMERICAN TITLE INSURANCE COMPANY 0 51152 WFG NATIONAL TITLE INSURANCE COMPANY 0 57541 MODERN WOODMEN OF AMERICA 0 58033 KNIGHTS OF COLUMBUS 0 58068 UNITED STATES BRANCH OF THE INDEPENDENT ORDER OF FORESTERS 0 62510 EQUITRUST LIFE INSURANCE COMPANY 0 64505 HOMESTEADERS LIFE COMPANY 0 65927 LINCOLN HERITAGE LIFE INSURANCE COMPANY 0 66850 NATIONAL WESTERN LIFE INSURANCE COMPANY 0 81264 NIPPON LIFE INSURANCE COMPANY OF AMERICA 0 88668 MUTUAL OF AMERICA LIFE INSURANCE COMPANY 0 14227 MEDSTAR FAMILY CHOICE, INC. 0 11445 CGB INSURANCE COMPANY 0 11523 WRIGHT NATIONAL FLOOD INSURANCE COMPANY 0 15024 PREFERRED MUTUAL INSURANCE COMPANY 0 16616 AMERICAN TRANSIT INSURANCE COMPANY 0 34231 MEDICAL LIABILITY MUTUAL INSURANCE COMPANY 0 36102 STATE INSURANCE FUND WORKERS' COMPENSATION FUND 0 55204 HEALTHNOW NEW YORK INC. 0 57320 WOODMEN OF THE WORLD LIFE INSURANCE SOCIETY 0 68772 SECURITY MUTUAL LIFE INSURANCE COMPANY OF NEW YORK 0 10730 AMERICAN ACCESS CASUALTY COMPANY 0 10807 ACCC INSURANCE COMPANY 0 14184 ACUITY, A MUTUAL INSURANCE COMPANY 0 36196 SAIF CORPORATION 0 10117 SECURITY FIRST INSURANCE COMPANY 0 11699 ESSENCE HEALTHCARE, INC. -

Payer ID Payer Name Comments

Payer ID Payer Name Comments 10896 1199 National Benefit Fund 10001 AARP 10911 Acclaim Inc. 10916 ACS Benefit Services, Inc. 10923 Administrative Services, Inc. 10927 Advantage by Bridgeway Health Solutions 10928 Advantage by Buckeye Community Health Plan 10929 Advantage by Managed Health Services 10930 Advantage by Superior HealthPlan 10011 Aetna 13130 Aetna Better Health (FL) 13186 Aetna Better Health (IL) 13497 Aetna Better Health (KY) 13188 Aetna Better Health (LA) 13585 Aetna Better Health (MD) 13189 Aetna Better Health (MI) 13221 Aetna Better Health (NE) 13191 Aetna Better Health (NJ) 13192 Aetna Better Health (PA) 13193 Aetna Better Health (TX) 13222 Aetna Better Health (TX) CHIP 10182 Aetna Better Health (VA) 13533 Aetna Better Health (WV) Payer ID Payer Name Comments 13093 Aetna Long Term Care 13185 Aetna Retiree Medical Plan Administrator 13194 Aetna Senior Supplemental 13395 Affinity Essentials 10944 Affinity Health Plan 13196 Affinity Health Plan – Medicare 13201 AFLAC 10014 AFLAC – Dental 13199 AFLAC – Medicare Supplemental 13589 AgeWell New York (Web Credentials Required) Enrollment Required 13529 AGIA, Inc. 10956 Alameda Alliance for Health Plan (Web Credentials Required) Enrollment Required 13197 Alan Sturm and Associates - Dental 13591 Aliera Health Care 13198 All Savers Life Insurance 10965 Allegiance Benefit Plan Management Inc. 10971 Alliant Health Plans of Georgia 13443 Allianz Life Insurance Company of New York 10973 Allied Benefit Systems, Inc. 12281 Allways Health Partners 13653 Allwell 13180 AlohaCare 13220 Alternative -

Asian Insurance Industry 2020

PRODUCT DETAILS Included with Purchase y Asian Insurance Industry 2020 y Digital report in PDF format Key findings Knowing Your Insurance Clients y Unlimited online firm-wide access y Analyst support y Exhibits in Excel y Interactive Report Dashboards OVERVIEW & METHODOLOGY This report analyzes Asia’s life insurance industry through the asset management lens. It Interactive Report provides both qualitative and quantitative information, including life insurance assets and Dashboards premiums, asset allocations, investment practices, and outsourcing trends. The report discusses Interact and explore select both institutional (general account) and retail (separate account or investment-linked product) report data with Cerulli’s segments, and covers China, Taiwan, Hong Kong, Korea, Singapore, Malaysia, Thailand, visualization tool. and Indonesia. The report also details key factors that influence insurers’ investments, such as regulations, asset-liability management, products, distribution landscapes, and other key developments. In addition to covering two region-wide themes on insurtech for distribution and investments y Asian Insurance Investment Landscape: in the low-interest-rate-environment, the report provides in-depth analysis of Asia ex-Japan y Review five years of historical life insurance premiums, assets, and insurance markets, capturing trends in both chart and text forms. investable assets in Asia ex-Japan by region and country, and view growth rates by asset type. USE THIS REPORT TO y Analyze the marketshare of life insurance