Assessing the Impacts of Sunrail Stations on Property Values and Development

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Examining the Traffic Safety Effects of Urban Rail Transit

Examining the Traffic Safety Effects of Urban Rail Transit: A Review of the National Transit Database and a Before-After Analysis of the Orlando SunRail and Charlotte Lynx Systems April 15, 2020 Eric Dumbaugh, Ph.D. Dibakar Saha, Ph.D. Florida Atlantic University Candace Brakewood, Ph.D. Abubakr Ziedan University of Tennessee 1 www.roadsafety.unc.edu U.S. DOT Disclaimer The contents of this report reflect the views of the authors, who are responsible for the facts and the accuracy of the information presented herein. This document is disseminated in the interest of information exchange. The report is funded, partially or entirely, by a grant from the U.S. Department of Transportation’s University Transportation Centers Program. However, the U.S. Government assumes no liability for the contents or use thereof. Acknowledgement of Sponsorship This project was supported by the Collaborative Sciences Center for Road Safety, www.roadsafety.unc.edu, a U.S. Department of Transportation National University Transportation Center promoting safety. www.roadsafety.unc.edu 2 www.roadsafety.unc.edu TECHNICAL REPORT DOCUMENTATION PAGE 1. Report No. 2. Government Accession No. 3. Recipient’s Catalog No. CSCRS-R{X}CSCRS-R18 4. Title and Subtitle: 5. Report Date Examining the Traffic Safety Effects of Urban Rail Transit: A Review April 15, 2020 of the National Transit Database and a Before-After Analysis of the 6. Performing Organization Code Orlando SunRail and Charlotte Lynx Systems 7. Author(s) 8. Performing Organization Report No. Eric Dumbaugh, Ph.D. Dibakar Saha, Ph.D. Candace Brakewood, Ph.D. Abubakr Ziedan 9. Performing Organization Name and Address 10. -

Summer 2007 TOD Sketchbook

Central Florida Commuter Rail Summer 2007 Central Florida Commuter Rail On the Inside: page Introduction ........................................ 1 DeLand Station................................... 5 Fort Florida Station ............................ 7 Sanford Station................................... 9 Lake Mary Station ............................ 11 Longwood Station............................. 13 Altamonte Springs Station................ 15 Maitland Station............................... 17 Winter Park Station.......................... 19 Florida Hospital Station ................... 21 LYNX Central Station......................... 23 Church Street Station........................ 25 Orlando Amtrak Station ................... 27 Sand Lake Road Station................... 29 Meadow Woods Station .................... 31 Osceola Parkway Station .................. 33 Kissimmee Station............................ 35 Poinciana Station.............................. 37 The Central Florida Commuter Rail project will provide the opportunity not only to move people more efficiently, but to also build new, walkable, transit-oriented communities around some of its stations and strengthen existing communities around others. In February 2007, FDOT conducted a week long charrette process, individually meeting with the agencies and major stakeholders from DeLand each of the jurisdictions along the proposed 61-mile commuter rail corridor. These The plans and concepts included: Volusia County, Seminole County, illustrated in this report Orange County, -

Functional Classification

City of Sanford Transportation Element TRANSPORTATION ELEMENT DATA, INVENTORY, AND ANALYSIS REPORT TABLE OF CONTENTS DATA, INVENTORY, AND ANALYSIS .........................................................................2-3 DEFINITIONS OF TERMS AND CONCEPTS ...............................................................2-4 EXISTING TRANSPORTATION MAP SERIES.............................................................2-6 ANALYSIS OF EXISTING TRANSPORTATION SYSTEMS ........................................2-7 Level of Service Calculation Methodology………..................................................2-7 Level of Service Standards ...................................................................................2-7 Existing (2009) Peak Hour Peak Direction Vehicle Trips ......................................2-7 Levels of Service and System Needs .................................................................2-11 Existing Modal Split and Vehicle Occupancy Rates............................................2-12 Existing Public Transit Facilities and Routes ......................................................2-12 Peak Hour Transit Capacities, Headways and Ridership by Route ....................2-13 Levels of Service and System Needs .................................................................2-14 Population Characteristics ..................................................................................2-14 Transportation Disadvantaged ............................................................................2-15 Existing Characteristics -

SCHEDULE December 10Th & 17Th, 2016 for the Latest Info: @Ridesunrail / Sunrail.Com Regular Fares Apply

SATURDAY SERVICE SCHEDULE December 10th & 17th, 2016 For the latest info: @RideSunRail / SunRail.com Regular fares apply. SOUTHBOUND P401 P403 P405 P407 P409 P411 P413 P415 P417 DeBary 1:00 PM 2:00 PM 3:00 PM 4:00 PM 5:00 PM 6:00 PM 7:00 PM 8:00 PM 9:00 PM Sanford 1:06 PM 2:06 PM 3:06 PM 4:06 PM 5:06 PM 6:06 PM 7:06 PM 8:06 PM 9:06 PM Lake Mary 1:13 PM 2:13 PM 3:13 PM 4:13 PM 5:13 PM 6:13 PM 7:13 PM 8:13 PM 9:13 PM Longwood 1:19 PM 2:19 PM 3:19 PM 4:19 PM 5:19 PM 6:19 PM 7:19 PM 8:19 PM 9:19 PM Altamonte Springs 1:23 PM 2:23 PM 3:23 PM 4:23 PM 5:23 PM 6:23 PM 7:23 PM 8:23 PM 9:23 PM Maitland 1:29 PM 2:29 PM 3:29 PM 4:29 PM 5:29 PM 6:29 PM 7:29 PM 8:29 PM 9:29 PM Winter Park 1:36 PM 2:36 PM 3:36 PM 4:36 PM 5:36 PM 6:36 PM 7:36 PM 8:36 PM 9:36 PM Florida Hospital Health Village 1:43 PM 2:43 PM 3:43 PM 4:43 PM 5:43 PM 6:43 PM 7:43 PM 8:43 PM 9:43 PM LYNX Central Station 1:48 PM 2:48 PM 3:48 PM 4:48 PM 5:48 PM 6:48 PM 7:48 PM 8:48 PM 10:15 PM Church Street 1:51 PM 2:51 PM 3:51 PM 4:51 PM 5:51 PM 6:51 PM 7:51 PM 8:51 PM 10:18 PM Orlando Health/Amtrak 1:54 PM 2:54 PM 3:54 PM 4:54 PM 5:54 PM 6:54 PM 7:54 PM 8:54 PM 10:21 PM Sand Lake Road 2:03 PM 3:03 PM 4:03 PM 5:03 PM 6:03 PM 7:03 PM 8:03 PM 9:03 PM 10:30 PM NORTHBOUND P402 P404 P406 P408 P410 P412 P414 P416 P418 Sand Lake Road 2:30 PM 3:30 PM 4:30 PM 5:30 PM 6:30 PM 7:30 PM 8:30 PM 9:30 PM 10:45 PM Orlando Health/Amtrak 2:37 PM 3:37 PM 4:37 PM 5:37 PM 6:37 PM 7:37 PM 8:37 PM 9:37 PM 10:52 PM Church Street 2:40 PM 3:40 PM 4:40 PM 5:40 PM 6:40 PM 7:40 PM 8:40 PM 10:15 PM 10:55 PM LYNX Central -

RFA for SAIL Financing, Including 2017 NHTF

Reflects 9-13-17 and 9-15-17 and 10-3-17 Modifications REQUEST FOR APPLICATIONS 2017-108 SAIL FINANCING OF AFFORDABLE MULTIFAMILY HOUSING DEVELOPMENTS TO BE USED IN CONJUNCTION WITH TAX-EXEMPT BOND FINANCING AND NON-COMPETITIVE HOUSING CREDITS Issued By: FLORIDA HOUSING FINANCE CORPORATION Issued: August 31, 2017 Due: October 12, 2017 Page 1 of 148 RFA 2017-108 Reflects 9-13-17 and 9-15-17 and 10-3-17 Modifications SECTION ONE INTRODUCTION This Request for Applications (RFA) is open to Applicants proposing the development of affordable, multifamily housing for Families and the Elderly utilizing State Apartment Incentive Loan (SAIL) funding in conjunction with (i) Tax-Exempt Bond financing (i.e., Corporation-issued Multifamily Mortgage Revenue Bonds (MMRB) or Non-Corporation-issued Tax-Exempt Bonds obtained through a Public Housing Authority (established under Chapter 421, F.S.), a County Housing Finance Authority (established pursuant to Section 159.604, F.S.), or a Local Government), (ii) Non-Competitive Housing Credits (HC), and, if applicable, (iii) National Housing Trust Fund (NHTF). A. SAIL Florida Housing Finance Corporation (the Corporation) expects to offer an estimated $87,320,000, comprised of a part of the Family and Elderly Demographic portion of the SAIL funding appropriated by the 2016 Florida Legislature. The amounts listed in 1 below include ELI Loan funding to cover the units that must be set aside for Extremely Low Income (ELI) Households, including the commitment for a portion of ELI Set-Aside units as Link Units for Persons with Special Needs, as further outlined in Sections Four A.6.d. -

Sunrail.Com Not to Scale

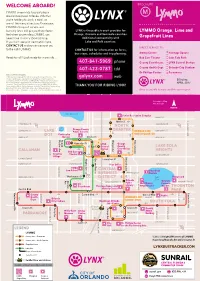

WELCOME ABOARD! BROCHURE LYMMO is your ride to great places M around Downtown Orlando. Whether you’re heading to work, a meal, or one of the many attractions Downtown, LYMMO’s frequent service and bus-only lanes will get you there faster. LYNX is the public transit provider for LYMMO Orange, Lime and And when you’re riding LYMMO, you Orange, Osceola and Seminole counties. never have to worry about parking. Additional connectivity with Grapefruit Lines If you don’t see your destination here, Lake and Polk counties. CONTACT US and we can connect you DIRECT SERVICE TO: to the right LYMMO. CONTACT US for information on fares, bus stops, schedules and trip planning: Amway Center Heritage Square Ready to roll? Look inside for more info... Bob Carr Theater Lake Eola Park 407-841-5969 phone County Courthouse LYNX Central Station 407-423-0787 tdd County Health Dept Orlando City Stadium Dr Phillips Center Parramore Notice of Title VI Rights: LYNX operates its programs and services without regard to race, color, golynx.com web religion, gender, age, national origin, disability, or family status in accordance with Title VI of the Civil Rights Act. Any person who believes Effective: he or she has been aggrieved by any unlawful discriminatory practice APRIL 2017 related to Title VI may file a complaint in writing to LYNX Title VI Officer Desna Hunte, 455 N. Garland Avenue, Orlando, Florida 32801 or by calling THANK YOU FOR RIDING LYNX! 407-254-6117, email [email protected] or www.golynx.com. Information in other languages or accessible formats available upon request. -

Big Freight Railroads to Miss Safety Technology Deadline

Big Freight railroads to miss safety technology deadline FILE - In this June 4, 2014 file photo, a Norfolk Southern locomotive moves along the tracks in Norfolk, Va. Three of the biggest freight railroads operating in the U.S. have told telling the government they won’t make a 2018 deadline to start using safety technology intended to prevent accidents like the deadly derailment of an Amtrak train in Philadelphia last May. Norfolk Southern, Canadian National Railway and CSX Transportation and say they won’t be ready until 2020, according to a list provided to The Associated Press by the Federal Railroad Administration. Steve Helber, File AP Photo BY JOAN LOWY, Associated Press WASHINGTON Three of the biggest freight railroads operating in the U.S. have told the government they won't meet a 2018 deadline to start using safety technology intended to prevent accidents like the deadly derailment of an Amtrak train in Philadelphia last May. Canadian National Railway, CSX Transportation and Norfolk Southern say they won't be ready until 2020, according to a list provided to The Associated Press by the Federal Railroad Administration. Four commuter railroads — SunRail in Florida, Metra in Illinois, the Massachusetts Bay Transportation Authority and Trinity Railway Express in Texas — also say they'll miss the deadline. The technology, called positive train control or PTC, relies on GPS, wireless radio and computers to monitor train positions and automatically slow or stop trains that are in danger of colliding, derailing due to excessive speed or about to enter track where crews are working or that is otherwise off limits. -

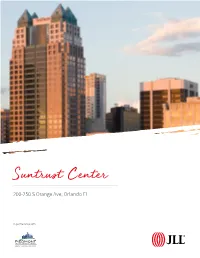

Suntrust Center

Suntrust Center 200-250 S Orange Ave, Orlando FL In partnership with Executive summary Suntrust Center encompasses more than 650,000 rentable square feet of Class A+ office space. The Center consists of the thirty-story main tower and the seven-story Park Building. The ground level public plaza features a spacious lawn area, reflection pool with fountains, shade trees, and multiple seating areas, which creates a unique gathering place for employees and visitors throughout the heart of the CBD. The main tower boasts a luxurious and expansive eight-story lobby, easy access to a plethora of street level retail and dining options, and spectacular views stretching far beyond city limits in all directions. The building’s trademark beige and green exterior and prominent roof, which incorporates four green pyramids and striking white lighting establishes Suntrust Center as one of the most recognizable landmarks in Central Florida. Prestigious design Designed by the world-renowned architectural firm of Skidmore, Owings & Merrill LLP, Suntrust Center is the preeminent Class A+ office tower in downtown Orlando, as well as one of the most exceptional properties in the state of Florida. Its incomparable architectural elements, high quality finishes, meticulous maintenance, and distinction as the city’s tallest office building, synergize to create a trophy asset. In 2001, 2002, and 2003, Suntrust Center was the recipient of BOMA’s “The Outstanding Building of the Year” award and it recently received the prestigious Leadership in Energy and Environmental Design (LEED) certification, with the U.S. Green Building Council awarding a Gold certification to the facility. Suntrust Center at a glance – Completed in 1988, the 654,618 s.f. -

Print Catalog Landscape, FINAL with COVER.Indd

orlando museum of art FLORIDA PRIZE in contemporary art ∙ anthea behm∙ adler guerrier∙maría martínez- cañas∙noelle mason∙ ernesto oroza∙ matt roberts∙dawn roe∙kyle trowbridge∙michael vasquez∙sergio vega∙ orlando museum of art FLORIDA PRIZE in contemporary art May 13 – August 28, 2016 Orlando Museum of Art 2416 North Mills Avenue Orlando, FL 32803 407.896.4231 Kyle Trowbridge, QR 3211806, 2012, acrylic on canvas, 76 x 76 inches, Courtesy of Emerson Dorsch Gallery, Miami. © Kyle [email protected] Trowbridge. Image courtesy of the artist. www.omart.org Major support for this exhibition is made possible through the generosity of: Exhibition Sponsors Anonymous Rita and Jeff rey Adler Foundation Rocky Santomassino PNC Bank Published in conjunction with the exhibition ORLANDO MUSEUM OF ART FLORIDA PRIZE IN CONTEMPORARY ART 2016 Additional support provided by: organized and presented by Orlando Museum of Art Wendy and Michael Henner May 13 - August 28, 2016 Terry and James Mahaff ey Catalog designed by Azela Santana Terry Snow Daisy and Jan Staniszkis Printed by Progressive Communications, Lake Mary, Florida Robert B. Feldman, M.D. Printed in the United States of Am erica Nancy and Jeff rey Baumann ISBN: 1880699133 ISBN-13: 978-1-880699-13-3 Library of Congress Control Number: 2016937509 Copyright © 2016 Orlando Museum of Art Orlando Museum of Art 2416 North Mills Avenue Orlando, Florida 32803 United States of America Telephone: 407.896.4231 Facsimile: 407.896.9920 www.omart.org Accredited by the American Alliance of Museums, the Orlando Museum of Art is a Blue Star Museum supported by the Museum’s Board of Trustees, the Ambassadors, Council of 101, Friends of American Art, Acquisition Trust, earned income, contributions from individuals, corporations and foundations; and is funded in part by Orange County Government through the Arts & Cultural Aff airs Program, sponsored in part by the State of Florida, All rights reserved. -

2019 Winter Events

2019 Winter Events Events will be updated regularly. Check back often for new reasons to ride SunRail! Church Street Station Orlando Magic Games Amway Center, 7:00PM Special 10:30PM southbound service from Church St. Station available for the following home games: January 18, 25, 29 & 31 February 7, 14, 22 & 28 March 8, 14, 20, 22 & 25 April 3 & 5 Hamilton Dr. Philips Performing Arts Center Friday, January 25, 8:00PM Tuesday, January 29, 8:00PM Thursday, January 31, 8:00PM Thursday, February 7, 8:00PM Special 10:30PM southbound service from Church Street Station available. For additional show dates, visit drphillipscenter.org Music for Lovers – Nat King Cole at 100 Dr. Philips Performing Arts Center Thursday, February 14, 8:00PM Special 10:30PM southbound service from Church Street Station available. Hand to God Mad Cow Theatre Friday, January 25, 7:30PM Thursday, January 31, 7:30PM Thursday, February 7, 7:30PM Special 10:30PM southbound service from Church Street Station available. For additional show dates, visit madcowtheatre.com Gloria Mad Cow Theatre Thursday, February 14, 7:30PM Thursday, February 28, 7:30PM Special 10:30PM southbound service from Church Street Station available. For additional show dates, visit madcowtheatre.com SANFORD STATION Free Trolley to Downtown Sanford The Sanford Trolley runs a loop from the SunRail station through Historic Downtown Sanford Monday-Friday. WINTER PARK STATION Winter Park 9 Bring your clubs and golf the Winter Park 9, the city’s award-winning 9-hole golf course. Walking distance from the station. For more information, visit https://cityofwinterpark.org/departments/parks-recreation/golf- course/ AdventHealth STATION Winter Science Spectacular – Dinos in Lights Orlando Science Center Now through January 6, 2019 Monday – Friday, every 30 min. -

Examining the Traffic Safety Effects of Urban Rail Transit

Examining the Traffic Safety Effects of Urban Rail Transit: A Review of the National Transit Database and a Before-After Analysis of the Orlando SunRail and Charlotte Lynx Systems April 15, 2020 Eric Dumbaugh, Ph.D. Dibakar Saha, Ph.D. Florida Atlantic University Candace Brakewood, Ph.D. Abubakr Ziedan University of Tennessee 1 www.roadsafety.unc.edu U.S. DOT Disclaimer The contents of this report reflect the views of the authors, who are responsible for the facts and the accuracy of the information presented herein. This document is disseminated in the interest of information exchange. The report is funded, partially or entirely, by a grant from the U.S. Department of Transportation’s University Transportation Centers Program. However, the U.S. Government assumes no liability for the contents or use thereof. Acknowledgement of Sponsorship This project was supported by the Collaborative Sciences Center for Road Safety, www.roadsafety.unc.edu, a U.S. Department of Transportation National University Transportation Center promoting safety. www.roadsafety.unc.edu 2 www.roadsafety.unc.edu TECHNICAL REPORT DOCUMENTATION PAGE 1. Report No. 2. Government Accession No. 3. Recipient’s Catalog No. CSCRS-R{X}CSCRS-R18 4. Title and Subtitle: 5. Report Date Examining the Traffic Safety Effects of Urban Rail Transit: A Review April 15, 2020 of the National Transit Database and a Before-After Analysis of the 6. Performing Organization Code Orlando SunRail and Charlotte Lynx Systems 7. Author(s) 8. Performing Organization Report No. Eric Dumbaugh, Ph.D. Dibakar Saha, Ph.D. Candace Brakewood, Ph.D. Abubakr Ziedan 9. Performing Organization Name and Address 10. -

Strategic Intermodal System Urban Fixed Guideway

Strategic Intermodal System Urban Fixed Guideway To plan for an efficient and safe Urban Fixed Guideway Terminals in Florida transportation network in Florida, Located Serves SIS Integrated Co-located with the state legislature and Florida Facility Name District System Designation at or near air, sea, or with other major Park-&- termini spaceport SIS system Ride Facility Department of Transportation (FDOT) DeLand Station* 5 SunRail SIS Hub No No No No developed the Strategic Intermodal DeBary Station 5 SunRail SIS Hub Yes No No No System (SIS). As part of the SIS, there Sanford Auto Train Track Station 5 SunRail SIS Station No No No No are specific elements Lake Mary Station 5 SunRail SIS Station No No No No that have been identified as critical to Longwood Station 5 SunRail SIS Station No No No No the economic success of Florida. Altamonte Springs Station 5 SunRail SIS Station No No No No Maitland Station 5 SunRail SIS Station No No No No One of these elements are Urban Fixed Winter Park / Amtrak Station 5 SunRail SIS Hub No No Yes No Guideway (UFG) terminals, which Advent Health Station 5 SunRail SIS Hub No No No Yes serve as hubs and stations for the urban Lynx Central Station 5 SunRail SIS Station No No No No fixed guideways throughout Florida. Church Street Station 5 SunRail SIS Station No No No No Orlando Health / Amtrak Station 5 SunRail SIS Hub No No Yes No The adjacent table lists the UFG Sand Lake Road 5 SunRail SIS Station No No No No terminals within Florida and whether Meadow Woods Station 5 SunRail SIS Station No No No No they are designated as a SIS Hub or Tupperware Station 5 SunRail SIS Station No No No No SIS Station, based on criteria defined Kissimmee / Amtrak Station 5 SunRail SIS Station No No No No by FDOT.