Parish and School Financial Policies & Procedures

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mass Intentions & Memorials St. John Neumann Catholic Church

Mass Intentions & Memorials St. John Neumann Catholic Church "What can we do to pray for a loved one, living or deceased, or how can we honor or memorialize them at St. John Neumann parish?" § Gifts to Funeral Ministry support us in providing hospitality and liturgical services for grieving families. Donations should be clearly marked with “Funeral Ministry” and the name of the person who is being honored or memorialized. Donations can be given to the Pastoral Care Associate. § Gifts to the Liturgy Donations Fund help with the cost of liturgical items, such as vestments, altar cloths, sacred vessels, etc. Donations should be clearly marked with “Liturgy Donations” and the name of the person who is being memorialized or honored. Donations can be given to the Pastoral Care Associate or the Liturgy Associate. They may also be placed in the collection or sent to the office. § Flower Donations can be made at any time, but are especially collected at Christmas and Easter. Donations should be marked with “Flower Donations” and the name of the person(s) being honored or memorialized. Donations can be placed in the collection or sent to the office. Persons honored or memorialized are listed in bulletins during the Christmas or Easter seasons. § Light a Votive Candle in the Chapel for any intention. Lighting a candle allows you to extend your prayer throughout the time that the candle is burning. It also allows others who pray in the chapel to lift up your intention in prayer. An optional small donation may be placed in the wooden box near the candles. -

Remuneration and Benefits for Archdiocesan Priests for Ministry Expenses Covered Under the Professional Allotment

May 26, 2021 Dear Rev. Monsignor / Father: Enclosed with this letter is the Remuneration Policy FY2022 for active priests assigned in the Archdiocese of Boston and approved by His Eminence, Cardinal Sean P. O'Malley, OFM, Cap. Kindly note that the policy, enclosed with this letter, applies to incardinated priests and religious order priests serving in assignments by the Archbishop to parishes or archdiocesan institutions within the Archdiocese of Boston; it does not apply to senior priests, priests on health leave, or other priests of the Archdiocese who receive stipends and benefits from the Clergy Trust or other funds. The name of Clergy Benefits has changed to “Clergy Trust” throughout the policy. I encourage you to read the enclosed document in detail and save it for future reference. Remuneration payment schedules attached to the enclosed policy indicate the approved remuneration according to year of ordination for Archdiocesan priests participating in Social Security and for religious order priests in Archdiocesan assignments. All priests are encouraged to enroll in Social Security. Not participating in Social Security may prevent a priest from accumulating 40 quarters which is needed to qualify for Medicare A & B at age 65, thereby creating an increased burden on the Clergy Funds. Effective July 1, 2021, the base stipend for an Archdiocesan priest for fiscal year 2022 is $30,867 and the base stipend for a religious order priest in an Archdiocesan assignment is $28,390, reflecting a 0.3% increase, based on the Boston Consumer Price Index increase. The annual assessment for priest health and dental benefits for fiscal year 2022 will increase to $20,676 per year. -

A Little Bit About Mass Stipends… Offering a Stipend to a Priest So That

A little bit about Mass stipends… Offering a stipend to a priest so that he will remember a particular intention of a member of the faithful is a longstanding custom in the Roman Catholic Church. All of the priests here at St. Monica are available for this and more than likely they are praying for someone’s particular intention every time they have a Mass. The stipend offering in the Archdiocese of Indianapolis is $10.00 and is intended to commit the priest to celebrating the Mass. The stipend is simply an offering; Masses can be offered free if the person desiring the intention is unable to offer any stipend. The intention for a Mass is mostly to pray for the repose of the soul of a person who has died, but can also be for a special intention or a private one. The stipend is offered for the priest to add this intention to his own personal intentions. A priest may have other intentions in addition to the one the stipend is offered for. Additionally, the priest does not have to know the person for whom the Mass is offered as long as he is celebrating the Mass according to the intention of the donor. There can be some confusion about how all this works at St. Monica, below are some guidelines to help you. If there are any questions don’t hesitate to call our office (317-253-2193, opt 2) and speak to one of our Administrative Assistants. Here are the guidelines: 1. Universal Church discipline as contained in the Code of Canon Law (Canons 945-958) of the 1983 Code of Canon Law is what regulates the offerings made for the celebration of Mass. -

Mass Stipend Guidelines to Our Parishioners

Mass Stipend Guidelines to Our Parishioners From the very beginnings of the Church, it was customary for the faithful to donate the bread and wine to be used in the celebration of the Holy Eucharist. In time, offerings of money were substituted for the actual bread and wine. Money given in excess of what was necessary for the procuring of the bread and wine was used to assist the poor and, eventually, to support the clergy. Thus, it became customary for the priest to accept from the faithful a donation (formerly called a “stipend”) in return for remembering a specific intention in the celebration of a Mass. Through this voluntary offering, the donor seeks spiritual benefits that God may bestow upon the persons or concerns that are specially held in prayer at the Mass. What is more, the Code of Canon Law (canon 946) notes that the donor himself benefits: “Christ’s faithful who make an offering so that Mass can be celebrated for their intention contribute to the good of the Church, and by that offering they share in the Church’s concern for the support of its ministers and its activities.” According to the Council of Trent (1545-1563) , the Mass “is quite properly offered according to apostolic tradition not only for the sins, punishments, satisfactions and other needs of the faithful who are living, but also for those who have died in Christ but are not yet fully purified” (Session XXII, Chapter 2). The deep faith and ardent charity of the parishioners of Parish of the Precious Blood manifests itself in the numerous Mass offerings you donate to the parish, especially for your beloved deceased. -

April 18 2021.Pub

Welcome to Sts. Gregory & Barnabas Parish 3 Sਕਁਙ ਏਆ Eਁਓਔਅ Aਐਉ 18, 2021 MISSION STATEMENT United As Catholic Christians, we will live to serve God and each other. And do His will as one family united in Faith. We will teach, serve, and be an example to the youth In Christ of the parish that they will come to a full understanding of Christ and His plan for their lives. We will nurture the gifts and talents of all parish members and use them wisely for the glory of God. We will compassionately implement the Spiritual and Corporal Pastor works of Mercy for those in our Parish, Diocese and throughout the world. Through the celebration of the Sacraments, especially the Eucharist, we affirm our Communion with Rev. Callistus I. Elue Christ and each other. All are welcome. Daily Mass: (See inside for locations) 8:00AM Monday Tuesday Wednesday Friday 6:30PM Thursday Weekend Liturgy: Saturday: 4:00PM (Daisytown) Sunday: 8:00AM (Bon Air) 11:00AM (Daisytown) 120 Boltz Street 408 Luzon Avenue Johnstown, PA 15902 Reconciliation: Saturday: 3:00–3:45PM (Daisytown) or you may request an appoint- ment for confessions by calling the office. You may call in anonymously. Phone: 814-536-6818 Sacrament of Baptism: Parents are to be examples to their children by being registered, active members of the Parish. Please call the rectory office to make Office Hours: arrangements. Monday - Friday Sacrament of Marriage: Couples planning to marry are to make arrangements 9:00AM - 2:00PM at least nine months prior to their wedding date. -

Our Lady of the Assumption Parish

Our Lady of the Assumption Parish 545 Stratfield Road Fairfield, CT 06825-1872 Tel. (203) 333-9065 Fax: (203) 333-2562 Email: [email protected] Website: https://www.olaffld.org “Ad Jesum per Mariam” To Jesus through Mary. Clergy/Lay Leadership Rev. Peter A. Cipriani, Pastor Rev. Michael Flynn, Parochial Vicar Deacon Raymond John Chervenak Deacon Robert McLaughlin Michael Cooney, Director of Music Dr. Claire Paolini, Trustee Daniel Ford, Esq., Trustee Masses Saturday Vigil Mass: 4 PM Sunday Masses: 7:30 AM, 9 AM (Family, ex- cept in the Summer), 10:30 AM, and 12 PM Morning Daily Mass: (Mon.-Sat.) 7:30 AM Evening Daily Mass: (Mon.-Fri.) 5:30 PM Holy Days: See Bulletin for schedule Sacrament of Reconciliation Saturday: 3- 3:45 PM or by appointment. Every Tuesday: 7-8:00 PM Rosary 7 AM Monday-Saturday 9 AM Friday Morning Rosary (Except for the First Friday of the month) 8 AM First Saturday Rosary Rite of Christian Initiation for Adults (RCIA) Adoration of the Blessed Sacrament Anyone interested in becoming a Roman Catholic becomes a part of this First Friday of each month from 8 AM process, as can any adult Catholic who has not received all the Sacraments of Friday to 7:15 AM Saturday. To volunteer initiation. For further information contact the Religious Education office. please contact Grand Knight, Jeffrey Thompson at (203) 374-9262. Sacrament of Baptism This Sacrament is celebrated on Sundays at 1:00 PM. It is required that Miraculous Medal Novena parents participate in a Pre-Baptismal class. Classes are held on the third 8 AM. -

Our Lady of the Assumption Parish 545 Stratfield Road Fairfield, CT 06825-1872 Tel

Our Lady of the Assumption Parish 545 Stratfield Road Fairfield, CT 06825-1872 Tel. (203) 333-9065 Fax: (203) 333-2562 Email: [email protected] Website: https://www.olaffld.org “Ad Jesum per Mariam” To Jesus through Mary. Clergy/Lay Leadership Rev. Peter A. Cipriani, Pastor Rev. Michael Flynn, Parochial Vicar Deacon Raymond John Chervenak Deacon Robert McLaughlin Michael Cooney, Director of Music Daniel Ford, Esq., Trustee Masses (Schedules subject to change) Saturday Vigil Mass: 4 PM Sunday Masses: 7:30 AM, 9 AM and 11 AM Morning Daily Mass: (Mon.-Sat.) 7:30 AM Evening Daily Mass: (Mon.-Fri.) 5:30 PM Holy Days: See Bulletin for schedule Sacrament of Reconciliation Saturday: 1:30– 2:30 PM or by appointment. Every Tuesday: 7-8:00 PM Rosary 7 AM Monday-Saturday 9 AM Friday Morning Rosary (Except for the First Friday of the month) 8 AM First Saturday Rosary Rite of Christian Initiation for Adults (RCIA) Adoration of the Blessed Sacrament Anyone interested in becoming a Roman Catholic becomes a part of this First Friday of each month from 8 AM process, as can any adult Catholic who has not received all the Sacraments of Friday to 7:15 AM Saturday. To volunteer initiation. For further information contact the Faith Formation office. contact Grand Knight, Michael Lauzon at (203) 817-7528. Sacrament of Baptism Novenas This Sacrament is celebrated on Sundays at 1:00 PM. It is required that parents participate in a Pre-Baptismal class. Classes are held on the third Miraculous Medal-8 AM. Monday Saturday of the month. -

218Template.Pdf

DIVINE MERCY PARISH --- WEBSITE: www.dmparish.com Parish Office: 108 West Cherry St. Shenandoah, PA 17976 Phone: 570-462-1968 Fax: 570-462-1388 E – Mail: [email protected] Office Hours: Monday 9:30 AM to 3:00 PM - Wednesday 8:30 AM to 2:00 PM - Friday 8:30 AM to 1:00 PM Rev. Msgr. Ronald C. Bocian, Pastor Fr. Charles J. Dene, In Residence Sr. Marietta, OSF, Parish Outreach Coordinator -- Phone: 570-462-2306 Sr. Helene Theresa McGroarty, IHM – Spanish Ministry Coordinator -- Phone: 570-462-3868 Mission of Divine Mercy Parish: Misión de la Parroquia de la Divina Misericordia: Divine Mercy Parish is a Eucharistic Community, a people Parroquia de la Divina Misericordia es una comunidad diverse in background united together as Catholic Christians eucarística, un pueblo, diverso en origen, unidos juntos around the altar of the Lord. We are nurtured by the como Cristianos Católicos en torno al altar del Señor. Somos Sacraments and sustained by prayer. Our mission is to fulfill alimentados de los Sacramentos y sostenidos por la oración. our Baptismal promises by proclaiming the message of the Nuestra misión es cumplir nuestras promesas bautismales, Gospel in our lives by our commitment to faithfully love and proclamando el Evangelio en nuestras vidas por nuestro serve the Lord and one another. compromiso de amar fielmente y servir al Señor ya los demás. Parish Membership: Importante -- Afiliación Parroquial: The Parish Community of Divine Mercy welcomes all La comunidad parroquial de la Divina Misericordia les individuals and families who have moved into the parish. da la bienvenida a todos los que se han movido en la Contact the Parish Office at your earliest convenience. -

POLICY 3.5.2 Mass Stipends

POLICY 3.5.2 Mass Stipends There is a long history in the Catholic Church of Mass stipends. These are donations made by the Catholic faithful to the priest for the celebration of Mass. Usually, the person making such a donation also asks the priest to pray for their intention during that Mass – this may be for the spiritual benefit of a deceased friend or relative, for the intention of the donor or of another worthy intention. The specifics of the intention need not even be known to the priest, but we trust that God knows of the donor’s intention. In every way, we are to discourage any semblance of simony, or the idea that one can “buy a Mass”. The Mass stipend is simply a donation made to the priest in consideration of his ministry. Because there is a service directly applied to the donation, a charitable donation receipt for income tax purposes cannot be given. The Code of Canon Law (Canons 945-958) has established some ground rules for Mass intentions, so that there be no abuse of this practice. In short, what is stipulated is that: The practice of accepting Mass stipends is safeguarded in Church practice. The stipend is for the free use of the priest only after that Mass has been celebrated. It cannot be used prior to satisfying the intention by saying the Mass. If a priest presides at a second Mass on the same day, the amount of the second stipend shall not be kept by the priest (see below). This does not apply to Christmas Day. -

10390794.Pdf

https://theses.gla.ac.uk/ Theses Digitisation: https://www.gla.ac.uk/myglasgow/research/enlighten/theses/digitisation/ This is a digitised version of the original print thesis. Copyright and moral rights for this work are retained by the author A copy can be downloaded for personal non-commercial research or study, without prior permission or charge This work cannot be reproduced or quoted extensively from without first obtaining permission in writing from the author The content must not be changed in any way or sold commercially in any format or medium without the formal permission of the author When referring to this work, full bibliographic details including the author, title, awarding institution and date of the thesis must be given Enlighten: Theses https://theses.gla.ac.uk/ [email protected] EUCHARISTIC SACRIFICE AND THE PATRISTIC TRADITION IN THE Th e o l o g y o f m a r t in b u c e r I534-I546. by Nicholas James Thompson Thesis submitted for the degree of Doctor of Philosophy at the University of Glasgow Appli^Qoo, © Nicholas Thompson 2ooo ProQuest Number: 10390794 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a complete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. uest ProQuest 10390794 Published by ProQuest LLO (2017). C o pyright of the Dissertation is held by the Author. -

Diocesan Policy Manual Rev. 2016

Diocese of Reno Diocesan Policy Manual Rev. 2016 2 I – DIOCESAN CONSULTATIVE BODIES Section A – College of Consultors 6 Section B – Presbyteral Council 7 Section C – Priest Personnel Board 9 Section D – Diocesan Finance Council 11 Section E – Catholic Service Appeal Board 12 Section F – Respect Life Commission 12 Section G – Life, Peace & Justice Commission 13 Section H – Liturgy Commission 14 Section I – Review Board for the Protection of Children & Young People 16 II – ADMINISTRATION Section A – Stewardship of Church Property 19 Section B – Financial Procedures 23 Section C – Deposits of Surplus 24 Section D – Capital Projects & Loans to Parish Corporations 25 Section E – Copyright 30 Section F – Grant Coordination 31 Section G – Missionary Co-op Plan 34 Section H – Transportation Vans 35 Section I – Internet Access, E-Mail, Voice Mail 36 Section J – Record Retention 37 Section K – Investment Policies 44 Section L – Collection Counting 48 Section M—Filming Policy 49 III – PARISH Section A – Authentic Catholic Life 52 Section B – Parish Administration 55 Section C – Parish Staff 58 Section D – Pastoral Council 59 Section E – Finance Council 61 Section F – Parish Vacancy 64 Section G – Parish Coverage 65 Section H – Parish Organizations 66 Section I – Stole Fees 67 Rev 2016 3 IV – CLERGY Section A – Preparation for Ministry 69 Section B – Clerical Attire 71 Section C – Assignment 72 Section D – Mentor Policy 73 Section E – Incardination 76 Section F – Non-Incardinated 77 Section G – Selection of Pastors 79 Section H – Responsibility of -

PPT Mass Stipend Workshop for Website-1.Pdf

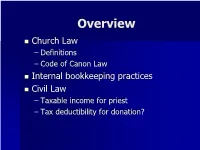

Overview Church Law – Definitions – Code of Canon Law Internal bookkeeping practices Civil Law – Taxable income for priest – Tax deductibility for donation? Definitions Stipend (Mass Stipend) A Stipend is a ‘free-will offering’ made by an individual (not by the Church) to a priest celebrating or concelebrating a Mass which is to be applied (said) for a specific intention. This is not dependent upon a payment, a priest will offer the Mass as a normal part of his duties without expectation of payment. Stole Fee (aka remuneration for extra clergy) A “Stole Fee” refers to money given to a cleric for the performance of sacramental functions i.e.: baptisms, weddings, funerals, penance services. Nota bene!! “Extra clergy” (not assigned to your parish) receive both the stipend (if there is one) and the stole fee. Clergy assigned to the parish receive only the stole fee for events that take place at the parish or are part of the parish ministry (e.g. a graveside-only service done by the priest/deacon as part of his parish duties). Code of Canon Law Canon 945 §1. In accord with the approved practice of the Church, any priest celebrating or concelebrating is permitted to receive an offering to apply the Mass for a specific intention. §2. It is recommended earnestly to priests that they celebrate Mass for the intention of the Christian faithful, especially the needy, even if they have not received an offering. Canon 946 The Christian faithful who give an offering to apply the Mass for their intention contribute to the good of the Church and by that offering share its concern to support its ministers and works.