BA Annual Report 2010.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

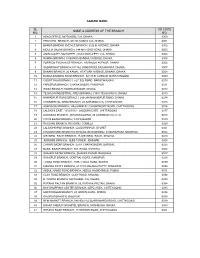

Agrani Bank Sl No. Name & Address of the Branch Ad Code

AGRANI BANK SL AD CODE NAME & ADDRESS OF THE BRANCH NO. NO. 1 HEAD OFFICE, MOTIJHEEL C/A, DHAKA 0000 2 PRINCIPAL BRANCH, 9/D DILKUSHA C/A, DHAKA 0001 3 BANGA BANDHU AVENUE BRANCH, 32 B.B. AVENUE, DHAKA 0002 4 MOULVI BAZAR BRANCH, 144 MITFORD ROAD, DHAKA. 0003 5 AMIN COURT, MOTIJHEEL, 62/63 MOTIJHEEL C/A, DHAKA 0004 6 RAMNA BRANCH, 18 BANGA BANDHU AVENUE, DHAKA 0005 7 FOREIGN EXCHANGE BRANCH, 1/B RAJUK AVENUE, DHAKA 0006 8 SADARGHAT BRANCH,3/7/1&2 JONSON RD,SADARGHAT, DHAKA. 0007 9 BANANI BRANCH, 26 KAMAL ATATURK AVENUE, BANANI, DHAKA. 0008 10 BANGA BANDHU ROAD BRANCH, 32/1 B.B. AVENUE, NARAYANGONJ 0009 11 COURT ROAD BRANCH, 52/1 B.B.ROAD, NARAYANGONJ 0010 12 FARIDPUR BRANCH, CHAWK BAZAR, FARIDPUR 0011 13 WASA BRANCH, KAWRAN BAZAR, DHAKA. 0012 14 TEJGAON INDUSTRIAL AREA BRANCH, 315/A TEJGAON I/A, DHAKA 0013 15 NAWABPUR ROAD BRANCH, 243-244 NAWABPUR ROAD, DHAKA 0014 16 COMMERCIAL AREA BRANCH, 28 AGRABAD C/A, CHITTAGONG 0015 17 ASADGONJ BRANCH, HAJI AMIR ALI CHOWDHURY ROAD, CHITTAGONG 0016 18 LALDIGHI EAST, 1012/1013 - LALDIGHI EAST, CHITTAGONG 0017 19 AGRABAD BRANCH, JAHAN BUILDING, 24 AGRABAD C/A, CTG 0018 20 COX'S BAZAR BRANCH, COX'S BAZAR 0019 21 RAJGANJ BRANCH, RAJGANJ, COMILLA 0020 22 LALDIGHIRPAR BRANCH, LALDIGHIRPAR, SYLHET 0021 23 CHAUMUHANI BRANCH,D.B.ROAD, BEGUMGONJ, CHAUMUHANI, NOAKHALI 0022 24 SIR IQBAL RAOD BRANCH, 25 SIR IQBAL RAOD, KHULNA 0023 25 JESSORE BRANCH, JESS TOWER, JESSORE 0024 26 CHAWK BAZAR BRANCH, 02/01 CHAWK BAZAR, BARISAL 0025 27 BARA BAZAR BRANCH, N.S. -

INTERNATIONAL FINANCE INVESTMENT and COMMERCE BANK LIMITED Audited Financial Statements As at and for the Year Ended 31 December 2019

INTERNATIONAL FINANCE INVESTMENT AND COMMERCE BANK LIMITED Audited Financial Statements as at and for the year ended 31 December 2019 INTERNATIONAL FINANCE INVESTMENT AND COMMERCE BANK LIMITED Consolidated Balance Sheet as at 31 December 2019 Amount in BDT Particulars Note 31 December 2019 31 December 2018 PROPERTY AND ASSETS Cash 18,056,029,773 16,020,741,583 Cash in hand (including foreign currency) 3.a 2,872,338,679 2,899,030,289 Balance with Bangladesh Bank and its agent bank(s) (including foreign currency) 3.b 15,183,691,094 13,121,711,294 Balance with other banks and financial institutions 4.a 5,637,834,204 8,118,980,917 In Bangladesh 4.a(i) 4,014,719,294 6,823,590,588 Outside Bangladesh 4.a(ii) 1,623,114,910 1,295,390,329 Money at call and on short notice 5 910,000,000 3,970,000,000 Investments 47,216,443,756 32,664,400,101 Government securities 6.a 41,369,255,890 27,258,506,647 Other investments 6.b 5,847,187,866 5,405,893,454 Loans and advances 232,523,441,067 210,932,291,735 Loans, cash credit, overdrafts etc. 7.a 221,562,693,268 198,670,768,028 Bills purchased and discounted 8.a 10,960,747,799 12,261,523,707 Fixed assets including premises, furniture and fixtures 9.a 6,430,431,620 5,445,835,394 Other assets 10.a 9,606,537,605 9,003,060,522 Non-banking assets 11 373,474,800 373,474,800 Total assets 320,754,192,825 286,528,785,052 LIABILITIES AND CAPITAL Liabilities Borrowing from other banks, financial institutions and agents 12.a 8,215,860,335 9,969,432,278 Subordinated debt 13 2,800,000,000 3,500,000,000 Deposits and other -

“E-Business and on Line Banking in Bangladesh: an Analysis”

“E-Business and on line banking in Bangladesh: an Analysis” AUTHORS Muhammad Mahboob Ali ARTICLE INFO Muhammad Mahboob Ali (2010). E-Business and on line banking in Bangladesh: an Analysis. Banks and Bank Systems, 5(2-1) RELEASED ON Wednesday, 07 July 2010 JOURNAL "Banks and Bank Systems" FOUNDER LLC “Consulting Publishing Company “Business Perspectives” NUMBER OF REFERENCES NUMBER OF FIGURES NUMBER OF TABLES 0 0 0 © The author(s) 2021. This publication is an open access article. businessperspectives.org Banks and Bank Systems, Volume 5, Issue 2, 2010 Muhammad Mahboob Ali (Bangladesh) E-business and on-line banking in Bangladesh: an analysis Abstract E-business has created tremendous opportunity all over the globe. On-line banking can act as a complementary factor of e-business. Bangladesh Bank has recently argued to introduce automated clearing house system. This pushed up- ward transition from the manual banking system to the on-line banking system. The study has been undertaken to ob- serve present status of the e-business and as its complementary factor on-line banking system in Bangladesh. The arti- cle analyzes the data collected from Bangladeshi banks up to February 2010 and also used snowball sampling tech- niques to gather answer from the five hundred respondents who have already been using on-line banking system on the basis of a questionnaire which was prepared for this study purpose. The study found that dealing officials of the banks are not well conversant about their desk work. The author observed that the country can benefit from successful utiliza- tion of e-business as this will help to enhance productivity. -

Sena Kalyan Bhaban Branch

Sena Kalyan Bhaban Branch 9 Chapter 2: Banking Sector in Bangladesh 2.1 Definition of Bank: Generally speaking bank is referred to an organization that deals in money. The definition of bank can be as follows. Provided by Famous Encyclopedia: A commercial banker is a dealer in money in substitutes for money, such as check or bill of exchange. – New Encyclopedia Britannica Establishment for custody of money, which it pays out on customers order. – The New Oxford Encyclopedia Dictionary Provided by and Ordinances: Banker includes a body of person whether incorporated or not, who carry on the business of banking. – English Bills of Exchange Act - 1882 A bank is a person or corporation carrying on bonafide banking business. – English Finance Act Provided by Banking Institutes: A bank performs an essentially distributive task, service or acts as an intermediary between borrowers & lenders. In broader sense, however, a bank can be considered the heart of a complex financial structure. – American Institute of Banking Stated very simply, banks deal in money and in that connection offer certain related financial services. – Harold Wallgren for American Bankers Association The above-mentioned characteristics sketched to outline the definition of a “bank” are nowadays shared by a lot of different types of financial institution. Therefore, because banking activities now overlap many diverse businesses, we will consider a variety of modern financial institutions 10 – including commercial banks but also savings-and-loan associations, brokerage firms, and mutual funds – as “banks”. 2.2 Objectives of a Bank: The objectives of a bank can be looked at from three different perspectives of the three key parties to the banking activities: the bank owner, the Government, and the bank clients. -

Sl. Correspondent / Bank Name SWIFT Code Country

International Division Relationship Management Application( RMA ) Total Correspondent: 156 No. of Country: 36 Sl. Correspondent / Bank Name SWIFT Code Country 1 ISLAMIC BANK OF AFGHANISTAN IBAFAFAKA AFGHANISTAN 2 MIZUHO BANK, LTD. SYDNEY BRANCH MHCBAU2S AUSTRALIA 3 STATE BANK OF INDIA AUSTRALIA SBINAU2S AUSTRALIA 4 KEB HANA BANK, BAHRAIN BRANCH KOEXBHBM BAHRAIN 5 MASHREQ BANK BOMLBHBM BAHRAIN 6 NATIONAL BANK OF PAKISTAN NBPABHBM BAHRAIN 7 AB BANK LIMITED ABBLBDDH BANGLADESH 8 AGRANI BANK LIMITED AGBKBDDH BANGLADESH 9 AL-ARAFAH ISLAMI BANK LTD. ALARBDDH BANGLADESH 10 BANGLADESH BANK BBHOBDDH BANGLADESH 11 BANGLADESH COMMERCE BANK LIMITED BCBLBDDH BANGLADESH BANGLADESH DEVELOPMENT BANK 12 BDDBBDDH BANGLADESH LIMITED (BDBL) 13 BANGLADESH KRISHI BANK BKBABDDH BANGLADESH 14 BANK ASIA LIMITED BALBBDDH BANGLADESH 15 BASIC BANK LIMITED BKSIBDDH BANGLADESH 16 BRAC BANK LIMITED BRAKBDDH BANGLADESH 17 COMMERCIAL BANK OF CEYLON LTD. CCEYBDDH BANGLADESH 18 DHAKA BANK LIMITED DHBLBDDH BANGLADESH 19 DUTCH BANGLA BANK LIMITED DBBLBDDH BANGLADESH 20 EASTERN BANK LIMITED EBLDBDDH BANGLADESH EXPORT IMPORT BANK OF BANGLADESH 21 EXBKBDDH BANGLADESH LTD 22 FIRST SECURITY ISLAMI BANK LIMITED FSEBBDDH BANGLADESH 23 HABIB BANK LTD HABBBDDH BANGLADESH 24 ICB ISLAMI BANK LIMITED BBSHBDDH BANGLADESH INTERNATIONAL FINANCE INVESTMENT 25 IFICBDDH BANGLADESH AND COMMERCE BANK LTD (IFIC BANK) 26 ISLAMI BANK LIMITED IBBLBDDH BANGLADESH 27 JAMUNA BANK LIMITED JAMUBDDH BANGLADESH 28 JANATA BANK LIMITED JANBBDDH BANGLADESH 29 MEGHNA BANK LIMITED MGBLBDDH BANGLADESH 30 MERCANTILE -

Procedure of Open Foreign Currency Account.Pdf

Embassy of Bangladesh Washington DC Wage Earner Development Bond Foreign Currency Foreign Currency Accounts Specimern Signature Specimern Signature FC Account Opening Form and Specimen Signature Extension [email protected] Diplomatic Bag /DHL/Fedex English Version The Government of the People’s Republic of Bangladesh have introduced special saving facilities for Non Resident Bangladeshis and also foreigner’s of Bangladeshi decent. Wage Earner Development Bond : Most profitable fixed deposit investment “Wage Earner Development Bond” for Non Resident Bangladeshi’s and Foreigners of Bangladeshi decent introduced by the Government of the People’s Republic of Bangladesh. Compound rate of profit is 12.00% per annum. Tk. 25,000 become Tk. 44,750 with profit after 5 years Tk. 50,000 become Tk. 89,500 with profit after 5 years Tk. 1,00,000 become Tk. 1,79,000 with profit after 5 years Tk. 5,00,000 become Tk. 8,95,000 with profit after 5 years Profits could be withdrawn at a rate of Tk. 1000.00 per month for every Tk. 100000.00. For withdrawal of profit simple rate is applicable. Nominee is entitled to 30% to 50% of invested amount as a death risk insurance at no extra charge in case of death of the bond owner. No income tax is levied on the initial investment or profits thereof. Initial investment amount could be transferred back in foreign currency. If encashed before maturity you will get interest at following rate : a. Before six month no interest b. After six month and before 1 year : 9% c. After 1 year and before 2 years : 10% d. -

Customs E-Payment Compliant Bank Contact

Name of the Executive Name of the Executive Group Email (Will be used for Name of the Bank Designation Department Branch Personal Email Mobile Designation Department Branch Personal Email Mobile (Primary) (Secondary) operational communication) Head Head AB bank Ltd Syed Mahmud Hossain SAVP & RTGS Manager RTGS Central Operation [email protected] 01784293385 Md. Ashifur Rahman SAVP RTGS Central Operation [email protected] 01712104950 [email protected] Office Office Muhammad Mujahid Head Head Al Arafah Bank Ltd. SVP ICT [email protected] +8801556331530 Md. Elias Haider PO BACH and RTGS [email protected] +880764045141 [email protected] Khalid Office Office Bangladesh Development AGM & RTGS Manager Central Accounts Head Engr. Mohammad Moniruzzaman PO & Member-Secretary Head [email protected], Ranjan Kumar Roy [email protected] 01715892419 ITSD 01913040807 [email protected] Bank Ltd. (RTGS Team) Department Office Monr (RTGS Team) Office [email protected] Head Head Bangladesh Krishi Bank Ltd. Md. Atiqur Rahman Senior Principal Officer Treasury Management [email protected] 01718715796 Shah Md. Mainul Hasan Senior Principal Officer Treasury Management [email protected] 01718416875 [email protected] Office Office Head 01711646645, Head Bank Asia Ltd. Syed Md. Ali Reza VP & RTGS Manager PSD [email protected] Mohammad Rezwanul Islam AVP PSD [email protected] 01711363982 [email protected] Office 01819156165 Office Head Head BASIC Bank Ltd. Abu Md. Mofazzal GM ICT [email protected] 01713063335 Md. Golam Sarwar Talukder Manager Back Office Division [email protected] 01711577929 [email protected] Office Office Vice President & RTGS Business Operations Head Business Operations Head Dhaka Bank Ltd. -

Degree Requirement Under the Faculty of Business & Economics, Daffodilinternationaluniversity

INTRODUCTION: This internship report is prepared primarily to fulfill the Bachelor of Business Administration (B.B.A) degree requirement under the Faculty of Business & Economics, DaffodilInternationalUniversity. Back Ground of the Report: The major occupation of the people of Bangladesh is “Krishi”. Krishi is a Bengali word which means “Agriculture”. About 85% of the population depends directly or indirectly on agriculture which contributes a significant portion to GDP. Bangladesh Krishi Bank (BKB) has been established under the Bangladesh Krishi Bank order 1973 (President’s Order No 27 of 1973). BKB is Banking Company under the Banking Company Act-1991. Its Head Office is located at Krishi Bank Bhaban, 83-85 Motijheel Commercial Area, Dhaka-1000, Bangladesh. Krishi bank has started commercial functioning since 1977 to generate more loan able fund from the idle rural and urban savings and invest them for the betterment of our economy. Origin of the report: As a prerequisite for the Bachelor of Business Administration Degree of Daffodil International University, I was required to complete an internship in a suitable business organization and submit a report on my findings. I had been selected to work as an Internee in Bangladesh Krishi Bank, Motijil for a period of 3 months from September 01, 2009 to November 30, 2009. Md Jelayet Hossain Mollaha Human Resources Development Department, Bangladesh Krishi Bank appointed me as an Internee. After discussion and getting consent, I started to work on the project titled “Foreign Exchange Activity of Bangladesh Krishi Bank: A Study on Motijil Branch”. Without practical exposure, theory can never be fruitful. For this reason, B.B.A program has been designed in such a way that a student can get practical knowledge. -

Financial Statements

FINANCIAL STATEMENTS 264 Annual Integrated Report 2019 265 Bank Asia Limited Independent Auditor’s Report to the Shareholders of Bank Asia Limited Report on the Audit of the Consolidated and Separate Financial Statements Opinion We have audited the consolidated financial statements of Bank Asia Limited and its subsidiaries (the “Group”), as well as the separate financial statements of Bank Asia Limited (the “Bank”),which comprise the consolidated and separate balance sheets as at 31 December 2019, and the consolidated and separate profit and loss accounts, consolidated and separate changes in equity and consolidated and separate cash flow statement for the year then ended, and notes to the consolidated and separate financial statements, including a summary of significant accounting policies. In our opinion, the accompanying consolidated financial statements of the group and separate financial statement of the Bank give true and fair view of the consolidated balance sheet of the group and the separate balance sheet of the Bank as at 31 December 2019, and of its consiladated and separate profit and loss accounts and its consolidated and separate cash flows for the year then ended in accordance with International Financial Reporting Standards (IFRSs) as explained in note 02-03. Basis for Opinion We conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilities under those standards are further described in the Auditors’ Responsibilities for the Audit of the Consolidated and Separate Financial Statements section of our report. We are independent of the Group and the Bank in accordance with the International Ethics Standards Board for Accountants’ Code of Ethics for Professional Accountants (IESBA Code), Bangladesh Securities and Exchange Commission (BSEC) and Bangladesh Bank, and we have fulfilled our other ethical responsibilities in accordance with the IESBA Code and the Institute of Chartered Accountants of Bangladesh (ICAB) Bye Laws. -

Internship Report: Profit Maximization and CSR Activities of NCC Bank

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by BRAC University Institutional Repository Internship Report: Profit Maximization and CSR activities of NCC Bank Submitted To Feihan Ahsan Lecturer, BRAC University Submitted By Rubaiyat Hossain ID: 13104255 Department: BBS Letter of Transmittal 16th May, 2016 Feihan Ahsan Lecturer, BRAC Business School Subject: Letter of Transmittal Dear Sir, With humble submission, I would like to state that I am Rubaiyat Hossain, (ID-13104255) have prepared the project report on “Profit Maximization and CSR Activities of NCC Bank” which was prepared based on my internship experience at NCC bank as a part of my final Project which is an essential part of my graduation program. I think it was a great opportunity for me to work in NCC bank as I got an idea about the overall banking activities. Though I joined as an HR intern but I had shuffled departments in every alternative week and have worked closely with all departments. I would like to express my gratitude to my Supervisor, Mr. Feihan Ahsan. Your steady thought and guidelines on the report helped me to structure the report and I would also like to thank, Md. Alauddin, Senior HR Officer at NCC Bank who allowed me his time, responded to my queries and also helped me in report preparation. It would be really grateful if you could provide your discreet approval on the report. Yours’ sincerely, Rubaiyat Hossain ID: 13104255 Department: BBS EXECUTIVE SUMMERY To provide a student with job acquaintance and a prospect of move of hypothetical learning into genuine experience, an entry level position is an absolute necessity. -

Internship Report Customer Satisfaction Towards Online Banking Service of Bank Asia Limited, Banani Branch Course Code

Internship Report Customer Satisfaction Towards Online Banking Service of Bank Asia Limited, Banani Branch Course code: BUS 400 Spring-2019 Submitted to, Ms. Mahreen Mamoon Assistant Professor BRAC University Business School BRAC University Submitted by, Ayesha Sumaya ID: 15104193 BRAC University Business School BRAC University Date of Submission: 29th April, 2019 Letter of Transmittal 29th April 2019 Ms. Mahreen Mamoon Assistant Professor BRAC Business School BRAC University 66 Mohakhali, Dhaka Subject: Submission of Internship Report for completing BBA Program Dear Madam, I would like to thank you for being so kindtowards me and providing me the opportunity of successfully completing the report on the topic of customer satisfaction towards online banking of bank Asia Limited, Banani Branch. I have tried my level best to provide the relevant information in my report. Throughout the journey of my internship program you have been very grateful and helpful to me. Without your support the report would not be able to complete. I hope and pray you will consider my mistakes and errors in this report. I would be very grateful if you accept my report and suggest me what can I change for the sake of the report. Thank you so much for your immense support and valuable time. Sincerely yours, Ayesha Sumaya ID: 15104193 BRAC Business School BRAC University Letter of endorsement This is to inform you that, Ayesha Sumaya, ID: 15104193, BBA program, BRAC University Business School, BRAC University has been submitted her internship report titled on “Customer attitude toward Online banking service of Bank Asia Limited , Banani Branch” to complete the Bachelor of Business Administration. -

District Bank Branch Location Bank Bank Branch Address DLI Office

DLI Bank Branch DLI District Bank Bank Branch Address A/C Location Office No. Bagerhat Bagerhat Agrani Bank Ltd Bagerhat, Khulna Khulna 737 Bagerhat Bagerhat Pubali Bank Ltd Bagerhat-9300 Khulna 9 Bagerhat Chakshree Bazar Bangladesh Krishi Bank Chakshree Bz. Rampal, Bagerhat Khulna 110 Bagerhat Chital Mari Bazar Bangladesh Krishi Bank Chitalmari Bz.,Bagerhat-9360 Khulna 214 Bagerhat Fakirhat Bangladesh Krishi Bank Fakirhat, Bagerhat-9370 Khulna 293 Bagerhat Mongla Pubali Bank Ltd Mongla Bazar,MadrasaRd.,Bagerhat-9351 Khulna 5 Bagerhat Morelgonj Bangladesh Krishi Bank Morelgonj, Bagerhat-9320 Khulna 281 Bagerhat Raindabazar Bangladesh Krishi Bank Raindabazar,Sarankhola, Bagerhat-9330 Khulna 263 Bagerhat Rampal Bangladesh Krishi Bank Rampal, Bagerhat-9340 Khulna 211 Bagerhat Doiboghohati Bangladesh Krishi Bank Morelgonj, Bagerhat-9320 Khulna 44 Bagerhat Foltita Bangladesh Krishi Bank Kolkolia, Fakirhat, Bagerhat Khulna 30 Bagerhat Mollahat Bangladesh Krishi Bank Mollahat, Bagerhat-9380 Khulna 243 Bagerhat Sannayashibazar Bangladesh Krishi Bank Morelgonj, Bagerhat-9321 Khulna 1 Bagerhat Town Noapara Bangladesh Krishi Bank Town Noapara, Fakirhat, Bagerhat-9370 Khulna 45 Bandarban Baishari Bangladesh Krishi Bank Baishari, Naikhagchari, Bandarban-4660 Chittagong 81 Bandarban Bandarban Pubali Bank Ltd Bandarban-4600 Chittagong 16 Bandarban Lama Bangladesh Krishi Bank Lama, Bandarban Chittagong 453 Barguna Amtoli Bangladesh Krishi Bank Amtoli, Borguna-8710 Barisal 149 Barguna Barguna Pubali Bank Ltd Barguna-8700 Barisal 9 Barguna Betagi Bangladesh