2014 Funds Budget

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Download The

August 31, 2015 The Honorable Arne Duncan U.S. Department of Education 400 Maryland Avenue, SW Washington, DC 20202 Dear Secretary Duncan: As college and university leaders, we appreciate the U.S. Department of Education’s responsiveness to concerns from the higher education community about a post-secondary rating system. Moreover, we support the Department’s recent announcement that it is instead focusing on the development of consumer-focused tools with newly available data. This effort could benefit students and their families, policymakers, and the public by providing them with new comparison tools and additional information on post-secondary institutions. That is why we are writing you about the Student Achievement Measure (SAM), a voluntary web-based tool that allows institutions to show the progress and graduation of significantly more students than the federal graduation rate. We know you share our belief that the most accurate data available should be used in order for these new tools to be effective and meaningful. Federal graduation rates as reported through the Integrated Postsecondary Education Data System (IPEDS) are a key piece of data likely under consideration for the new reporting tool. However, the commonly used federal graduation rate is limited to the success of first-time, full-time college students who graduate from their original institution. This has led to a misrepresentation of institutional performance because the federal rate does not account for the success of all students – particularly those students who attend multiple institutions. This month a report from the National Student Clearinghouse revealed that more than one- third of the 3.8 million first-time, full-time students who entered college in 2008 transferred at least once within six years and nearly half of those students changed institutions multiple times. -

Guide to Retirement in National Village

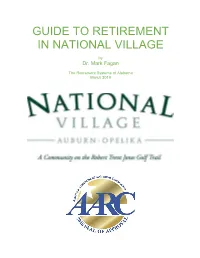

GUIDE TO RETIREMENT IN NATIONAL VILLAGE by Dr. Mark Fagan The Retirement Systems of Alabama March 2019 Seal of Approval for National Village National Village was selected in 2018 for the Seal of Approval Program of the American Association of Retirement Communities (AARC) by meeting their criteria for planned retirement communities. It received “best in class” recognition as a community which made a commitment, both in hard amenity offerings and soft programs, to provide a high- quality lifestyle for retirees. AARC is a not-for-profit professional association established in 1994 to support the efforts of states and municipalities, as well as community developers and for-profit businesses, who market to retirees. Master-Planned Developments in this program include Tennessee with two, North Carolina with two, Virginia with one, Arkansas with one, and Georgia with one. Now, Alabama has two (National Village and The Colony at The Grand in Fairhope). About National Village National Village in Auburn-Opelika, Alabama is one of two resort/retirement communities in Alabama under development by The Retirement Systems of Alabama (RSA). The second community is The Colony at The Grand in Fairhope, Alabama. RSA is the pension fund for public teachers and employees in Alabama. RSA has 358,000 members and $43 billion under management. RSA has many other investments in Alabama, including the Robert Trent Jones Golf Trail (26 golf courses at 11 sites, eight resort hotels, and six spas). RSA has developed 15 buildings and 14 parking decks in Alabama. RSA owns the largest office building in New York City (55 Water street) and is invested in television stations and newspapers. -

Minutes from February 5, 2016

MINUTES OF RECONVENED MEETING OF THE BOARD OF TRUSTEES OF AUBURN UNIVERSITY FEBRUARY 5, 2016 DRAFT SCHEDULE & AGENDA AUBURN UNIVERSITY BOARD OF TRUSTEES FEBRUARY 5, 2016 ROOMS 222-223, TAYLOR CENTER AUMCAMPUS THURSDAY, FEBRUARY 4, 2016 I. 1:30 p.m. - Workshop (President's Office Board Room, 107 Samford Hall) FRIDAY, FEBRUARY 5, 2016 I. Meetings (Room 222-223, Taylor Center, AUM Campus) **Meetings will begin at 9:30 a.m. -- all other meetings are subject to change in starting time, depending upon the length of individual meetings. A. Property and Facilities/Chairperson Roberts/9:30 a.m. 1. Band Practice Dressing Rooms, Storage Building, & Artificial Turf, Approval of Project Program, Site, Budget, Funding Plan, and Schematic Design (Dan King/Joe Aistrup) 2. Poultry Research Farm Unit Relocation-Phase I, Approval of Project Program, Site, Budget, Funding Plan, and Schematic Design (Dan King/Art Appel) 3. Auburn University Hotel P01te-Cochere and Front Drive Improvements, Approval of Project Initiation and Project Program, Site, Budget, Funding Plan, and Schematic (Dan King/Don Large) 4. Auburn University Hotel Governors Room, Board Room, and Restroom Renovations, Approval of Project Initiation and the Project Architect Selection (Dan King/Don Large) 5. Mell Classroom Building, Approval of Budget Increase (Dan King/Tim Boosinger) 6. Public Safety Building Expansion, Approval of Project Initiation and Authorization to Commence the Project Architect Selection Process (Dan King/Melvin Owens) 7. Campus Master Plan Update: Landscape Master Plan & Building Element (Dan King) 8. North Auburn Telecommunication Tower Lease (Dan King/Mark Stirling) 9. North Parking Deck Real Estate Acquisition (Dan King/Mark Stirling) 10. -

August 31, 2015 the Honorable Arne Duncan U.S. Department Of

August 31, 2015 The Honorable Arne Duncan U.S. Department of Education 400 Maryland Avenue, SW Washington, DC 20202 Dear Secretary Duncan: As college and university leaders, we appreciate the U.S. Department of Education’s responsiveness to concerns from the higher education community about a post-secondary rating system. Moreover, we support the Department’s recent announcement that it is instead focusing on the development of consumer-focused tools with newly available data. This effort could benefit students and their families, policymakers, and the public by providing them with new comparison tools and additional information on post-secondary institutions. That is why we are writing you about the Student Achievement Measure (SAM), a voluntary web-based tool that allows institutions to show the progress and graduation of significantly more students than the federal graduation rate. We know you share our belief that the most accurate data available should be used in order for these new tools to be effective and meaningful. Federal graduation rates as reported through the Integrated Postsecondary Education Data System (IPEDS) are a key piece of data likely under consideration for the new reporting tool. However, the commonly used federal graduation rate is limited to the success of first-time, full-time college students who graduate from their original institution. This has led to a misrepresentation of institutional performance because the federal rate does not account for the success of all students – particularly those students who attend multiple institutions. This month a report from the National Student Clearinghouse revealed that more than one- third of the 3.8 million first-time, full-time students who entered college in 2008 transferred at least once within six years and nearly half of those students changed institutions multiple times. -

War Eagles: Auburn University's Tradition of Training Soldiers By

War Eagles: Auburn University’s Tradition of Training Soldiers by Daniel Garrison McCall A thesis submitted to the Graduate Faculty of Auburn University in partial fulfillment of the requirements for the Degree of Master of Arts Auburn, Alabama May 4, 2014 Reserve Officers’ Training Corps, Army, Auburn University, Specialized Training Program, Summer Camp, Land-grant Copyright 2014 by Daniel McCall Approved by Mark Sheftall, Assistant Professor of History Charles Israel, Associate Dean for Academic Affairs and Associate Professor of History David Carter, Associate Professor of History Abstract As a land-grant university, Auburn University maintains a tradition of training American soldiers. Its Army Reserve Officers’ Training Corps (ROTC) unit was once central to campus life, but in 1969 the university eliminated its mandatory ROTC program. Having offered a remarkable contribution to national defense, as a case study Auburn University Army ROTC embodies an exceptional microcosm for understanding how the United States government has prepared the Army to fight wars requiring mass mobilization. With the old model of cadet training based upon raising a mass army to fight wars in the industrial age and the new model based upon fighting wars with more powerful weaponry but fewer personnel in the modern age of science and technology, examining how these developments within the Army interrelate to the evolution of Auburn University Army ROTC provides an opportunity to consider the significance of how Auburn’s commitment as a land-grant university to supporting ROTC has remained constant, although the centrality of Army ROTC to campus life is dramatically different. ii Table of Contents Abstract .............................................................................................................................. -

From the Dean Bonnie Macewan

FALL ISSUE 2008 FALL ISSUE 2008 From the Dean Bonnie MacEwan Last year was a busy one for We’ve undertaken many efforts to move our goals forward. the libraries and you may notice Some are changes to the building including a major expansion of we haven’t slowed down since the Digital Resources Lab with generous funding from Provost the summer. As we prepare for John Heilman and Executive Vice President Don Large. The the future, we can step back and DRL now includes Movies, Music and More bringing our non- assess all we’ve accomplished print media resources together with our digital capabilities and and take stock of the next providing both production and viewing spaces. On the third projects we hope to tackle. floor, we’ve designated space for graduate student and faculty After a broad-ranging individual study. With funding from the Concessions Board and series of assessment activities input from the Graduate Student Council, we will be furnishing with students, faculty and the area for comfortable and productive research. You may notice community members, we our new color scheme selected in collaboration with the Student developed a strategic plan for Advisory Council. Watch for new carpeting to be installed on the next five years. It is available the first and second floors during the winter break. Two of at www.lib.auburn.edu/summit. our instruction labs have been renovated to allow for laptop I’d encourage you to take a look and let us know what you think. computer use or reading when classes are not in session. -

Cole Bennett

Table of Contents Auburn Football . .13-29 History . .133-183 2007 Quick Facts Academics . .14-15 All-Time Results . .133-147 Jordan-Hare Stadium . .16-19 Miscellaneous . .148 Practice Facilities . .19 Yearly Records . .149 General Information Auburn Strength and Conditioning . .20-21 Records vs. All Opponents . .150 Location ....................................................Auburn, Ala. Auburn Sports Medicine . .22-23 Results vs. 2007 Opponents . .151-152 Founded....................................................................1856 Uniquely Auburn . .24-26 Auburn Bowl History . .153 Enrollment ............................................................23,547 The Fable of War Eagle . .27 Lettermen . .154-164 President ..................................................Dr. Jay Gogue Aubie . .28 All-Time Coaching Records . .165 Athletics Director ..........................................Jay Jacobs Auburn’s Symbols . .29 Pat Sullivan, 1971 Heisman . .166 Faculty Representative ....................Marcia Boosinger Bo Jackson, 1985 Heisman . .167 Nickname ..............................................................Tigers 2007 Outlook . .30-38 Zeke Smith, 1958 Outland . .168 Colors ............................Burnt Orange and Navy Blue Tracy Rocker, 1988 Outland/Lombardi . .169 ..........................................................(PMS 172 and 289) Alphabetical Roster . .30-31 Carlos Rogers, 2004 Jim Thorpe . .170 Stadium........................Jordan-Hare Stadium (87,451) Numerical Roster . .32-33 Auburn All-Americans . .171-178 -

David Bransby Receives Award for Excellence from the President’S Office

• AUBURN UNIVERSITY’S OUTREACH SCHOLARSHIP MAGAZINE • FALL 2006 David Bransby Receives Award for Excellence from the President’s Office At Auburn, we are continually expanding on our base of extension, continuing education and technical assistance services to engage the university’s research and faculty expertise to create practical solutions for the challenges of today and tomorrow. From alternative energy applications to natural disaster response, Auburn outreach is making a difference. It’s exciting work that promises to positively impact quality of life in Alabama and around the world. Auburn University’s outreach mission has changed significantly over the decades, but our goal remains the same — reach out, serve, make a difference. That’s Auburn’s promise to this and future generations. Auburn must become an even more integral part of the economic development of Alabama which will involve the positioning of AU’s programs for the next 25 years. I remain confident that in 2031 when AU celebrates its 175th birthday, alumni and supporters will look back at 2006 and confirm that it was indeed a benchmark year. Sincerely, ED RICHARDSON PRESIDENT AUBURN UNIVERSITY Dear Friends: As we approach the last quarter of Auburn University’s sesquicentennial, it’s important to recognize Auburn’s long standing commitment to helping people improve their lives through our outreach programs. From our beginnings in agricultural and mechanical ON THE COVER applied research, Auburn’s faculty have built an impressive Switchgrass growth rate measured at an Auburn research site. body of innovative programming and services responsive to the needs of people. Auburn serves the farmer and the ------ Submit news items and story ideas to Teresa Whitman-McCall, Office of engineer, but also the teacher and the business owner. -

War Eagle Girls and Plainsmen Tour Information

War Eagle Girls and Plainsmen Tour Information SAMFORD HALL (1888) HISTORY: The original building on this site was Old Main, the main classroom building of East Alabama Male College. CURRENT USE: The building now holds the Administration and the Office of the President. INTERESTING FACT(S): Old Main burned down on June 24, 1887 and Samford Hall was built to replace it shortly after. In the early days of Samford Hall it served as classrooms, Library and administrative offices. The building is named for William James Samford, who is an Auburn graduate and served as the 31st Governor of the State of Alabama. Donated in 1977 by a family in Opelika, an electric carillon in the tower plays hourly and the fight song at noon. Samford Hall and the University Chapel across the street were used as hospitals for wounded soldiers in the battle of Atlanta during the Civil War. The name Samford has been closely associated with Auburn throughout its history. A family member has served on the board of trustees for 80 of the last 100 years. LANGDON HALL (1846): HISTORY: Originally built as a chapel for the Auburn Masonic Female College for $2,500. INTERESTING FACT(S): It soon became the first public meeting hall for Auburn and hosted the famous secession debates in the late 1850's. Langdon served as classrooms after Old Main burned down in 1887, and graduation exercises were held there for many years. It’s named after Charles Carter Langdon, a trustee from 1872-1889. The building was rolled on logs from North Gay Street to its present location in 1883. -

Auburn University

PARENT RESOURCE GUIDE FROM THE OFFICE OF PARENT AND FAMILY PROGRAMS ABOUT CONTACT The Office of Parent and Family Programs WEBSITE auburn.edu/aupa keeps you informed about campus news, PHONE (334) 844-1493 dates to remember, resources to ensure EMAIL [email protected] your student's academic success, and ADDRESS 255 Heisman Drive exciting campus events. Student Center 3248 Auburn, AL 36849 1 ABOUT THE OFFICE OF PARENT AND FAMILY PROGRAMS The Office of Parent and Family Programs is your one-stop-shop for all questions while your student is at Auburn University. Located in the Division of Student Affairs, Parent and Family Programs is the one office on campus designed specifically to serve you. MEET THE STAFF: AUBURN UNIVERSITY Tess Gibson joined the Office of Parent PARENTS’ ASSOCIATION: and Family Programs as Coordinator in Participating in the Auburn University Parents’ Association May 2014. Tess is a two-time alumna (AUPA) is an excellent way to stay connected as a part from Auburn University. She earned of the Auburn Family and support the education of your her Bachelor of Arts in Political student. As a member, you will receive information regarding Science with a concentration in Public important dates, deadlines and events that are relevant to Administration, and then completed you and your student. her Masters in Administration of Higher Education. Prior to her time working with Parent and Through activities such as Home Sweet Auburn and Fall Family Programs, Tess served as a graduate assistant in both Family Weekend, the Parents’ Association provides you with First Year Experience and Student Involvement. -

August 31, 2015 the Honorable Arne

August 31, 2015 The Honorable Arne Duncan U.S. Department of Education 400 Maryland Avenue, SW Washington, DC 20202 Dear Secretary Duncan: As college and university leaders, we appreciate the U.S. Department of Education’s responsiveness to concerns from the higher education community about a post-secondary rating system. Moreover, we support the Department’s recent announcement that it is instead focusing on the development of consumer-focused tools with newly available data. This effort could benefit students and their families, policymakers, and the public by providing them with new comparison tools and additional information on post-secondary institutions. That is why we are writing you about the Student Achievement Measure (SAM), a voluntary web-based tool that allows institutions to show the progress and graduation of significantly more students than the federal graduation rate. We know you share our belief that the most accurate data available should be used in order for these new tools to be effective and meaningful. Federal graduation rates as reported through the Integrated Postsecondary Education Data System (IPEDS) are a key piece of data likely under consideration for the new reporting tool. However, the commonly used federal graduation rate is limited to the success of first-time, full-time college students who graduate from their original institution. This has led to a misrepresentation of institutional performance because the federal rate does not account for the success of all students – particularly those students who attend multiple institutions. This month a report from the National Student Clearinghouse revealed that more than one- third of the 3.8 million first-time, full-time students who entered college in 2008 transferred at least once within six years and nearly half of those students changed institutions multiple times. -

2008 WT MG.Qxp

Table of Contents/Quick Facts Table of Contents Preview SEC/Opponents 2008 Quick Facts Table of Contents/Quick Facts ____________1 2007 SEC Standings ______________________18 General Information Roster________________________________________2 2008 Opponenets ____________________19-20 School__________________________________Auburn University Covering The Tigers ________________________2 Location ______________________________________Auburn, Ala. Outlook____________________________________3-4 History/Records Founded ______________________________________________1856 All-Time Results __________________________21 Enrollment ________________________________________23,547 Coaching Staff Year-By-Year Results__________________22-25 Nickname____________________________________________Tigers Head Coach Tim Gray ______________________5 All-Time Victories ________________________26 Conference __________________________________Southeastern Assistant Coach Ashley Bentley____________6 Coaching History__________________________27 Colors ______________________Burnt Orange and Navy Blue Jay Swamidass, Alyss Hart ________________6 All-Time Awards __________________________28 __________________________________(PMS 158 and PMS 289) All-Time Letterwinners __________________29 President ____________________________________Dr. Jay Gogue Athlete Profiles Athletics Director ______________________________Jay Jacobs Whitney Chappell __________________________7 Auburn University Associate Athletics Director/SWA ____Meredith Jenkins Assistant Athletics Director ________________David