Federal Register/Vol. 65, No. 15/Monday, January 24, 2000/Rules and Regulations

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2021 7 Day Working Days Calendar

2021 7 Day Working Days Calendar The Working Day Calendar is used to compute the estimated completion date of a contract. To use the calendar, find the start date of the contract, add the working days to the number of the calendar date (a number from 1 to 1000), and subtract 1, find that calculated number in the calendar and that will be the completion date of the contract Date Number of the Calendar Date Friday, January 1, 2021 133 Saturday, January 2, 2021 134 Sunday, January 3, 2021 135 Monday, January 4, 2021 136 Tuesday, January 5, 2021 137 Wednesday, January 6, 2021 138 Thursday, January 7, 2021 139 Friday, January 8, 2021 140 Saturday, January 9, 2021 141 Sunday, January 10, 2021 142 Monday, January 11, 2021 143 Tuesday, January 12, 2021 144 Wednesday, January 13, 2021 145 Thursday, January 14, 2021 146 Friday, January 15, 2021 147 Saturday, January 16, 2021 148 Sunday, January 17, 2021 149 Monday, January 18, 2021 150 Tuesday, January 19, 2021 151 Wednesday, January 20, 2021 152 Thursday, January 21, 2021 153 Friday, January 22, 2021 154 Saturday, January 23, 2021 155 Sunday, January 24, 2021 156 Monday, January 25, 2021 157 Tuesday, January 26, 2021 158 Wednesday, January 27, 2021 159 Thursday, January 28, 2021 160 Friday, January 29, 2021 161 Saturday, January 30, 2021 162 Sunday, January 31, 2021 163 Monday, February 1, 2021 164 Tuesday, February 2, 2021 165 Wednesday, February 3, 2021 166 Thursday, February 4, 2021 167 Date Number of the Calendar Date Friday, February 5, 2021 168 Saturday, February 6, 2021 169 Sunday, February -

Payroll Calendar 2021

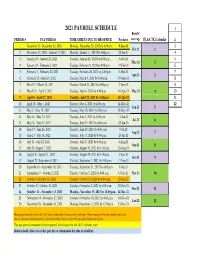

2021 PAYROLL SCHEDULE 1 Benefit PERIOD # PAY PERIOD TIME SHEETS DUE TO HR OFFICE Paydates coverage FLSA 7K Calendar 2 1 December 13- December 26, 2020 Monday, December 28, 2020 by 4:00 p.m. 8-Jan-21 3 Feb-21 1 2 December 27, 2020 - Janurary 9, 2021 Monday, January 11, 2021 by 4:00 p.m. 22-Jan-21 4 3 January 10 - January 23, 2021 Tuesday, January 26, 2021 by 4:00 p.m. 5-Feb-21 5 Mar-21 2 4 January 24 - February 6, 2021 Tuesday, February 9, 2021 by 4:00 p.m. 19-Feb-21 6 5 February 7 - February 20, 2021 Tuesday, February 26, 2021 by 4:00 p.m. 5-Mar-21 7 Apr-21 3 6 February 21 - March 6, 2021 Tuesday, March 9, 2021 by 4:00 p.m. 19-Mar-21 8 7 March 7 - March 20, 2021 Tuesday, March 23, 2021 by 4:00 p.m. 2-Apr-21 9 8 March 21 - April 3, 2021 Tuesday, April 6, 2021 by 4:00 p.m. 16-Apr-21 May-21 4 10 9 April 4 - April 17, 2021 Tuesday, April 20, 2021 by 4:00 p.m. 30-Apr-21 11 10 April 18 - May 1, 2021 Tuesday, May 4, 2021 by 4:00 p.m. 14-May-21 12 Jun-21 5 11 May 2 - May 15, 2021 Tuesday, May 18, 2021 by 4:00 p.m. 28-May-21 12 May 16 - May 29, 2021 Tuesday, June 1, 2021 by 4:00 p.m. 11-Jun-21 Jul-21 6 13 May 30 - June 12, 2021 Tuesday, June 15, 2021 by 4:00 p.m. -

January 24, 2020

JANUARY 24, 2020 UPCOMING o Monday, January 27, 6:30 PM – City Council Meeting – City Hall o Tuesday, January 28, 9:00 AM – Cultural Arts Commission Meeting – City Hall o Tuesday, January 28, 7:00 PM - Malibu Library Speaker Series - Dan Pfeiffer – City Hall (RSVP required) o Wednesday, January 29, 6:00 PM – City Council Special Meeting Addressing Homelessness in Malibu - City Hall o Thursday, January 30, 6:00 PM – Insurance Workshop with CA Insurance Commissioner Lara and Assemblymember Bloom - City Hall MALIBU REBUILDS - DEADLINES The City Council approved several measures to assist fire victims with rebuilding. There are important timelines to pay attention to. Please contact the Fire Rebuild Team at [email protected] or call 310-456-2489 to discuss any questions or concerns you may have. Like-for-like and like-for-like +10% fee waivers – City Council approved refunds and fee waivers through June 30, 2020. See FAQs. Rebuilding non-conforming structures – To rebuild non-conforming homes and structures without having to bring the structure into compliance or seek variances, property owners must apply with the Planning Department by November 8, 2020. Extensions may be requested. Contact the Fire Rebuild team for details. MALIBU REBUILDS – REBUILD CONSULTATIONS The Fire Rebuild team is available for complimentary one-on-one consultations about any fire rebuild project. Contact Aundrea Cruz at [email protected] to set an appointment or drop by City Hall and a team member will meet with you as soon as possible. For ideas about how to get started with your project, visit the Rebuild Page, where you can view rebuild options and find all related forms and handouts. -

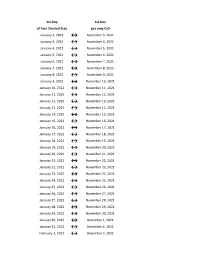

Flex Dates.Xlsx

1st Day 1st Day of Your Desired Stay you may Call January 2, 2022 ↔ November 3, 2021 January 3, 2022 ↔ November 4, 2021 January 4, 2022 ↔ November 5, 2021 January 5, 2022 ↔ November 6, 2021 January 6, 2022 ↔ November 7, 2021 January 7, 2022 ↔ November 8, 2021 January 8, 2022 ↔ November 9, 2021 January 9, 2022 ↔ November 10, 2021 January 10, 2022 ↔ November 11, 2021 January 11, 2022 ↔ November 12, 2021 January 12, 2022 ↔ November 13, 2021 January 13, 2022 ↔ November 14, 2021 January 14, 2022 ↔ November 15, 2021 January 15, 2022 ↔ November 16, 2021 January 16, 2022 ↔ November 17, 2021 January 17, 2022 ↔ November 18, 2021 January 18, 2022 ↔ November 19, 2021 January 19, 2022 ↔ November 20, 2021 January 20, 2022 ↔ November 21, 2021 January 21, 2022 ↔ November 22, 2021 January 22, 2022 ↔ November 23, 2021 January 23, 2022 ↔ November 24, 2021 January 24, 2022 ↔ November 25, 2021 January 25, 2022 ↔ November 26, 2021 January 26, 2022 ↔ November 27, 2021 January 27, 2022 ↔ November 28, 2021 January 28, 2022 ↔ November 29, 2021 January 29, 2022 ↔ November 30, 2021 January 30, 2022 ↔ December 1, 2021 January 31, 2022 ↔ December 2, 2021 February 1, 2022 ↔ December 3, 2021 1st Day 1st Day of Your Desired Stay you may Call February 2, 2022 ↔ December 4, 2021 February 3, 2022 ↔ December 5, 2021 February 4, 2022 ↔ December 6, 2021 February 5, 2022 ↔ December 7, 2021 February 6, 2022 ↔ December 8, 2021 February 7, 2022 ↔ December 9, 2021 February 8, 2022 ↔ December 10, 2021 February 9, 2022 ↔ December 11, 2021 February 10, 2022 ↔ December 12, 2021 February -

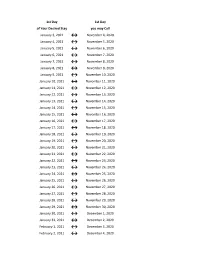

Flex Dates.Xlsx

1st Day 1st Day of Your Desired Stay you may Call January 3, 2021 ↔ November 4, 2020 January 4, 2021 ↔ November 5, 2020 January 5, 2021 ↔ November 6, 2020 January 6, 2021 ↔ November 7, 2020 January 7, 2021 ↔ November 8, 2020 January 8, 2021 ↔ November 9, 2020 January 9, 2021 ↔ November 10, 2020 January 10, 2021 ↔ November 11, 2020 January 11, 2021 ↔ November 12, 2020 January 12, 2021 ↔ November 13, 2020 January 13, 2021 ↔ November 14, 2020 January 14, 2021 ↔ November 15, 2020 January 15, 2021 ↔ November 16, 2020 January 16, 2021 ↔ November 17, 2020 January 17, 2021 ↔ November 18, 2020 January 18, 2021 ↔ November 19, 2020 January 19, 2021 ↔ November 20, 2020 January 20, 2021 ↔ November 21, 2020 January 21, 2021 ↔ November 22, 2020 January 22, 2021 ↔ November 23, 2020 January 23, 2021 ↔ November 24, 2020 January 24, 2021 ↔ November 25, 2020 January 25, 2021 ↔ November 26, 2020 January 26, 2021 ↔ November 27, 2020 January 27, 2021 ↔ November 28, 2020 January 28, 2021 ↔ November 29, 2020 January 29, 2021 ↔ November 30, 2020 January 30, 2021 ↔ December 1, 2020 January 31, 2021 ↔ December 2, 2020 February 1, 2021 ↔ December 3, 2020 February 2, 2021 ↔ December 4, 2020 1st Day 1st Day of Your Desired Stay you may Call February 3, 2021 ↔ December 5, 2020 February 4, 2021 ↔ December 6, 2020 February 5, 2021 ↔ December 7, 2020 February 6, 2021 ↔ December 8, 2020 February 7, 2021 ↔ December 9, 2020 February 8, 2021 ↔ December 10, 2020 February 9, 2021 ↔ December 11, 2020 February 10, 2021 ↔ December 12, 2020 February 11, 2021 ↔ December 13, 2020 -

Sunday, January 24, 2021

Sunday, January 24, 2021 PARISH STAFF: Pastor: Fr. Tim Wozniak Ext. 104 Weekend Assistant: Fr. Mike Erlander Business Administrator: Karen Maza Ext. 100 Music Director: Chris Ángel Ext. 107 Liturgical Ministry Coord & RCIA: Jackie Graham Ext. 110 Pastoral Care: Call 651-683-9808 Director of Faith Formation: Mary McDonald Ext. 108 Director of Outreach and Confirmation: Dez Sobiech Ext. 109 Coordinator Middle School Faith Formation Lori Skare Ext. 111 Database Administrator: Becky Olson Ext. 102 Communications Associate: Monica Lopez Ext. 101 Evening Receptionist: Kevie Skogh Ext. 102 Safe Environment Coord: Pam Magyar Ext. 103 Director of Strategic Planning: Kevin Magyar, Ext. 106 Maintenance: Dave Schelitzche Ext. 105 CONTACT US : VISIT US: ONLINE: www.stbeagan.org 4455 South Robert Trail Parish Office Hours: Eagan, MN 55123 Bulletin & Calendar Monday / Wed / Th 9:00 am - 3:00 pm Like Us on FACEBOOK Phone: (651) 683-9808 Tuesday 9:00 am - 7:30 pm Friday 9:00 am - 1:00 pm CONFESSIONS: Fax:(651) 683-0361 Lord's Day Masses: All Are Welcome Call parish office for appointment [email protected] See website for current information. JANUARY 24, 2021 2 Welcome! a Catholic Community Where ALL are Welcome. If you do not have a church home, we would be honored to have you as part of our parish family. Registration Forms are available at the New Parishioner Welcome Kiosk in the Commons, and online or call our Office at (651) 683-9808 , and we will help you out. All parents (must be parishioners) are asked to attend a baptism preparation meeting prior to the baptism of their child. -

Julian Date Cheat Sheet for Regular Years

Date Code Cheat Sheet For Regular Years Day of Year Calendar Date 1 January 1 2 January 2 3 January 3 4 January 4 5 January 5 6 January 6 7 January 7 8 January 8 9 January 9 10 January 10 11 January 11 12 January 12 13 January 13 14 January 14 15 January 15 16 January 16 17 January 17 18 January 18 19 January 19 20 January 20 21 January 21 22 January 22 23 January 23 24 January 24 25 January 25 26 January 26 27 January 27 28 January 28 29 January 29 30 January 30 31 January 31 32 February 1 33 February 2 34 February 3 35 February 4 36 February 5 37 February 6 38 February 7 39 February 8 40 February 9 41 February 10 42 February 11 43 February 12 44 February 13 45 February 14 46 February 15 47 February 16 48 February 17 49 February 18 50 February 19 51 February 20 52 February 21 53 February 22 54 February 23 55 February 24 56 February 25 57 February 26 58 February 27 59 February 28 60 March 1 61 March 2 62 March 3 63 March 4 64 March 5 65 March 6 66 March 7 67 March 8 68 March 9 69 March 10 70 March 11 71 March 12 72 March 13 73 March 14 74 March 15 75 March 16 76 March 17 77 March 18 78 March 19 79 March 20 80 March 21 81 March 22 82 March 23 83 March 24 84 March 25 85 March 26 86 March 27 87 March 28 88 March 29 89 March 30 90 March 31 91 April 1 92 April 2 93 April 3 94 April 4 95 April 5 96 April 6 97 April 7 98 April 8 99 April 9 100 April 10 101 April 11 102 April 12 103 April 13 104 April 14 105 April 15 106 April 16 107 April 17 108 April 18 109 April 19 110 April 20 111 April 21 112 April 22 113 April 23 114 April 24 115 April -

Pay Date Calendar

Pay Date Information Select the pay period start date that coincides with your first day of employment. Pay Period Pay Period Begins (Sunday) Pay Period Ends (Saturday) Official Pay Date (Thursday)* 1 January 10, 2016 January 23, 2016 February 4, 2016 2 January 24, 2016 February 6, 2016 February 18, 2016 3 February 7, 2016 February 20, 2016 March 3, 2016 4 February 21, 2016 March 5, 2016 March 17, 2016 5 March 6, 2016 March 19, 2016 March 31, 2016 6 March 20, 2016 April 2, 2016 April 14, 2016 7 April 3, 2016 April 16, 2016 April 28, 2016 8 April 17, 2016 April 30, 2016 May 12, 2016 9 May 1, 2016 May 14, 2016 May 26, 2016 10 May 15, 2016 May 28, 2016 June 9, 2016 11 May 29, 2016 June 11, 2016 June 23, 2016 12 June 12, 2016 June 25, 2016 July 7, 2016 13 June 26, 2016 July 9, 2016 July 21, 2016 14 July 10, 2016 July 23, 2016 August 4, 2016 15 July 24, 2016 August 6, 2016 August 18, 2016 16 August 7, 2016 August 20, 2016 September 1, 2016 17 August 21, 2016 September 3, 2016 September 15, 2016 18 September 4, 2016 September 17, 2016 September 29, 2016 19 September 18, 2016 October 1, 2016 October 13, 2016 20 October 2, 2016 October 15, 2016 October 27, 2016 21 October 16, 2016 October 29, 2016 November 10, 2016 22 October 30, 2016 November 12, 2016 November 24, 2016 23 November 13, 2016 November 26, 2016 December 8, 2016 24 November 27, 2016 December 10, 2016 December 22, 2016 25 December 11, 2016 December 24, 2016 January 5, 2017 26 December 25, 2016 January 7, 2017 January 19, 2017 1 January 8, 2017 January 21, 2017 February 2, 2017 2 January -

Due Date Chart 201803281304173331.Xlsx

Special Event Permit Application Due Date Chart for Events from January 1, 2019 - June 30, 2020 If due date lands on a Saturday or Sunday, the due date is moved to the next business day Event Date 30 Calendar days 90 Calendar Days Tuesday, January 01, 2019 Sunday, December 02, 2018 Wednesday, October 03, 2018 Wednesday, January 02, 2019 Monday, December 03, 2018 Thursday, October 04, 2018 Thursday, January 03, 2019 Tuesday, December 04, 2018 Friday, October 05, 2018 Friday, January 04, 2019 Wednesday, December 05, 2018 Saturday, October 06, 2018 Saturday, January 05, 2019 Thursday, December 06, 2018 Sunday, October 07, 2018 Sunday, January 06, 2019 Friday, December 07, 2018 Monday, October 08, 2018 Monday, January 07, 2019 Saturday, December 08, 2018 Tuesday, October 09, 2018 Tuesday, January 08, 2019 Sunday, December 09, 2018 Wednesday, October 10, 2018 Wednesday, January 09, 2019 Monday, December 10, 2018 Thursday, October 11, 2018 Thursday, January 10, 2019 Tuesday, December 11, 2018 Friday, October 12, 2018 Friday, January 11, 2019 Wednesday, December 12, 2018 Saturday, October 13, 2018 Saturday, January 12, 2019 Thursday, December 13, 2018 Sunday, October 14, 2018 Sunday, January 13, 2019 Friday, December 14, 2018 Monday, October 15, 2018 Monday, January 14, 2019 Saturday, December 15, 2018 Tuesday, October 16, 2018 2019 Tuesday, January 15, 2019 Sunday, December 16, 2018 Wednesday, October 17, 2018 Wednesday, January 16, 2019 Monday, December 17, 2018 Thursday, October 18, 2018 Thursday, January 17, 2019 Tuesday, December 18, 2018 -

Waltham Weekly Food Guide January 18

Waltham Free Food Resources January 18 to January 24, 2021 Compiled by WATCH CDC www.watchcdc.org Please have only one family member go for pick up – children do not need to be present. Monday, January 18 10am–12pm [Breakfast & Lunch to go for anyone] Salvation Army - 33 Myrtle Street 11:30am [Meals to go for Seniors] Springwell - Waltham Clark Apts. 48 Pine Street 12:30 [Lunch to go for anyone] The Community Day Center, 16 Felton Street 4:30pm-5:30pm [Dinner to go for anyone] MHSA - Immanuel Methodist Church, 545 Moody Street Tuesday, January 19 10am–12pm [Breakfast & Lunch to go for anyone] Salvation Army - 33 Myrtle Street 11:30am [Meals to go for Seniors] Springwell - Waltham Clark Apts. 48 Pine Street & Mills Apartments, 174 Moody St 12:30 [Lunch to go for anyone] The Community Day Center, 16 Felton Street 1:30 - 2:30pm [Meals to go for anyone] Charles River Mobile Market - 495 Western Ave, Brighton. Open to patients of Charles River Community Health Center Waltham or Brighton. 2:30pm-6pm [Groceries, toiletries] Centre St. Food Pantry - 11 Homer St., Newton, Lower level of Trinity Church, pick up on Furber Lane. Must register the first time.New families must register. More info. at www.centrestfoodpantry.org 3:30-4:30 [Meals to go for 18 and younger] Waltham Boys and Girls Club - 20 Exchange St. No registration required. 4:30pm-5:30pm [Dinner to go for anyone] MHSA - Immanuel Methodist Church, 545 Moody Street Wednesday, January 20 9am-12pm [Groceries for anyone] MHSA - Immanuel Church, 545 Moody St. -

Date of Close Contact Exposure

Date of Close Contact Exposure 7 days 10 days 14 days Monday, November 16, 2020 Tuesday, November 24, 2020 Friday, November 27, 2020 Tuesday, December 1, 2020 Tuesday, November 17, 2020 Wednesday, November 25, 2020 Saturday, November 28, 2020 Wednesday, December 2, 2020 Wednesday, November 18, 2020 Thursday, November 26, 2020 Sunday, November 29, 2020 Thursday, December 3, 2020 Thursday, November 19, 2020 Friday, November 27, 2020 Monday, November 30, 2020 Friday, December 4, 2020 Friday, November 20, 2020 Saturday, November 28, 2020 Tuesday, December 1, 2020 Saturday, December 5, 2020 Saturday, November 21, 2020 Sunday, November 29, 2020 Wednesday, December 2, 2020 Sunday, December 6, 2020 Sunday, November 22, 2020 Monday, November 30, 2020 Thursday, December 3, 2020 Monday, December 7, 2020 Monday, November 23, 2020 Tuesday, December 1, 2020 Friday, December 4, 2020 Tuesday, December 8, 2020 Tuesday, November 24, 2020 Wednesday, December 2, 2020 Saturday, December 5, 2020 Wednesday, December 9, 2020 Wednesday, November 25, 2020 Thursday, December 3, 2020 Sunday, December 6, 2020 Thursday, December 10, 2020 Thursday, November 26, 2020 Friday, December 4, 2020 Monday, December 7, 2020 Friday, December 11, 2020 Friday, November 27, 2020 Saturday, December 5, 2020 Tuesday, December 8, 2020 Saturday, December 12, 2020 Saturday, November 28, 2020 Sunday, December 6, 2020 Wednesday, December 9, 2020 Sunday, December 13, 2020 Sunday, November 29, 2020 Monday, December 7, 2020 Thursday, December 10, 2020 Monday, December 14, 2020 Monday, November -

Washington, Saturday, January 24, 1942

¿ s FEDERAL REGISTER VOLUME 7 1 9 3 4 ¿ r NUMBER 17 4 </a « t e d ^ Washington, Saturday, January 24, 1942 The President said Act, and to exercise its powers and CONTENTS perform its duties thereunder, hereby makes and promulgates the following THE PRESIDENT EXECUTIVE ORDER regulation: Executive Order: Page 1. Section 202.1 of the Economic Reg Washington, land reserved for R eserving a T ract op Land for U se by ulations is hereby amended to read as use of Commerce Depart the D epartment o p C ommerce as a follows: ment as beacon site---------- 499 B eacon S it e § 202.1 Forms of monthly reports of RULES, REGULATIONS, WASHINGTON financial and operating statistics. Fi ORDERS nancial and statistical reports shall be By virtue of the authority vested in me T itl e 14—C iv il A viation: as President of the United States, it is made by the air carriers as follows: Civil Aeronautics Board: ordered that the following-described (a) Each air carrier engaged in reg Economic regulations tract of land within the exterior boun ularly scheduled interstate air transpor amended: daries of the Wenatchee National Forest, tation within the continental limits of Form of accounts-------------- 500 in the State of Washington, claim to the United States and each air carrier Forms of monthly reports of which has been released by the Northern engaged in regularly scheduled opera financial and operating Pacific Railway Company in accordance tions within the territory of Hawaii shall statistics_____________ 499 with section 321 (b) of the Transporta for the month of January 1942 and each T itle 30—M ineral R esources: tion Act of 1940 (54 Stat.