Royal Bank of Canada Investor Presentation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Promoting Canada's Economic and Financial Well-Being

Bank of Canada: Promoting Canada’s Economic and Financial Well-Being Remarks to the Greater Sudbury Chamber of Commerce Sudbury, Ontario 10 February 2014 John Murray Deputy Governor Bank of Canada Table of Contents . Bank of Canada’s mandate . Four main activities . Economic outlook . Introduction of Bank of Canada Regional Directors and representatives 2 Mandate 3 Mandate The Bank of Canada’s mandate is to contribute to the economic and financial well-being of Canadians We do this by: . aiming to keep inflation low, stable, and predictable . promoting a stable and efficient financial system . supplying secure, quality bank notes . providing banking services to the federal government and key financial system players 4 The Bank’s approach In each of these four core areas, we follow the same consistent approach: . a clear objective . accountability and transparency . a longer-term perspective 5 Key responsibilities: Monetary policy Our objective: To foster confidence in the value of money by keeping inflation at or near the 2 per cent inflation target This is important because: . it allows consumers, businesses, and investors to read price signals clearly, and to make financial decisions with confidence . it reduces the inequity associated with arbitrary redistributions of income caused by unexpected changes in inflation . it also makes the economy more resilient to shocks and enhances the effectiveness of monetary policy 6 Monetary policy: Low and stable inflation 12-month rate of increase, monthly data % 14 12 10 8 6 4 2 0 -2 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 Inflation target CPI Sources: Statistics Canada and Bank of Canada calculations Last observation: December 2013 7 Central bank policy rates dropped to historic lows during the recession Policy interest rates, daily data % 5.0 4.0 3.0 2.0 1.0 0.0 2008 2009 2010 2011 2012 2013 2014 Canada United States Euro area Japan Sources: Bank of Canada, U.S. -

WHY DID the BANK of in Financial Markets and Monetary Economics

NBER WORKING PAPER SERIES WHY DIDTHEBANK OF CANADA EMERGE IN 1935? Michael Bordo Angela Redish Working Paper No. 2079 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 November 1986 The research reported here is part of the NBER's research program in Financial Markets and Monetary Economics. Any opinions expressed are those of the authors and not those of the National Bureau of Economic Research. NBER Working Paper #2079 November 1986 Why Did the Bank of Canada Emerge in 1935? ABSTRACT Three possible explanations for the emergence of the Canadian central bank in 1935 are examined: that it reflected the need of competitive banking systems for a lender of the last resort; that it was necessary to anchor the unregulated Canadian monetary system after the abandonment of the gold standard in 1929; and that it was a response to political rather than purely economic pressures. Evidence from a variety of sources (contemporary statements to a Royal Comission, the correspondence of chartered bankers, newspaper reports, academic writings and the estimation of time series econometric models) rejects the first two hypotheses and supports the third. Michael D. Bordo Angela Redish Department of Economics Department of Economics College of Business Administration University of British Columbia University of South CArolina Vancouver, B.C. V6T lY2 Columbia, SC 29208 Canada Why Did the Bank of Canada Emeroe in 1935? Michael D. Bordo and Angela Redish Three possible explanations for the emergence of the Canadian central bank in 1935 are examined: that it reflected the need of competitive banking systems for a lender of last resort; that it was necessary to anchor the unregulated Canadian monetary system after the abandonment of the gold standard in 1929; and that it was a response to political rather than purely economic pressures. -

The National Bank of Canada Accelerates Deployments at Scale

The National Bank of Canada Accelerates Deployments at Scale About National Bank Executive Summary of Canada The National Bank of Canada (NBC), the country’s sixth-largest commercial bank, set out to transform its infrastructure for speed and scale. NBC’s ultimate goal was to dedicate more of the organization’s time and resources to business innovation instead of infrastructure management. By shifting away from an on-premises installation of its core trading solution, Murex’s MX.3 platform, the bank was able to provision new instances in minutes instead of months and gain better visibility into costs. NBC now runs its non-production MX.3 environments exclusively on Amazon EC2 instances. A Commercial Bank Seeks an Easier-to-Manage Solution The National Bank of Canada (NBC), one of Canada’s largest financial services organizations, wanted to optimize its existing on-premises installation of MX.3, an open platform from Murex that supports trading, treasury, risk, and post-trade operations. The National Bank of Canada Across the numerous projects in parallel, MX.3 ran on more than 100 servers in the bank’s own data center. NBC spent significant time and resources managing and upgrading this (NBC) is the sixth-largest on-premises infrastructure, making deployments of new installations a complex, nearly commercial bank in Canada, impossible process. “We wanted to scale the infrastructure to provision environments to with 2.4 million customers meet growing business needs. The business continued to enhance MX.3 and create new and branches in most projects, but it typically took weeks or months to order, procure, and implement new Canadian provinces. -

64 Canadian Banks and Their Branches

64 Canadian Banks and their Branches. Location. Bank. Manager or Agent. Halifax People's Bank of Halifax, head office . Peter Jack, cashr. Bank of British North America Jeffry Penfold. Bank of Montreal F. Gundry. Hamilton . Canadian Bank of Commerce John C. Kemp. Bank of Hamilton H.C. HammondjCshr. Bank of Montreal T. R. Christian. Merchants'Bank of Canada A. M. Crombie. Bank of British North America Thomas Corsan. Consolidated Bank of Canada J. M. Burns. Exchange Bank of Canada C. M. Counsell. Ingersoll., The Molsons Bank W. Dempster. Merchants' Bank of Canada D. Miller. Imperial C. S. Hoare. Joliette . Hochelaga Bank N. Boire. Exchange Bank of Canada R. Terroux, jnr. Kingston . Bank of British North America G. Durnford. Bank of Montreal K. M. Moore. Merchants' Bank of Canada D. Fraser. Kincardine Merchants' Bank of Canada T. B. P. Trew. Kentville, N. S.. Bank of Nova Scotia L. O. V. Chipman. Liverpool, N. S.. Bank of Liverpool R, S. Sternes, cshr. Lockport People's Bank of Halifax Austin Locke. Lunenburg Merchants' Bank of Halifax Austin Locke. Listowell Hamilton Bank W. Corbould Levis Merchants' Bank I. Wells. London Merchants'Bank of Canada W. F. Harper. Bank of Montreal F. A. Despard. Canadian Bank of Commerce H. W. Smylie. Bank of British North America Oswald Weir. The Molsons Bank. Joseph Jeffrey. Federal Bank of Canada Charles Murray. Standard Bank A. H. Ireland. Lindsay. Bankol Montreal , C. M. Porteous. Ontario Bank S. A. McMurtry. Lucan Canada Bank of Commerce J. E. Thomas. Maitland, N. S. Merchants' Bank of Halifax David Frieze. Markliam Standard Bank F. -

Money and Monetary Policy in Canada

MONEY AND MONETARY POLICY IN CANADA MODULE 8: EXCHANGE RATES . “Money and Monetary Policy In Canada” by Gary Rabbior A publication of the Canadian Foundation for Economic Education Supported by the Bank of Canada Telephone 1-888-570-7610 110 Eglinton Ave. W. Suite 201 www.cfee.org Fax 416-968-0488 Toronto, ON, M4R 1A3 [email protected] TABLE OF CONTENTS Contents 8.1 The International Exchange of Currencies ______________________________________ 1 8.2 The Exchange Rate _______________________________________________________ 3 8.3 Canada's Economy—Relatively Open and Relatively Small ________________________ 6 8.4 Who Buys and Sells Canadian Dollars? ______________________________________ 10 8.5 Factors Influencing the Buying and Selling of Our Dollar __________________________ 12 8.6 Should One Canadian Dollar Equal One U.S. Dollar? ____________________________ 19 8.7 The Bank of Canada and the Exchange Rate __________________________________ 21 8.8 Fixed Versus Flexible Exchange Rates _______________________________________ 22 Pg. 01 8.1 THE INTERNATIONAL EXCHANGE OF CURRENCIES 8.1 THE INTERNATIONAL EXCHANGE OF CURRENCIES The Value of Our Money Is Important to Canadians Canadians have a keen interest in the value and purchasing power of their money. Its value affects our ability to buy goods and services produced here at home. Canadians also buy goods and services from other countries. They don’t usually buy them directly from foreign producers—although that is becoming much more common with online shopping. But they do buy imported goods from retailers in Canada who bought them from foreign producers. Either way, Canadians spend a lot of money on imported goods and services. Economic Why Do Canadians Buy Goods and Services Produced in Insight: why Other Countries? Canadians buy There are various reasons why Canadians buy goods and services produced in other countries, such as: goods and services from • Some goods—for example, bananas—are simply not produced here in Canada. -

Directors As of October 31, 1997

directors as of October 31, 1997 Directors JOHN E. CLEGHORN, F.C.A. L.YVES FORTIER, C.C., Q.C. GUY SAINT-PIERRE,O.C. (1990) April 1995, was President of McCain (1987) (1992) Montreal Foods Limited, Mr. David P.O’Brien Toronto Montreal Chairman of the Board who, prior to May 1996, was President Chairman and Chairman SNC-Lavalin Group Inc. and Chief Operating Officer of Canadian Pacific Limited, prior to February 1995, Chief Executive Officer Ogilvy Renault ROBERT T.STEWART (1988) was Chairman and Chief Executive Royal Bank of Canada THE HON. PAULE GAUTHIER, Vancouver Officer of Pan Canadian Petroleum Limited and prior to December 1994 THEODORE M.ALLEN (1992) P.C., O.C., Q.C. (1991) Company Director was Chairman, President and Chief Winnipeg Quebec City ALLAN R.TAYLOR, O.C. (1983) Executive Officer of Pan Canadian President and Partner Toronto Petroleum Limited, Mr. Robert B. Chairman of the Board Desjardins Ducharme Stein Retired Chairman and Peterson who, prior to July 1994, was United Grain Growers Limited Monast Chairman and Chief Executive Officer Chief Executive Officer and prior to September 1992 was * SIR JAMES BALL (1990) * CHARLES H. KNIGHT (1983) Royal Bank of Canada President and Chief Operating Officer London, England Regina of Imperial Oil Limited, Mr. Hartley T. JOHN A.TORY,Q.C. (1971) Emeritus Professor Chief Executive Officer Richardson who, prior to April 1993, Toronto London Business School Denro Holdings Ltd. was President of the Real Estate Division Deputy Chairman of James Richardson & Sons, Limited, JACQUES BOUGIE, O.C. (1991) * THE HON. E. PETER The Thomson Corporation Mr. -

Statement of the Government of Canada and the Bank of Canada on Monetary Policy Objectives

fiirnli1 ..t....1R,J, B.ANK OF CANADA FOR IMMEDIATE RELEASE CONTACf: Ottawa, 22 December 1993 Guy Theriault (613) 782-8899 The Boani of DiItttors of the Bank of Canada announced today that, p=uant to Section 6 of the Bank of Canada Act, it has appointed Gotdon G. Thiessen as Governor of the Bank of Canada for a seven year term. effective February 1st, 1994. He succeeds John W. Crow, who will have completed his term as Governor. Mr. Crow has indicated that he was not a candidate for a second term. Mr. lbiessen has been Senior Deputy Governor and a member of the Board of Directors and Executive Committee since 27 October 1987. Mr. Thiessen was born in 1938 and grew up in a number of small towns in Saskatchewan. After graduating from high school in Moosomin, Saskatchewan, he worked in a chanered bank in that province. He studied economics at the University of Saskatchewan, graduating with an Honours B.A. in 1960 and an M.A. in 1961, and then attended the London School of Economics during 1965-67 and received a Ph.D. in Economics in 1972. Mr. Thiessen joined the Research Deparonent of the Bank. of Canada in 1963. He has spent most of his career at the Bank. except for a period in 1965-67 when he was in London to complete his Ph.D. and a period in 1973-75 which he spent as a visiting economist at the Reserve Bank: of Australia. Mr. Thiessen worked. in the Research and Monetary and Financial Analysis Departments of the Bank until he was appointed Adviser to the Governor in 1979. -

Brief History of the Canadian Dollar

BRIEF HISTORY OF THE CANADIAN DOLLAR This summary provides a perspective of the modern-day history of Canadian-US dollar exchange rate fl uctuations, recognizing the recent decline in the Canadian dollar. Chart 1 shows the level of exchange rates from 1953 to January 2016. Chart 1— History of Canadian-US Exchange Rates 1.1 1.0 0.9 r Canadian Dollar 0.8 0.7 U.S. Dollars pe Dollars U.S. 0.6 1953 1958 1962 1966 1971 1975 1980 1984 1988 1993 1997 2002 2006 2011 2015 Date Source: Bank of Canada The Canadian dollar spent much of 1953 to 1960 in the $1.02 to $1.06 (US) range. It topped out 1953 - at $1.0614 (US) on August 20, 1957. Until 2007 this was considered the modern-day peak for 1960 the Canadian dollar versus the US currency. The Canadian dollar was at $2.78 (US) in 1864 during the US Civil War, but in those days it was pegged to the gold standard, a practice the US had already abandoned. In the early 1960s, the Bank of Canada governor James Coyne and Prime Minister John Diefenbaker 1961 - were on diff erent economic paths. The government wanted expansion while Coyne wanted to 1969 maintain a tight money supply. Coyne subsequently resigned and in May 1962, the government pegged the Canadian dollar at 92.5 cents (US) plus or minus a 1% band. 1970 - In May 1970, with rising infl ation and serious wage pressures, the Trudeau government allowed the 1972 Canadian dollar to fl oat. -

Take a Central Role #Boconcampus

Take a Central Role #BoConcampus bankofcanada.ca/careers Approx. 1,700 employees across Canada 90 per cent are based in Ottawa VANCOUVER CALGARY COS MONTREAL HALIFAX COS = Calgary Operational Site OTTAWA Head Office in Ottawa Regional Offices TORONTO NEW YORK bankofcanada.ca/careers Governing Council MONETARY FINANCIAL POLICY SYSTEM CORE RESPONSIBILITIES CURRENCY FUNDS MANAGEMENT bankofcanada.ca/careers MONETARY POLICY The objective of monetary policy is to preserve the value of money by keeping inflation low, stable and predictable. Canadian Economic Analysis Department International Economic Analysis Department CORE RESPONSIBILITIES bankofcanada.ca/careers FINANCIAL SYSTEM The Bank promotes safe, sound and efficient financial systems, within Canada and internationally, and conducts transactions in financial markets in support of these objectives Financial Markets Department Financial Stability Department CORE RESPONSIBILITIES bankofcanada.ca/careers CORE RESPONSIBILITIES FUNDS MANAGEMENT The Bank provides funds-management services for the Government of Canada, the Bank itself and other clients. For the government, the Bank provides treasury management services and administers and advises on the public debt and foreign exchange reserves. Funds Management and Banking Department bankofcanada.ca/careers CORE RESPONSIBILITIES CURRENCY The Bank designs, issues and distributes Canada’s bank notes, oversees the note distribution system and ensures a consistent supply of quality bank notes that are readily accepted and secure against counterfeiting. -

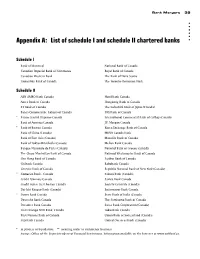

List of Schedule I and Schedule II Chartered Banks

Bank Mergers 39 Appendix A: List of schedule I and schedule II chartered banks Schedule I Bank of Montreal National Bank of Canada Canadian Imperial Bank of Commerce Royal Bank of Canada Canadian Western Bank The Bank of Nova Scotia Laurentian Bank of Canada The Toronto-Dominion Bank Schedule II ABN AMRO Bank Canada Hanil Bank Canada Amex Bank of Canada Hongkong Bank of Canada BT Bank of Canada The Industrial Bank of Japan (Canada) Banca Commerciale Italiana of Canada ING Bank of Canada * Banco Central Hispano-Canada International Commercial Bank of Cathay (Canada) Bank of America Canada J.P. Morgan Canada * Bank of Boston Canada Korea Exchange Bank of Canada Bank of China (Canada) MBNA Canada Bank Bank of East Asia (Canada) Manulife Bank of Canada Bank of Tokyo-Mitsubishi (Canada) Mellon Bank Canada Banque Nationale de Paris (Canada) National Bank of Greece (Canada) The Chase Manhattan Bank of Canada National Westminster Bank of Canada Cho Hung Bank of Canada Paribas Bank of Canada Citibank Canada Rabobank Canada Citizens Bank of Canada Republic National Bank of New York (Canada) ** Comerica Bank - Canada Sakura Bank (Canada) Crédit Lyonnais Canada Sanwa Bank Canada Credit Suisse First Boston Canada Société Générale (Canada) Dai-Ichi Kangyo Bank (Canada) Sottomayor Bank Canada * Daiwa Bank Canada State Bank of India (Canada) Deutsche Bank Canada The Sumitomo Bank of Canada Dresdner Bank Canada Swiss Bank Corporation (Canada) First Chicago NBD Bank, Canada Tokai Bank Canada First Nations Bank of Canada Union Bank of Switzerland (Canada) Fuji Bank Canada United Overseas Bank (Canada) * in process of liquidation; ** awaiting order to commence business Source: Office of the Superintendent of Financial Institutions. -

Royal Bank of Canada (Channel Islands) Limited

HNW_NRG_A_Bleed_Mask Royal Bank of Canada (Channel Islands) Limited General Terms and Conditions Effective date: 25 May 2018 Wealth Management Wealth Management | 2 Contents 1. Definitions and Interpretation 3 2. Introduction 4 3. General Information 4 4. The Account 6 5. Joint Accounts 9 6. Instructions 10 7. FX Transactions 12 8. Issue of Visa Debit Cards by The Bank 12 9. Issue of Credit/Charge Cards by Parties Other than The Bank 14 10. Client Representations and Warranties 14 11. Client Acknowledgements 15 12. Not Used 16 13. Confidentiality 16 14. Notices and Other Communication 16 15. Complaints 17 16. Severability 17 17. General 17 18. Exclusion of Supply of Goods and Services (Jersey) Law 2009 17 19. Force Majeure 17 20. Governing Law and Jurisdiction 18 21. Commissions 18 22. Investment Services 18 23-26. Additional Terms and Conditions Relating to Custodial Services 23 23. Custodial Services 23 24. Custodial Service (Miscellaneous) 24 25. Notices issued under the Companies Act of the United Kingdom and Analogous Legislation of Other Jurisdictions 27 26. Termination 27 27. Assignment 28 Wealth Management | 3 Terms and Conditions payments to third parties that are not directly related to the purchase of securities or any 1. Definitions and Interpretation other assets that are eligible to be held in 1.1 In these Terms, unless the context otherwise a Custody Account and such account is not requires: subject to the bare trust which otherwise applies to Property held under the Custodial Service); “Account” means any or all accounts -

Monetary Policy Report July 2020 Canada’S Infl Ation-Control Strategy1

Monetary Policy Report July 2020 Canada’s Infl ation-Control Strategy1 pre-set days during the year, and full updates of the Bank’s Infl ation targeting and the economy outlook, including risks to the projection, are published four . The Bank’s mandate is to conduct monetary policy to promote times per year in the Monetary Policy Report. the economic and nancial well-being of Canadians. Canada’s experience with in ation targeting since 1991 has shown that the best way to foster con dence in the value Infl ation targeting is symmetric and fl exible of money and to contribute to sustained economic growth, . Canada’s in ation-targeting approach is symmetric, which employment gains and improved living standards is by keeping means that the Bank is equally concerned about in ation rising in ation low, stable and predictable. above or falling below the 2 percent target. In 2016, the Government and the Bank of Canada renewed . Canada’s in ation-targeting framework is exible. Typically, Canada’s in ation-control target for a further ve-year period, the Bank seeks to return in ation to target over a horizon of six ending December 31, 2021. The target, as measured by the to eight quarters. However, the most appropriate horizon for consumer price index (CPI), remains at the 2 percent midpoint returning in ation to target will vary depending on the nature of the control range of 1 to 3 percent. and persistence of the shocks buffeting the economy. The monetary policy instrument Monitoring infl ation . The Bank carries out monetary policy through changes in the .