DOUBLE DISSOLUTION of FEDERAL PARLIAMENT the FIFTH DOUBLE DISSOLUTION by DENIS P

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sir Ninian Stephen Lecture 2003

THE HIGH COURT’S ABANDONMENT OF ‘THE TIME-HONOURED METHODOLOGY OF THE COMMON LAW’ IN ITS INTERPRETATION OF NATIVE TITLE IN MIRRIUWUNG GAJERRONG AND YORTA YORTA Sir Ninian Stephen Annual Lecture 2003 Noel Pearson Law School University of Newcastle 17 March 2003 There are fundamental problems with the way in which the High Court has interpreted native title in Australian law in its two most recent decisions: Mirriuwung Gajerrong1 and Yorta Yorta2. In the space of this lecture I will only be able to deal with three key problems: the court‟s misinterpretation of the definition of native title in section 223(1) of the Native Title Act 1993-1998 (Cth) (“Native Title Act”) the court‟s misinterpretation of how the common law treats traditional indigenous occupants of land when the Crown acquires sovereignty over their land as an injusticiable act of State the court‟s disavowal of native title as a doctrine or body of law within the common law – 1 State of Western Australia v Ward [2002] HCA 28 (8 August 2002). Referred to variously as Ward and Mirriuwung Gajerrong 2 Members of the Yorta Yorta Aboriginal Community v Victoria [2002] HCA 58 (12 December 2002) 1 and its failure to judge the Yorta Yorta people‟s claim in accordance with this body of law I will close with some views about what I think needs to be done in all justice to indigenous Australians. But before I undertake this critique, let me first set out my understanding of what Mabo3 and native title should have meant to Australians. -

1835. EXECUTIVE. *L POST OFFICE DEPARTMENT

1835. EXECUTIVE. *l POST OFFICE DEPARTMENT. Persons employed in the General Post Office, with the annual compensation of each. Where Compen Names. Offices. Born. sation. Dol. cts. Amos Kendall..., Postmaster General.... Mass. 6000 00 Charles K. Gardner Ass't P. M. Gen. 1st Div. N. Jersey250 0 00 SelahR. Hobbie.. Ass't P. M. Gen. 2d Div. N. York. 2500 00 P. S. Loughborough Chief Clerk Kentucky 1700 00 Robert Johnson. ., Accountant, 3d Division Penn 1400 00 CLERKS. Thomas B. Dyer... Principal Book Keeper Maryland 1400 00 Joseph W. Hand... Solicitor Conn 1400 00 John Suter Principal Pay Clerk. Maryland 1400 00 John McLeod Register's Office Scotland. 1200 00 William G. Eliot.. .Chie f Examiner Mass 1200 00 Michael T. Simpson Sup't Dead Letter OfficePen n 1200 00 David Saunders Chief Register Virginia.. 1200 00 Arthur Nelson Principal Clerk, N. Div.Marylan d 1200 00 Richard Dement Second Book Keeper.. do.. 1200 00 Josiah F.Caldwell.. Register's Office N. Jersey 1200 00 George L. Douglass Principal Clerk, S. Div.Kentucky -1200 00 Nicholas Tastet Bank Accountant Spain. 1200 00 Thomas Arbuckle.. Register's Office Ireland 1100 00 Samuel Fitzhugh.., do Maryland 1000 00 Wm. C,Lipscomb. do : for) Virginia. 1000 00 Thos. B. Addison. f Record Clerk con-> Maryland 1000 00 < routes and v....) Matthias Ross f. tracts, N. Div, N. Jersey1000 00 David Koones Dead Letter Office Maryland 1000 00 Presley Simpson... Examiner's Office Virginia- 1000 00 Grafton D. Hanson. Solicitor's Office.. Maryland 1000 00 Walter D. Addison. Recorder, Div. of Acc'ts do.. -

Curriculum Vitae Neil Young Qc

CURRICULUM VITAE NEIL YOUNG QC Address Melbourne Ninian Stephen Chambers (Chambers) Level 38, 140 William Street, Melbourne Vic 3000 Email [email protected] Clerk Michael Green – Ph 03 9225 7864 Sydney New Chambers 126 Phillip Street, Sydney NSW 2000 Email [email protected] Clerk Ian Belshaw – Ph 02 9151 2080 Present position Queen’s Counsel, all Australian States Academic LL.B (1st class honours), University of Melbourne Qualifications LL.M Harvard, 1977 Current Member of the Court of Arbitration for Sport, Geneva, since 1999 professional Director, Victorian Bar Foundation positions Director of the Melbourne Law School Foundation Board Previous Vice-Chairman, Victorian Bar Council, September 1995 to March 1997 professional Director, Barristers’ Chambers Limited, 1994 to 1998 positions Chairman of the Victorian Bar Council, March 1997 to September 1998 President, Australian Bar Association, January 1999 to February 2000 Member, Faculty of Law, University of Melbourne, 1997 2005 Member of the Monash University Faculty of Law Selection Committee, 1998 Member of the JD Advisory Board, Melbourne University, since 1999 Member of the Steering Committee, Forum of Barristers and Advocates of the International Bar Association, January 1999 to February 2000 Member of the Trade Practices and Taxation Law Committees of the Law Council of Australia Chairman of the Continuing Legal Education Committee of the Victorian Bar, 2003 – November 2005 Justice of the Federal Court of Australia, 2005-2007 Page 1 of 2 Admission Details Barrister and Solicitor of the Supreme Court of Victoria since 3 March 1975 Practitioner of the High Court of Australia and the Federal Court since 3 April 1975 Signed the Victorian Bar Roll on 15 March 1979 Admitted as a barrister, or barrister and solicitor in each of the other States of Australia Appointment Appointed one of Her Majesty’s Counsel for the State of Victoria on 27 November to the Inner Bar 1990. -

Votes and Proceedings

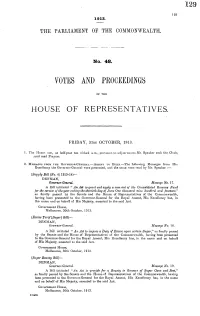

129 129 1913. THE PARLIAMENT OF THE COMMONWEALTH. No. 48. VOTES AND PROCEEDINGS OF THE HOUSE OF REPRESENTATIVES. FRIDAY, 31ST OCTOBER, 1913. 1. The H[ou, mielt, at half-past ten o'clock a.m., puirsunt to adjourniiniit.Mr. Speaker took the Chair, .and read Prayers. 2. MESSAGES FROM THE GOVERNOR-GENERAL.-ASSENT TO BILLS.-The following Messages from His Excellency the Governor-General were presented, and the same were read by IMr.Speaker :- (Supply Bill (No. 4) 1913-14)-- DENMAN, Governor-General. Message No. 17. A Bill intituled " An Act to grant and apply a sum out of the Consolidated Revenue Fund for the service of the year ending the thirtieth day of June One thousand nine hundred and fourteen," as finally passed by the Senate and the House of Representatives of the Commonwealth, having been presented to the -Governor-General for the Royal Assent, His Excellency has, in the name and on behalf of His Majesty, assented to the said Act. Government House, Melbourne, 30th October, 1913. (Excise Tarif'[Sugar] Bill)- DENMAN, Governor-General. Message No. 18. A Bill intituled " An Act to impose a Duty of Excise upon certain Sugar," as finally passed by the Senate and the House of Representatives of the Commonwealth, having been presented to the Governor-General for the Royal Assent, His Excellency has, in the name and on behalf of His Majesty, assented to the said Act. Government House, Melbourne, 30th October, 1913. (Sugar Bounty Bill)- DENMAN, Governor-General. Message No. 19. A Bill intituled "An Act to provide for a Bounty to Growers of Sugar Cane and Beet," as finally passed by the Senate and the House of Representatives of the Commonwealth, having been presented to the Governor-General for the Royal Assent, His Excellency has, in the name and on behalf of His Majesty, assented to the said Act. -

Voting in AUSTRALIAAUSTRALIA Contents

Voting IN AUSTRALIAAUSTRALIA Contents Your vote, your voice 1 Government in Australia: a brief history 2 The federal Parliament 5 Three levels of government in Australia 8 Federal elections 9 Electorates 10 Getting ready to vote 12 Election day 13 Completing a ballot paper 14 Election results 16 Changing the Australian Constitution 20 Active citizenship 22 Your vote, your voice In Australia, citizens have the right and responsibility to choose their representatives in the federal Parliament by voting at elections. The representatives elected to federal Parliament make decisions that affect many aspects of Australian life including tax, marriage, the environment, trade and immigration. This publication explains how Australia’s electoral system works. It will help you understand Australia’s system of government, and the important role you play in it. This information is provided by the Australian Electoral Commission (AEC), an independent statutory authority. The AEC provides Australians with an independent electoral service and educational resources to assist citizens to understand and participate in the electoral process. 1 Government in Australia: a brief history For tens of thousands of years, the heart of governance for Aboriginal and Torres Strait Islander peoples was in their culture. While traditional systems of laws, customs, rules and codes of conduct have changed over time, Aboriginal and Torres Strait Islander peoples continue to share many common cultural values and traditions to organise themselves and connect with each other. Despite their great diversity, all Aboriginal and Torres Strait Islander communities value connection to ‘Country’. This includes spirituality, ceremony, art and dance, family connections, kin relationships, mutual responsibility, sharing resources, respecting law and the authority of elders, and, in particular, the role of Traditional Owners in making decisions. -

Referendum - the Australian Way

THE SEVENTH SIR JOHN QUICK BENDIGO LECTURE REFERENDUM - THE AUSTRALIAN WAY THE RT HON SIR NINIAN STEPHEN SIR JOHN QUICK LECTURE 11 OCTOBER 2000 LA TROBE UNIVERSITY, BENDIGO ISSN 1325 - 0787 The publication of the Year 2000 Lecture is generously supported by Robertson HYETTS Solicitors, Molesworth Chambers, 51 Bull Street, Bendigo. Sir John Quick was a partner in the Bendigo law firm, Quick Hyett and Rymer, later Quick and Hyett, from 1890 to 1912. From 1891 the firm practised from premises at 51 Bull Street. Robertson Hyetts are proud to be associated with the Sir John Quick Lecture. REFERENDUM - THE AUSTRALIAN WAY THE RT HON SIR NINIAN STEPHEN When asked to give this Sir John Quick Lecture I immediately thought of s.128 of our Constitution and its referendum procedure, so closely associated with John Quick, whose memory this series of lectures honours. The most intriguing thing about the Australian form of Constitutional referendum is surely how we ever came to have it formally written into our constitution. In 1900 the referendum was not only a very rare feature of constitutions world wide; it was directly opposed to the principle of representative democracy which Australia had inherited from Britain and which before federation was accepted by all six of the Australian colonies as the normal and very traditional form of government. It was that principle which Edmund Burke described when, in his speech to the electors of Bristol in 1774, he said "you choose a member indeed; but when you have chosen him, he is not a member of Bristol, but he is a Member of Parliament". -

Table of Contents Chronology of Events

Table of Contents Chronology of Events .............................................................................................................................................................. 4 History- 1788 to 1900 .............................................................................................................................................. 5 Plenary ‘sovereign’ Parliaments ........................................................................................................................................ 5 History- Towards Federation- 1880 to 1990 ................................................................................................... 6 Federation (1901)...................................................................................................................................................... 7 Commonwealth of Australia Constitution Act 1900 (Imp) ...................................................................................... 7 Post Federation- 1901 to 1986 (Parliamentary Sovereignty) ................................................................... 8 ‘Balfour Declaration 1926’ [1.3.9E] .................................................................................................................................. 8 Statute of Westminster 1931 (UK) [1.3.11E] ................................................................................................................ 8 The Australia Acts .................................................................................................................................................................. -

Australia's System of Government

61 Australia’s system of government Australia is a federation, a constitutional monarchy and a parliamentary democracy. This means that Australia: Has a Queen, who resides in the United Kingdom and is represented in Australia by a Governor-General. Is governed by a ministry headed by the Prime Minister. Has a two-chamber Commonwealth Parliament to make laws. A government, led by the Prime Minister, which must have a majority of seats in the House of Representatives. Has eight State and Territory Parliaments. This model of government is often referred to as the Westminster System, because it derives from the United Kingdom parliament at Westminster. A Federation of States Australia is a federation of six states, each of which was until 1901 a separate British colony. The states – New South Wales, Victoria, Queensland, Western Australia, South Australia and Tasmania - each have their own governments, which in most respects are very similar to those of the federal government. Each state has a Governor, with a Premier as head of government. Each state also has a two-chambered Parliament, except Queensland which has had only one chamber since 1921. There are also two self-governing territories: the Australian Capital Territory and the Northern Territory. The federal government has no power to override the decisions of state governments except in accordance with the federal Constitution, but it can and does exercise that power over territories. A Constitutional Monarchy Australia is an independent nation, but it shares a monarchy with the United Kingdom and many other countries, including Canada and New Zealand. The Queen is the head of the Commonwealth of Australia, but with her powers delegated to the Governor-General by the Constitution. -

Dialogue Vol. 22, 2/2003

he Academy of the Social Sciences in Australia was established in 1971. T Previously, some of the functions were carried out through the Social Science Research Council of Australia, established in 1942. Elected to the Academy for distinguished contributions to the social sciences, the 382 Fellows of the Academy offer expertise in the fields of accounting, anthropology, demography, economics, economic history, education, geography, history, law, linguistics, philosophy, political science, psychology, social medicine, sociology and statistics. The Academy’s objectives are: · to promote excellence in and encourage the advancement of the social sciences in Australia; · to act as a coordinating group for the promotion of research and teaching in the social sciences; · to foster excellence in research and to subsidise the publication of studies in the social sciences; · to encourage and assist in the formation of other national associations or institutions for the promotion of the social sciences or any branch of them; · to promote international scholarly cooperation and to act as an Australian national member of international organisations concerned with the social sciences; · to act as consultant and adviser in regard to the social sciences; and, · to comment where appropriate on national needs and priorities in the area of the social sciences. These objectives are fulfilled through a program of activities, research projects, independent advice to government and the community, publication and cooperation with fellow institutions both within -

The Supreme Court and Responsible Government: 1864–1930, 40 Neb

Nebraska Law Review Volume 40 | Issue 1 Article 3 1960 The uprS eme Court and Responsible Government: 1864–1930 Roscoe Pound Harvard Law School Follow this and additional works at: https://digitalcommons.unl.edu/nlr Recommended Citation Roscoe Pound, The Supreme Court and Responsible Government: 1864–1930, 40 Neb. L. Rev. 16 (1961) Available at: https://digitalcommons.unl.edu/nlr/vol40/iss1/3 This Article is brought to you for free and open access by the Law, College of at DigitalCommons@University of Nebraska - Lincoln. It has been accepted for inclusion in Nebraska Law Review by an authorized administrator of DigitalCommons@University of Nebraska - Lincoln. The Supreme Court and Responsible Government: 1864-1930* Roscoe Pound* * I. INTRODUCTION A just balance between the general and the local government is of the very essence of a federal polity. What is general and for the general government, and what is local and for the local govern- ment, must be distinguished clearly and maintained consistently. But what is general and what local is not always and everywhere indicated by an exactly drawn line and may vary from time to time or place to place, so that lines have to be redrawn in view of changes in economics, industry, and commerce. Moreover, a federal polity calls for constitutional law. A con- stitution is not a mere body of constitutionally prescribed rules; rules prescribing mode of choice, terms of office, powers, remunera- tion, and causes and modes of removal of officials; nor of rules of policing, definition of offenses, such, for example, as treason, and fixing and imposing penalties. -

Stories of Confederation Reference Guide

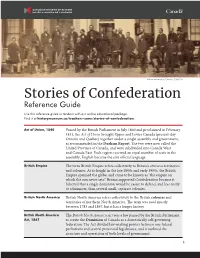

Library and Archives Canada, C-000733 Stories of Confederation Reference Guide Use this reference guide in tandem with our online educational package. Find it at historymuseum.ca/teachers-zone/stories-of-confederation. Act of Union, 1840 Passed by the British Parliament in July 1840 and proclaimed in February 1841, the Act of Union brought Upper and Lower Canada (present-day Ontario and Quebec) together under a single assembly and government, as recommended in the Durham Report. The two were now called the United Province of Canada, and were subdivided into Canada West and Canada East. Each region received an equal number of seats in the assembly; English became the sole official language. British Empire The term British Empire refers collectively to Britain’s overseas territories and colonies. At its height in the late 1800s and early 1900s, the British Empire spanned the globe, and came to be known as “the empire on which the sun never sets.” Britain supported Confederation because it believed that a single dominion would be easier to defend, and less costly to administer, than several small, separate colonies. British North America British North America refers collectively to the British colonies and territories of northern North America. The term was used mostly between 1783 and 1867, but it has a longer history. British North America The British North America Act was a law passed by the British Parliament Act, 1867 to create the Dominion of Canada as a domestically self-governing federation. The Act divided law-making powers between one federal parliament and several provincial legislatures, and it outlined the structure and operations of both levels of government. -

The Constitutional Conventions and Constitutional Change: Making Sense of Multiple Intentions

Harry Hobbs and Andrew Trotter* THE CONSTITUTIONAL CONVENTIONS AND CONSTITUTIONAL CHANGE: MAKING SENSE OF MULTIPLE INTENTIONS ABSTRACT The delegates to the 1890s Constitutional Conventions were well aware that the amendment mechanism is the ‘most important part of a Cons titution’, for on it ‘depends the question as to whether the state shall develop with peaceful continuity or shall suffer alternations of stagnation, retrogression, and revolution’.1 However, with only 8 of 44 proposed amendments passed in the 116 years since Federation, many commen tators have questioned whether the compromises struck by the delegates are working as intended, and others have offered proposals to amend the amending provision. This paper adds to this literature by examining in detail the evolution of s 128 of the Constitution — both during the drafting and beyond. This analysis illustrates that s 128 is caught between three competing ideologies: representative and respons ible government, popular democracy, and federalism. Understanding these multiple intentions and the delicate compromises struck by the delegates reveals the origins of s 128, facilitates a broader understanding of colonial politics and federation history, and is relevant to understanding the history of referenda as well as considerations for the section’s reform. I INTRODUCTION ver the last several years, three major issues confronting Australia’s public law framework and a fourth significant issue concerning Australia’s commitment Oto liberalism and equality have been debated, but at an institutional level progress in all four has been blocked. The constitutionality of federal grants to local government remains unresolved, momentum for Indigenous recognition in the Constitution ebbs and flows, and the prospects for marriage equality and an * Harry Hobbs is a PhD candidate at the University of New South Wales Faculty of Law, Lionel Murphy postgraduate scholar, and recipient of the Sir Anthony Mason PhD Award in Public Law.