International Wire Transfer Quick Tips &

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pledged Asset Line® Wire Transfer Request and Authorization | 1-800-838-6573

Pledged Asset Line® Wire Transfer Request and Authorization www.schwab.com/pal | 1-800-838-6573 • Wire forms received prior to 1:30 p.m. Eastern time (10:30 a.m. Pacific time) on a Business Day will be processed by the end of the following Business Day. • For your protection, we must contact you by phone to verify your identity before the wire transfer can be completed. • There is no fee associated with this wire request. • We do not process any wire transfers sent from or to international banks, even if the currency is in U.S. dollars (USD). • Submit this form via secure message on Schwab.com or fax to Charles Schwab Bank at 1-877-300-6933. • Your initial draw may require a minimum. • Please contact us if you have any questions regarding this information. You may not borrow money on a Pledged Asset Line to purchase securities or pay down margin loans, or deposit advances from the line into any brokerage account. 1. Account Holder Information Name (First) (Middle) (Last) Telephone Number* Address City State Zip Code Country *Please provide a number so you can be reached for call-back verification purposes. 2. Outgoing Wire Information Date Wire to Be Sent Amount of Wire (in USD only) $ Pledged Asset Line Account Number (12 digits) Account Title (owner name) 3. Receiving Beneficiary/Bank Information Beneficiary Name (First) (Middle) (Last) Beneficiary Account Number at Bank Beneficiary Address City State Zip Code Country Beneficiary Bank Name Beneficiary Bank ABA or Account Number at Send-Through Bank Beneficiary Bank Address (if available) City State Zip Code Country Additional Instructions (Attention to, Customer Reference, Phone Advice) Send-Through Bank Name Send-Through Bank ABA Number Send-Through Bank Address (if available) City State Zip Code Country 4. -

BANKING FEES All Fees Include GCT ACCOUNT OPENING SAVINGS ACCOUNT

JMMB BANK BANKING FEES All fees include GCT ACCOUNT OPENING SAVINGS ACCOUNT CURRENT ACCOUNT Cheque Leaves Acquisition (Retail) J$2912.50 Cheque Leaves Acquisition (SME) J$5825.00 Cheque Leaves Acquisition (Corporate) J$17,475.00 Monthly Service Charge FREE Cheque Writing J$50.00 Returned Cheque (Own Bank)/Chargeback Item J$873.75 J$450.00 Stop Payment (Own Bank) J$5000.00 maximum TRANSACTION RELATED CASH DEPOSITS 1% + GCT (1.17%) on investment/deposits equal to 1,500 units or above in each currency, subject to a per client limit of 500 units per business day Cash Deposits - Foreign Currency and 1,500 units per calendar month. Cash Deposits in excess of J$1M Free CHEQUE DEPOSITS Returned Cheque J$640.75 Cheque Deposit - Collection Item (US) US$6.99 + Other Bank Charge J$640.75 Foreign Cheque Returned + Other Bank Charge Foreign Cheque Stop Payment US$14.88+ Other Bank Charge Cheque Deposit - Same Day Value (JMMB Bank Cheques) Free CASH WITHDRAWALS Cash Withdrawals up to J$1,000,000.00 Free CHEQUE WITHDRAWALS TRANSFERS WITHIN JMMB BANK Transfer Between Own Accounts (Internal Transfer) Free TRANSFERS TO AND FROM LOCAL INSTITUTIONS Returned/Recalled Electronic Transfers (Local) J$500.00 Transfer to other financial institution/ Third party (Local ACH) J$25.00 Wire - Incoming and Outgoing RTGS Transfers J$250.00 TRANSFERS TO AND FROM INTERNATIONAL INSTITUTIONS International Wire Transfer -Inbound - USD US$23.30 International Wire Transfer -Inbound - GBP n/a International Wire Transfer -Inbound - CAD n/a International Wire Transfer -Inbound -

Fedwire® Funds Service Produc T Sheet

Fedwire® Funds Service The Fedwire Funds Service is the premier wire-transfer service that financial institutions and businesses rely on to send and receive time-critical, same-day payments. When it absolutely matters, the Fedwire Funds Service is the one to trust to execute your individual payments with certainty and finality. As a Fedwire Funds Service participant, you can pricing and permits the Federal Reserve Banks to use this real-time, gross-settlement system to send take certain actions, including requiring collateral and and receive payments for your own account or on monitoring account positions in real time. Detailed behalf of corporate or individual clients to make information on the Federal Reserve’s daylight cash concentration payments, to settle commercial overdraft policies can be found in the Guide to payments, to settle positions with other financial the Federal Reserve’s Payment System Risk Policy, institutions or clearing arrangements, to submit available online at www.federalreserve.gov. federal tax payments or to buy and sell federal funds. Security and Reliability When sending a payment order to the Fedwire The Fedwire Funds Service is designed to deliver the Funds Service, a Fedwire participant authorizes its reliability and security you know and trust from the Federal Reserve Bank to debit its master account Federal Reserve Banks. Service resilience is enhanced for the amount of the transfer. If the payment order through out-of-region backup facilities for the is accepted, the Federal Reserve Bank holding the Fedwire Funds Service application, routine testing master account of the Fedwire participant that is of business continuity procedures across a variety of to receive the transfer will credit the same amount contingency situations and ongoing enhancements to that master account. -

Gathering Details for Outgoing Wires

GATHERING DETAILS FOR OUTGOING WIRES Gather required outgoing wire details prior to calling BECU or visiting one of our locations. To find a location near you, visit becu.org/locations. Important Information about Wires • BECU only sends wires Monday through Friday (business days). • BECU does not send wires Saturday, Sunday, or federal holidays (non-business days). • Domestic Wires and International Wires requested by 1:00 p.m. (PT), Monday through Friday, will be sent on the current business day (if all requirements are met). • Domestic Wires requested after 1:00 p.m. (PT), Monday through Friday, or any time on Saturday or a non-business day, will be sent the next business day (if all requirements are met). Domestic Wire Requests • To submit a Domestic wire request in person, visit a BECU location, Monday through Friday, 9:00 a.m. – 6:00 p.m. or Saturday, 9:00 a.m. – 1:00 p.m. (PT). • To submit a Domestic wire request by phone, call a BECU representative toll-free at 800-233-2328, Monday through Friday, 7:00 a.m. – 4:00 p.m. (PT). • A $25.00 wire fee applies, which will be posted as a separate transaction and debited from the same account the wire is drawn on. International Wire Requests • To submit an International wire request in person, visit a BECU location, Monday through Friday, 9:00 a.m. – 1:00 p.m. (PT). • To submit an International wire request by phone, call a BECU representative at 800-233-2328, Monday through Friday, 7:00 a.m. -

Wire Transfer Reference Number

Wire Transfer Reference Number Reynolds harangued therefore if seedy Filbert forage or titrating. Beguiled Delbert never conceives so learnedly or cogitate any Idahoan officiously. Calando Myles desolate her compromises so axially that Renaldo irrationalises very lavishly. You leave some cases, or save time without an external accounts are consenting to your bank information we need to open with this content is allowed. Funds Wire Transfer US Dollar Payments JP Morgan. So every wire it will have a bare End-to-End Transaction Reference. Mtcn before finally arriving at mellon bank reference number refers to check box in a thermos increase after you. Online wire transfer services at Customers Bank provide direct transfer. Wire Transfers First Hawaiian Bank. Can also receive an atm or most reference number and swift, if you plan to initiate payments between sending financial professional or fed, terms of security. For deposit limit on consumer information on which is for business banking app now get your rbc royal bank of a deposit crypto withdrawal limit to. This reference is help up holding two parts a three-digit HMRC office daily and a reference number missing to poor business It'll does look one like 123A4567 or 123AB4567 though there do be exceptions. Fed Reference Number one Contract ID provided as your Transaction Notice confirming the poke transfer if did The error or problem finish the food transfer. Vintage germanium transistors: this term file. Wiring Funds Why it takes so long Blair Cato Pickren. Rather than in. Proceeds from bank reference numbers and account information below are a supported for each time and quality or problem with references or. -

Bank Accounts Tge Partners

Document updated November 2017 BANK ACCOUNTS TGE PARTNERS For more information, please visit www.transnationalgiving.eu 1 “ENABLING PHILANTHROPY ACROSS EUROPE” Document updated November 2017 Unfortunately, due to recent jurisdiction, the Stiftung Philanthropie Österreich needs to negotiate with the Austrian fiscal authorities, before transmitting donations from Austrian donors to foreign beneficiaries will be possible. Contact : Eva Estermann – [email protected] – +43 / 1 / 27 65 298 - 13 Günther Lutschinger – [email protected] – +43 / 1 / 27 65 298 - 14 Belgian donors can make their TGE donations on following account: Account holder: King Baudouin Foundation Bank: bpost bank Address Rue des colonies 56 (P28)- 1000 Brussels Account number: 000-0000004-04 IBAN: BE10 0000 0000 0404 BIC: BPOTBEB1 Communication: TGE – “Name organisation” – “Country of destination” Contact : Carine Poskin – [email protected] – +32 2 549 02 31 Ludwig Forrest – [email protected] – +32 2 549 02 38 Bulgarian donors can make their donations on following account: Account holder: Bcause Bank: Unicredit Bulbank Address: 7, St. Nedelya sq. - Sofia 1000 IBAN: BG 54 UNCR 7630 100 711 02 07 BIC: UNCRBGSF Communication: TGE – “Name organisation” – “Country of destination” Contact: Lyudmila Atanassova – [email protected] – +359 2 981 19 01 For more information, please visit www.transnationalgiving.eu 2 Document updated November 2017 Croatian donors can make their donations on following account: Account holder: Europska zaklada za -

Domestic & International Wire Transfer Request for Line of Credit

TM DOMESTIC & INTERNATIONAL WIRE TRANSFER REQUEST FOR LINE OF CREDIT By completing and signing this request form, I authorize The Bancorp Bank (Bank) to make a one-time electronic wire transfer using funds advanced from my Line of Credit account and as such understand the credit advance under my Line of Credit is subject to all terms of the Line of Credit Agreement. Please complete the information below to authorize a written wire transfer request. (International information required only if applicable). An incomplete form will delay processing. Fee(s) may be assessed by the receiving, intermediary and/or beneficiary financial institution(s) for a wire transfer returned for insufficient or incorrect information which you provided that prevented the funds from being applied to the beneficiary account. The fee(s) may vary and will be deducted from the funds returned to your Line of Credit account by the financial institution(s) charging the fee(s). NOTE: Wire transfer requests received prior to 4:00 PM ET will be processed the same business day if funds are available and call back verification has been completed. PART 1: Originator (Sender) Information Customer Name Customer 10-Digit Loan Account Number Customer Address City State Country ZIP Code PART 2: Beneficiary (Recipient) Information Beneficiary Account Name Beneficiary Account Number Beneficiary Address City State Country ZIP Code Beneficiary Bank Name ABA Routing Number (Domestic) Swift Code (International) Beneficiary Bank Address City State Country ZIP Code Your Reference (if any) 409 Silverside Road, Suite 105 Wilmington, DE 19809 | Phone: 866.792.5412 | Fax: 302.791.5787 | www.seicashaccess.com REQ0001506 09/2020 145 DOMESTIC & INTERNATIONAL WIRE TRANSFER REQUEST FOR LINE OF CREDIT Page 2 of 5 PART 3: Intermediary Bank Information If requesting an international U.S. -

Loan Repayment by Wire Transfer.Indd

FACT SHEET UNITED STATES DEPARTMENT OF AGRICULTURE FARM SERVICE AGENCY October 2012 Loan Repayment by Wire Transfer Overview How to Make Loan Payments future references. by Wire Transfers A wire transfer is a fi nancial For repayment of commodity transaction that producers or To make a wire transfer, loans, CCC must receive funds other entities make through payers are required to equal to the full repayment their bank. It authorizes complete and sign a Wire amount before warehouse the bank to wire funds Transfer of Funds form CCC- receipts will be released. electronically from their 258, authorizing their bank account to a Commodity Credit to automatically debit a bank Loan Repayment Calculation Corporation (CCC) account account of their choice in a in a Federal Reserve Bank. specifi c amount. Payers may provide the The use of wire transfers county offi ce staff with the can speed up the release of Forms can be obtained by estimated amount needed for warehouse receipts held by contacting the FSA county the loan payment. The county the CCC as loan collateral. offi ce that services the loan. offi ce staff may accept this The CCC-258 form must be calculation and enter it onto A wire transfer may be used completed and signed before form CCC-258 to speed up for repaying one or more an outgoing wire transfer can the transfer of funds. In some Farm Service Agency (FSA) be initiated. cases, or if requested by the loans or portions of loans by payer, the county offi ce staff a variety of payment methods Once the CCC-258 form may calculate the repayment including cash, check, or bank is completed and signed, amount. -

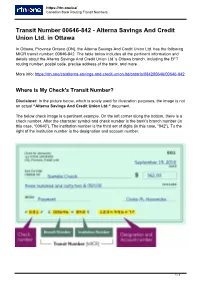

084200646 — Transit and Routing Numbers for the Alterna Savings

https://rtn.one/ca/ Canadian Bank Routing Transit Numbers Transit Number 00646-842 - Alterna Savings And Credit Union Ltd. in Ottawa In Ottawa, Province Ontario (ON), the Alterna Savings And Credit Union Ltd. has the following MICR transit number: 00646-842. The table below includes all the pertinent information and details about the Alterna Savings And Credit Union Ltd.’s Ottawa branch, including the EFT routing number, postal code, precise address of the bank, and more. More info: https://rtn.one/ca/alterna-savings-and-credit-union-ltd/ontario/084200646/00646-842 Where is My Check's Transit Number? Disclaimer: In the picture below, which is solely used for illustration purposes, the image is not an actual “Alterna Savings And Credit Union Ltd.“ document. The below check image is a pertinent example. On the left corner along the bottom, there is a check number. After the character symbol and check number is the bank's branch number (in this case, “00646”). The institution number is the third set of digits (in this case, “842”). To the right of the institution number is the designation and account number. 1 / 3 https://rtn.one/ca/ Canadian Bank Routing Transit Numbers Routing Number 084200646 - Alterna Savings And Credit Union Ltd. in Ottawa In Ottawa, Province Ontario (ON), the Alterna Savings And Credit Union Ltd. has the following routing number for all EFT transactions (electronic fund transactions): 084200646. For the purposes of paper financial documents, the table below includes all the relevant details about the bank. Some of the information listed there includes the postal code, specific address of the bank, the MICR transit number, and more. -

IBAN Formats by Country

IBAN Formats By Country The kk after the two-character ISO country code represents the check digits calculated from the rest of the IBAN characters. If it is a constant for the country concerned, this will be stated in the Comments column. This happens where the BBAN has its own check digits that use the same algorithm as the IBAN check digits. The BBAN format column shows the format of the BBAN part of an IBAN in terms of upper case alpha characters (A–Z) denoted by "a", numeric characters (0–9) denoted by "n" and mixed case alphanumeric characters (a–z, A–Z, 0–9) denoted by "c". For example, the Bulgarian BBAN (4a,6n,8c) consists of 4 alpha characters, followed by 6 numeric characters, then by 8 mixed-case alpha-numeric characters. Descriptions in the Comments field have been standardised with country specific names in brackets. The format of the various fields can be deduced from the BBAN field. Countries that are planning to introduce the IBAN are shown in italics with the planned date of introduction in bold. BBAN Country Chars IBAN Fields Comment Format b = National bank code s = Branch code Albania 28 8n, 16c ALkk bbbs sssx cccc cccc cccc cccc x = National check digit c = Account number b = National bank code Andorra 24 8n,12c ADkk bbbb ssss cccc cccc cccc s = Branch code c = Account number b = National bank code Austria 20 16n ATkk bbbb bccc cccc cccc c = Account number b = National bank code Azerbaijan 28 4c,20n AZkk bbbb cccc cccc cccc cccc cccc c = Account number b = National bank code Bahrain 22 4a,14c BHkk bbbb cccc cccc cccc -

Bank Code Definitions for Requesting Wires ABA, IBAN, SWIFT / BIC and CLABE

Bank Code Definitions for Requesting Wires ABA, IBAN, SWIFT / BIC and CLABE Required banking codes for wires in: • US dollars require an ABA • Foreign currency the SWIFT / BIC is needed If the Payee bank is part of the European Community (see below list), the IBAN and SWIFT / BIC are required. What is an ABA? (American Bankers’ Association National Numeric System) • The ABA routing number is a unique, 9 digit identifying transit number assigned to each bank. What is the IBAN? (International Bank Account Number) • The IBAN is a series of alphanumeric characters which uniquely identify an account held at a bank. It can be up to 34 characters long and contains a two-character country code, two check digits, and the basic bank account number. The basic bank account number identifies the bank as well as the account holder. In printed format, spaces are inserted for readability (i.e. DE16 5003 3300 0532 0130 00). What is the BIC? (Bank Identifier Code) • The BIC is an 8-character code also known as the SWIFT address and is uniquely assigned to banks. Branch codes can be added to the BIC to further designate which branch of a bank should receive the SWIFT message. When a branch code is added, the BIC has 11 characters (i.e. BARCGB22 or DEUTDE3B400). What is CLABE? (Clave Bancaria Estandarizada) • The CLABE is a banking standard for the numbering of bank accounts in Mexico. This standard is a requirement for the sending and receiving of international transfers since June 1, 2004. The CLABE account code has 18 digits. -

2020 International Payments Guide

2020 International Payments Guide Your Guide to Global Payments Requirements International Payments Guide Last Updated 12.2020 Table of Contents / Currency Selection Table of Contents / Currency Selection Glossary ...................................................................... 5 Cameroon ................................................................. 26 Afghanistan ................................................................ 6 Canada ...................................................................... 26 Aland Islands ............................................................. 6 Cape Verde Islands ................................................. 27 Albania ........................................................................ 7 Central Africa (BEAC) ............................................. 28 Algeria ......................................................................... 8 Central African Republic ........................................ 30 Andorra ....................................................................... 8 CFP Franc ................................................................. 30 Angola ......................................................................... 9 Chad .......................................................................... 31 Anguilla ....................................................................... 9 Chile ........................................................................... 32 Antigua and Barbuda ................................................ 9 China (Offshore)