View Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

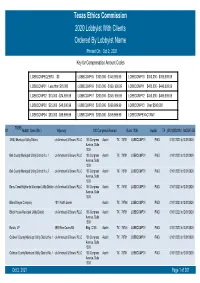

Texas Ethics Commission 2020 Lobbyist with Clients Ordered by Lobbyist Name Printed on Oct 2, 2021 Key for Compensation Amount Codes

Texas Ethics Commission 2020 Lobbyist With Clients Ordered By Lobbyist Name Printed On Oct 2, 2021 Key for Compensation Amount Codes LOBBCOMPEQZERO $0 LOBBCOMP05 $100,000 - $149,999.99 LOBBCOMP10 $350,000 - $399,999.99 LOBBCOMP01 Less than $10,000 LOBBCOMP06 $150,000 - $199, 999.99 LOBBCOMP11 $400,000 - $449,999.99 LOBBCOMP02 $10,000 - $24,999.99 LOBBCOMP07 $200,000 - $249, 999.99 LOBBCOMP12 $450,000 - $499,999.99 LOBBCOMP03 $25,000 - $49,000.99 LOBBCOMP08 $250,000 - $299,999.99 LOBBCOMP13 Over $500,000 LOBBCOMP04 $50,000 - $99,999.99 LOBBCOMP09 $300,000 - $349,999.99 LOBBCOMPEXACTAMT 70358 #1 Abbott, Sean (Mr.) Attorney 100 Congress Avenue Suite 1300 Austin TX (512)4352334 MODIFIED 3 B&J Municipal Utility District c/o Armbrust & Brown, PLLC 100 Congress Austin TX 78701 LOBBCOMP01 PAID 01/01/2020 to12/31/2020 Avenue, Suite 1300 Bell County Municipal Utility District No. 1 c/o Armbrust & Brown, PLLC 100 Congress Austin TX 78701 LOBBCOMP01 PAID 01/01/2020 to12/31/2020 Avenue, Suite 1300 Bell County Municipal Utility District No. 2 c/o Armbrust & Brown, PLLC 100 Congress Austin TX 78701 LOBBCOMP01 PAID 01/01/2020 to12/31/2020 Avenue, Suite 1300 Berry Creek Highlands Municipal Utility District c/o Armbrust & Brown, PLLC 100 Congress Austin TX 78701 LOBBCOMP01 PAID 01/01/2020 to12/31/2020 Avenue, Suite 1300 Blake Magee Company 1011 North Lamar Austin TX 78704 LOBBCOMP01 PAID 01/01/2020 to12/31/2020 Block House Municipal Utility District c/o Armbrust & Brown, PLLC 100 Congress Austin TX 78701 LOBBCOMP01 PAID 01/01/2020 to12/31/2020 Avenue, Suite 1300 Bonzo, LP 3939 Bee Caves Rd. -

DOCU00000007.Pdf (11.49Mb)

I HP% IIIII{fj!I, ` GRA CIVIC ND MILL . 4 i In Philudelph ebra try i2h1,? 1832, being the 100th A ea v r M the 114 v_uww Me dry A to mt Wool adar morning with salvo'. of cannon fmm the has, net the city, Kns S.rd, too whites of too gms ran di,rh.rgcd; rod rte+,,,, u tour the mint tbnegh the dlffrrtnt preen of control and r.ngan or - and WI no1ieeofthefu drnrmin.lioo of JI to rl,.rnIn.Or.itneath., nice rrra ,I,. ccaion. Incry ri umetanre of'I,e eallter was G+or.l,lr I tle p.ad it :d' n tsi to by the pmrer satl,ure ier,o remo+e a far a possible u,;4 .1-1, the procession eu In p.s.. riser .e r deronted n;tl, tlogt, e nd streamon, I `ram thcu -.4. t c " I,nhh,build- nell .r many pri nn our. d opt.,rd fly;. ,.pt d wraJon, i,d dsre t '[,.d,, rice Cnmhini and Ni11 spar s l l a of rendrx+ w l the bra m ->f f lie dot and the different a of thrlr. craft and r. d rag end cnfnt ahilr h,erful -t, T, kmadin or, and of e,erv sip. N'hrn the d,fferent ron,pnnics lud brru sepal I cro marched iotn Third street, to rain thrir atai,a i,.'lie girr'rs r 'An enn-1" it +a. impootibir'hot t-rh,mtnene nmuhen Nitl, d f wloo, t1. Ie be A,,[ tl raid`. -

June 2021 City Manager's Report

JUNE 2021 CITY MANAGER’S REPORT WWW.GALVESTONTX.GOV/CITYMANAGERSREPORT A MESSAGE FROM OUR CITY MANAGER The City is in the midst of the budget season, in balance is in good shape at a projected $18.4 which we set the tax rate and the budget for the million, or 116 days of operating expenses in fiscal year beginning on October 1. reserves. The property tax revenue for the next For the current fiscal year, the tax rate is $.56 year could increase by $400,000 to $1 million per $100 valuation of the appraised property depending on the tax roll, while the sales tax is value. We anticipate the tax rate will be reduced; estimated to be up 4.2 percent, thanks to job however, the rate has not yet been proposed growth in the metro area. awaiting final numbers for the tax roll from the As for expenditures, we estimate we’re looking Galveston County Appraisal District. The budget at an approximately $1.8 million in increase due will be filed with the City Secretary on Wednes- to a 2 percent cost of living adjustment for all day, August 11, for review by the Galveston City employees, health insurances increases, addi- Council and the public. The following day, Thurs- tional savings requirements to the infrastructure day, August 12, the Galveston City Council will fund, and an increase in EMS costs, among other discuss it during a council meeting. We invite the things. public to attend this hearing at City Hall, 823 Please take a moment to look through this Rosenberg. -

September 2019 City Manager's Report

September 2019 CITY MANAGER’S REPORT WWW.GALVESTONTX.GOV/CITYMANAGERSREPORT A MESSAGE FROM OUR CITY MANAGER e are wrapping up a busy financial season with The budget – including maintenance and operating Wthe adoption of the budget for the next fiscal expenditures, one-time appropriations, and the year. In September, Galveston City Council adopted capital budget – is $235.1 million, 5.36 percent a $235.1 million budget for the fiscal year 2020 less than last year’s combined total. The budget focused on delivering high-quality service, capital includes adequate reserves in all funds and allocates improvements and continuing valuable programs. additional available resources to meet the City’s This budget is intended to meet the city’s strategic highest priorities. The fiscal year begins on October street and infrastructure priorities while also 1, 2019. providing those services that make Galveston a Residents who are over 65 or disabled and qualified better place to live and ensuring our public safety for homestead exemptions will not see any increase personnel are compensated at the average pay level to their taxes. The budget and Capital Improvement of our peer comparative cities. The City reached Plan are both available online at www.galvestontx. collective bargaining agreement with the police gov/financialtransparency. and fire associations that included raises for public Sincerely, safety employees. Brian Maxwell, City Manager TABLE OF CONTENTS 04 CITY MARSHAL 05 CONSTRUCTION 06 DEVELOPMENT SERVICES 07 ENGINEERING 10 FACILITIES 11 FINANCE 15 FIRE DEPARTMENT/EM 16 FLEET FACILITIES 17 GRANTS AND HOUSING 19 HUMAN RESOURCES 20 INFORMATION TECHNOLOGY 22 ISLAND TRANSIT 23 PARKS AND RECREATION 26 PLANNING AND DEVELOPMENT 28 POLICE DEPARTMENT 29 PUBLIC INFORMATION OFFICE 31 PUBLIC WORKS 33 SCHOLES AIRPORT LAST MONTH’S CITY MARSHAL ACCOMPLISHMENTS • 15 Public Nuisances were abated. -

American National Insurance Company Financial Statements

SECURITIES AND EXCHANGE COMMISSION FORM 485BPOS Post-effective amendments [Rule 485(b)] Filing Date: 2017-04-27 SEC Accession No. 0001193125-17-143312 (HTML Version on secdatabase.com) FILER AMERICAN NATIONAL VARIABLE LIFE SEPARATE Mailing Address Business Address ONE MOODY PLAZA ONE MOODY PLAZA ACCOUNT CORPORATE COMPLIANCE CORPORATE COMPLIANCE 14TH FL 14TH FL CIK:867289| IRS No.: 740484030 | Fiscal Year End: 1231 GALVESTON TX 77550 GALVESTON TX 77550 Type: 485BPOS | Act: 33 | File No.: 333-53122 | Film No.: 17790120 4097666845 AMERICAN NATIONAL VARIABLE LIFE SEPARATE Mailing Address Business Address ONE MOODY PLAZA ONE MOODY PLAZA ACCOUNT CORPORATE COMPLIANCE CORPORATE COMPLIANCE 14TH FL 14TH FL CIK:867289| IRS No.: 740484030 | Fiscal Year End: 1231 GALVESTON TX 77550 GALVESTON TX 77550 Type: 485BPOS | Act: 40 | File No.: 811-06160 | Film No.: 17790121 4097666845 Copyright © 2017 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document Table of Contents SECURITIES AND EXCHANGE COMMISSION WASHINGTON, DC 20549 FORM N-6 REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 Post-Effective Amendment No. 24 and/or REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 Amendment No. 41 American National Variable Life Separate Account (Exact Name of Registrant) American National Insurance Company (Name of Depositor) One Moody Plaza, Galveston, Texas 77550 (Address of Depositors Principal Executive Offices) (Zip Code) (409)763-4661 (Depositors Telephone Number, Including Area Code) Name and Address of Agent for service: Please send copies of communications to: Dwain Akins, Esq., Sr. Vice President Gregory Garrison American National Insurance Company Greer, Herz & Adams, L.L.P. One Moody Plaza One Moody Plaza Galveston, TX 77550 Galveston, Texas 77550 Approximate Date of Proposed Pubic Offering It is proposed that this filing will become effective (check appropriate box): ☐ Immediately upon filing pursuant to paragraph (b) of Rule 485. -

FULFILLING OUR 500-YEAR CHARTER Planning a Future Built on Past Success

AMERICAN NATIONAL INSURANCE COMPANY 2018 OVERVIEW FULFILLING OUR 500-YEAR CHARTER Planning a Future Built on Past Success 1905 1930s 1940s BUILDING A STRONG GROWTH DURING LESSONS TO GUIDE FOUNDATION DEPRESSION THE FUTURE When it was founded by W.L. Moody, Jr. in While dark economic times descended upon As a Marine serving in the South Pacific 1905, American National Insurance Company the country during the Great Depression of the during World War II, W.L. Moody, IV, grandson was a fledgling business with just 10 1930s, American National not only survived of American National founder W. L. Moody, Jr. employees and 500 square feet of office space but thrived. Through prudent management, asked his grandfather for advice on how best in Galveston, Texas. In American National’s the company’s assets continued to increase to conduct his business and personal affairs. very first annual report, Mr. Moody explained and its surplus doubled. Even more His answer is known as The Founder’s his business philosophy – one that still impressive, while millions of Americans were Philosophy. guides the company to this day, “Care and laid off or out of work, American National economy have been our watchwords in didn’t dismiss any employees. the management of the business.” 500 Year Charter CERTIFICATE STATE OF TEXAS Department of Insurance I, JNO. M. SCOTT, Commissioner of Insurance of the State of Texas, do hereby certify that the instrument which is hereunto attached is a true, full and correct copy of ORIGINAL CHARTER AND AMENDMENTS THERETO of the AMERICAN NATIONAL INSURANCE COMPANY, GALVESTON, TEXAS now on file in and forming a part of the records of this Department. -

American National Insurance Company

AMERICAN NATIONAL INSURANCE COMPANY 2016 OVERVIEW AMERICAN NATIONAL Reaching the Summit he late May morning dawned clear and bright pounds of baggage. Even as he broke away from the larger group over the Himalayas — a relief after days of for his final ascent, Hillary was accompanied and aided every step unrelenting snow and wind. Having slowly ascended the of the way by his guide Tenzing Norgay. The two men worked as a slopes of Mount Everest for the past two months, Edmund Hillary synchronous team to finally conquer Everest. had just 1,000 perilous feet left to reach the summit. So, on the While few of us will ever make the perilous journey to the morning of May 29, 1953, carrying a 30-pound pack on his back summit of Everest, most of us will face our own mountains in life. In and wearing boots that had been frozen solid by the punishing fact, life offers endless challenges – whether it involves becoming conditions, Hillary carefully inched his way up a vertical slope face, a parent, getting a college degree or, in the case of American wedging his body in a small crack between the rock and ice. Finally National founder W.L. Moody Jr., building a financial services reaching the summit at 11:30 a.m., Hillary cemented his legacy as business that has stood the test of time. The people who most the first to successfully stand atop the world’s highest peak. successfully navigate these challenges are the people who realize Although his name is the one we remember, Hillary didn’t do they need the help of others and, therefore, approach life as a team it alone. -

American National 10-K As of 12.31.20

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ☒ Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the fiscal year ended December 31, 2020 or ☐ Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Commission File No. 001-39369 American National Group, Inc. (Exact name of registrant as specified in its charter) (formerly American National Insurance Company) Delaware 30-1221711 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) One Moody Plaza Galveston, Texas 77550-7999 (Address of principal executive offices) (Zip Code) (409) 763-4661 (Registrant’s telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: Title of Each Class Trading Symbol Name of Each Exchange on which Registered Common Stock, par value $0.01 ANAT NASDAQ Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☒ Yes ☐ No Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. ☐ Yes ☒ No Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

July 2021 City Manager's Report

JULY 2021 CITY MANAGER’S REPORT WWW.GALVESTONTX.GOV/CITYMANAGERSREPORT A MESSAGE FROM OUR CITY MANAGER We’re now at the peak of storm season, and while we increase in COVID cases. We urge our residents to follow hope we don’t experience any storms, the city stands the advice of health professionals and get vaccinated. ready to implement our emergency response plan. The city occasionally hosts free vaccination events, which September is usually one of the wettest months in Gal- we advertise in advance on galvestontx.gov, social media, veston. During this time, in particular, the city frequently and local media. The Galveston County Health District is runs our pre-storm readiness plan, which means clearing administering vaccines for free at its offices in Texas City. any debris or visible clogs that could impede drainage. You can sign up for an appointment at https://www.gchd. We ask for residents to do their part in ensuring your org/. yards and properties are free of any items that could blow The health district is giving booster shots to immunocom- or float into a drain during a rainstorm. promised individuals who have already had the first two Also, be sure your household is hurricane-ready with doses. an evacuation plan, should we need it, and at least a Regardless of whether you’re vaccinated, we urge resi- week’s worth of any necessary medications. If you need dents to practice healthy hygiene and take precautions assistance evacuating, sign up for the state’s emergency to slow the spread of the highly contagious Delta variant. -

AMERICAN NATIONAL INSURANCE COMPANY One Moody Plaza Galveston, Texas 77550

AMERICAN NATIONAL INSURANCE COMPANY One Moody Plaza Galveston, Texas 77550 NOTICE OF ANNUAL STOCKHOLDERS' MEETING To Be Held April 25, 2014 In Galveston, Texas Notice is hereby given that the Annual Meeting of Stockholders of AMERICAN NATIONAL INSURANCE COMPANY, a Texas insurance company (the “Company”), will be held in the Mary Moody Northen Auditorium of the American National Insurance Company Building, Second Floor, One Moody Plaza, Galveston, Texas, at 10:00 a.m. local time on April 25, 2014 for the following purposes: 1. The election of a Board of nine (9) directors of the Company; 2. A non-binding advisory vote to approve the compensation of the Company’s executive officers as disclosed in the accompanying proxy statement; 3. A non-binding advisory vote on the desired frequency of future non-binding advisory votes on executive officer compensation; 4. Ratification of the appointment of KPMG LLP as auditors for 2014; and 5. The transaction of such other business as may properly come before the meeting or any adjournment thereof. Only holders of common stock of the Company of record at the close of business on March 3, 2014 are entitled to notice of, and to vote at, the meeting or any adjournment thereof. Except for the ratification of the appointment of KPMG LLP as auditors for 2014, your broker is not permitted to vote on your behalf on any matters to be considered at the stockholders’ meeting unless you provide specific instructions. For your vote to be counted, you will need to communicate your voting decisions to your broker, bank or other financial institution before the date of the stockholders’ meeting. -

Charting Our Course

AMERICAN NATIONAL INSURANCE COMPANY CHARTING OUR COURSE 2017 OVERVIEW AMERICAN NATIONAL Charting Our Course In 1905, William L. Moody, Jr. set out on a journey by offerings. In the following decades, operations expanded founding American National, a company he envisioned to include property and casualty insurance, health operating on the core ideals of “strong management, insurance and credit-related insurance. Existing lines also prudent investment and financial strength” – a company expanded to include newer and more innovative types of so fundamentally solid that it would still be thriving 500 products such as universal life and indexed life. years into the future. As the company has grown in size and scope, In American National’s first annual report, issued management has remained true to the core values of in 1910, W.L. Moody laid out his business philosophy – our founder by focusing on four corporate goals that one that still guides the company to this day; “Care and emphasize profitable growth, customer satisfaction, economy have been our watchwords in the management internal business processes, and employees and of the business …We see no reason why each year should learning. These four goals reflect our strategic focus, not record a greater success than the preceding one.” each supported by focused objectives. Key Performance In the earliest years, American National’s focus was Indicators will help effectively measure our progress on the on life insurance. Annuities were soon added to the journey forward. b | 2017 Annual Overview Beyond the Boundaries From our very first days with just 10 employees in financial products and services that offer security and 500-square-feet of Galveston office space we have grown peace of mind. -

March 2021 City Manager's Report

MARCH 2021 CITY MANAGER’S REPORT WWW.GALVESTONTX.GOV/CITYMANAGERSREPORT A MESSAGE FROM OUR CITY MANAGER Spring is a time for new beginnings, and we’re and increasing the size of the outfall at the bay to celebrating several at the City of Galveston. move water more quickly during storms. In April, we opened the new City Hall Plaza and Even as spring arrives, our crews are still busy celebrated with the dedication of the Hope stat- responding to the damage caused by the February ue, created by local sculptor Doug McLean as a winter storm. We continue clean-up in our parks, 1900 storm memorial. The plaza is the newest drainage system, and along roadways primarily public green space in the city and adds to years caused by landscaping debris. of positive changes on City Hall grounds, includ- We’ve gone through several emergencies in the ing the construction of Fire Station 1 and the last year. In addition to the pandemic, we experi- demolition of the City Hall annex. A generous enced three hurricanes and a winter storm. As we grant from the Moody Foundation funded the new approach the upcoming storm season, we’re ask- plaza, and the Hope statue was made possible by ing all residents to sign up for emergency alerts numerous local donors and sponsors. so we can stay in contact and keep you informed. We’ve also started construction on a major To sign up, visit alert.galvestontx.gov/subscribe. drainage project along 18th Street by installing Please take a moment to read through the latest large drainage boxes near Harborside Drive.