Special-Purpose Financial Statement Leon County District School Board's

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Course Catalog 2017-2018 the American Workforce Needs Have Changed Drastically Over the Course of His- Tory in Our Country

Course Catalog 2017-2018 The American workforce needs have changed drastically over the course of his- tory in our country. This creates a constant need for highly trained individuals in numerous areas that must be met. Lively Technical Center strives constantly to provide the training to meet these needs. It is our hope that we provide the training, skills and knowledge that will make you successful in the workplace. Lively Technical Center welcomes you. Lively Technical Center, in partnership with the extended community, empowers students for success in a career focused education. We hope this mission pro- vides you with the training necessary to be a success in your chosen field. Accredited by: The Accrediting Commission of the Council on Occupational Education 7840 Roswell Road, Building 300, Suite 325, Atlanta, Georgia 30350 770.396.3898. AdvancED Florida (SACSCASI) University of West Florida, 11000 University Parkway, Pensacola, FL 32514 800.865.9068 Lively is approved for training by the following State Approved Agencies: The Florida Department of Veterans Affairs, The Florida Board of Cosmetology, The Florida State Board of Nursing, The Federal Aviation Administration, The Florida Real Estate Commission, The Florida Department of Insurance, The Florida of Business and Professional Regulation, The American Heart Association, The Florida Department of Transportation, The Department of Highway Safety and Motor Vehicles, The Florida Rider Training Program, The Motorcycle Safety Foundation, The HVAC Excellence for Heating & Air, ASE Certified, NATEF and The Lively Technical Center Medical Assisting Program is accredited by the Commission on Accreditation of Allied Health Education Programs (CAAHEP), on recommendation of the Curriculum Review Board of the American Association of Medical Assistants’ Endowment (AAMAE). -

Searching for a Job in Tallahassee

Searching for a Job in Tallahassee Objectives 1. Become familiar with online and print job search resources specific to Tallahassee and Leon County. 2. Identify local employers and job opportunities. Getting Started Utilize the local phone book. One of the most reliable resources for finding a job in Tallahassee is the Blue Pages of the current telephone book. These listings include government agency offices, telephone numbers, and often, job lines. Yellow Pages online at www.yp.com can also be used. Use this information as a base, but do not stop there. Expect to do some research. You can use resources such as those available in The Career Center Library, or review the resources listed in this guide. Not all of the information you need is probably in print or online so you might want to expand your research to include people resources! Networking is another great way to learn about job opportunities in the area. If you have not created a What’s Inside LinkedIn profile, review the “Building Your LinkedIn Tallahassee & Leon County Resources..................2 Presence” guide at www.career.fsu.edu/Resources/ State of Florida Resources.......................................3 Career-Guides to learn about networking. Federal Government Resources.............................3 Take advantage of information from experts. Public Non-Profit Organizations.......................................3 employees, such as those in workforce assistance Private Sector............................................................4 centers, have a lot of knowledge to share. Have Additional Resources..............................................4 conversations with these people and others you encounter in your search. They can often provide useful information if you listen and persist in your networking efforts. Tallahassee Profile Use the Internet. -

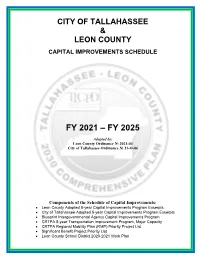

Capital Improvements Schedule

CITY OF TALLAHASSEE & LEON COUNTY CAPITAL IMPROVEMENTS SCHEDULE FY 2021 – FY 2025 Adopted by: Leon County Ordinance № 2021-04 City of Tallahassee Ordinance № 21-O-06 Components of the Schedule of Capital Improvements: • Leon County Adopted 5-year Capital Improvements Program Excerpts • City of Tallahassee Adopted 5-year Capital Improvements Program Excerpts • Blueprint Intergovernmental Agency Capital Improvements Program • CRTPA 5-year Transportation Improvement Program, Major Capacity • CRTPA Regional Mobility Plan (RMP) Priority Project List • Significant Benefit Project Priority List • Leon County School District 2020-2021 Work Plan Leon County 5-year Capital Improvements Program Excerpts Leon County Board of County Commissioners CIE Schedule of Projects Plan Amendment FY 2021 - FY 2025 Funding Source: Proportionate Share/Grant Accounts FY 2020 Adjusted Fund Description FY 2021 FY 2022 FY 2023 FY 2024 FY 2025 Project Total Budget Comprehensive Plan Capital Improvements: Transportation (Mobility) Element 125 Magnolia Drive Multi-Use Trail 5,216,800 - - - - - 5,216,800 125 Smith Creek Bike Lanes Phase I 1,108,000 - - - - - 1,108,000 125 Smith Creek Bike Lanes Phase II 977,901 - - - - - 977,901 NONE - - - - - - - Comprehensive Plan Capital Improvements: Stormwater Element NONE Comprehensive Plan Capital Improvements: Parks and Recreation Element 125 St. Marks Headwaters Greenway 5,351,126 - - - - - 5,351,126 Comprehensive Plan Capital Improvements: Utilities Element 125 Belair-Annawood Sewer Project 1,166,488 - - - - - 1,166,488 125 -

The Tallahassee-Leon County 2020 Census Initiative

Page 1 Table of Contents Executive Summary .................................................................................................................................... 2 Communication Plan Objectives ............................................................................................................... 4 Census Timeline ........................................................................................................................................ 10 Make It Count: Multimedia Public Information Campaign ................................................................. 12 Background on Previous Census Participation ....................................................................................... 12 Target Markets ....................................................................................................................................... 13 Communication Challenges .................................................................................................................... 15 Leon County and City of Tallahassee Strategies .................................................................................... 16 Measuring Success .................................................................................................................................... 22 Marketing and Promotional Materials ................................................................................................... 24 Page 2 Executive Summary Every 10 years an enormous effort is conducted: counting every living person -

LCSO 2020 Annual Report

2020 Annual Report Leon County Sheriff’s Office TABLE OF CONTENTS Message from the Sheriff ...................................... 3 Mission, Vision and Values .................................. 5 Area: 702 square miles Crime Trends ......................................................... 6 Population: 293,582 (2019) Strategic Plan .......................................................... 7 LCSO in Action ..................................................... 9 Average Household Income: $50,682 World Class Service ............................................... 10 Executive Staff ........................................................ 11 Organizational Chart ............................................ 13 Administration ...................................................... 15 Community & Media Relations ........................... 17 Detention Facility .................................................. 19 Fiscal ....................................................................... 21 Fleet ......................................................................... 23 Investigations ......................................................... 25 Judicial Services ..................................................... 27 Patrol Support ........................................................ 29 Professional Standards .......................................... 35 Records ................................................................... 37 Leon County Sheriff’s Office: Uniform Patrol ...................................................... -

November 21, 2011

FSU MOBILE Popular app now includes Blackboard Mobile Learn, 4 MEDICINE Graduate medical education gets reaccredited, 5 UNIVERSITY LIBRARIES Digital research repository to StateThe Florida State University Faculty-Staff Bulletin promote open access, 6 Volume 46 • Number 7 November 21 - December 11, 2011 Creating the nation’s most Coburn receives national award veteran-friendly By Jeffery Seay EDITOR IN CHIEF campus Mary B. Coburn, vice presi- dent for Student Affairs, was By Jill Elish INTERIM DIRECTOR, NEWS AND RESEARCH COMMUNICATIONS named a Pillar of the Profes- sion by the NASPA Founda- Florida State University is well on raising awareness about their educational tion, the fundraising arm of its way to becoming the most veteran- needs and service to our country among NASPA-Student Affairs Ad- friendly public university in the nation. the student body in general. ” ministra- Working with the Collegiate Veterans Veterans House tors in Association, President Eric J. Barron The Pearl Tyner Welcome Center at H i g h e r has established a Florida State Veter- the Alumni Association complex has E d u c a - ans House, hired a director of a newly been temporarily pressed into service as tion. The created Florida State Veterans Center, the Florida State Veterans House until distinction and launched a Student Veteran Film a permanent facility can be built. honors in- Festival. A ceremonial ribbon was cut on Nov. d iv i d u a l s The three initiatives are designed to 12 to mark the beginning of the wel- who pro- provide support and services to assist come center’s latest use. -

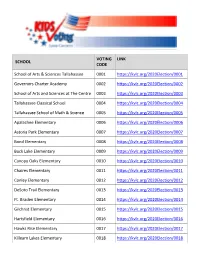

School Codes Available Here

VOTING LINK SCHOOL CODE School of Arts & Sciences Tallahassee 0001 https://kvlc.org/2020Election/0001 Governors Charter Academy 0002 https://kvlc.org/2020Election/0002 School of Arts and Sciences at The Centre 0003 https://kvlc.org/2020Election/0003 Tallahassee Classical School 0004 https://kvlc.org/2020Election/0004 Tallahassee School of Math & Science 0005 https://kvlc.org/2020Election/0005 Apalachee Elementary 0006 https://kvlc.org/2020Election/0006 Astoria Park Elementary 0007 https://kvlc.org/2020Election/0007 Bond Elementary 0008 https://kvlc.org/2020Election/0008 Buck Lake Elementary 0009 https://kvlc.org/2020Election/0009 Canopy Oaks Elementary 0010 https://kvlc.org/2020Election/0010 Chaires Elementary 0011 https://kvlc.org/2020Election/0011 Conley Elementary 0012 https://kvlc.org/2020Election/0012 DeSoto Trail Elementary 0013 https://kvlc.org/2020Election/0013 Ft. Braden Elementary 0014 https://kvlc.org/2020Election/0014 Gilchrist Elementary 0015 https://kvlc.org/2020Election/0015 Hartsfield Elementary 0016 https://kvlc.org/2020Election/0016 Hawks Rise Elementary 0017 https://kvlc.org/2020Election/0017 Killearn Lakes Elementary 0018 https://kvlc.org/2020Election/0018 VOTING LINK SCHOOL CODE Oak Ridge Elementary 0019 https://kvlc.org/2020Election/0019 Pineview Elementary 0020 https://kvlc.org/2020Election/0020 Riley Elementary 0021 https://kvlc.org/2020Election/0021 Roberts Elementary 0022 https://kvlc.org/2020Election/0022 Ruediger Elementary 0023 https://kvlc.org/2020Election/0023 Sabal Palm Elementary 0024 https://kvlc.org/2020Election/0024 -

FSU's Bernard James Doesn't Regret Road Traveled to College Basketball

Tallahassee CommuniTy College In the News February 16, 2010 - March 25 , 2011 February 16, 2010 - March 25, 2011 Tallahassee CommuniTy College In the News Print Media • Enhanced Online News 1 • The Times 1 • Florida Capital News 1 • WCTV . 4 • FSVIEW . 1 • WTXL . 3 • Inside Hire ED . 1 • Tallahassee Democrat 16 • The FAMUAN 2 Electronic Media • February 22 WCTV FPSI hosts Black History Month breakfast • March 4 WCTV Meet TCC President Jim Murdaugh • March 9 WCTV TCC Eagles head to NJCAA Basketball Tournament • March 9 WCTV/WTXL Emerald Warriors train, teach at FPSI The Times of Apalachicola & Carrabelle - February 16, 2011 3 Top teachers to be honored tonight David Adlerstein Barbara Lee During the last 15 years, she’s taught middle and high school English, and served as media specialist, as well For high school English literature teacher Barbara Lee, as been active with extracurriculars, from coaching the art of instruction is the art of enabling students to cheerleading, volleyball and track to serving as class challenge their assumptions and to think things through sponsor for themselves She and husband John have two daughters, Kayla, who “Don’t follow the crowd just because they’re doing it,” she served in the U S Air Force and is now studying physical advises “Remember you’re free to speak in this class what therapy in Montgomery, Ala, , and Bryanne Rajamannar, you think and feel ” who is married and living in Jacksonville with a 3-month- As teacher of 11th grade American literature, and an old daughter Sienna Advanced Placement (AP) -

2020-2021 Course Catalog

Lively Technical College Course Catalog 2020-2021 SPRING 500 North Appleyard Drive | Tallahassee, FL 32304 | 850.487.7555 www.livelytech.com Table of Contents Mission Statement 3 Vision 3 Accreditation Information 3 General School Information 4 Nondiscrimination Information 5 Campus Map 6 Enrollment Information 7 Clock Hour 8 Academic Year 8 Cost of Attendance 8 Tuition & Fees 8 Fee Exemption Request 8 Late Registration 9 Student Accident Insurance 9 Student ID/Parking Permit 9 Transfer Policy 9 Transcripts 9 Refund Policy/Withdrawal from Program 9-10 Enrollment Requirements 10-11 Secondary Students (Dual Enrolled) 11 Testing Requirements 11 Basic Skills Exemptions 11-14 Registration 14 Student Services 14 Graduation 15 Financial Aid 15 Other Types of Financial Aid 15-16 Testing Center 16 Academic Enrichment Guide 16-17 Learning Resource Services 17 Placement & Follow-Up Services 17 Veterans Affairs 17 CareerSource Florida 17 Occupational Advisory Committees (OAC) 17 School Advisory Council (SAC) 18 Post-Secondary Career Certificate Programs 18 Program Offerings by Career Cluster 18 Traditional Student Calendar 19 Program Schedule 20-22 Applied Academics for Adult Education (AAAE) 23 1 Table of Contents (Continued) Automotive Maintenance & Light Repair Technician 24-25 Automotive Service Technology 1 26-27 Automotive Service Technology 2 28-29 Aviation Airframe Mechanic 30-31 Aviation Powerplant Mechanic 32-33 Baking & Pastry Arts 34-35 Barbering 36-38 Building Trades & Construction Design Technology 39-40 Commercial Photography Technology -

Course Catalog 2019-2020

Course Catalog 2019-2020 500 North Appleyard Drive | Tallahassee, FL 32304 850.487.7555 | www.Livelytech.com Table of Contents Mission Statement 3 Vision 3 Accreditation Information 3 General School Information 4 Nondiscrimination Information 5 Campus Map 6 Enrollment Information 7 Clock Hour 8 Academic Year 8 Cost of Attendance 8 Tuition & Fees 8 Fee Exemption Request 8 Late Registration 9 Student Accident Insurance 9 Student ID/Parking Permit 9 Transfer Policy 9 Transcripts 9 Refund Policy/Withdrawal from Program 9-10 Enrollment Requirements 10-11 Secondary Students (Dual Enrolled) 11 Testing Requirements 11 TABE/Wonderlic Exemptions 11 Registration 11 Student Services 11 Graduation 12 Financial Aid 12 Other Types of Financial Aid 12 Testing Center 13 Academic Enrichment Guide 13-14 Learning Resource Services 14 Placement & Follow-Up Services 14 Veterans Affairs 14 CareerSource Florida 14 Occupational Advisory Committees (OAC) 14 School Advisory Council (SAC) 14 Post-Secondary Career Certificate Programs 15 Program Offerings by Career Cluster 15 Traditional Student Calendar 16 Program Schedule 17-19 Applied Academics for Adult Education (AAAE) 20 1 Table of Contents (Continued) Administrative Office Specialist 21-22 Automotive Drivetrain Technician 23-24 Automotive Electrical Technician 25-26 Automotive General Service Technician 27-28 Automotive Maintenance & Light Repair Technician 29-30 Automotive Performance Technician 31-32 Automotive Service Technology 1 33-34 Automotive Service Technology 2 35-36 Aviation Airframe Mechanics 37-38 -

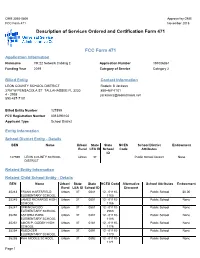

Description of Services Ordered and Certification Form 471 FCC Form

OMB 3060-0806 Approval by OMB FCC Form 471 November 2015 Description of Services Ordered and Certification Form 471 FCC Form 471 Application Information Nickname YR 22 Network Cabling 2 Application Number 191006861 Funding Year 2019 Category of Service Category 2 Billed Entity Contact Information LEON COUNTY SCHOOL DISTRICT Roderic B Jackson 2757 W PENSACOLA ST TALLAHASSEE FL 3230 850-487-7101 4 - 2998 [email protected] 850-487-7101 Billed Entity Number 127599 FCC Registration Number 0012290102 Applicant Type School District Entity Information School District Entity - Details BEN Name Urban/ State State NCES School District Endowment Rural LEA ID School Code Attributes ID 127599 LEON COUNTY SCHOOL Urban 37 Public School District None DISTRICT Related Entity Information Related Child School Entity - Details BEN Name Urban/ State State NCES Code Alternative School Attributes Endowment Rural LEA ID School ID Discount 35243 FRANK HARTSFIELD Urban 37 0041 12 - 01110- Public School $0.00 ELEMENTARY SCHOOL 1165 35245 JAMES RICKARDS HIGH Urban 37 0051 12 - 01110- Public School None SCHOOL 1166 35247 SPRINGWOOD Urban 37 0501 12 - 01110- Public School None ELEMENTARY SCHOOL 2568 35250 ASTORIA PARK Urban 37 0401 12 - 01110- Public School None ELEMENTARY SCHOOL 1188 35251 AMOS P. GODBY HIGH Urban 37 0161 12 - 01110- Public School None SCHOOL 1176 35254 RUEDIGER Urban 37 0091 12 - 01110- Public School None ELEMENTARY SCHOOL 1170 35255 RAA MIDDLE SCHOOL Urban 37 0092 12 - 01110- Public School None 1171 Page 1 BEN Name Urban/ State State NCES Code Alternative School Attributes Endowment Rural LEA ID School ID Discount 35256 SAIL HIGH SCHOOL Urban 37 0204 12 - 01110- Public School None 1178 35257 JOHN G. -

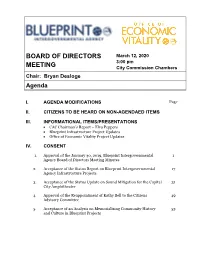

Board of Directors Meeting Minutes

BOARD OF DIRECTORS March 12, 2020 3:00 pm MEETING City Commission Chambers Chair: Bryan Desloge Agenda I. AGENDA MODIFICATIONS Page II. CITIZENS TO BE HEARD ON NON-AGENDAED ITEMS III. INFORMATIONAL ITEMS/PRESENTATIONS • CAC Chairman’s Report – Elva Peppers • Blueprint Infrastructure Project Updates • Office of Economic Vitality Project Updates IV. CONSENT 1. Approval of the January 30, 2019, Blueprint Intergovernmental 1 Agency Board of Directors Meeting Minutes 2. Acceptance of the Status Report on Blueprint Intergovernmental 17 Agency Infrastructure Projects 3. Acceptance of the Status Update on Sound Mitigation for the Capital 31 City Amphitheater 4. Approval of the Reappointment of Kathy Bell to the Citizens 49 Advisory Committee 5. Acceptance of an Analysis on Memorializing Community History 53 and Culture in Blueprint Projects Blueprint Intergovernmental Agency Board of Directors - Meeting Agenda Date: March 12, 2020 Page 2 of 2 V. GENERAL BUSINESS/PRESENTATIONS 6. Acceptance of the Status Report on the Arena District Convention 97 Center Project and Consideration of Next Steps VI. CITIZENS TO BE HEARD Citizens desiring to speak must fill out a Speaker Request Form the Chair reserves the right to limit the number of speakers or time allotted to each VII. ADJOURN NEXT BOARD OF DIRECTORS MEETING: May 21, 2020, 3:00 PM In accordance with the Americans with Disabilities Act and Section 286.26, Florida Statutes, persons needing a special accommodation to attend this meeting should contact Susan Emmanuel, Public Information Officer, 315 South Calhoun Street, Suite 450, Tallahassee, Florida, 32301, at least 48 hours prior to the meeting. Telephone: 850-219- 1060; or 1-80 0-955-8770 (Voice) or 711 via Florida Relay Service.