Natural Gas Consumption in the CIS and the Quest for Efficiency

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Specialised Asset Management

specialised research and investment group Russian Power: The Greatest Sector Reform on Earth www.sprin-g.com November 2010 specialised research and investment group Specialised Research and Investment Group (SPRING) Manage Investments in Russian Utilities: - HH Generation - #1 among EM funds (12 Months Return)* #2 among EM funds (Monthly return)** David Herne - Portfolio Manager Previous positions: Member, Board of Directors - Unified Energy Systems, Federal Grid Company, RusHydro, TGK-1, TGK-2, TGK-4, OGK-3, OGK-5, System Operator, Aeroflot, etc. (2000-2008) Chairman, Committee for Strategy and Reform - Unified Energy Systems (2001-2008) Boston Consulting Group, Credit Suisse First Boston, Brunswick. * Top 10 (by 12 Months Return) Emerging Markets (E. Europe/CIS) funds in the world by BarclayHedge as of 30 September 2010 ** Top 10 (by Monthly Return) Emerging Markets (E. Europe/CIS) funds in the world by BarclayHedge as of 31 August 2010 2 specialised research and investment group Russian power sector reform: Privatization Pre-Reform Post-Reform Government Government 52% 1 RusHydro 1 FSK RAO ES RAO UES 58% 79% hydro generation HV distribution 53% Far East Holding control control Independent energos 53% 1 MRSK Holding 14 TGKs 0% (Bashkir, Novosibirsk, ~72 energos 0% generation (CHP) generation Irkutsk, Tat) 35 federal plants transmission thermal 11 MRSK distribution 51% hydro LV distribution 0% ~72 SupplyCos supply 6 OGKs other 0% generation 45% InterRAO 0% ~100 RepairCos Source: UES, Companies Data, SPRING research 3 specialised research -

Energy Without Borders

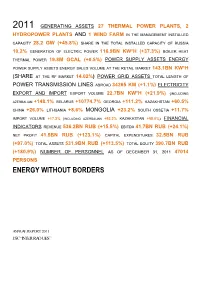

2011 GENERATING ASSETS 27 THERMAL POWER PLANTS, 2 HYDROPOWER PLANTS AND 1 WIND FARM IN THE MANAGEMENT INSTALLED CAPACITY 28.2 GW (+45.8%) SHARE IN THE TOTAL INSTALLED CAPACITY OF RUSSIA 10.2% GENERATION OF ELECTRIC POWER 116.9BN KW*H (+37.3%) BOILER HEAT THERMAL POWER 19.8M GCAL (+0.5%) POWER SUPPLY ASSETS ENERGY POWER SUPPLY ASSETS ENERGY SALES VOLUME AT THE RETAIL MARKET 143.1BN KW*H (SHARE AT THE RF MARKET 14.02%) POWER GRID ASSETS TOTAL LENGTH OF POWER TRANSMISSION LINES ABROAD 34265 KM (+1.1%) ELECTRICITY EXPORT AND IMPORT EXPORT VOLUME 22.7BN KW*H (+21.9%) (INCLUDING AZERBAIJAN +148.1% BELARUS +10774.7% GEORGIA +111.2% KAZAKHSTAN +60.5% CHINA +26.0% LITHUANIA +8.6% MONGOLIA +23.2% SOUTH OSSETIA +11.7% IMPORT VOLUME +17.2% (INCLUDING AZERBAIJAN +93.2% KAZAKHSTAN +58.0%) FINANCIAL INDICATORS REVENUE 536.2BN RUB (+15.5%) EBITDA 41.7BN RUB (+24.1%) NET PROFIT 41.5BN RUB (+123.1%) CAPITAL EXPENDITURES 32.5BN RUB (+97.0%) TOTAL ASSETS 531.9BN RUB (+113.5%) TOTAL EQUITY 390.7BN RUB (+180.9%) NUMBER OF PERSONNEL AS OF DECEMBER 31, 2011 47014 PERSONS ENERGY WITHOUT BORDERS ANNUAL REPORT 2011 JSC “INTER RAO UES” Contents ENERGY WITHOUT BORDERS.........................................................................................................................................................1 ADDRESS BY THE CHAIRMAN OF THE BOARD OF DIRECTORS AND THE CHAIRMAN OF THE MANAGEMENT BOARD OF JSC “INTER RAO UES”..............................................................................................................8 1. General Information about the Company and its Place in the Industry...........................................................10 1.1. Brief History of the Company......................................................................................................................... 10 1.2. Business Model of the Group..........................................................................................................................12 1.4. -

a Leading Energy Company in the Nordic Area

- a leading energy company in the Nordic area Presentation for investors September 2007 Disclaimer This presentation does not constitute an invitation to underwrite, subscribe for, or otherwise acquire or dispose of any Fortum shares. Past performance is no guide to future performance, and persons needing advice should consult an independent financial adviser. 2 • Fortum today • European power markets • Russia • Financials / outlook • Supplementary material 3 Fortum's strategy Fortum focuses on the Nordic and Baltic Rim markets as a platform for profitable growth Become the leading Become the power and heat energy supplier company of choice Benchmark business performance 4 Presence in focus market areas Nordic Generation 53.2 TWh Electricity sales 60.2 TWh Distribution cust. 1.6 mill. Electricity cust. 1.3 mill. NW Russia Heat sales 20.1 TWh (in associated companies) Power generation ~6 TWh Heat production ~7 TWh Baltic countries Heat sales 1.0 TWh Poland Distribution cust. 23,000 Heat sales 3.6 TWh Electricity sales 8 GWh 2006 numbers 5 Fortum Business structure Fortum Markets Fortum's comparable Large operating profit in 2006 NordicNordic customers EUR 1,437 million Fortum wholesalewholesale Small Power marketmarket customers Generation Nord Pool and Markets 0% bilateral Other retail companies Deregulated Distribution 17% Regulated Transmission Power and system Fortum Heat 17% Generation services Distribution 66% 6 Strong financial position ROE (%) EPS, cont. (EUR) Total assets (EUR billion) 20 1.50 1.42 20.0 16.8 17.5 17.3 1.22 18 15.1 -

QUARTERLY REPORT Public Joint-Stock Company

QUARTERLY REPORT Public Joint-Stock Company Federal Hydrogeneration Company RusHydro Code of the Issuer: 55038-E for Q4 2015 Address of the Issuer: 43 Dubrovinskogo St., bldg. 1, Krasnoyarsk, Krasnoyarsk Krai, 660017. The information contained herein is subject to disclosure pursuant to the securities legislation of the Russian Federation Chairman of the Management Board ― General Director ___________________ N.G. Shulginov Date: 15.04.2016 signature _________________ D.V. Finkel Chief Accountant signature Date: 15.04.2016 Contact person: Roman Yurievich Sorokin, Head of Methodology of Corporate Governance and Property Management Department Tel.: +7 800 333 8000 Fax: +7(495) 225-3737 E-mail: [email protected] The address of the Internet site (sites) where the information contained herein is to be disclosed: www.rushydro.ru, http://www.e-disclosure.ru/portal/company.aspx?id=8580 1 Table of Contents Table of Contents .................................................................................................................................................... 2 I. Information on Bank Accounts, Auditor (Audit Organization), Appraiser, and Financial Advisor of the Issuer, as well as on Persons who Have Signed the Quarterly Report ................................................................................ 6 1.1. Information on the Issuer's Bank Accounts .................................................................................................. 6 1.2. Information on the Issuer's Auditor (Audit Organization) .......................................................................... -

An Overview of Boards of Directors at Russia's Largest

An Overview of Boards of Directors at Russia’s Largest Public Companies Andrei Rakitin Milena Barsukova Arina Mazunova Translated from Russian August 2020 Key Results According to information disclosed by 109 of Russia’s largest public companies: • “Classic” board compositions of 11, nine, and seven seats prevail • The total number of persons on Boards of the companies under study is not as low as it might seem: 89% of all Directors were elected to only one such Board • Female Directors account for 12% and are more often elected to the audit, nomination, and remuneration committees than to the strategy committee • Among Directors, there are more “humanitarians” than “techies”, while the share of “techies” among chairs is greater than across the whole sample • The average age for Directors is 53, 56 for Chairmen, and 58 for Independent Directors • Generation X is the most visible on Boards, and Generation Y Directors will likely quickly increase their presence if the development of digital technologies continues • The share of Independent Directors barely reaches 30%, and there is an obvious lack of independence on key committees such as audit • Senior Independent Directors were elected at 17% of the companies, while 89% of Chairs are not independent • The average total remuneration paid to the Board of Directors is RUR 69 million, with the difference between the maximum and minimum being 18 times • Twenty-four percent of companies disclosed information on individual payments made to their Directors. According to this, the average total remuneration is approximately RUR 9 million per annum for a Director, RUR 17 million for a Chair, and RUR 11 million for an Independent Director The comparison of 2020 findings with results of a similar study published in 2012 paints an interesting dynamic picture. -

Annual Report JSC “Quadra – Power Generation”

Annual Report JSC “Quadra – Power Generation” 2012 Preliminarily approved by the Board of Directors of JSC “Quadra – Power Generation” Minutes #19 / 160 dated 29.04.2013 Approved by resolution of Annual General Shareholders Meeting of JSC “Quadra – Power Generation” “26” June 2013 Minutes #1 / 16 dated 27/06/2013 General Director of JSC “Quadra - Power Generation” V.V. Shelkov Chief Accountant of JSC “Quadra - Power Generation” I.A. Lapitskaya 2 Contents: Disclaimer 5 Address by the Chairperson of the Board of Directors to shareholders 6 Address by the General Director to shareholders 8 Introduction: TGC in the structure of sector 10 SECTION 1. JSC “Quadra – Power Generation” on the electricity and heat market 14 1. 1 Market position 14 1.2 Competitive environment and competitive advantages 16 1.3 Strategic areas of business 18 1.4 Risk map 21 1.5 Macroeconomic situation 27 1.6 JSC “Quadra – Power Generation” – 5 years of stable energy supplies 28 SECTION 2. Corporate governance 33 2.1 Corporate governance principles 33 2.2 General Meeting of Shareholders 34 2.3 Board of Directors 34 2.4 General Director. Management Board. 38 2.5 Committees under the Board of Directors 40 2.6 Internal Audit Commission 40 2.7 Remuneration 42 2.8 Internal control and audit 43 SECTION 3. For shareholders and investors 44 3.1 Joint-stock capital 44 3.2 Securities 44 3.3 Dividend history 48 3.4 Trading in securities 48 3.5 Compliance with the law on insider information 50 SECTION 4. Production activities 51 4.1 Main production indicators 54 4.2 Current sales indicators in terms of market segments 56 4.3 Energy saving and operational efficiency improvement 57 SECTION 5. -

OAO IRKUTSKENERGO Address to Shareholders Performance OAO Irkutskenergo: PRODUCTION

OAO IRKUTSKENERGO Address to shAreholders PerformAnCe oAo irkUtskenerGo: ProdUCtion ....................... 27 by the ChAirmAn hiGhliGhts ........................... 9 An overview ...................... 15 of the boArd ........................ 5 instAlled CAPACity rePort of direCtors GenerAl informAtion........ 16 of Power PlAnts ................ 28 Address to shAreholders on ComPAny by the GenerAl PerformAnCe .................... 11 ComPAny strUCtUre........... 17 Power GenerAtion ............ 28 direCtor .............................. 7 mAjor events PlAnts And fACilities ......... 18 ProdUCtion And develoPments ............. 12 PerformAnCe ..................... 31 Power GenerAtion ComPAny’s CAPACity of the ComPAny ... 22 ProCUrement ..................... 31 objeCtives, ACtivities, And fUtUre ........................ 13 shAreholder’s eqUity ....... 23 oPerAtionAl qUAlity of the Power system ......... 32 ProdUCtion effiCienCy imProvement ProGrAm ........................... 33 OAO IRKUTSKENERGO heAt And eleCtriCity orGAnizAtionAl investment soCiAl PoliCy ..................... 60 mArket .............................. 35 strUCtUre of CorPorAte ACtivities ........................... 57 mAnAGement ..................... 44 AUditor’s stAtement ......... 62 tAriffs And tAriff PoliCy ............... 37 stAndArdizAtion And streAmlininG enerGy sAles ...................... 38 of bUsiness ProCesses ....... 47 domestiC mArket ............... 40 finAnCiAl mAnAGement ..... 50 eXternAl mArket ............... 41 hUmAn resoUrCes .............. 53 environmentAl -

INTER RAO Share Placement Price – 0.0535 RUB

Additional share issue Fundamentals Basic results of Private placement : INTER RAO share placement price – 0.0535 RUB Number of shares issued – 13,800,000,000,000 common shares Total number of shares placed with the participants of private placement – 6,822,972,629,771 shares. A total of 49.4% of newly issued shares were placed Number of shares placed with Inter RAO Capital – 2,917,890,939,501 (including shares for deal with Norilsk Nickel, stock option program and future deals) Final volume of Inter RAO’s authorized capital after private placement - 9,716,000,000,000 ordinary shares (increase by a factor of 3.36) Value of the share capital of the Company - 272.997 billion RUB* Total value of assets acquired by Inter RAO within the private placement: • Shares of utility companies - 283.2 bn RUB** • Cash – 81.8 bn RUB Share of government and state-owned companies in the authorized capital of Inter RAO amounts to 60%; Registration of additional share placement report by Federal Service for Financial Markets is planned for June 2011 Newly issued shares should start trading in June 2011 and merge into main symbol in October 2011 (MICEX) * Par value of 1 share - 0.02809767 RUB ** Value of assets based on independent appraisers. It does not include assets that might be received by INTER RAO’ s subsidiaries (closed subscription participants) after May, 17 2 Ownership structure Equity structure before Equity structure to May 17, 2011 Target equity structure after deals placement Minority finalization shareholders Federal Property Federal Property -

E P R G W O R K in G P a P

Market power issues in the reformed Russian electricity supply industry EPRG Working Paper 1333 Cambridge Working Paper in Economics 1358 Nadia Chernenko Abstract The paper examines long-run and short-run levels of market power in the liberalised Russian electricity market. We observe that despite potential for market power abuse, actual exercise of market power as measured by price-cost markups remained low. We attribute the result to the bid-at-cost rule implemented as a part of a special unit commitment procedure on the day-ahead market. We first look at the restructured industry and discuss the mergers and acquisitions and their impact on competition in long term. The M&A were undertaken in different market zones and thus did not seem to increase concentration (HHI remains almost unchanged) although with future zone integration competition in long run is put at risk. We then examine short-run level of market power by estimating hourly price-cost mark-ups and assessing their dynamics in 2010 and 2011, a year preceeding and following the G PAPER market liberalisation respectively. Using time series models (AR models) N we reject hypothesis of actual market power abuse. Further, using a Tobit regression we find that the liberalisation decreased the mark-ups by about 1.66 percetage points. .Keywords Russian electricity market, liberalisation, market power, concentration, price-cost mark-ups JEL Classification L11, L13, L94 Contact [email protected] Publication June 2013 EPRG WORKI Financial Support Trinity College Eastern European Research Bursary www.eprg.group.cam.ac.uk EPRG 1333 Market power issues in the reformed Russian electricity supply industry Nadia Chernenko October 2013 Abstract. -

Jsc Atomenergoprom

Credit rating: BBB-/Stable/A-3 National scale rating: ruAAA/--/-- ATOMIC ENERGY POWER CORPORATION JSC ATOMENERGOPROM PRESENTATION www.atomenergoprom.ru 1 Presentation contents ATOMENERGOPROM in brief Nuclear energy industry development forecast Affiliates of ATOMENERGOPROM www.atomenergoprom.ru 2 Restructuring of the atomic industry State Atomic Energy Corporation ROSATOM Atomic Energy Power Corporation JSC “Atomenergoprom” Nuclear and Nuclear Nuclear fuel Engineering Machine Power radiation safety, defense complex cycle export Engineering generation decommissioning Sales of Non - nuclear Nuclear Science Nuclear Navy Technology R&D uranium and development activities services Goals of the establishment of JSC “Atomenergoprom”: To consolidate the civil part of nuclear industry, to increase its efficiency and to enhance its competitiveness To split commercial and defense sectors of nuclear industry To provide conditions to meet requirements of international integration processes To realize effectively a large-scale program of NPP construction in Russia www.atomenergoprom.ru 3 General Company Information JSC Atomenergoprom was established in 2007 according to Russian Federation Presidential Decree № 556 dated 27.04.2007. The State Atomic Energy Corporation Rosatom owns 100% shares of JSC Atomenergoprom (Federal law N 317-FL of 01.12.2007) According to Government Decree N 319 “On Measures for Creation of Joint Stock Company “Atomic Energy Power Corporation” dated May 26, 2007 shares of Russian nuclear industry enterprises were contributed into the equity of JSC Atomenergoprom. The staff total is approximately 177,000 employees. JSC Atomenergoprom imbibes a unique experience, which has been accumulated through all sectors of nuclear fuel cycle and NPP construction during last 60 years. In 2008 consolidated proceeds of JSC Atomenergoprom constituted 290 billion RUR. -

KYMENLAAKSON AMMATTIKORKEAKOULU University of Applied Sciences Energy Engineering Double Degree / Specialization

KYMENLAAKSON AMMATTIKORKEAKOULU University of Applied Sciences Energy Engineering Double Degree / Specialization Iuliia Gerlitc Rinat Biktuganov A REVIEW TO WIND ENERGY UTILIZATION IN NORTH-WEST RUSSIA Bachelor’s Thesis 2013 ABSTRACT KYMENLAAKSON AMMATTIKORKEAKOULU University of Applied Sciences Energy Engineering Gerlitc Iuliia Biktuganov Rinat A Review to Wind Energy Utilization in North-West Russia Bachelor’s Thesis 79 pages + 1 page of appendices Supervisor Mäkelä Merja, Principal Lecturer Commissioned by Empower Oy November 2013 Keywords Wind turbines, electrical grid, and grid connection The problem of using renewable energy sources is studied in this thesis work. The at- tention is concentrated on the feasibilities of using the wind energy in the North-West Russia and on some problems which can appear. Some of them are the place of a pos- sible wind farm, laws of new sources connection, and the protection of the electrical grid. The aim of the work was to realize the possibility of inserting new energy resources into the Russian electrical grid and the importance of using renewables. An answer was sought to the question why the country network had no changes for a long time and what factors are preventing the changes. The study was carried out with the help of technical encyclopedias and energy com- panies official websites. Some information was retrieved through the conversation with specialists from the largest Russian energy companies. The idea of inserting new energy resources in the Russian economy looks very prom- ising. Naturally, some investments and time are needed. In the next few years the problem of renewables will become very actual and then this work will be very useful. -

INTER RAO UES Generating Assets: Target Shareholding Structure

INTER RAO UES Generating Assets: Target Shareholding Structure March,16 2012 1. Strategy recap and update INTER RAO at a Glance A Leading Russian Power Company Diversified Group Structure . Diversified power holding involved in electricity/heat generation and supply, export/import of electricity and engineering . Operates and manages 27 thermal, 2 hydro power plants and 1 wind power farm Domestic Engineering . Total installed electricity capacity of 29GW and electricity output of Generation Trading Supply International 117 TWh⁽¹⁾ in 2011 . INTER RAO – . RAO Nordic Oy . 9 supply companies . Generation: . Quartz Group . 2 Hydro PP - 0.2 GW Electrogeneration (Finland) . Customer base: . 4 Thermal PP - 5.2 GW . JV with Worley Leading Russian export-import operator accounting for 97% of Russian (100%) . Kazenergoresurs . 1 wind power farm - Parsons electricity export in 2011 . 314 thousand 0.03 GW . OGK-1 (75%) (Kazakhstan) legal entities and . Distribution . JV with Rosatom . OGK-3 (82%) . TGR Enerji (Turkey) . c. 34 ths. km of power . Operations in over 14 countries, including Russia, Belarus, Lithuania, 9.8 million . JV with GE lines (Georgia, residential . TGK-11 (68%) . INTER RAO Lietuva Armenia) Georgia, Armenia, Kazakhstan, Tajikistan, Moldova, and Finland . EMAlliance (the Baltics) customers Engineering (2) . Listed on RTS and MICEX (List A1), MCAP of $10.2bn. Shares are (2) included into MSCI Large Caps Index (0,54%) . GDRs admitted to LSE trading Ownership Structure Broad Geographical Coverage INTER RAO UES Finland Generation Assets