Dow Jones STOXX Indices Rulebook

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Euro Stoxx 50® Index

MARKET-LINKED PRODUCTS UNDERLIER: EURO STOXX 50® INDEX Market-Linked Products, considered complex investments, are linked to the performance of an underlying asset, such as the EURO STOXX 50® Index (“Index”). Dividends paid on the underlier are not passed through to the Market- Linked Product. If held to maturity, any potential coupon payments or gains will be paid out based on the performance of the Index, as detailed in the offering documents. Additionally, your statement value will reflect any upward or downward movements in the volatility of the Index. ® EURO STOXX 50 Index – Historical Look at Gains & Losses The chart below illustrates the number of times the Index’s return, measured from the beginning to the end of different time periods within the past 20 years, landed within various return ranges. Total Rolling Total Total 0 to -6 to -11 to -16 to -21 to -26 to -31 to -36 to 0% to 11 to 21 to 31 to Periods Gains Losses -5% -10% -15% -20% -25% -30% -35% -40% < -40% 10% 20% 30% 40% > 40% 1-Yr 229 131 98 16 17 14 16 11 7 4 5 8 46 63 16 5 1 3-Yr 205 113 92 14 11 10 11 9 7 13 10 7 31 29 10 10 33 5-Yr 181 105 76 10 6 9 11 13 9 1 1 16 25 20 15 23 22 7-Yr 157 89 68 5 4 5 8 11 24 7 2 2 26 17 17 15 14 10-Yr 121 65 56 3 6 4 9 15 1 8 9 1 16 23 14 7 5 The chart below illustrates the percentage of times1 (based on total rolling periods) the Index’s return, measured from the beginning to the end of different time periods within the past 20 years, landed within various return ranges. -

Annual Report 2019 Contains a Full Overview of Its Corporate Stakeholder Expectations As Well As Long-Term Trends Governance Practices

Table of Contents Management report Company overview ............................................................................................................................................................................... 4 Business overview ................................................................................................................................................................................ 5 Disclosures about market risk ............................................................................................................................................................... 44 Group organizational structure ............................................................................................................................................................. 47 Key transactions and events in 2019 .................................................................................................................................................... 50 Recent developments ........................................................................................................................................................................... 53 Research and development .................................................................................................................................................................. 54 Sustainable development .................................................................................................................................................................... -

Prospectus Sicav Bnp Paribas Easy Fr

PROSPECTUS SICAV BNP PARIBAS EASY FR A SICAV (OPEN-ENDED COLLECTIVE INVESTMENT SCHEME) COVERED BY EUROPEAN DIRECTIVE 2009/65/EC 1 PROSPECTUS – SICAV BNP PARIBAS EASY FR I- GENERAL CHARACTERISTICS I.1 - FORM OF THE UCITS NAME: BNP PARIBAS EASY FR LEGAL FORM AND MEMBER STATE IN WHICH THE UCITS WAS ESTABLISHED: A French société d investissement à capital variable (hereafter the "SICAV") having its registered office at 1, boulevard Haussmann, 75009 PARIS, registered at the Paris Trade and Companies Registry (RCS). CREATION DATE AND INTENDED LIFETIME: The SICAV was created on 16 September 2013 for a term of 99 years. FUND OVERVIEW: BNP PARIBAS EASY STOXX EUROPE 600 UCITS ETF: MINIMUM MINIMUM CURRENCY LISTING INITIAL NET ALLOCATION SUBSCRIPTION AMOUNT OF OF SUBSCRIBERS EXCHANGE NAME ASSET ISIN CODES OF DISTRIBUTABLE AMOUNT PURCHASES/SAL DENOMIN CONCERNED (SECONDARY VALUE AMOUNTS (PRIMARY ES (SECONDARY ATION MARKET) MARKET) MARKET) EUR 2 million EUR EURONEXT apart from 36.3757 PARIS companies of All the BNP EUR C (Divided FR0011550193 Accumulation EUR subscribers ONE UNIT XETRA Paribas by 5 on 8 Group and June authorised SIX SWISS 2018) participants EXCHANGE EUR EUR 2 million EURONEXT 100.000 apart from PARIS 0 Accumulation companies of All EUR C/D FR0011550672 and/or EUR the BNP ONE UNIT XETRA (Divided subscribers Distribution Paribas Group by 14 on and authorised 8 June SIX SWISS participants 2018) EXCHANGE BNP PARIBAS EASY S&P 500 UCITS ETF: MINIMUM MINIMUM CURRENCY LISTING ALLOCATION SUBSCRIPTION AMOUNT OF INITIAL NET OF SUBSCRIBERS EXCHANGE -

In EURO STOXX 50®

EURO STOXX 50® ESG Futures & Options Launch date 9 Nov 2020 August 2021 EURO STOXX® 50 ESG Futures & Options Eurex has been the first exchange establishing ESG versions of major European benchmarks ▪ The product suite offers a hedging alternative to existing benchmarks ▪ Expanding product suite to the most liquid benchmark(s) incorporating ESG ▪ Strong support by Market Makers and Banks onscreen and off-book, as demand in ESG increases as a general investment approach ▪ Better performance of ESG also during the COVID19 market turbulence ▪ Incorporating ESG means lowering the risk ▪ Easy and understandable index concept ▪ The indexes incorporate the broadest exclusions while seeking to maintain a profile similar to market cap indexes ▪ Screening of the minimum standards / ESG screen1) ▪ Weight selected securities by free-float market capitalization ▪ Fast Exit Rule 1) (As identified by Sustainalytics. Additionally, companies w hich do not have product involvement data are not considered for selection. Companies w ith no ESG scores are assigned a zero score) 2 August 2021 Internal Development EURO STOXX 50 STOXX EURO Development Capitalised Volume in M. EUR 1,000,000 1,500,000 2,000,000 2,500,000 500,000 0 Nov-10 Feb-11 May-11 Aug-11 Nov-11 Feb-12 May-12 Capitalized Volume in EUR Volume Capitalized Aug-12 Nov-12 Feb-13 May-13Maker Market Aug-13 Nov-13 Feb-14 May-14 Agent Aug-14 Nov-14 Feb-15 May-15 Aug-15 Nov-15 Capitalized Open Interest Adjusted in EUR Interest Adjusted Open Capitalized Feb-16 May-16 Aug-16 Nov-16 Feb-17 May-17 Aug-17 Nov-17 Internal Feb-18 May-18 ® 3 Aug-18 Nov-18 (FESX) Futures Feb-19 May-19 Aug-19 Nov-19 Feb-20 May-20 Aug-20 Nov-20 Feb-21 May-21 Aug-21 0 20,000 40,000 60,000 80,000 100,000 120,000 140,000 160,000 180,000 Capitalised Open Interest in M. -

Annual Report 2019 Contains a Full Overview of Its Corporate Stakeholder Expectations As Well As Long-Term Trends Governance Practices

Table of Contents Management report Company overview 4 Business overview 5 Disclosures about market risk 44 Group organizational structure 47 Key transactions and events in 2019 50 Recent developments 53 Research and development 54 Sustainable development 57 Corporate governance 67 Luxembourg takeover law disclosure 108 Additional information 110 Chief executive officer and chief financial officer’s responsibility statement 115 Financial statements of ArcelorMittal parent company for the year ended December 31, 2019 116 Statements of financial position 117 Statements of operations and statements of other comprehensive income 118 Statements of changes in equity 119 Statements of cash flows 120 Notes to the financial statements 121 Report of the réviseur d’entreprises agréé 170 4 Management report Company overview other countries, such as Kazakhstan, South Africa and Ukraine. In addition, ArcelorMittal’s sales of steel products History and development of the Company are spread over both developed and developing markets, which have different consumption characteristics. ArcelorMittal is the world’s leading integrated steel and ArcelorMittal’s mining operations, present in North and mining company. It results from the merger in 2007 of its South America, Africa, Europe and the CIS region, are predecessor companies Mittal Steel Company N.V. and integrated with its global steel-making facilities and are Arcelor, each of which had grown through acquisitions over important producers of iron ore and coal in their own right. many years. Since its creation ArcelorMittal has experienced periods of external growth as well consolidation Products: ArcelorMittal produces a broad range of high- and deleveraging (including through divestments), the latter quality finished and semi-finished steel products (“semis”). -

Euro Stoxx 50® Corporate Bond Index

BOND INDEX FACTSHEET 1/2 EURO STOXX 50® CORPORATE BOND INDEX STOXX® EUROPE 600 EURO STOXX 50® REGIONS COUNTRIES SIZES SUPERSECTORS STYLE, STRATEGIES & THEME BOND STATED OBJECTIVES INDEX PERFORMANCE* The EURO STOXX 50® Corporate Bond Index tracks the performance of the 140 Euro-denominated, investment grade corporate bonds of the EURO STOXX 120 100 50® constituents – the equity index that is established as the gauge of the 80 Eurozone equity market. The issuers are the highly liquid, top-flight blue-chip 60 companies of the Eurozone which are also household names for the investors. 40 As such, the EURO STOXX 50® Corporate Bond Index is the fixed income 20 equivalent of the unrivalled equity index for the Eurozone region. 0 The bond index provides exposure to the most liquid and representative EURO STOXX 50® Corporate Bond Price Index EUR EURO STOXX 50® Corporate Bond Total Return Index EUR Eurozone investment grade corporate bonds, giving access to approximately 250-300 bonds in its universe. Its performance profile shows stability and ANNUAL RETURNS high risk-adjusted return, while offering a diversified allocation across geographies, credit ratings, sectors and industries. 12% EURO STOXX 50® Corporate Bond Total Return Index EUR 10% EURO STOXX 50® Corporate Bond Price Index EUR KEY FACTS 8% 6% 4% REAL-TIME CALCULATION STOXX® bond index calculations are performed in real-time every minute 2% providing enhanced market transparency. 0% -2% -4% EXPOSURE AND DIRECT LINK TO THE BENCHMARK 2010 2011 2012 2013 2014 2015 YtD (2016) The concept is designed to provide a direct link to the widely recognized equity benchmark, EURO STOXX 50®, and therefore can serve as a basis for a consistent analysis of bond and equity markets. -

Euro Stoxx® Islamic 50 Index

FAITH-BASED INDICES 1 EURO STOXX® ISLAMIC 50 INDEX Stated objective Key facts The STOXX Islamic Indices are designed to provide European and » The underlying share basket is composed of liquid stocks to ensure Eurozone equity market exposure in compliance with it can be tracked by a wide range of financial products Shariahprinciples. The index components are selected by means of an advanced proprietary screening technique. The screening process is monitored by the STOXX European Islamic Index Shariah Supervisory Board, comprising Dr. Abdul Aziz Khalifah Al-Qassar, Dr. Eissa Zaki Eissa and Dr. Esam Al-Enezi.The following indices are calculated: the STOXX Europe Islamic, which is derived from the STOXX Europe 600; the STOXX Europe Islamic 50 and the EURO STOXX Islamic 50, which are blue-chip indices derived from the STOXX Europe Islamic Index. Descriptive statistics Index Market cap (EUR bn.) Components (EUR bn.) Component weight (%) Turnover (%) Full Free-float Mean Median Largest Smallest Largest Smallest Last 12 months EURO STOXX Islamic 50 Index 1,542.4 1,227.9 24.6 13.0 119.3 6.0 9.7 0.5 46.2 EURO STOXX Index 4,398.5 3,240.8 11.0 4.5 119.3 1.0 3.7 0.0 3.7 Supersector weighting (top 10) Country weighting Risk and return figures1 Index returns Return (%) Annualized return (%) Last month YTD 1Y 3Y 5Y Last month YTD 1Y 3Y 5Y EURO STOXX Islamic 50 Index 2.0 5.8 17.9 60.5 74.2 26.0 8.6 17.5 16.6 11.4 EURO STOXX Index 1.6 4.5 19.2 56.3 49.3 21.1 6.6 18.8 15.6 8.1 Index volatility and risk Annualized volatility (%) Annualized Sharpe ratio2 EURO STOXX Islamic 50 Index 16.3 13.0 12.5 17.8 18.5 0.2 0.7 1.2 0.9 0.6 EURO STOXX Index 15.2 13.3 12.7 19.3 20.0 -0.1 0.5 1.2 0.8 0.4 Index to benchmark Correlation Tracking error (%) EURO STOXX Islamic 50 Index 1.0 1.0 1.0 1.0 1.0 3.7 3.9 3.7 4.4 4.9 Index to benchmark Beta Annualized information ratio EURO STOXX Islamic 50 Index 1.0 0.9 0.9 0.9 0.9 1.1 0.5 -0.3 0.1 0.5 1 For information on data calculation, please refer to STOXX calculation reference guide. -

EURO STOXX 50 Index

EURO STOXX 50® Europe’s Leading Blue-Chip Index June 2020 1 | Confidential – Not for Redistribution – Copyright © 2020 Qontigo GmbH. Qontigo is part of Deutsche Börse Group. Content 02 Introduction Drivers of Strategic and Tactical 12 Allocations to the Eurozone 17 Appendix STOXX is now Part of Qontigo… A new financial intelligence driver, modernizing investment management Index Analytics STOXX & DAX AXIOMA World-class indices that are licensed to more Best of breed portfolio construction and risk than 500 companies, including the world’s analytics tools. largest financial product issuers, capital owners and asset managers. 3 | Confidential – Not for Redistribution – Copyright © 2020 Qontigo GmbH. Qontigo is part of Deutsche Börse Group. EURO STOXX 50® - A Unique Offering for Liquid, Diversified Access to the Eurozone Features Regional Coverage1) ▪ Comprehensive and transparent: completely rules-based coverage of the Eurozone1) ▪ Balanced: selection mechanism ensures balanced representation of supersectors using Industry Classification Benchmark (ICB) ▪ Representative and liquid: coverage of about 60% of total free-float through liquid supersector leaders. Components ranked and weighted by free-float subject to 10% cap ▪ Continuous pulse on market changes: quarterly rebalancing, annual review ▪ Established: launched on Feb. 26, 1998 1) Country composition as of March 2020: Belgium, Finland, France, Germany, Ireland, Italy, Luxembourg, the Netherlands and Spain 4 | Confidential – Not for Redistribution – Copyright © 2020 Qontigo GmbH. Qontigo is part of Deutsche Börse Group. Methodology Leads to Balanced Representation of Eurozone Supersector Leaders Sub- Universe universes Pre-selection Selection Weighting ... rank stocks by free- EURO STOXX® Select 50 largest float and select largest (covers approximately Within each of the 19 stocks as measured Weight by free-float stocks jointly by free-float from all subject to 10% cap 95% of Eurozone free- supersectors .. -

Euro Stoxx 50® Index

EURO STOXX 50® INDEX Components1 Company Supersector Country Weight (%) ASML HLDG Technology Netherlands 7.89 LVMH MOET HENNESSY Consumer Products & Services France 6.03 SAP Technology Germany 4.31 LINDE Chemicals Germany 4.16 TOTALENERGIES Energy France 3.47 SANOFI Health Care France 3.35 SIEMENS Industrial Goods & Services Germany 3.34 L'OREAL Consumer Products & Services France 3.18 ALLIANZ Insurance Germany 2.99 SCHNEIDER ELECTRIC Industrial Goods & Services France 2.49 AIR LIQUIDE Chemicals France 2.29 AIRBUS Industrial Goods & Services France 2.18 DAIMLER Automobiles & Parts Germany 2.16 IBERDROLA Utilities Spain 2.10 ENEL Utilities Italy 2.09 BNP PARIBAS Banks France 2.07 BASF Chemicals Germany 1.98 DEUTSCHE TELEKOM Telecommunications Germany 1.90 BCO SANTANDER Banks Spain 1.90 VINCI Construction & Materials France 1.86 DEUTSCHE POST Industrial Goods & Services Germany 1.85 Kering Retail France 1.83 ADYEN Industrial Goods & Services Netherlands 1.81 ANHEUSER-BUSCH INBEV Food, Beverage & Tobacco Belgium 1.79 ADIDAS Consumer Products & Services Germany 1.79 BAYER Health Care Germany 1.73 SAFRAN Industrial Goods & Services France 1.58 AXA Insurance France 1.52 ESSILORLUXOTTICA Health Care France 1.48 INTESA SANPAOLO Banks Italy 1.43 ING GRP Banks Netherlands 1.42 INFINEON TECHNOLOGIES Technology Germany 1.41 VOLKSWAGEN PREF Automobiles & Parts Germany 1.33 PHILIPS Health Care Netherlands 1.31 DANONE Food, Beverage & Tobacco France 1.27 Prosus Technology Netherlands 1.25 PERNOD RICARD Food, Beverage & Tobacco France 1.23 Industria -

PR ENGIE Acquires

Press release 6 Decembre 2018 ENGIE acquires services provider, CAM and strengthens its customer solutions offer in Latin America In line with ENGIE’s strategy to strengthen its customer solutions offer in Latin America, the Group acquired today CAM (Compañía Americana de Multiservicios), leader in the field of installation, operation and maintenance services for the electricity and telecommunications sectors in the region. Through this transaction, ENGIE focuses on the customer services segment as a pillar of growth and value creation in Latin America. This acquisition will reinforce the Group’s presence in the region and will expand ENGIE’s access to an extensive range of industrial and utility customers of different sizes. The Group is now consolidating a unique and comprehensive offer comprising a wide range of solutions in energy infrastructure, power generation and specialized customer services. Following the integration of CAM’s 10,000 employees, ENGIE’s Latin America Business Unit will triple its headcount from 4,800 employees to approximately 15,000. Pierre Chareyre, ENGIE Executive Vice-President, in charge of the business units Global Energy Management and Latin America said: "By combining ENGIE and CAM’s activities in Latin America, the Group is taking an important step in the implementation of its regional strategy, focused on the development of customer solutions.” Pierre Devillers, ENGIE Latin America Chief Customer Solutions Officer added: “In the context of the energy transition and the digital transformation, this acquisition will broaden ENGIE’s expertise and expand its offer for industrial clients and cities. The Group’s ambition is to build a multi-solution and multi-country platform serving its current and future clients." ENGIE’S Latin America business unit (excluding Brazil) is present in Chile, Argentina, Peru and Mexico. -

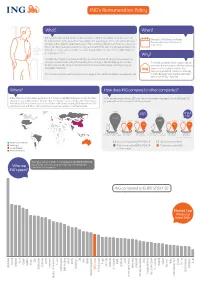

2015 Remuneration Fact Sheet

ING’s Remuneration Policy What? When? ING needs to attract and retain excellent leaders so that it can deliver on its promise to its Changes to ING’s Executive Board 34 million clients in the more than 40 countries it is operating in. At the same time, ING has Remuneration are eective as of to balance the interests of all stakeholders. The Supervisory Board reconfirms its support of 1 Jan 2016. ING´s Executive Board Remuneration Policy aimed at further reducing the gap between the total direct compensation of ING’s Executive Board and the median of the EURO STOXX 50 peer group over time. Why? For 2016, the Supervisory Board decided to increase the total (at target) remuneration of Executive Board members by 2%. Including these changes, ING will still pay its Executive To remain competitive, ING needs to attract Board well below the median for national and international companies in its peer group and retain the best leaders with international (the EURO STOXX 50). experience for its global activities. The Supervisory Board will continue to annually For more information see the remuneration page or the full Annual Report on www.ing.com. monitor developments and the applicable benchmark (EURO STOXX 50). Where? How does ING compare to other companies? ING is a European bank with a global presence. It has over 54,000 employees serving 34 million ING’s total remuneration for its CEO is far below the median (see graph). Also, its CFO and CRO customers across 40 countries. At least 70% of employees work outside of the Netherlands. -

Euro Stoxx® 50 Low Carbon Index

THEME INDICES 1 EURO STOXX® 50 LOW CARBON INDEX Index description Key facts These STOXX Low Carbon indices cover benchmark indices and the blue-chip »Derived from STOXX broad, yet liquid broad indices to ensure tradability. index EURO STOXX 50®. By utilizing both estimated and reported carbon intensity scores, this index family represents broad indices with a variable »As indices derived from those well-known broad indices, investor can easily number of components, covering the regions Global, Europe, Eurozone, USA use it for benchmark purposes. and Japan. These indices closely track the risk-return profile of the underlying benchmark indices while offering a reduction in carbon »Comprehensive offering by covering global regions, Europe, Eurozone and USA. emissions in the overall portfolio of constituents by overweighting lower carbon emitters, while underweighting higher carbon emitters. »Usage of a reliable data sources: CDP for reported data. »Only companies with reported data are available for selection. STOXX uses CDP and ISS ESG as reliable and professional data sources for the estimated and reported data. Data considered comprise Scope 1 (All direct GHG emissions) and Scope 2 (Indirect GHG emissions from consumption of purchased electricity, heat or steam) emissions. Descriptive statistics Index Market cap (USD bn.) Components (USD bn.) Component weight (%) Turnover (%) Full Free-float Mean Median Largest Smallest Largest Smallest Last 12 months EURO STOXX 50 Low Carbon Index N/A 101,495.7 2029.9 1619.4 6166.8 218.0 6.1 0.2 14.6