Securitization & Hedge Funds

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Documento Che Attesta La Proprietà Di Una Quota Del Cap- Itale Sociale È Il Titolo Azionario E Garantisce Una Serie Di Diritti Al Titolare

Università degli Studi di Padova Facoltà di Scienze Statistiche Corso di Laurea Specialistica in Scienze Statistiche, Economiche, Finanziarie e Aziendali Tesi di Laurea : PORTFOLIO MANAGEMENT : PERFORMANCE MEASUREMENT AND FEATURE-BASED CLUSTRERING IN ASSET ALLOCATION Laureando: Nono Simplice Aimé Relatore: Prof. Caporin Massimiliano Anno accademico 2009-2010 1 A Luise Geouego e a tutta la mia famiglia. 2 Abstract This thesis analyses the possible effects of feature-based clustering (using information extracted from asset time series) in asset allocation. In particu- lar, at first, it considers the creation of asset clusters using a matrix of input data which contains some performance measure. Some of these are choosen between the classical measures, while others between the most sofisticated ones. Secondly, it statistically compares the asset allocation results obtained from data-driven groups (obtained by clustering) and a-priori classifications based on assets industrial sector. It also controls how these results can change over time. Sommario Questa tesi si propone di esaminare l’eventuale effetto di una classificazione dei titoli nei portafogli basata su informazioni contenute nelle loro serie storiche In particolare, si tratta di produrre inizialmente una suddivisione dei titoli in gruppi attraverso una cluster analysis, avendo come matrice di input alcune misure di performance selezionate fra quelle classiche e quelle più sofisticate e in un secondo momento, di confrontare i risultati con quelli ottenuti operando una diversificazione dei titoli in macrosettori industriali; infine di analizzare come i risultati ottenuti variano nel tempo. Indice 1 Asset Allocation 7 1.1 Introduzione . 7 1.2 Introduzione alle azioni . 8 1.3 Criterio Rischio-Rendimento . -

Newsletter - November 2017

Newsletter - November 2017 In this month’s newsletter: New Stakeholders SBAI in Canada Factor-based investing working group launched Upcoming events New Stakeholders We are thrilled to welcome new additions to the SBAI family: Signatories ARP Americas LLC (USA) Highbridge Capital Management LLC (USA) Polar Asset Management Partners Inc (Canada) SBAI in Canada Over 50 Canadian institutional investors and managers gathered at the annual SBAI roundtable in Montreal. The speakers and panellists explored innovations in investor risk management and factor-based investing. The panel on factor investing and alternative/dynamic beta focussed on: Importance for investors to understand sources of return: Risk premia (investors are compensated for a systematic risk), i.e. asset class risk premia and factor risk premia, Alpha (information edge, behavioural edge, implementation edge), and Arbitrage Key considerations: Not all factors are risk premia, some are “firm characteristics” Data mined factors (with no greater probability of delivering future returns) Self-destruction of certain sources of return (investors arbitrage the exploitable pattern away) Implementation challenges: “Devil in the implementation” – small variations in implementation can result in wide range of outcomes Need for back-testing standards Whether factors can be timed (timing and selection of factors as a source of alpha) 1 In order to further explore this area, the SBAI has established a working group. The institutional risk management panel explored the following topics from the perspective from a corporate and a public pension plan: Approaches to organising the risk function, incl. group wide risk management with specialist risk teams within the alternative investment group. Approaches to building diverse risk teams, incl. -

Asset Securitization

L-Sec Comptroller of the Currency Administrator of National Banks Asset Securitization Comptroller’s Handbook November 1997 L Liquidity and Funds Management Asset Securitization Table of Contents Introduction 1 Background 1 Definition 2 A Brief History 2 Market Evolution 3 Benefits of Securitization 4 Securitization Process 6 Basic Structures of Asset-Backed Securities 6 Parties to the Transaction 7 Structuring the Transaction 12 Segregating the Assets 13 Creating Securitization Vehicles 15 Providing Credit Enhancement 19 Issuing Interests in the Asset Pool 23 The Mechanics of Cash Flow 25 Cash Flow Allocations 25 Risk Management 30 Impact of Securitization on Bank Issuers 30 Process Management 30 Risks and Controls 33 Reputation Risk 34 Strategic Risk 35 Credit Risk 37 Transaction Risk 43 Liquidity Risk 47 Compliance Risk 49 Other Issues 49 Risk-Based Capital 56 Comptroller’s Handbook i Asset Securitization Examination Objectives 61 Examination Procedures 62 Overview 62 Management Oversight 64 Risk Management 68 Management Information Systems 71 Accounting and Risk-Based Capital 73 Functions 77 Originations 77 Servicing 80 Other Roles 83 Overall Conclusions 86 References 89 ii Asset Securitization Introduction Background Asset securitization is helping to shape the future of traditional commercial banking. By using the securities markets to fund portions of the loan portfolio, banks can allocate capital more efficiently, access diverse and cost- effective funding sources, and better manage business risks. But securitization markets offer challenges as well as opportunity. Indeed, the successes of nonbank securitizers are forcing banks to adopt some of their practices. Competition from commercial paper underwriters and captive finance companies has taken a toll on banks’ market share and profitability in the prime credit and consumer loan businesses. -

Understanding Securitization

Understanding Securitization It is important to have a general familiarity with mortgage securitization in order to understand the foreclosure process. Securitization involves a series of conveyances of the note evidencing the residential loan and assignment of the mortgage or trust deed securing it. Therefore, chain of title and beneficial interest issues frequently turn on the securitization trajectories. Securitization is the process pooling loans into “mortgage‐ backed securities” or “MBS” for sale to investors. MBS is an investment instrument backed by an undivided interest in a pool of mortgages or trust deeds. Income from the underlying mortgages is used to pay interest and principal on the securities. Figure A below is a simplified schematic depicting the general securitization process and some of the parties involved. The process begins with Originators, which are the lenders (such as banks or finance companies) that initially make the loans to homeowners. Sponsor/Sellers (or “sponsors”) purchase these loans from one or more Originators to form the pool of assets to be securitized. (Most large financial institutions are both Originators and Sponsor/Sellers.) A Depositor creates a Securitization Trust, a special‐purpose entity, for the securitized transaction. The depositor acquires the pooled assets from the Sponsor/Seller and in turn deposits them into the Securitization Trust. An Issuer acquires the Securitization Trust and issues certificates to eventually be sold to investors. However, the Issuer does not directly offer the certificates for sale to the investors. Instead, the Issuer conveys the certificate to the Depositor in exchange for the pooled assets. An Underwriter, usually an investment bank, purchases all of the certificates from the Depositor with the responsibility of offering to them for sale to the ultimate investors. -

Hedge Funds Oversight, Report of the Technical Committee Of

Hedge Funds Oversight Consultation Report TECHNICAL COMMITTEE OF THE INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS MARCH 2009 This paper is for public consultation purposes only. It has not been approved for any other purpose by the IOSCO Technical Committee or any of its members. Foreword The IOSCO Technical Committee has published for public comment this consultation report on Hedge Funds Oversight. The Report makes preliminary recommendations of regulatory approaches that may be used to mitigate the regulatory risks posed by hedge funds. The Report will be finalised after consideration of comments received from the public. How to Submit Comments Comments may be submitted by one of the three following methods on or before 30 April 2009. To help us process and review your comments more efficiently, please use only one method. 1. E-mail • Send comments to Greg Tanzer, Secretary General, IOSCO at the following email address: [email protected] • The subject line of your message should indicate “Public Comment on the Hedge Funds Oversight: Consultation Report”. • Please do not submit any attachments as HTML, GIF, TIFF, PIF or EXE files. OR 2. Facsimile Transmission Send a fax for the attention of Greg Tanzer using the following fax number: + 34 (91) 555 93 68. OR 3. Post Send your comment letter to: Greg Tanzer Secretary General IOSCO 2 C / Oquendo 12 28006 Madrid Spain Your comment letter should indicate prominently that it is a “Public Comment on the Hedge Funds Oversight: Consultation Report” Important: All comments will be made available publicly, unless anonymity is specifically requested. Comments will be converted to PDF format and posted on the IOSCO website. -

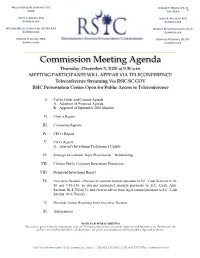

2020.12.03 RSIC Meeting Materials

WILLIAM (BILL) H. HANCOCK, CPA RONALD P. WILDER, PH. D CHAIR VICE-CHAIR 1 PEGGY G. BOYKIN, CPA ALLEN R. GILLESPIE, CFA COMMISSIONER COMMISSIONER WILLIAM (BILL) J. CONDON, JR. JD, MA, CPA REBECCA M. GUNNLAUGSSON, PH. D COMMISSIONER COMMISSIONER EDWARD N. GIOBBE, MBA REYNOLDS WILLIAMS, JD, CFP COMMISSIONER COMMISSIONER _____________________________________________________________________________________ Commission Meeting Agenda Thursday, December 3, 2020 at 9:30 a.m. MEETING PARTICIPANTS WILL APPEAR VIA TELECONFERENCE Teleconference Streaming Via RSIC.SC.GOV RSIC Presentation Center Open for Public Access to Teleconference I. Call to Order and Consent Agenda A. Adoption of Proposed Agenda B. Approval of September 2020 Minutes II. Chair’s Report III. Committee Reports IV. CEO’s Report V. CIO’s Report A. Quarterly Investment Performance Update VI. Strategic Investment Topic Presentation – Rebalancing VII. Chinese Public Company Investment Discussion VIII. Delegated Investment Report IX. Executive Session – Discuss investment matters pursuant to S.C. Code Sections 9-16- 80 and 9-16-320; to discuss personnel matters pursuant to S.C. Code Ann. Section 30-4-70(a)(1); and receive advice from legal counsel pursuant to S.C. Code Section 30-4-70(a)(2). X. Potential Action Resulting from Executive Session XI. Adjournment NOTICE OF PUBLIC MEETING This notice is given to meet the requirements of the S.C. Freedom of Information Act and the Americans with Disabilities Act. Furthermore, this facility is accessible to individuals with disabilities, and special accommodations will be provided if requested in advance. 1201 MAIN STREET, SUITE 1510, COLUMBIA, SC 29201 // (P) 803.737.6885 // (F) 803.737.7070 // WWW.RSIC.SC.GOV 2 AMENDED DRAFT South Carolina Retirement System Investment Commission Meeting Minutes September 10, 2020 9:30 a.m. -

Fixed Income Strategies and Alternatives in a Zero-Interest Rate Environment - September 2016 - September 2016

September 2016 PROMOTION. FOR INVESTMENT PROFESSIONALS ONLY. NOT FOR PUBLIC DISTRIBUTION Insurance linked Strategies Uncorrelated risk Premia and active Management Time to Look at European Asset Backed Securities Bringing Direct Lending to the Nordics Alternative Credit: an Oasis of Yield in the NIRP Desert Fixed Income Strategies and Alternatives in a Zero-Interest Rate Environment www.hedgenordic.com - September 2016 www.hedgenordic.com - September 2016 PROMOTION. FOR INVESTMENT PROFESSIONALS ONLY. NOT FOR PUBLIC DISTRIBUTION Contents INTRODUCTION HedgeNordic is the leading media covering the Nordic alternative Viewing the Credit LAndSCApe MoMA AdViSorS roLLS expenSiVe VALuAtionS, But SupportiVe teChniCALS for investment and hedge fund universe. through An ALternAtiVe LenS out ASgArd Credit KAMeS inVeStMent grAde gLobal Bond fund The website brings daily news, research, analysis and background that is relevant StrAtegy to Nordic hedge fund professionals from the sell and buy side from all tiers. HedgeNordic publishes monthly, quarterly and annual reports on recent developments in her core market as well as special, indepth reports on “hot topics”. HedgeNordic also calculates and publishes the Nordic Hedge Index (NHX) and is host to the Nordic Hedge Award and organizes round tables and seminars. 62 20 40 the Long And Short of it - the tortoiSe & the hAre: gLobal CorporAte BondS - Targeting opportunitieS in SCAndinaviAn,independent, A DYNAMIC APPROacH TO FIXED INCOME & SRI/ESG in SeArCh of CouponS u.S. LeVerAged Credit eSg, CAt Bond inVeSting HIGH YIELD INVESTING HedgeNordic Project Team: Glenn Leaper, Pirkko Juntunen, Jonathan Furelid, Tatja Karkkainen, Kamran Ghalitschi, Jonas Wäingelin Contact: 33 76 36 48 58 Nordic Business Media AB BOX 7285 SE-103 89 Stockholm, Sweden Targeting opportunities in End of the road - How CTAs the Added intereSt Corporate Number: 556838-6170 The Editor – Faith and Fixed Income.. -

Why Convertible Arbitrage Is a True Market Neutral Strategy

WHY CONVERTIBLE ARBITRAGE IS A TRUE MARKET NEUTRAL STRATEGY How does convertible arbitrage perform in different markets? Transcript of a video recorded on November 30, 2017. Eli Pars, Co-CIO, Head of Alternative Strategies and Co-Head of Convertible Strategies, Senior Co-PM, explains that convertible arbitrage has performed well in most equity market environments—and that the strategy has done its best in declining equity markets historically. ELI PARS The nice thing is it tends to perform well in most equity market environments. In a rising market, you benefit from Co-CIO, Head of the net long, the net long embedded in the hedge. So you can make a little bit of money there and you can trade Alternative Strategies and Co-Head of around the volatility. It tends to do a little better in more volatile markets. Convertible Strategies, Senior Co-PM The interesting thing is, historically, it’s often done its best in declining equity markets. Now, sometimes it depends on the nature of the equity market and the nature of the bear market, but if you look back to the early 2000s when the equity market sold off materially, convert arb did really well. Investors made money, made significant money in a lot of cases, when the equity market was down. That wasn’t the case in 2008 when it was more of a financial crisis, but it’s kind of helpful for investors as they look forward and think where the next bear market might be. If to the extent you’re in the camp that you think that ultimately it’ll be an over-valued equity market that corrects similar to what we had in the early 2000s, that could quite possibly be a very nice environment for convert arb. -

Post-Modern Portfolio Theory Supports Diversification in an Investment Portfolio to Measure Investment's Performance

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Rasiah, Devinaga Article Post-modern portfolio theory supports diversification in an investment portfolio to measure investment's performance Journal of Finance and Investment Analysis Provided in Cooperation with: Scienpress Ltd, London Suggested Citation: Rasiah, Devinaga (2012) : Post-modern portfolio theory supports diversification in an investment portfolio to measure investment's performance, Journal of Finance and Investment Analysis, ISSN 2241-0996, International Scientific Press, Vol. 1, Iss. 1, pp. 69-91 This Version is available at: http://hdl.handle.net/10419/58003 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend -

307439 Ferdig Master Thesis

Master's Thesis Using Derivatives And Structured Products To Enhance Investment Performance In A Low-Yielding Environment - COPENHAGEN BUSINESS SCHOOL - MSc Finance And Investments Maria Gjelsvik Berg P˚al-AndreasIversen Supervisor: Søren Plesner Date Of Submission: 28.04.2017 Characters (Ink. Space): 189.349 Pages: 114 ABSTRACT This paper provides an investigation of retail investors' possibility to enhance their investment performance in a low-yielding environment by using derivatives. The current low-yielding financial market makes safe investments in traditional vehicles, such as money market funds and safe bonds, close to zero- or even negative-yielding. Some retail investors are therefore in need of alternative investment vehicles that can enhance their performance. By conducting Monte Carlo simulations and difference in mean testing, we test for enhancement in performance for investors using option strategies, relative to investors investing in the S&P 500 index. This paper contributes to previous papers by emphasizing the downside risk and asymmetry in return distributions to a larger extent. We find several option strategies to outperform the benchmark, implying that performance enhancement is achievable by trading derivatives. The result is however strongly dependent on the investors' ability to choose the right option strategy, both in terms of correctly anticipated market movements and the net premium received or paid to enter the strategy. 1 Contents Chapter 1 - Introduction4 Problem Statement................................6 Methodology...................................7 Limitations....................................7 Literature Review.................................8 Structure..................................... 12 Chapter 2 - Theory 14 Low-Yielding Environment............................ 14 How Are People Affected By A Low-Yield Environment?........ 16 Low-Yield Environment's Impact On The Stock Market........ -

Hedge Fund Performance During the Internet Bubble Bachelor Thesis Finance

Hedge fund performance during the Internet bubble Bachelor thesis finance Colby Harmon 6325661 /10070168 Thesis supervisor: V. Malinova 1 Table of content 1. Introduction p. 3 2. Literature reviews of studies on mutual funds and hedge funds p. 5 2.1 Evolution of performance measures p. 5 2.2 Studies on performance of mutual and hedge funds p. 6 3. Deficiencies in peer group averages p. 9 3.1 Data bias when measuring the performance of hedge funds p. 9 3.2 Short history of hedge fund data p. 10 3.3 Choice of weight index p. 10 4. Hedge fund strategies p. 12 4.1 Equity hedge strategies p. 12 4.1.1 Market neutral strategy p. 12 4.2 Relative value strategies p. 12 4.2.1 Fixed income arbitrage p. 12 4.2.2 Convertible arbitrage p. 13 4.3 Event driven strategies p. 13 4.3.1 Distressed securities p. 13 4.3.2 Merger arbitrage p. 14 4.4 Opportunistic strategies p. 14 4.4.1 Global macro p. 14 4.5 Managed futures p. 14 4.5.1 Trend followers p. 15 4.6 Recent performance of different strategies p. 15 5. Data description p. 16 6. Methodology p. 18 6.1 Seven factor model description p. 18 6.2 Hypothesis p. 20 7. Results p. 21 7.1 Results period 1997-2000 p. 21 7.2 Results period 2000-2003 p. 22 8. Discussion of results p. 23 9. Conclusion p. 24 2 1. Introduction A day without Internet today would be cruel and unthinkable. -

40Actplussm Application for Hedge Funds and Private

Executive Risk Indemnity Inc. Administrative Offices/Mailing Address: Home Office 82 Hopmeadow Street Wilmington, Delaware 19805-1297 Simsbury, Connecticut 06070-7683 40ACTPLUSSM APPLICATION FOR HEDGE FUNDS AND PRIVATE INVESTMENT FUNDS NOTICE: THE POLICY FOR WHICH THIS APPLICATION IS MADE APPLIES, SUBJECT TO ITS TERMS, ONLY TO “CLAIMS” FIRST MADE DURING THE “POLICY PERIOD,” OR ANY EXTENDED REPORTING PERIOD. THE LIMIT OF LIABILITY AVAILABLE TO PAY DAMAGES OR SETTLEMENTS WILL BE REDUCED, AND MAY BE EXHAUSTED, BY “DEFENSE EXPENSES,” AND “DEFENSE EXPENSES” WILL BE APPLIED AGAINST THE RETENTION. THE UNDERWRITER HAS NO DUTY UNDER THIS POLICY TO DEFEND ANY “CLAIM.” ACCEPTANCE OR RECEIPT BY THE UNDERWRITER OF THIS APPLICATION WILL NOT OBLIGATE THE UNDERWRITER TO ISSUE ANY POLICY OF INSURANCE, NOR PROVIDE REQUESTED COVERAGE FOR ALL ENTITIES LISTED IN THIS APPLICATION OR IN ANY SCHEDULE ATTACHED HERETO. PLEASE READ THE ENTIRE APPLICATION CAREFULLY BEFORE SIGNING. 1. (a) Name of Applicant: Business Address: City: State: ZIP Code: Web site Internet address (if applicable): (b) Name and title of the officer at the principal sponsor or organization for the Applicant designated as the representative to receive all notices from the Underwriter on behalf of all person(s) and entity(ies) proposed for this insurance: 2. (a) SCHEDULE OF PRIVATE FUNDS (Please attach separate sheet if necessary.) Name of Type Total Total General Partner’s Minimum 3(c)7 Fund Structure Date Private (see chart Assets Equity Equity Invest- (Yes/No) (LP, LLC, Opened Fund below) Market ($mm) ($mm) ment etc.) Value ($mm) ($mm) TYPES OF PRIVATE FUNDS Market Neutral Distressed Securities Market Timing Funds of Funds Aggressive Growth Short Selling Emerging Markets Global Macro Merger Arbitrage Income Convertible Arbitrage Other: Form C27429 (08/2012) 1 Catalog No.