1285-Supermarket.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Confectionery Snack World!

MANIA SpA Legal + Operational Headquarters: Via Gambulaga Masi 111/A 44015 Gambulaga di Portomaggiore (FERRARA) - Italy WILL YOU TRUST US Ph. +39 0532 812092 [email protected] [email protected] WITH YOUR CASE? www.caramellamania.it V.A.T. IT 01806010383 SELF-DECLARED SHERLOCK OF THE GOURMET/ CONFECTIONERY SNACK WORLD! CONSTANTLY ON THE LOOKOUT FOR EXCITING AND INNOVATIVE NEW PRODUCTS TO ADD TO OUR GOURMET OR CONFECTIONERY RANGES! GOURMET CONFECTIONERY • ORGANIC PRODUCTS • SWEETS/CANDIES • SWEET AND SAVOURY SAUCES • SNACK BARS • HEALTHY SNACKS • TRADITIONAL SWEETS • FRUIT SNACKS • CHARACTER CONFECTIONERY • HEALTHY BEVERAGES • UNUSUAL OR INNOVATIVE PRODUCTS • SEASONAL HOLIDAY GIFTS AND CANDY • SNACK POTS/SEED POTS • BISCUITS • CEREAL BARS • BISCUIT BARS OUR BRANDS PARTNER BRANDS In search of the sweeter things in life... UNDER MANIA UMBRELLA CONFECTIONERY GOURMET SUPERMARKETS WEB SALES MAKING LIFE THAT LITTLE BIT SWEETER... Making life that little bit sweeter... EST. 1989 SPECIALIZED IN CONFECTIONERY AND TREATS SINCE 1989, WE LOVE WHAT WE DO AND IT SHINES THROUGH. OUR CORE BUSINESS IS DISTRIBUTING AND RE-PACKING PRODUCE FOR OUR CLIENTS AND OUR CLIENTS LOVE WHAT WE DO TOO. WE CATER FOR ALL HOLIDAYS: FROM CHRISTMAS TO EASTER, FROM HALLOWEEN TO ST. VALENTINES. OR JUST BRINGING SWEETER MOMENTS TO EVERYDAY LIFE... WE SUPPLY TREATS FOR ALL OCCASIONS. www.caramellamania.it TAKING THE TIME TO TAKE LIFE TO ANOTHER LEVEL... Taking the time to take life to another level... GOURMET OUR EMPHASIS AND FOCUS FOR THIS PROJECT IS ON THE ‘FINE FOOD MARKET’, AIMING TO RAISE THE BAR AND INTRODUCE GOOD QUALITY, HIGH-END FOODS FOR ‘TRUE FOODIES’. OUR GOODIES ON YOUR DOORSTEP.. -

Completed Acquisition by Co-Operative Foodstores Limited of Eight My Local Grocery Stores from ML Convenience Limited and MLCG Limited

Completed acquisition by Co-operative Foodstores Limited of eight My Local grocery stores from ML Convenience Limited and MLCG Limited Decision on relevant merger situation and substantial lessening of competition ME/6625/16 The CMA’s decision on reference under section 22(1) of the Enterprise Act 2002 given on 19 October 2016. Full text of the decision published on 10 November 2016. Please note that [] indicates figures or text which have been deleted or replaced in ranges at the request of the parties for reasons of commercial confidentiality. CONTENTS Page SUMMARY ................................................................................................................. 2 ASSESSMENT ........................................................................................................... 3 Parties ................................................................................................................... 3 Transaction ........................................................................................................... 4 Jurisdiction ............................................................................................................ 4 Counterfactual....................................................................................................... 5 Frame of reference ............................................................................................... 7 Competitive assessment ..................................................................................... 11 Third party views ................................................................................................ -

Establishing ROOTS in the German Organic Food Market

establishing ROOTS in the German organic food market 2012 Foreword The organic market is growing worldwide with fast paces. The German market for or-ganic food and beverages was in 2010 the second largest organic market in the world. It is a fast growing market estimated to about 6.59 billion euros in 2011, growing by 9 per cent a year, encompassing 3.7 per cent of the entire Mette Gjerskov (Photo: Rune Johansen) food market in Germany in 2011. This is an opportunity for organic food companies, as it has never been seen before! It is my aspiration that this window of opportunity will be opened by providing high quality Danish organic products for a fast growing organic market. Many Danish companies are already active in the fi eld of foreign trade, participating at international fairs and export promotions. Danish companies have the advantage of a well-established business platform and many are already acting with competence and skill on the German market greatly supported by “Bio aus Dänemark”. 2 The organic sector in Denmark has a very high credibility with a large degree of self-regulation. Our strict state-run control system from farm to fork is not only securing high credibility of the organic products, but also contributing to the safety of food products, since the organic inspection is part of the general food inspection. As a result of this our Danish consumers have a very high confi dence and trust in organic products. Well-established public-private cooperation provides a prolifi c environment for new incentives motivated and supported by the Danish Government. -

Attitudes of Consumers, Retailers and Producers to Farm Animal Welfare

Attitudes of Consumers, Retailers and Producers to Farm Animal Welfare edited by Unni Kjærnes, Mara Miele and Joek Roex WELFARE QUALITY REPORTS NO. 2 This report is dedicated to the memory of Jonathan Murdoch. Welfare Quality Reports Edited by Mara Miele and Joek Roex School of City and Regional Planning Cardiff University Glamorgan Building King Edward VII Avenue Cardiff CF10 3WA Wales UK Tel.: +44(0)292087; fax: +44(0)2920874845; e-mail: [email protected] January 2007 The present study is part of the Welfare Quality research project which has been co- financed by the European Commission, within the 6th Framework Programme, contract No. FOOD-CT-2004-506508. The text represents the authors’ views and does not necessarily represent a position of the Commission who will not be liable for the use made of such information. © Copyright is with the authors of the individual contributions. ISBN 1-902647-73-4 ISSN 1749-5164 CONTENTS Preface iii PART I Farm Animal Welfare and Food Consumption Practices: Results from Surveys in Seven Countries (edited by Unni Kjærnes and Randi Lavik) 1 Introduction to Part I 1 2 Background and Research Questions 3 3 Methods 9 4 People Are Interested but Not Necessarily Worried 11 5 Considerations of Animal Friendliness When Purchasing Food 17 6 Availability Is a Bigger Problem Than Price 21 7 The Truth-telling of Institutional Actors 23 8 Concluding Remarks to Part I 29 PART II Analysis of the Retail Survey of Products that Carry Welfare-claims and of Non-retailer Led Assurance Schemes whose Logos Accompany Welfare-claims (edited by Emma Roe and Terry Marsden) 9 Introduction to Part II 33 10 Comparative Overview of Animal Welfare Claims 35 11 Welfare Bundling on Packaging 45 12 Comparative Analysis of Non-retailer Led Schemes of Production 51 13 Comparative Analysis of Marketing Schemes of Non-retailer Led 59 Assurance Schemes 14 Conclusions to Part II 65 PART III Pig Farmers and Animal Welfare: A Study of Beliefs, Attitudes and Behaviour of Pig Producers across Europe (edited by Bettina B. -

Lebensmittel Marke Produktname Zuckeralternat… Vegan Bioqualität Gibt's Bei

Lebensmittel Marke Produktname Zuckeralternat… Vegan Bioqualität Gibt's bei Tropical Gold Ananas Dole Premium ohne ja nein Edeka (Konserve) Pineapple Ananas Ananas im Alnatura, tegut, Alnatura ohne ja ja (Konserve) eigenen Saft Rossmann Ananas- Dessertstücke Ananas natursüß, Libby's ohne ja nein Real, Rewe, tegut (Konserve) Ananas in Scheiben natursüß Ananas REWE Beste Ananas ohne ja nein Rewe (Konserve) Wahl Desserstücke Ananasringe Ananas dennree oder -stücke im ohne ja ja Bioläden, denn's (Konserve) eigenen Saft Apfelmus Campo Verde Apfelmark ohne ja ja Real, Rewe Apfelmus real Quality Apfelmark ohne ja nein Real Apfelmus enerBIO Apfelmark ohne ja ja Rossmann Alnatura, Müller Apfelmus Alnatura Apfelmark ohne ja ja Drogeriemarkt, Rossmann, tegut Apfelmus dmBio Apfelmark ohne ja ja dm Apfelmus EDEKA Bio Apfelmark ohne ja ja Edeka Apfelmus REWE Bio Apfelmark ohne ja ja Rewe Apfelmus dennree Apfelmark pur ohne ja ja Bioläden, denn's Aprikosen Aprikosen Libby's ohne ja nein Real, Rewe, tegut (Konserve) natursüß Aprikosen Aprikosen halbe dennree Apfelsaftkonze… ja ja Bioläden, denn's (Konserve) Frucht Bananenchips Bananenchips Lihn ohne ja ja Bioläden ungesüßt Cornakes REWE Bio Cornakes ohne ja ja Rewe Cornakes Cornakes dmBio ohne ja ja dm ungesüßt Alnatura, Cornakes Alnavit Bio Cornakes ohne ja ja Bioläden, tegut Alnatura, Müller Cornakes Cornakes Alnatura ohne ja ja Drogeriemarkt, ungesüßt tegut, Rossmann Cranberries Morgenland Cranberries Apfelsaftkonze… ja ja Bioläden Lebensmittel Marke Produktname Zuckeralternat… Vegan Bioqualität Gibt's -

Global Vs. Local-The Hungarian Retail Wars

Journal of Business and Retail Management Research (JBRMR) October 2015 Global Vs. Local-The Hungarian Retail Wars Charles S. Mayer Reza M. Bakhshandeh Central European University, Budapest, Hungary Key Words MNE’s, SME’s, Hungary, FMCG Retailing, Cooperatives, Rivalry Abstract In this paper we explore the impact of the ivasion of large global retailers into the Hungarian FMCG space. As well as giving the historical evolution of the market, we also show a recipe on how the local SME’s can cope with the foreign competition. “If you can’t beat them, at least emulate them well.” 1. Introduction Our research started with a casual observation. There seemed to be too many FMCG (Fast Moving Consumer Goods) stores in Hungary, compared to the population size, and the purchasing power. What was the reason for this proliferation, and what outcomes could be expected from it? Would the winners necessarily be the MNE’s, and the losers the local SME’S? These were the questions that focused our research for this paper. With the opening of the CEE to the West, large multinational retailers moved quickly into the region. This was particularly true for the extended food retailing sector (FMCG’s). Hungary, being very central, and having had good economic relations with the West in the past, was one of the more attractive markets to enter. We will follow the entry of one such multinational, Delhaize (Match), in detail. At the same time, we will note how two independent local chains, CBA and COOP were able to respond to the threat of the invasion of the multinationals. -

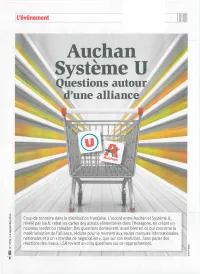

Questions Autour D'une Alliance!^

L'événement 11 Auçhan SystèmQuestions autoue Ur d'une alliance!^ Coup de tonnerre dans la distribution française. L'accord entre Auchan et Système U, révélé par lsa.fr, rebat les cartes des achats alimentaires dans l'Hexagone, en créant un nouveau leader ou coleader. Des questions demeurent, aussi bien en ce qui concerne la matérialisation de l'alliance, réduite pour le moment aux seules marques internationales, nationales et à un «mandat de négociation», que sur son évolution. Sans parler des réactions des rivaux. LSA revient en cinq questions sur ce rapprochement. n L'événement Est-cela naissanced'un nouveau leader ? Par la grâce d'un accord mettant leurs achats en commun via un mandat de négociation confié à la centrale Eurauchan, Serge Papin, patron de Système U, et Vianney Mulliez, président du conseil de ' 1« *' | surveillance d'Auchan, passent en France du statut de challenger à jJ <r> H, H 0 celui de poids lourds de la distribution alimentaire. LES CHIFFRES VENTES CUMULÉES 44,5 Mrds€ (CA TTC avec carburants) 210 hypers, ur le papier, l'addition des chiffres d'affaires comme une concentration, et ne sera pas notifié 1039 supers, d'Auchan et de Système U place le nouvel à l'Autorité de la concurrence. Il n'empêche, leurs 715 proxi Sensemble en position de leader virtuel de la parts de marché cumulées constitueront bien le AUCHAN distribution alimentaire en France. «Système A», véritable poids économique à l'achat des nouveaux 16,8 Mrds€ (-2,6%) comme certains nomment déjà la nouvelle alliance, alliés. Ils détiennent ensemble 21,5 % de part de 139 magasins «pèse» 44,5 Mrds € de chiffre d'affaires TTC avec marché depuis le début de l'année (selon Kantar), SIMPLYMARKET carburants, selon le dernier top 100 de LSA. -

Matas A/S’ Future Operating Results, Financial Position, Cash Flows, Business Strategy and Plans for the Future

“Good advice makes the difference” Happy New Year | SEB Nordic Seminar – Copenhagen 8. January 2014 Forward looking statements This presentation contains statements relating to the future, including statements regarding Matas A/S’ future operating results, financial position, cash flows, business strategy and plans for the future. The statements can be identified by the use of words such as “believes”, “expects”, “estimates”, “projects”, “plans”, “anticipates”, “continues” and “intends” or any variations of such words or other words with similar meaning. The statements are based on management’s reasonable expectations and forecasts at the time of the disclosure of the interim report. Any such statements are subject to risks and uncertainties and a number of different factors, of which many are beyond Matas A/S’ control, can mean that the actual development and the actual result will differ significantly from the expectations contained in the interim report. Without being exhaustive, such factors include general economics and commercial factors, including market and competitive matters, supplier issues and financial issues. 2 Agenda . Introduction to Matas . The Strategic Priorities . Trading Update for Q3 2013/14 3 The Matas share . Listed on NASDAQ OMX 28 June 2013 . 40.8m shares in one share class . Market capitalization DKK 6.0bn (USD ~1bn) . 180 days lock-up for CVC and the former store owners expired 10 December 2013 4 Our Achievements n°1 Health and Beauty n°1 ~1.35 million Retailer in Denmark Beauty and Personal Care Club Matas Members Brand in Denmark 295 98% Stores Across Brand Awareness Among Denmark Women 5 38% StyleBox Stores Market Share in Beauty ~25m 62% Transactions Market Share in High-end in 2012/13 Beauty ~5% DKK 3.2bn Annual Long-Term Revenue in FY 2012/13E Historical Chain Growth 5 Our History . -

In Denemarken

FOOD RETAIL IN DENEMARKEN FLANDERS INVESTMENT & TRADE MARKTSTUDIE FOOD RETAIL IN DENEMARKEN December 2015 Flanders Investment & Trade Gothersgade 103, 2. Sal DK-1123 København K Tel.nr. +45 33 13 04 88 - [email protected] Inhoudstabel 1 Algemene informatie ................................................................................................................ 3 2 Marktinformatie ....................................................................................................................... 3 3 Marktstructuur ......................................................................................................................... 4 3.1 Overzicht marktaandeel van concerns en ketens 2014..................................................... 4 3.2 De belangrijkste spelers................................................................................................. 5 3.3 Overzicht met contactgegevens ..................................................................................... 8 3.4 Overzicht verschillende types warenhuizen in Denemarken ........................................... 10 3.5 Online supermarkten .................................................................................................. 10 4 De kiosken en groothandelaars ................................................................................................ 11 5 Foodservice............................................................................................................................ 13 6 Prijsniveau van voeding en dranken -

Comunicato 2

Esplode l'e-commerce alimentare Comunicato : Il lockdown imposto dal governo per limitare il Covid-19 premia i supermercati online con numeri da capogiro. In seguito all'isolamento necessario per limitare la propagazione del Coronavirus, gli italiani si sono messi prima in coda davanti ai supermercati fisici e poi si sono lanciati sui supermercati online. Numeri incredibili con crescite imprevedibili che portano l'e-commerce dei prodotti alimentari e di largo consumo ad un nuovo livello inaspettato fino a febbraio. La piattaforma per la spesa online locale SpesaRossa, nata per sostenere i piccoli negozianti di paese durante questa crisi epocale, ha condotto uno studio con l'ausilio dei più importanti strumenti di analisi web per capire i tassi di crescita e i vincitori di questa corsa al commercio elettronico alimentare, confrontando la crescita a cavallo dell’inizio dell’epidemia. Secondo lo studio, le piattaforme di supermercati online crescono in modo differente in funzione del traffico dei mesi precedenti. Sul fronte della crescita vince Supermercato24 con un +1.230%, mentre dal punto di vista del numero di visite Esselunga vince con Esselunga.it e Esselungaacasa.it rispettivamente con quasi 9 milioni di visite e 7 milioni di visite. E’ stato analizzato il traffico di utenti, i tempi di permanenza sui siti, le pagine viste e il bounce rate, ossia la frequenza di rimbalzo che consente di valutare l’aspettativa del visitatore. Secondo Ivan Laffranchi, digital entrepreneur e fondatore di SpesaRossa, “il mercato dell’e-commerce alimentare e dei prodotti di consumo, ha raggiunto in 30 giorni un livello di maturità tale per cui cambieranno radicalmente le abitudini dei consumatori. -

The Mixed Brand and Private Label Strategy – Retailer's Perspective

The Mixed Brand and Private Label Strategy – Retailer’s Perspective illustrated by the Rema1000 case Jesper Kolind (WORK IN PROGRESS) Jesper Kolind is ph.d. student at the University of Southern Denmark, Department of Entrepreneurship and Relationship Management, Engstien 1, 6000 Kolding, Denmark E‐mail: [email protected] Page 1 Abstract In this paper, the terms “Focused” and “Mixed” suppliers / retailers are introduced and presented in an interface model. The general thesis is that suppliers and retailers face similar challenges and difficulties strategically and organizationally when they work with a mixed brand and private label strategy (working with both brands and private label in the same organization). Different models have been used with different results and the success/failure is not only a result of the individual approach but moreover of the co‐operation between the two parties. This paper is limited to the retailers perspective and is covered through a literature review in particular about the reasons for retailers to get involved in private label and illustrated by an explorative case study of the discounter Rema1000. Keywords: Retailers, suppliers, private label, interactions, dyads Introduction The last 10 years, I have been directly involved in selling private label products both in a company dominated by branded sales where private label had low priority but also in a private label dominated company where the priorities were opposite. During this period I have often experienced how difficult it is for the suppliers to balance the strategic focus between brands and private label. Likewise, I have experienced that retailers face the same strategic and organizational difficulties when it comes to a mixed strategy involving both brands and private labels. -

Retail Food Sector Retail Foods France

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: 9/13/2012 GAIN Report Number: FR9608 France Retail Foods Retail Food Sector Approved By: Lashonda McLeod Agricultural Attaché Prepared By: Laurent J. Journo Ag Marketing Specialist Report Highlights: In 2011, consumers spent approximately 13 percent of their budget on food and beverage purchases. Approximately 70 percent of household food purchases were made in hyper/supermarkets, and hard discounters. As a result of the economic situation in France, consumers are now paying more attention to prices. This situation is likely to continue in 2012 and 2013. Post: Paris Author Defined: Average exchange rate used in this report, unless otherwise specified: Calendar Year 2009: US Dollar 1 = 0.72 Euros Calendar Year 2010: US Dollar 1 = 0.75 Euros Calendar Year 2011: US Dollar 1 = 0.72 Euros (Source: The Federal Bank of New York and/or the International Monetary Fund) SECTION I. MARKET SUMMARY France’s retail distribution network is diverse and sophisticated. The food retail sector is generally comprised of six types of establishments: hypermarkets, supermarkets, hard discounters, convenience, gourmet centers in department stores, and traditional outlets. (See definition Section C of this report). In 2011, sales within the first five categories represented 75 percent of the country’s retail food market, and traditional outlets, which include neighborhood and specialized food stores, represented 25 percent of the market. In 2011, the overall retail food sales in France were valued at $323.6 billion, a 3 percent increase over 2010, due to price increases.