Audit Report on the Accounts of District Government Okara

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Government of the Punjab Primary & Secondary

GOVERNMENT OF THE PUNJAB PRIMARY & SECONDARY HEALTHCARE DEPARTMENT Dated Lahore, the 22nd, June 2021 O R D E R No.SO(WMO-II)22-30/2021(Adhoc), The following candidates are hereby appointed as Women Medical Officer (BS-17), on adhoc basis with immediate effect for a period of one year in District Okara or till the availability of regular incumbent/ selectee of the Punjab Public Service Commission, Lahore, whichever is earlier on the place of posting mentioned against each: Sr. Name of Doctor Proposed Station by Committee # 1. Dr. Asma Sadiq d/o Muhammad Sadiq DHQ Hospital Okara City THQ Hospital Haveli Lakha (Against the post of 2. Dr. Hafiza Bushra Shakoor d/o Abdul Shakoor SWMO(OPS) DHQ Hospital (SC) Okara Against the post of 3. Dr. Ammara Masood d/o Masood Iqbal SWMO(OPS) 4. Dr. Aqsa Moatter d/o Zikrullah BHU Muhammad Nagar 5. Dr. Maliha Tul Zahra d/o Ashfaq Ahmad Saqi BHU Daula Mehr Chand THQ Hospital Haveli Lakha Against the post of 6. Dr. Kiran Javed d/o Javed Anjum SWMO(OPS) 7. Dr. Aiman Khalil d/o Khalil Ur Rehman RHC Hujra Shah Muqeem 8. Dr. Aisha Fakhar d/o Fakhar Hussain THQ Hospital Depalpur, Okara 9. Dr. Iqra Aslam d/o Muhammad Aslam BHU Kohla 10. Dr. Huma Ali d/o Sabir Ali THQ Hospital Depalpur, Okara THQ Hospital Depalpur, Okara (Against the post 11. Dr. Maharukh Abbas d/o Muhammad Abbas of SWMO(OPS) Powered by: Health Information and Service Delivery Unit (HISDU) 12. Dr. Qurt Ul Ain Javed d/o Muhammad Javed THQ Hospital Haveli Lakha Okara 13. -

District OKARA CRITERIA for RESULT of GRADE 8

District OKARA CRITERIA FOR RESULT OF GRADE 8 Criteria OKARA Punjab Status Minimum 33% marks in all subjects 98.00% 87.61% PASS Pass + Minimum 33% marks in four subjects and 28 to 32 marks Pass + Pass with 98.15% 89.28% in one subject Grace Marks Pass + Pass with Pass + Pass with grace marks + Minimum 33% marks in four Grace Marks + 99.82% 96.89% subjects and 10 to 27 marks in one subject Promoted to Next Class Candidate scoring minimum 33% marks in all subjects will be considered "Pass" One star (*) on total marks indicates that the candidate has passed with grace marks. Two stars (**) on total marks indicate that the candidate is promoted to next class. PUNJAB EXAMINATION COMMISSION, RESULT INFORMATION GRADE 8 EXAMINATION, 2019 DISTRICT: OKARA Students Students Students Pass % with Pass + Promoted Pass + Gender Registered Appeared Pass 33% marks Students Promoted % Male 11433 11232 11023 98.14 11216 99.86 Public School Female 10466 10324 10147 98.29 10309 99.85 Male 3058 3017 2950 97.78 3011 99.80 Private School Female 3214 3169 3113 98.23 3164 99.84 Male 957 897 858 95.65 891 99.33 Private Candidate Female 737 716 677 94.55 710 99.16 29865 29355 28768 PUNJAB EXAMINATION COMMISSION, GRADE 8 EXAMINATION, 2019 DISTRICT: OKARA Overall Position Holders Roll NO Name Marks Position 86-218-109 Aqsa Bibi 489 1st 86-108-313 Sana Rasool 482 2nd 86-256-203 Arshyia Azam 482 2nd 86-109-321 Iman Fatima 479 3rd PUNJAB EXAMINATION COMMISSION, GRADE 8 EXAMINATION, 2019 DISTRICT: OKARA Male Position Holders Roll NO Name Marks Position 86-219-170 Huzafa Imdad Bhatti 472 1st 86-151-270 Kashif Khawaja 470 2nd 86-137-349 Muhammmad Umar 467 3rd PUNJAB EXAMINATION COMMISSION, GRADE 8 EXAMINATION, 2019 DISTRICT: OKARA FEMALE Position Holders Roll NO Name Marks Position 86-218-109 Aqsa Bibi 489 1st 86-108-313 Sana Rasool 482 2nd 86-256-203 Arshyia Azam 482 2nd 86-109-321 Iman Fatima 479 3rd j b i i i i Punjab Examination Commission Grade 8 Examination 2019 School wise Results Summary Sr. -

FLOOD RISK ASSESSMENT REPORT a Hi-Tech Knowledge Management Tool for Disaster Risk Assessment at UNION COUNCIL Level

2015 FLOOD RISK ASSESSMENT REPORT A Hi-Tech Knowledge Management Tool for Disaster Risk Assessment at UNION COUNCIL Level A PROPOSAL IN VIEW OF LESSONS LEARNED ISBN (P) 978-969-638-093-1 ISBN (D) 978-969-638-094-8 205-C 2nd Floor, Evacuee Trust Complex, F-5/1, Islamabad 195-1st Floor, Deans Trade Center, Peshawar Cantt; Peshawar Landline: +92.51.282.0449, +92.91.525.3347 E-mail: [email protected], Website: www.alhasan.com ALHASAN SYSTEMS PRIVATE LIMITED A Hi-Tech Knowledge Management, Business Psychology Modeling, and Publishing Company 205-C, 2nd Floor, Evacuee Trust Complex, Sector F-5/1, Islamabad, Pakistan 44000 195-1st Floor, Dean Trade Center, Peshawar Can ; Peshawar, Pakistan 25000 Landline: +92.51.282.0449, +92.91.525.3347 Fax: +92.51.835.9287 Email: [email protected] Website: www.alhasan.com Facebook: www.facebook.com/alhasan.com Twi er: @alhasansystems w3w address: *Alhasan COPYRIGHT © 2015 BY ALHASAN SYSTEMS All rights reserved. No part of this publica on may be reproduced, stored in a retrieval system, or transmi ed, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior wri en permission of ALHASAN SYSTEMS. 58 p.; 8.5x11.5 = A3 Size Map ISBN (P) 978-969-638-093-1 ISBN (D) 978-969-638-094-8 CATALOGING REFERENCE: Disaster Risk Reduc on – Disaster Risk Management – Disaster Risk Assessment Hyogo Framework for Ac on 2005-2015 Building the Resilience of Na ons and Communi es to Disasters IDENTIFY, ACCESS, AND MONITOR DISASTER RISKS AND ENHANCE EARLY WARNING x Risk assessments -

Census 1998 OKARA

Census 1998 OKARA Basic ·Population and Housing Data by Union Councils Government of Pakistan Statistics Division Population Census Organization www.census.gov. pk - - -- - Ill PREFACE With the introduction of the nei,.y local government system in the country, under the devolution of power plan, Union Councils have become the primary unit of the new set-up. As such, census data at the union council level is in demand. I( Since the present government is attaching great importance to development planning at the micro level, it has been considered appropriate to publish data on some important population and housing characteristics by union councils, within a district. in concise form to meet the requirement of the Local Government Departments as well as the common data users. This brief report contains three tables. The first one gives a summary of the population data by tehsils and individual urban localities in the district whereas the second and third tables present basic population and housing statistics by union councils and census areas/mauzas/ villages respectively. j I hope this report will be a handy and useful reference fo~ data users and · especially the planners who would be involved in development of various civic plans Il at micro level. 'f I would like to express my deep appreciation for officers and staff of the Data Processing Branch and the Geography Branch for their efforts and contribution in bringing out this valuable publication. NAJAM HASAN Islamabad, July, 2005 Chief Census Commissioner iv CONTENTS Page No. Okara District at a glance v District map showing boundaries of Union Councils vii Table 1 - Area, population by sex, sex ratio, population density, household size and growth rate 1 Table 2 - Population by sex, literacy ratio. -

Ehsaas Undergraduate Scholarship Program University of Okara List Of

Ehsaas Undergraduate Scholarship Program University of Okara List of Recommended and waitlist Students o. Name of N Application Father . the Complete Address core (W) r ID Name S House S Income Candidate Gender Remarks / Waiting List ather Status Evaluation Structure of Expenditure F Recommended Total Monthly Total Monthly Class/Program Domicile (City) 1 (R) 1st Year Merit List Male Father is deceased muhammad parmanand khas p\o mandi ahmad Kutcha brother is a 1. 259641 liaqat ali Botany Male Okara Deceased 10000 17389 85.833 R sher abad House rickshaw driver and married. 2 sisters. 1 sister QAMAR Software Kutcha doing nothing. 1 2. 184912 ZAFAR IQBAL Male Dipalpur Deceased 14000 17350 Mohalla Gilania Dipalpur, Okara 81.750 R RAZA Engineering House sister in school. He teaches at home tuition. Semi Naeem Sakhi 3. 273189 Statistics Male Dipalpur Deceased 20000 24660 Pucca 79.583 R Abbas Muhammad House Father is deceased. 1 elder brother is Muslim town chak no 53/5L daak Semi Muhammad laborer, 1 brother 4. 264678 Khalil Ahmad Biology Male Sahiwal Deceased 20000 17708 khana okara cantt tehsil o district Pucca 79.500 R Danish is teaching at sahiwal House home. 1 sister married. 1 sis un married. 1 younger Muhammad Semi Renala chak no 30/1AL shergarh tehsil renal sister college. 5. 206028 Awais Abdul Rasheed Physics Male Deceased 27000 21000 Pucca 79.250 R Khurd khurd district okara Rasheed House 6 bro sis, 1 sis and 1 bro married. Muhammad Muhammad Satgarah Post Office KHas Tehsil & Kutcha Father is farmer 6. 267528 Biology Male Okara Alive 15000 21631 77.917 R Shafiq Rafiq District Okara House and at home due to accident 1 in coma. -

The Military and Denied Development in the Pakistani Punjab Anthem Frontiers of Global Political Economy

The Military and Denied Development in the Pakistani Punjab Anthem Frontiers of Global Political Economy The Anthem Frontiers of Global Political Economy series seeks to trigger and attract new thinking in global political economy, with particular reference to the prospects of emerging markets and developing countries. Written by renowned scholars from different parts of the world, books in this series provide historical, analytical and empirical perspectives on national economic strategies and processes, the implications of global and regional economic integration, the changing nature of the development project, and the diverse global-to-local forces that drive change. Scholars featured in the series extend earlier economic insights to provide fresh interpretations that allow new understandings of contemporary economic processes. Series Editors Kevin Gallagher – Boston University, USA Jayati Ghosh – Jawaharlal Nehru University, India Editorial Board Stephanie Blankenburg – School of Oriental and African Studies (SOAS), UK Ha-Joon Chang – University of Cambridge, UK Wan-Wen Chu – RCHSS, Academia Sinica, Taiwan Léonce Ndikumana – University of Massachusetts-Amherst, USA Alica Puyana Mutis – Facultad Latinoamericana de Ciencias Sociales (FLASCO-México), Mexico Matías Vernengo – Banco Central de la República Argentina, Argentina Robert Wade – London School of Economics and Political Science (LSE), UK Yu Yongding – Chinese Academy of Social Sciences (CASS), China The Military and Denied Development in the Pakistani Punjab An Eroding Social Consensus Shahrukh Rafi Khan and Aasim Sajjad Akhtar with Sohaib Bodla Anthem Press An imprint of Wimbledon Publishing Company www.anthempress.com This edition first published in UK and USA 2014 by ANTHEM PRESS 75–76 Blackfriars Road, London SE1 8HA, UK or PO Box 9779, London SW19 7ZG, UK and 244 Madison Ave #116, New York, NY 10016, USA Copyright © 2014 Shahrukh Rafi Khan, Aasim Sajjad Akhtar, Sohaib Bodla The moral right of the authors has been asserted. -

Water Supply & Sanitation

WATER SUPPLY & SANITATION VISION Provision of adequate, safe drinking water and sanitation facilities to the entire rural and urban communities of Punjab through equitable, efficient and sustainable services. WATER & SANITATION POLICY • Government of the Punjab aims to provide safe drinking water of an adequate quantity at an affordable cost through equitable, efficient and sustainable services to all citizens (Drinking Water Policy Approved in May, 2011). • The goal of the provincial sanitation policy is to ensure that the entire population of Punjab has access to safe and affordable sanitation for a quality life. (Punjab Sanitation Policy has been formulated recognizing the significance of sanitation which is under approval). OBJECTIVES · To improve socio economic condition · To improve health and nutrition outcome · To raise living standard of the community by providing quality drinking water and improved sanitation services. · To reduce spread of water borne diseases. STRATEGIC INTERVENTIONS · Special focus on need based interventions in water supply & sanitation sector. · Effective measures have been taken to serve Southern Punjab. · Maximum allocation is for on-going programme for timely completion of on-going schemes to avoid the cost overrun. · Ensuring priority in resource distribution for sanitation sector. · Ensuring regional equity (North & South Punjab) in the developmental portfolio. 145 · Ensuring water quality under Saaf Pani Initiative. · 415 Water Supply Schemes (75 Urban and 340 Rural) are being executed by allocating funds of Rs. 4,575.387 million. · 810 Sanitation schemes (160 Urban and 650 Rural) are being executed for which funds of Rs. 9,793.525 million are allocated. · 19 Punjab based scheme are being executed for which funds of Rs. -

U.S. Department of State ARCHIVED CONTENT

5/28/2020 Pakistan You are viewing: ARCHIVED CONTENT Information released online from January 20, 2009 to January 20, 2017. NOTE: Content in this archive site is NOT UPDATED, and links may not function. External links to other Internet sites should not be construed as an endorsement of the views contained therein. Go to the current State.gov website for up-to-date information. (http://www.state.gov/) U.S. Department of State Diplomacy in Action Pakistan Country Reports on Human Rights Practices Bureau of Democracy, Human Rights, and Labor 2000 February 23, 2001 On October 12, 1999, the elected civilian Government of former Prime Minister Mian Nawaz Sharif was overthrown in a bloodless coup led by Army Chief of Staff General Pervez Musharraf. In consultation with senior military commanders, General Musharraf designated himself Chief Executive, and suspended the Constitution, the Parliament, and the provincial assemblies. The office of the President, which is mainly ceremonial, was retained. General Musharraf appointed an advisory National Security Council, which included both military and civilian advisers, and a civilian cabinet. The government bureaucracy continued to function; however, at all levels, the functioning of the Government after the coup was "monitored" by military commanders. In May the Supreme Court ruled that the Musharraf Government was constitutional and imposed a 3-year deadline--starting from October 12, 1999--to complete a transition to democratic, civilian rule. On December 31, local elections were held in 18 districts on a non-party basis; however the Government has not set a timetable for national elections. Corruption and inefficiency remained acute in all branches of government. -

Table -23 Selected Population Statistics of Rural

TABLE -23 SELECTED POPULATION STATISTICS OF RURAL LOCALITIES POPULATION CHARACTERISTICS AGE GROUP HADBAST EDUCATIONAL ATTAINMENT POPULATION LITERACY % (10+ YEARS) HOLDING NAME OF MAUZA / DEH / NUMBER / RELIGION WORKED C.N.I. AREA IN MATRIC BUT BELOW DEGREE VILLAGE / SETTLMENT DEH PRIMARY BUT BELOW MATRIC DEGREE & ABOVE 10 YEARS 18 YEARS 60 YEARS (10 YEARS CARD (18 ACRES NUMBER & OTHERS ALL TRANSGE ALL TRANSGE & ABOVE & ABOVE & ABOVE & ABOVE) YEARS & MALE FEMALE MALE FEMALE TRANSGE TRANSGE TRANSGE NON ABOVE) SEXES NDER SEXES NDER MALE FEMALE MALE FEMALE MALE FEMALE MUSLIM NDER NDER NDER MUSLIM 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 OKARA DISTRICT 2,198,262 1,127,158 1,070,979 125 51.97 61.50 41.96 29.60 272,273 177,163 12 108,909 59,857 7 21,038 15,698 4 2,169,936 28,326 1,579,025 1,191,276 147,837 502,990 959,733 1047961 DEPALPUR TEHSIL 1,033,260 531,297 501,909 54 46.48 56.62 35.74 20.37 115,276 69,190 2 41,392 18,659 2 8,611 4,783 1 1,032,554 706 733,351 550,841 68,406 249,100 426,350 604588 BASIRPUR QH 88,750 45,627 43,116 7 45.01 55.64 33.80 14.29 9,578 5,556 - 3,225 1,240 - 818 367 1 88,694 56 63,471 48,005 6,662 23,044 35,848 55725 ADL MARHA PC 6,457 3,303 3,154 - 51.75 64.01 39.02 - 745 442 - 262 122 - 69 35 - 6,453 4 4,587 3,406 480 1,654 2,688 2420 BATTOK 0000350 1,608 797 811 - 48.22 63.26 33.10 - 178 77 - 53 21 - 10 3 - 1,608 - 1,151 861 126 423 661 601 CHAK UTTAM SINGH 0000346 187 87 100 - 43.48 57.58 30.56 - 14 4 - 11 8 - 1 1 - 187 - 138 113 16 56 91 199 CHAKARKE 0000349 1,082 552 530 - 51.49 -

DRAFT LIST of POLLING STATION, NA-141 OKARA-I (Mr. Mumtaz

DRAFT LIST OF POLLING STATION, NA-141 OKARA-I (Mr. Mumtaz Ahmad, Addl: District & Sessions Judge, Okara, RO) Polling Constituency Polling Station Electoral Area Male Female Total Male Female Total Booth Station Polling Station Name Electoral Area Block Code Number Name Urdu Urdu Voters Voters Voters Booths Booths Booths Type Serial No 1 2 3 4 5 6 7 8 9 10 11 12 13 14 چاہ اروڑیاں واﻻ / / Chah Arrorian Wala 193140101 332 0 332 چوک پراچہ مو ڑ Chowk Paracha Mor ی مصط یف آباد گورنمنٹ بوائز ہائ ,Govt. Boys High School ر Mustafa Abad Street Male 4 0 4 346 0 346 193140105 سٹیٹ طالب حس یی سکول صدرگوگ ٹہ ایسٹ (NA-141 1 Sadar Gogera ( East Side Talib Hussain Wali وایل سائیڈ *(P) کمپ ین باغ ، سول Company Bagh, Civil 193140201 382 0 382 ہسپتال ،عیل س رٹ ی ٹ Hospital, Ali Street چاہ اروڑیاں واﻻ / / Chah Arrorian Wala 193140101 0 276 276 چوک پراچہ مو ڑ Chowk Paracha Mor ی مصطف آباد ی ,Govt. Boys High School ر Mustafa Abad Street گورنمنٹ بوائز ہائ Female 2 2 0 248 248 0 193140105 سٹیٹ طالب حس یی (NA-141 2 Sadar Gogera ( West Side Talib Hussain Wali سکول صدر گوگ ٹہ وایل *(P) کمپ ین باغ ، سول Company Bagh, Civil 193140201 0 327 327 ہسپتال ،عیل س رٹیٹ Hospital, Ali Street بس ین مصط یف آباد / / Basti Mustafa Abad 193140102 238 0 238 بس ین عبدالستار Basti Abdul Sattar گورنمنٹ ۔ان رٹکالج ,Govt. Inter College 295 0 295 193140103 بس ین عبدالستا ر Basti Abdul Sattar Male 3 0 3 ،جندراکہ روڈ گوگ ٹہ NA-141 3 Jandraka Road Gogera مر یض پورہ ، Marzi Pura, Haji ایسٹ سائیڈ *(East Portion) (P) 424 0 424 193140104 حا یج چوک ، محلہ Chowk, Moh: Umer ع م ر ف ا ر و ق Farooq بس ین مصط یف آباد / Basti Mustafa Abad 193140102 0 192 192 / بس ین عبدالس ت ا ر Basti Abdul Sattar گورنمنٹ گرلز پرائمری ,Govt. -

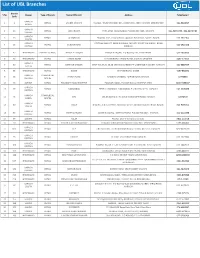

To Download UBL Branch List

List of UBL Branches Branch S No Region Type of Branch Name Of Branch Address Telephone # Code KARACHI 1 2 RETAIL LANDHI KARACHI H-G/9-D, TRUST CERAMIC IND., LANDHI IND. AREA KARACHI (EPZ) EXPORT 021-5018697 NORTH KARACHI 2 19 RETAIL JODIA BAZAR PARA LANE, JODIA BAZAR, P.O.BOX NO.4627, KARACHI. 021-32434679 , 021-32439484 CENTRAL KARACHI 3 23 RETAIL AL-HAROON Shop No. 39/1, Ground Floor, Opposite BVS School, Sadder, Karachi 021-2727106 SOUTH KARACHI CENTRAL BANK OF INDIA BUILDING, OPP CITY COURT,MA JINNAH ROAD 4 25 RETAIL BUNDER ROAD 021-2623128 CENTRAL KARACHI. 5 47 HYDERABAD AMEEN - ISLAMIC PRINCE ALLY ROAD PRINCE ALI ROAD, P.O.BOX NO.131, HYDERABAD. 022-2633606 6 46 HYDERABAD RETAIL TANDO ADAM STATION ROAD TANDO ADAM, DISTRICT SANGHAR. 0235-574313 KARACHI 7 52 RETAIL DEFENCE GARDEN SHOP NO.29,30, 35,36 DEFENCE GARDEN PH-1 DEFENCE H.SOCIETY KARACHI 021-5888434 SOUTH 8 55 HYDERABAD RETAIL BADIN STATION ROAD, BADIN. 0297-861871 KARACHI COMMERCIAL 9 65 NAPIER ROAD KASSIM CHAMBERS, NAPIER ROAD,KARACHI. 32775993 CENTRAL CENTRE 10 66 SUKKUR RETAIL FOUJDARY ROAD KHAIRPUR FOAJDARI ROAD, P.O.BOX NO.14, KHAIRPUR MIRS. 0243-9280047 KARACHI 11 69 RETAIL NAZIMABAD FIRST CHOWRANGI, NAZIMABAD, P.O.BOX NO.2135, KARACHI. 021-6608288 CENTRAL KARACHI COMMERCIAL 12 71 SITE UBL BUILDING S.I.T.E.AREA MANGHOPIR ROAD, KARACHI 32570719 NORTH CENTRE KARACHI 13 80 RETAIL VAULT Shop No. 2, Ground Floor, Nonwhite Center Abdullah Harpoon Road, Karachi. 021-9205312 SOUTH KARACHI 14 85 RETAIL MARRIOT ROAD GILANI BUILDING, MARRIOT ROAD, P.O.BOX NO.5037, KARACHI. -

Okara Blockwise

POPULATION AND HOUSEHOLD DETAIL FROM BLOCK TO DISTRICT LEVEL PUNJAB (OKARA DISTRICT) ADMIN UNIT POPULATION NO OF HH OKARA DISTRICT 3,039,139 493,180 DEPALPUR TEHSIL 1,374,912 226,721 AHMADABAD MC 39,447 6539 CHARGE NO 19 39,447 6539 CIRCLE NO 01 12,020 1831 195190101 1,522 206 195190102 1,982 320 195190103 1,277 197 195190104 1,123 187 195190105 1,972 290 195190106 1,572 238 195190107 833 116 195190108 1,172 195 195190109 567 82 CIRCLE NO 02 9,630 1665 195190201 1,829 279 195190202 860 150 195190203 1,708 317 195190204 1,647 305 195190205 2,069 365 195190206 1,517 249 CIRCLE NO 03 7,432 1299 195190301 606 110 195190302 1,272 225 195190303 588 90 195190304 1,510 271 195190305 1,627 278 195190306 1,829 325 CIRCLE NO 04 5,805 981 195190401 1,481 257 195190402 1,451 252 195190403 1,350 222 195190404 1,016 173 195190405 507 77 CIRCLE NO 05 4,560 763 195190501 1,530 228 195190502 834 165 195190503 807 138 195190504 856 150 195190505 533 82 BASIRPUR MC 48,326 8194 CHARGE NO 17 23,338 3792 CIRCLE NO 01 9,355 1582 195170101 1,169 209 195170102 1,640 283 195170103 2,105 327 195170104 1,363 233 195170105 1,706 298 195170106 1,372 232 Page 1 of 89 POPULATION AND HOUSEHOLD DETAIL FROM BLOCK TO DISTRICT LEVEL PUNJAB (OKARA DISTRICT) ADMIN UNIT POPULATION NO OF HH CIRCLE NO 02 5,882 979 195170201 1,178 204 195170202 1,203 207 195170203 794 138 195170204 1,237 208 195170205 1,470 222 CIRCLE NO 03 8,101 1231 195170301 1,736 289 195170302 1,233 183 195170303 2,086 275 195170304 1,559 246 195170305 1,487 238 CHARGE NO 18 24,988 4402 CIRCLE NO 01 6,695 1221