Easier Hedge Accounting Rules Now Available

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hedge Funds Oversight, Report of the Technical Committee Of

Hedge Funds Oversight Consultation Report TECHNICAL COMMITTEE OF THE INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS MARCH 2009 This paper is for public consultation purposes only. It has not been approved for any other purpose by the IOSCO Technical Committee or any of its members. Foreword The IOSCO Technical Committee has published for public comment this consultation report on Hedge Funds Oversight. The Report makes preliminary recommendations of regulatory approaches that may be used to mitigate the regulatory risks posed by hedge funds. The Report will be finalised after consideration of comments received from the public. How to Submit Comments Comments may be submitted by one of the three following methods on or before 30 April 2009. To help us process and review your comments more efficiently, please use only one method. 1. E-mail • Send comments to Greg Tanzer, Secretary General, IOSCO at the following email address: [email protected] • The subject line of your message should indicate “Public Comment on the Hedge Funds Oversight: Consultation Report”. • Please do not submit any attachments as HTML, GIF, TIFF, PIF or EXE files. OR 2. Facsimile Transmission Send a fax for the attention of Greg Tanzer using the following fax number: + 34 (91) 555 93 68. OR 3. Post Send your comment letter to: Greg Tanzer Secretary General IOSCO 2 C / Oquendo 12 28006 Madrid Spain Your comment letter should indicate prominently that it is a “Public Comment on the Hedge Funds Oversight: Consultation Report” Important: All comments will be made available publicly, unless anonymity is specifically requested. Comments will be converted to PDF format and posted on the IOSCO website. -

2020.12.03 RSIC Meeting Materials

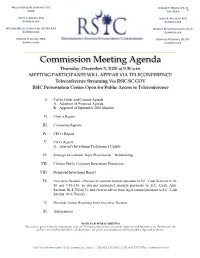

WILLIAM (BILL) H. HANCOCK, CPA RONALD P. WILDER, PH. D CHAIR VICE-CHAIR 1 PEGGY G. BOYKIN, CPA ALLEN R. GILLESPIE, CFA COMMISSIONER COMMISSIONER WILLIAM (BILL) J. CONDON, JR. JD, MA, CPA REBECCA M. GUNNLAUGSSON, PH. D COMMISSIONER COMMISSIONER EDWARD N. GIOBBE, MBA REYNOLDS WILLIAMS, JD, CFP COMMISSIONER COMMISSIONER _____________________________________________________________________________________ Commission Meeting Agenda Thursday, December 3, 2020 at 9:30 a.m. MEETING PARTICIPANTS WILL APPEAR VIA TELECONFERENCE Teleconference Streaming Via RSIC.SC.GOV RSIC Presentation Center Open for Public Access to Teleconference I. Call to Order and Consent Agenda A. Adoption of Proposed Agenda B. Approval of September 2020 Minutes II. Chair’s Report III. Committee Reports IV. CEO’s Report V. CIO’s Report A. Quarterly Investment Performance Update VI. Strategic Investment Topic Presentation – Rebalancing VII. Chinese Public Company Investment Discussion VIII. Delegated Investment Report IX. Executive Session – Discuss investment matters pursuant to S.C. Code Sections 9-16- 80 and 9-16-320; to discuss personnel matters pursuant to S.C. Code Ann. Section 30-4-70(a)(1); and receive advice from legal counsel pursuant to S.C. Code Section 30-4-70(a)(2). X. Potential Action Resulting from Executive Session XI. Adjournment NOTICE OF PUBLIC MEETING This notice is given to meet the requirements of the S.C. Freedom of Information Act and the Americans with Disabilities Act. Furthermore, this facility is accessible to individuals with disabilities, and special accommodations will be provided if requested in advance. 1201 MAIN STREET, SUITE 1510, COLUMBIA, SC 29201 // (P) 803.737.6885 // (F) 803.737.7070 // WWW.RSIC.SC.GOV 2 AMENDED DRAFT South Carolina Retirement System Investment Commission Meeting Minutes September 10, 2020 9:30 a.m. -

Hedge Accounting FBS 2013 USER CONFERENCE

9/12/2013 Hedge Accounting FBS 2013 USER CONFERENCE Purpose of a Hedge • Provide a change in value of the hedging instrument in the opposite direction of the hedged item. • For tax purposes, the gains or losses on from hedging activities are recognized when hedges are lifted • For accounting purposes, hedging gains/losses are recognized in the period the gains or losses occur – Hedging is consider normal business operation so should be matched to gross revenue and expense 1 9/12/2013 What is Hedging? • Hedging is a risk management strategy that attempts to offset price movements of owned assets, planned production of a commodity or good, or planned purchases of commodity or good against a derivative instrument (which generally derives its value from an underlying physical commodity). • It is not an attempt to make money in the futures and options markets, but rather an attempt to offset price changes in the cash market, thereby protecting the producers net income. What is Not Hedging? • Speculation – Taking a futures or options position in a commodity not owned or produced. – Taking the same position in the futures or options market as exists (or will exist) on the farm. • Forward contracts – Fixed price, delayed or deferred price contracts, basis contracts, installment sale contracts, etc. 2 9/12/2013 Tax Purposes • May be different from GAAP • An agricultural producer normally reports hedging gains or losses when the hedge is closed (similar to GAAP). • However, if the producer meets certain requirements, they can elect to report all hedging gains and losses on a mark- to-market basis (i.e. -

Hedge Fund Performance During the Internet Bubble Bachelor Thesis Finance

Hedge fund performance during the Internet bubble Bachelor thesis finance Colby Harmon 6325661 /10070168 Thesis supervisor: V. Malinova 1 Table of content 1. Introduction p. 3 2. Literature reviews of studies on mutual funds and hedge funds p. 5 2.1 Evolution of performance measures p. 5 2.2 Studies on performance of mutual and hedge funds p. 6 3. Deficiencies in peer group averages p. 9 3.1 Data bias when measuring the performance of hedge funds p. 9 3.2 Short history of hedge fund data p. 10 3.3 Choice of weight index p. 10 4. Hedge fund strategies p. 12 4.1 Equity hedge strategies p. 12 4.1.1 Market neutral strategy p. 12 4.2 Relative value strategies p. 12 4.2.1 Fixed income arbitrage p. 12 4.2.2 Convertible arbitrage p. 13 4.3 Event driven strategies p. 13 4.3.1 Distressed securities p. 13 4.3.2 Merger arbitrage p. 14 4.4 Opportunistic strategies p. 14 4.4.1 Global macro p. 14 4.5 Managed futures p. 14 4.5.1 Trend followers p. 15 4.6 Recent performance of different strategies p. 15 5. Data description p. 16 6. Methodology p. 18 6.1 Seven factor model description p. 18 6.2 Hypothesis p. 20 7. Results p. 21 7.1 Results period 1997-2000 p. 21 7.2 Results period 2000-2003 p. 22 8. Discussion of results p. 23 9. Conclusion p. 24 2 1. Introduction A day without Internet today would be cruel and unthinkable. -

Arbitrage Pricing Theory∗

ARBITRAGE PRICING THEORY∗ Gur Huberman Zhenyu Wang† August 15, 2005 Abstract Focusing on asset returns governed by a factor structure, the APT is a one-period model, in which preclusion of arbitrage over static portfolios of these assets leads to a linear relation between the expected return and its covariance with the factors. The APT, however, does not preclude arbitrage over dynamic portfolios. Consequently, applying the model to evaluate managed portfolios contradicts the no-arbitrage spirit of the model. An empirical test of the APT entails a procedure to identify features of the underlying factor structure rather than merely a collection of mean-variance efficient factor portfolios that satisfies the linear relation. Keywords: arbitrage; asset pricing model; factor model. ∗S. N. Durlauf and L. E. Blume, The New Palgrave Dictionary of Economics, forthcoming, Palgrave Macmillan, reproduced with permission of Palgrave Macmillan. This article is taken from the authors’ original manuscript and has not been reviewed or edited. The definitive published version of this extract may be found in the complete The New Palgrave Dictionary of Economics in print and online, forthcoming. †Huberman is at Columbia University. Wang is at the Federal Reserve Bank of New York and the McCombs School of Business in the University of Texas at Austin. The views stated here are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of New York or the Federal Reserve System. Introduction The Arbitrage Pricing Theory (APT) was developed primarily by Ross (1976a, 1976b). It is a one-period model in which every investor believes that the stochastic properties of returns of capital assets are consistent with a factor structure. -

Securitization & Hedge Funds

SECURITIZATION & HEDGE FUNDS: COLLATERALIZED FUND OBLIGATIONS SECURITIZATION & HEDGE FUNDS: CREATING A MORE EFFICIENT MARKET BY CLARK CHENG, CFA Intangis Funds AUGUST 6, 2002 INTANGIS PAGE 1 SECURITIZATION & HEDGE FUNDS: COLLATERALIZED FUND OBLIGATIONS TABLE OF CONTENTS INTRODUCTION........................................................................................................................................ 3 PROBLEM.................................................................................................................................................... 4 SOLUTION................................................................................................................................................... 5 SECURITIZATION..................................................................................................................................... 5 CASH-FLOW TRANSACTIONS............................................................................................................... 6 MARKET VALUE TRANSACTIONS.......................................................................................................8 ARBITRAGE................................................................................................................................................ 8 FINANCIAL ENGINEERING.................................................................................................................... 8 TRANSPARENCY...................................................................................................................................... -

Session 7 Derivatives and Hedging

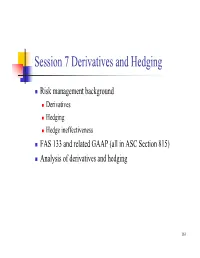

Session 7 Derivatives and Hedging Risk management background Derivatives Hedging Hedge ineffectiveness FAS 133 and related GAAP (all in ASC Section 815) Analysis of derivatives and hedging 163 Extant Proposals to Change Hedge Accounting In May 2010, the FASB issued Proposed Accounting Standards Update, Accounting for Financial Instruments and Revisions to the Accounting for Derivative Instruments and Hedging Activities (“the proposed ASU”) Simpler than but reasonably consistent with FAS 133 Somewhat easier to obtain hedge accounting Hedge accounting obscures volatility less After putting the project on the back burner, the FASB began redeliberating the proposed ASU in February 2015 Summary of deliberations through March 23, 2016 is available on FASB website FASB currently plans to issue an exposure draft in 2016Q3 164 Extant Proposals to Change Hedge Accounting (2) In November 2013, the IASB issued new, bank-friendlier hedge accounting rules in IFRS 9 (replacing rules in IAS 39) Provides more flexibility to define the hedged item than either IAS 39 or FAS 133: groups of positions (including derivatives), net positions (including net nil positions), risk layers (including last layers) Also provides more flexibility to define the hedge than IAS 39 or FAS 133: non-derivative/cash instruments classified at fair value through profit and loss Treats certain types of hedge ineffectiveness (e.g., option time value) as a cost of hedging to be amortized into income over time Hedge accounting allowed if economic hedging relationship exists consistent with firm’s risk management strategy; no quantitative threshold need be met The IASB has an ongoing project to allow “macro” hedging of open portfolios; issued discussion paper in April 2014 but does not appear to 165 have made much progress since then Derivatives Under FAS 133 (ASC 815), the payoffs on a derivative depend on the notional amount of one or more underlyings principal amount physical quantity one or more prices interest rates, exchange rates, commodity prices.. -

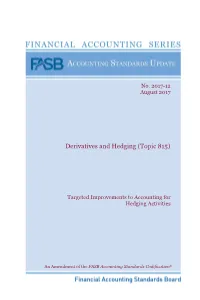

Derivatives and Hedging (Topic 815)

No. 2017-12 August 2017 Derivatives and Hedging (Topic 815) Targeted Improvements to Accounting for Hedging Activities An Amendment of the FASB Accounting Standards Codification® The FASB Accounting Standards Codification® is the source of authoritative generally accepted accounting principles (GAAP) recognized by the FASB to be applied by nongovernmental entities. An Accounting Standards Update is not authoritative; rather, it is a document that communicates how the Accounting Standards Codification is being amended. It also provides other information to help a user of GAAP understand how and why GAAP is changing and when the changes will be effective. For additional copies of this Accounting Standards Update and information on applicable prices and discount rates contact: Order Department Financial Accounting Standards Board 401 Merritt 7 PO Box 5116 Norwalk, CT 06856-5116 Please ask for our Product Code No. ASU2017-12. FINANCIAL ACCOUNTING SERIES (ISSN 0885-9051) is published monthly with the exception of May, July, and November by the Financial Accounting Foundation, 401 Merritt 7, PO Box 5116, Norwalk, CT 06856-5116. Periodicals postage paid at Norwalk, CT and at additional mailing offices. The full subscription rate is $255 per year. POSTMASTER: Send address changes to Financial Accounting Series, 401 Merritt 7, PO Box 5116, Norwalk, CT 06856-5116. | No. 456 Copyright © 2017 by Financial Accounting Foundation. All rights reserved. Content copyrighted by Financial Accounting Foundation may not be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the Financial Accounting Foundation. Financial Accounting Foundation claims no copyright in any portion hereof that constitutes a work of the United States Government. -

Hedge Accounting Under the New Market Conditions

Hedge Accounting under the new Market Conditions Market conditions and expectations play an important role in applying hedge accounting, and this unprecedented period of market disruption may significantly impact hedging programs. After several years of low volatility and strong economic growth, many companies suddenly face some big changes to their risk profiles and risks for which they were not prepared. Many existing hedging relationships were established during a time of minimal market volatility, when forecasting Changes to hedged transactions future transactions and exposures seemed straight forward. It is important to highlight that the way hedging relationships are documented at inception influences the A hedged transaction must be defined with sufficient detail accounting for the duration of the hedging relationship. so that it is identifiable. This requirement often results Most companies are likely to be impacted by the market in companies designating a specified amount of sales/ instabilities, either directly or indirectly, and the increased purchases over a period or interest payments on a specific economic uncertainty and risk may have significant financial debt instrument or portfolio. reporting implications. Due to the market instabilities, a company may need to In particular, the instabilities may affect a company’s risk revisit its portfolios by making changes to items originally exposures and how it manages them. Hence if a company designated as hedged items in hedge accounting applies hedge accounting as part of its management relationships. For example, airlines that would have strategy under IIAS 39, IFRS 9 or FRS 102 (“IFRS”), it must designated a highly probable forecast purchase of fuel carefully consider the effects of the market instabilities during the months of April/May may need to designate on the hedging relationships in place and whether the purchases of fuel in other months. -

Mitigating Tax Risks of Hedge Fund Investments in Loans

CLIENT MEMORANDUM MITIGATING TAX RISKS OF HEDGE FUND INVESTMENTS IN LOANS The tax risks for offshore hedge funds of investing in loans, whether directly or through derivatives, are attracting more attention. (See, for example, “Hedge Funds See Tax Issue,” Wall Street Journal, page C2, January 5, 2007.) We understand that these investments are also playing a larger role in funds’ arbitrage strategies in the credit-derivatives markets. Offshore hedge funds have been making these investments for years and generally take the position that the activity does not constitute a US trade or business and therefore does not result in US taxation. The funds rely on a special safe harbor rule that trading in stocks and securities by non-US persons, even if conducted in the United States, is generally not treated as constituting a US trade or business. By contrast, there is a substantial risk that regularly negotiating and originating loans in the US does constitute a US trade or business, and that the income and gain from such a business is subject to an effective federal tax rate of up to approximately 55% when earned by a non-US corporation (such as an offshore hedge fund). Engaging in a US trade or business also requires the filing of US tax returns. Because of this risk of US taxation, most offshore hedge funds investing in loans avoid regularly originating loans. They instead invest in loans either by purchasing the loans in a secondary market or investing in derivatives on the loans. Such funds also usually take steps to minimize the risk that the seller or counterparty in these transactions might be treated as their agent, which would potentially result in the loan-origination activity of the agent being attributed to the fund, causing the fund to be treated as engaged in a US trade or business. -

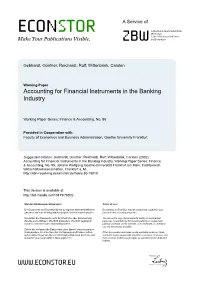

Accounting for Financial Instruments in the Banking Industry

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Gebhardt, Günther; Reichardt, Rolf; Wittenbrink, Carsten Working Paper Accounting for Financial Instruments in the Banking Industry Working Paper Series: Finance & Accounting, No. 95 Provided in Cooperation with: Faculty of Economics and Business Administration, Goethe University Frankfurt Suggested Citation: Gebhardt, Günther; Reichardt, Rolf; Wittenbrink, Carsten (2002) : Accounting for Financial Instruments in the Banking Industry, Working Paper Series: Finance & Accounting, No. 95, Johann Wolfgang Goethe-Universität Frankfurt am Main, Fachbereich Wirtschaftswissenschaften, Frankfurt a. M., http://nbn-resolving.de/urn:nbn:de:hebis:30-18018 This Version is available at: http://hdl.handle.net/10419/76902 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen -

Frs139-Guide.Pdf

The KPMG Guide: FRS 139, Financial Instruments: Recognition and Measurement i Contents Introduction 1 Executive summary 2 1. Scope of FRS 139 1.1 Financial instruments outside the scope of FRS 139 3 1.2 Definitions 3 2. Classifications and their accounting treatments 2.1 Designation on initial recognition and subsequently 5 2.2 Accounting treatments applicable to each class 5 2.3 Financial instruments at “fair value through profit or loss” 5 2.4 “Held to maturity” investments 6 2.5 “Loans and receivables” 7 2.6 “Available for sale” 8 3. Other recognition and measurement issues 3.1 Initial recognition 9 3.2 Fair value 9 3.3 Impairment of financial assets 10 4. Derecognition 4.1 Derecognition of financial assets 11 4.2 Transfer of a financial asset 11 4.3 Evaluation of risks and rewards 12 4.4 Derecognition of financial liabilities 13 5. Embedded derivatives 5.1 When to separate embedded derivatives from host contracts 14 5.2 Foreign currency embedded derivatives 15 5.3 Accounting for separable embedded derivatives 16 5.4 Accounting for more than one embedded derivative 16 6. Hedge accounting 17 7. Transitional provisions 19 8. Action to be taken in the first year of adoption 20 Appendices 1: Accounting treatment required for financial instruments under their required or chosen classification 21 2: Derecognition of a financial asset 24 3: Financial Reporting Standards and accounting pronouncements 25 1 The KPMG Guide: FRS 139, Financial Instruments: Recognition and Measurement Introduction This KPMG Guide introduces the requirements of the new FRS 139, Financial Instruments: Recognition and Measurement.