Bank Asia Inner Layout.Indd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Agrani Bank Sl No. Name & Address of the Branch Ad Code

AGRANI BANK SL AD CODE NAME & ADDRESS OF THE BRANCH NO. NO. 1 HEAD OFFICE, MOTIJHEEL C/A, DHAKA 0000 2 PRINCIPAL BRANCH, 9/D DILKUSHA C/A, DHAKA 0001 3 BANGA BANDHU AVENUE BRANCH, 32 B.B. AVENUE, DHAKA 0002 4 MOULVI BAZAR BRANCH, 144 MITFORD ROAD, DHAKA. 0003 5 AMIN COURT, MOTIJHEEL, 62/63 MOTIJHEEL C/A, DHAKA 0004 6 RAMNA BRANCH, 18 BANGA BANDHU AVENUE, DHAKA 0005 7 FOREIGN EXCHANGE BRANCH, 1/B RAJUK AVENUE, DHAKA 0006 8 SADARGHAT BRANCH,3/7/1&2 JONSON RD,SADARGHAT, DHAKA. 0007 9 BANANI BRANCH, 26 KAMAL ATATURK AVENUE, BANANI, DHAKA. 0008 10 BANGA BANDHU ROAD BRANCH, 32/1 B.B. AVENUE, NARAYANGONJ 0009 11 COURT ROAD BRANCH, 52/1 B.B.ROAD, NARAYANGONJ 0010 12 FARIDPUR BRANCH, CHAWK BAZAR, FARIDPUR 0011 13 WASA BRANCH, KAWRAN BAZAR, DHAKA. 0012 14 TEJGAON INDUSTRIAL AREA BRANCH, 315/A TEJGAON I/A, DHAKA 0013 15 NAWABPUR ROAD BRANCH, 243-244 NAWABPUR ROAD, DHAKA 0014 16 COMMERCIAL AREA BRANCH, 28 AGRABAD C/A, CHITTAGONG 0015 17 ASADGONJ BRANCH, HAJI AMIR ALI CHOWDHURY ROAD, CHITTAGONG 0016 18 LALDIGHI EAST, 1012/1013 - LALDIGHI EAST, CHITTAGONG 0017 19 AGRABAD BRANCH, JAHAN BUILDING, 24 AGRABAD C/A, CTG 0018 20 COX'S BAZAR BRANCH, COX'S BAZAR 0019 21 RAJGANJ BRANCH, RAJGANJ, COMILLA 0020 22 LALDIGHIRPAR BRANCH, LALDIGHIRPAR, SYLHET 0021 23 CHAUMUHANI BRANCH,D.B.ROAD, BEGUMGONJ, CHAUMUHANI, NOAKHALI 0022 24 SIR IQBAL RAOD BRANCH, 25 SIR IQBAL RAOD, KHULNA 0023 25 JESSORE BRANCH, JESS TOWER, JESSORE 0024 26 CHAWK BAZAR BRANCH, 02/01 CHAWK BAZAR, BARISAL 0025 27 BARA BAZAR BRANCH, N.S. -

Sl. Correspondent / Bank Name SWIFT Code Country

International Division Relationship Management Application( RMA ) Total Correspondent: 156 No. of Country: 36 Sl. Correspondent / Bank Name SWIFT Code Country 1 ISLAMIC BANK OF AFGHANISTAN IBAFAFAKA AFGHANISTAN 2 MIZUHO BANK, LTD. SYDNEY BRANCH MHCBAU2S AUSTRALIA 3 STATE BANK OF INDIA AUSTRALIA SBINAU2S AUSTRALIA 4 KEB HANA BANK, BAHRAIN BRANCH KOEXBHBM BAHRAIN 5 MASHREQ BANK BOMLBHBM BAHRAIN 6 NATIONAL BANK OF PAKISTAN NBPABHBM BAHRAIN 7 AB BANK LIMITED ABBLBDDH BANGLADESH 8 AGRANI BANK LIMITED AGBKBDDH BANGLADESH 9 AL-ARAFAH ISLAMI BANK LTD. ALARBDDH BANGLADESH 10 BANGLADESH BANK BBHOBDDH BANGLADESH 11 BANGLADESH COMMERCE BANK LIMITED BCBLBDDH BANGLADESH BANGLADESH DEVELOPMENT BANK 12 BDDBBDDH BANGLADESH LIMITED (BDBL) 13 BANGLADESH KRISHI BANK BKBABDDH BANGLADESH 14 BANK ASIA LIMITED BALBBDDH BANGLADESH 15 BASIC BANK LIMITED BKSIBDDH BANGLADESH 16 BRAC BANK LIMITED BRAKBDDH BANGLADESH 17 COMMERCIAL BANK OF CEYLON LTD. CCEYBDDH BANGLADESH 18 DHAKA BANK LIMITED DHBLBDDH BANGLADESH 19 DUTCH BANGLA BANK LIMITED DBBLBDDH BANGLADESH 20 EASTERN BANK LIMITED EBLDBDDH BANGLADESH EXPORT IMPORT BANK OF BANGLADESH 21 EXBKBDDH BANGLADESH LTD 22 FIRST SECURITY ISLAMI BANK LIMITED FSEBBDDH BANGLADESH 23 HABIB BANK LTD HABBBDDH BANGLADESH 24 ICB ISLAMI BANK LIMITED BBSHBDDH BANGLADESH INTERNATIONAL FINANCE INVESTMENT 25 IFICBDDH BANGLADESH AND COMMERCE BANK LTD (IFIC BANK) 26 ISLAMI BANK LIMITED IBBLBDDH BANGLADESH 27 JAMUNA BANK LIMITED JAMUBDDH BANGLADESH 28 JANATA BANK LIMITED JANBBDDH BANGLADESH 29 MEGHNA BANK LIMITED MGBLBDDH BANGLADESH 30 MERCANTILE -

Customs E-Payment Compliant Bank Contact

Name of the Executive Name of the Executive Group Email (Will be used for Name of the Bank Designation Department Branch Personal Email Mobile Designation Department Branch Personal Email Mobile (Primary) (Secondary) operational communication) Head Head AB bank Ltd Syed Mahmud Hossain SAVP & RTGS Manager RTGS Central Operation [email protected] 01784293385 Md. Ashifur Rahman SAVP RTGS Central Operation [email protected] 01712104950 [email protected] Office Office Muhammad Mujahid Head Head Al Arafah Bank Ltd. SVP ICT [email protected] +8801556331530 Md. Elias Haider PO BACH and RTGS [email protected] +880764045141 [email protected] Khalid Office Office Bangladesh Development AGM & RTGS Manager Central Accounts Head Engr. Mohammad Moniruzzaman PO & Member-Secretary Head [email protected], Ranjan Kumar Roy [email protected] 01715892419 ITSD 01913040807 [email protected] Bank Ltd. (RTGS Team) Department Office Monr (RTGS Team) Office [email protected] Head Head Bangladesh Krishi Bank Ltd. Md. Atiqur Rahman Senior Principal Officer Treasury Management [email protected] 01718715796 Shah Md. Mainul Hasan Senior Principal Officer Treasury Management [email protected] 01718416875 [email protected] Office Office Head 01711646645, Head Bank Asia Ltd. Syed Md. Ali Reza VP & RTGS Manager PSD [email protected] Mohammad Rezwanul Islam AVP PSD [email protected] 01711363982 [email protected] Office 01819156165 Office Head Head BASIC Bank Ltd. Abu Md. Mofazzal GM ICT [email protected] 01713063335 Md. Golam Sarwar Talukder Manager Back Office Division [email protected] 01711577929 [email protected] Office Office Vice President & RTGS Business Operations Head Business Operations Head Dhaka Bank Ltd. -

Degree Requirement Under the Faculty of Business & Economics, Daffodilinternationaluniversity

INTRODUCTION: This internship report is prepared primarily to fulfill the Bachelor of Business Administration (B.B.A) degree requirement under the Faculty of Business & Economics, DaffodilInternationalUniversity. Back Ground of the Report: The major occupation of the people of Bangladesh is “Krishi”. Krishi is a Bengali word which means “Agriculture”. About 85% of the population depends directly or indirectly on agriculture which contributes a significant portion to GDP. Bangladesh Krishi Bank (BKB) has been established under the Bangladesh Krishi Bank order 1973 (President’s Order No 27 of 1973). BKB is Banking Company under the Banking Company Act-1991. Its Head Office is located at Krishi Bank Bhaban, 83-85 Motijheel Commercial Area, Dhaka-1000, Bangladesh. Krishi bank has started commercial functioning since 1977 to generate more loan able fund from the idle rural and urban savings and invest them for the betterment of our economy. Origin of the report: As a prerequisite for the Bachelor of Business Administration Degree of Daffodil International University, I was required to complete an internship in a suitable business organization and submit a report on my findings. I had been selected to work as an Internee in Bangladesh Krishi Bank, Motijil for a period of 3 months from September 01, 2009 to November 30, 2009. Md Jelayet Hossain Mollaha Human Resources Development Department, Bangladesh Krishi Bank appointed me as an Internee. After discussion and getting consent, I started to work on the project titled “Foreign Exchange Activity of Bangladesh Krishi Bank: A Study on Motijil Branch”. Without practical exposure, theory can never be fruitful. For this reason, B.B.A program has been designed in such a way that a student can get practical knowledge. -

District Bank Branch Location Bank Bank Branch Address DLI Office

DLI Bank Branch DLI District Bank Bank Branch Address A/C Location Office No. Bagerhat Bagerhat Agrani Bank Ltd Bagerhat, Khulna Khulna 737 Bagerhat Bagerhat Pubali Bank Ltd Bagerhat-9300 Khulna 9 Bagerhat Chakshree Bazar Bangladesh Krishi Bank Chakshree Bz. Rampal, Bagerhat Khulna 110 Bagerhat Chital Mari Bazar Bangladesh Krishi Bank Chitalmari Bz.,Bagerhat-9360 Khulna 214 Bagerhat Fakirhat Bangladesh Krishi Bank Fakirhat, Bagerhat-9370 Khulna 293 Bagerhat Mongla Pubali Bank Ltd Mongla Bazar,MadrasaRd.,Bagerhat-9351 Khulna 5 Bagerhat Morelgonj Bangladesh Krishi Bank Morelgonj, Bagerhat-9320 Khulna 281 Bagerhat Raindabazar Bangladesh Krishi Bank Raindabazar,Sarankhola, Bagerhat-9330 Khulna 263 Bagerhat Rampal Bangladesh Krishi Bank Rampal, Bagerhat-9340 Khulna 211 Bagerhat Doiboghohati Bangladesh Krishi Bank Morelgonj, Bagerhat-9320 Khulna 44 Bagerhat Foltita Bangladesh Krishi Bank Kolkolia, Fakirhat, Bagerhat Khulna 30 Bagerhat Mollahat Bangladesh Krishi Bank Mollahat, Bagerhat-9380 Khulna 243 Bagerhat Sannayashibazar Bangladesh Krishi Bank Morelgonj, Bagerhat-9321 Khulna 1 Bagerhat Town Noapara Bangladesh Krishi Bank Town Noapara, Fakirhat, Bagerhat-9370 Khulna 45 Bandarban Baishari Bangladesh Krishi Bank Baishari, Naikhagchari, Bandarban-4660 Chittagong 81 Bandarban Bandarban Pubali Bank Ltd Bandarban-4600 Chittagong 16 Bandarban Lama Bangladesh Krishi Bank Lama, Bandarban Chittagong 453 Barguna Amtoli Bangladesh Krishi Bank Amtoli, Borguna-8710 Barisal 149 Barguna Barguna Pubali Bank Ltd Barguna-8700 Barisal 9 Barguna Betagi Bangladesh -

Initiation and Recent Status of Mobile Banking in Bangladesh

International Journal of Science and Research (IJSR) ISSN: 2319-7064 Impact Factor (2018): 7.426 Initiation and Recent Status of Mobile Banking in Bangladesh Shahjady Sultana Abstract: Mobile Banking is a financial service provided by a bank or a financial organization that allows financial transactions using a mobile device. It’s an independent service that is not connected to any other account; you can call this a bank in your pocket. These transactions are very popular in rural areas, especially for small transactions. There are around 151.82 million people in Bangladesh as of 2012; only 13 percent of them have bank accounts. But more than 95 percent of people in Bangladesh use mobile phones. Banks can now offer banking services to both the rural community and the wider population (without banking transactions) through mobile phones. Day by day this service will become more popular in Bangladesh. Through it, it is possible to take money easily to remote areas. Small transactions are become very easy through mobile banking. Not only in rural areas, but also in urban areas these transactions are equally popular. Since the beginning of 2011, mobile financial service has become quite popular in eight years. The article describes the popularity, benefits and present situation in mobile banking in Bangladesh. Keywords: Meaning of Mobile Banking, Features, Benefits, Present Situation 1. Introduction are usually provided by these operators. If the customer is using smart phone this transaction becomes easier. “Mobile Banking” is a sign of possibility for Bangladesh. Customers can receive these services through an app. It has Mobile Banking idea at first came in October, 2009. -

BA Annual Report 2010.Pdf

The cover theme stands for the inner mechanism, the inner dynamics that represent a bank involved in core banking activities. In other words, a bank doing business in its sphere, providing core services to customers. As a bank, Bank Asia offers the same. As a dynamic bank, we try to figure out the basic characteristics of Bank Asia through different symbols, which are derived from Bank Asia logo. Having realistic and positive perspective towards stakeholders, we define our inherent spirit through some artistic graphical symbols. Each of the symbols describes the basic strength of Bank Asia. At the same time, Bank’s focus on expansion and diversification is signified through these visuals. Table of contents represents the segregation of a single point into different sides. Moreover, the other symbols communicate directly with different aspects of the Bank’s characteristics. Corporate Office Tea Board Building (1st Floor), 111-113 Motijheel C/A Dhaka-1000, Bangladesh Tel: +880 2 716 0938, 717 7031-2, 717 7034 Fax: +880 2 717 5524, SWIFT: BALBBDDH E-mail: [email protected] web: www.bankasia-bd.com, www.bankasia.net Key Achievements Million Taka unless otherwise specified To increase the Deposit base Export customer base at a Change Particulars 2010 2009 increased increased further rate in the 53.21% Total Asset 105,198.05 68,663.20 expansionary market we focused on, in one Deposit 83,601.26 54,832.82 side the liability and 52.47% asset growth, on the 52.47% 85.06% other side, on strong 58.16% Loans and Advances 79,504.23 50,267.92 presence in trade finance. -

Premittances.Pdf

BANGLADESH BANK Statistics Department (BOP Division) Wage Earners’ Remittance during the month of September’2021 (Million USD) Sl. Bank Sep,2021 no State Owned Commercial Banks 01-02,Sep 05-09,Sep 12-16,Sep 19-23,Sep 01-23,Sep 1 Agrani Bank 8.88 46.99 40.12 25.57 121.56 2 Janata Bank 5.30 18.30 14.79 10.40 48.79 3 Rupali Bank 3.72 11.14 8.91 10.13 33.90 4 Sonali Bank 11.93 18.33 29.07 17.47 76.80 5 BASIC Bank 0.01 0.05 0.03 0.02 0.11 6 BDBL 0.00 0.00 0.00 0.00 0.00 Sub Total 29.84 94.81 92.92 63.59 281.16 Specialized Banks 7 Bangladesh Krishi Bank 2.67 11.59 10.17 5.99 30.42 8 RAKUB. 0.00 0.00 0.00 0.00 0.00 Sub Total 2.67 11.59 10.17 5.99 30.42 Private Commercial Banks 9 AB Bank Ltd. 1.70 4.04 2.81 2.52 11.07 10 Al-Arafah Islami Bank Ltd. 3.41 10.83 11.82 10.58 36.64 11 Bangladesh Commerce Bank Ltd. 0.14 0.35 0.27 0.20 0.96 12 Bank Asia Ltd. 9.42 24.57 19.44 15.83 69.26 13 BRAC Bank Ltd. 2.14 9.40 6.76 5.03 23.33 14 Community Bank Bangladesh Ltd. 0.00 0.00 0.00 0.00 0.00 15 Dhaka Bank Ltd. -

International Division Relationship Management Application( RMA ) Total Correspondent: 154 No

International Division Relationship Management Application( RMA ) Total Correspondent: 154 No. of Country: 35 Sl. Correspondent / Bank Name SWIFT Code Country 1 MIZUHO BANK, LTD. SYDNEY BRANCH MHCBAU2S AUSTRALIA 2 STATE BANK OF INDIA AUSTRALIA SBINAU2S AUSTRALIA 3 KEB HANA BANK, BAHRAIN BRANCH KOEXBHBM BAHRAIN 4 MASHREQ BANK BOMLBHBM BAHRAIN 5 NATIONAL BANK OF PAKISTAN NBPABHBM BAHRAIN 6 AB BANK LIMITED ABBLBDDH BANGLADESH 7 AGRANI BANK LIMITED AGBKBDDH BANGLADESH 8 AL-ARAFAH ISLAMI BANK LTD. ALARBDDH BANGLADESH 9 BANK ASIA LIMITED BALBBDDH BANGLADESH 10 BANGLADESH BANK BBHOBDDH BANGLADESH BANGLADESH DEVELOPMENT BANK 11 BDDBBDDH BANGLADESH LIMITED (BDBL) 12 BANGLADESH COMMERCE BANK LIMITED BCBLBDDH BANGLADESH 13 BANGLADESH KRISHI BANK BKBABDDH BANGLADESH 14 BASIC BANK LIMITED BKSIBDDH BANGLADESH 15 BRAC BANK LIMITED BRAKBDDH BANGLADESH 16 SONALI BANK LIMITED BSONBDDH BANGLADESH 17 COMMERCIAL BANK OF CEYLON LTD. CCEYBDDH BANGLADESH 18 DUTCH BANGLA BANK LIMITED DBBLBDDH BANGLADESH 19 DHAKA BANK LIMITED DHBLBDDH BANGLADESH EXPORT IMPORT BANK OF BANGLADESH 20 EXBKBDDH BANGLADESH LTD 21 EASTERN BANK LIMITED EBLDBDDH BANGLADESH 22 THE FARMERS BANK LIMITED FRMSBDDH BANGLADESH 23 FIRST SECURITY ISLAMI BANK LIMITED FSEBBDDH BANGLADESH 24 HABIB BANK LTD HABBBDDH BANGLADESH 25 ISLAMI BANK LIMITED IBBLBDDH BANGLADESH INTERNATIONAL FINANCE INVESTMENT 26 IFICBDDH BANGLADESH AND COMMERCE BANK LTD (IFIC BANK) 27 JAMUNA BANK LIMITED JAMUBDDH BANGLADESH 28 JANATA BANK LIMITED JANBBDDH BANGLADESH 29 MERCANTILE BANK LIMITED MBLBBDDH BANGLADESH 30 MIDLAND -

General Banking of KRISHI BANK

INTERNSHIP REPORT ON A REVIEW OF FINANCIAL SITUATION OF KRISHI BANK Submitted To SYED MAHMUDUR RAHMAN Senior Lecturer BRAC Business School (BBS) [email protected] Submitted by FARDIN SATTER ID: 11304104 [email protected] Submission date: 3rd December, 2015 Letter Of Transmittal 3rd December 2015 Syed Mahmudur Rahman Senior Lecturer Barc Business School, Brac University 66 Mohakhali, Dhaka1212 Subject: Submission of Internship report on General banking at Bangladesh Krishi Bank. Dear sir, I am pleased to inform you about the completion of my internship report on "Financial Situation Of Krishi Bank" and my training under Nazmul Alam , Assistant General Manager, local principal office, Motijheel. This report focuses on my 12-week work experience which has been nothing short of a memorable journey at one of the reputed companies of Bangladesh. Moreover, this internship program provided me with the opportunity to get exposure into the general banking works. On the ending note, your kindness and earnest supervision throughout the semester is what kept me going and I am truly grateful for that. Sincerely, Fardin Satter, ID: 11304104 Department: BBA Brac Business School, Mohakhali, Dhaka. 2 Acknowledgement At first I want I am very Thankful to Almighty Allah because He has give me the patience and strength to finish this report and doing the whole internship program. Then, my special thanks to my honorable teacher, who is my supervisor of my internship, Mr. Syed Mahmudur Rahaman. He helped me very much in doing this report. It was a great experience at Bangladesh Krishi bank, Local principal Office. Here for the first time I have met with corporate environment and I taught a lot from there. -

Impact Assessment of Banglade for Financing Agricultural & N

A Study Report on Impact Assessment of Bangladesh Bank's Re-finance Scheme for Financing Agricultural & Non-farm Rural Borrowers of Bangladesh Krishi Bank and Rajshahi Krishi Unnayan Bank January, 2015 Research Department Bangladesh Bank Head Office, Dhaka i Study Team Md. Julhas Uddin Deputy General Manager Research Department Bangladesh Bank Head Office, Dhaka Phone: +88-02-9530189 (office) +88-01556341621 (cell) E-mail: [email protected] Md. Sanaullah Talukder Tarek Aziz Joint Director Deputy Director Research Department Research Department Bangladesh Bank Bangladesh Bank Head Office, Dhaka Head Office, Dhaka Phone: +88-01711948834 Phone: +88-01717589476 E-mail: [email protected] E-mail: [email protected] Field Survey Teams Survey Responsibility in Name of Official Designation Team the Study Team Deputy General Manager 1. Md. Julhas Uddin Team Leader Research Department Deputy Director Team-A 2. Md. Shamsher Ali Member Research Department Assistant Director 3. Ataur Rahaman Member Research Department Deputy General Manager 1. Md. Mostafizur Rahman Sarder Team Leader Research Department Joint Director Team-B 2. Md. Sanaullah Talukder Member Research Department Deputy Director 3. Md. Nazrul Islam Member Department of Banking Inspection 3 Deputy General Manager 1. Md. Golam Moula Team Leader Research Department Deputy Director Team-C 2. Mohammad Abdullah Al Masum Agricultural Credit & Financial Member Inclusion Department Deputy Director 3. Tarek Aziz Member Research Department ii Acknowledgement This study was initiated as per the instruction of the 344th Board of Directors’ Meeting of Bangladesh Bank (BB) to find out the impact(s) of the refinance scheme of BB through assessing the economic well-being of the people who have taken loan from Bangladesh Krishi Bank (BKB) and Rajshahi Krishi Unnayan Bank (RAKUB). -

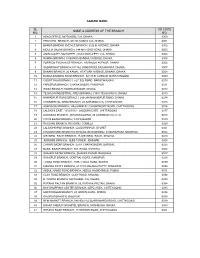

Bangladesh Bank Roll Enrolment Name of Successful Candidates & Father's Name of Center No

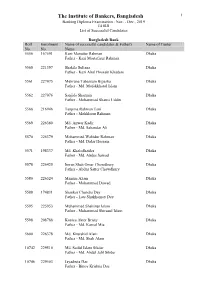

The Institute of Bankers, Bangladesh 1 Banking Diploma Examination : Nov. - Dec., 2019 JAIBB List of Successful Candidates Bangladesh Bank Roll Enrolment Name of successful candidates & Father's Name of Center No. No. Name 5556 167591 Kazi Masudur Rahman Dhaka Father - Kazi Mostafizur Rahman 5560 221397 Shakila Sultana Dhaka Father - Kazi Abul Hossain Khadem 5561 227075 Mehruna Tabassum Bipasha Dhaka Father - Md. Mofakkharul Islam 5562 227076 Sanjida Sharmin Dhaka Father - Mohammad Shams Uddin 5568 216946 Tanjima Rahman Tani Dhaka Father - Mokhlesur Rahman 5569 226380 Md. Anwar Kadir Dhaka Father - Md. Sakandar Ali 5570 226379 Mohammed Wahidur Rahman Dhaka Father - Md. Didar Hossain 5571 198337 Md. Khaledhaider Dhaka Father - Md. Abdus Samad 5578 226425 Imran Shah Omar Chowdhury Dhaka Father - Abdus Satter Chowdhury 5580 226524 Mamun Azam Dhaka Father - Mohammed Dawed 5588 174831 Shankar Chandra Dey Dhaka Father - Late Shukhamoy Dey 5595 225953 Muhammad Shahinur Islam Dhaka Father - Muhammad Shirazul Islam 5598 208788 Konica Akter Bristy Dhaka Father - Md. Kamal Mia 5600 226378 Md. Khurshid Alam Dhaka Father - Md. Shah Alam 10742 229510 Md. Saiful Islam Sikdar Dhaka Father - Md. Abdul Jalil Sikder 10746 229503 Jayadruta Das Dhaka Father - Binoy Krishna Das The Institute of Bankers, Bangladesh 2 Banking Diploma Examination : Nov. - Dec., 2019 JAIBB List of Successful Candidates Bangladesh Bank Roll Enrolment Name of successful candidates & Father's Name of Center No. No. Name 10747 229502 Rakesh Saha Dhaka Father - Chitta Ranjan Saha 10748 229505 Muhammad Saddam Hosain Dhaka Father - Md. Mokter Hosain 10752 217317 Dipu Sana Dhaka Father - Tapan Kumar Sana 12007 191409 Fahmida Akhter Dhaka Father - G. M. Zakaria 12015 86755 Md.