Government of Assam

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LIST of ACCEPTED CANDIDATES APPLIED for the POST of GD. IV of AMALGAMATED ESTABLISHMENT of DEPUTY COMMISSIONER's, LAKHIMPUR

LIST OF ACCEPTED CANDIDATES APPLIED FOR THE POST OF GD. IV OF AMALGAMATED ESTABLISHMENT OF DEPUTY COMMISSIONER's, LAKHIMPUR Date of form Sl Post Registration No Candidate Name Father's Name Present Address Mobile No Date of Birth Submission 1 Grade IV 101321 RATUL BORAH NAREN BORAH VILL:-BORPATHAR NO-1,NARAYANPUR,GOSAIBARI,LAKHIMPUR,Assam,787033 6000682491 30-09-1978 18-11-2020 2 Grade IV 101739 YASHMINA HUSSAIN MUZIBUL HUSSAIN WARD NO-14, TOWN BANTOW,NORTH LAKHIMPUR,KHELMATI,LAKHIMPUR,ASSAM,787031 6002014868 08-07-1997 01-12-2020 3 Grade IV 102050 RAHUL LAMA BIKASH LAMA 191,VILL NO 2 DOLABARI,KALIABHOMORA,SONITPUR,ASSAM,784001 9678122171 01-10-1999 26-11-2020 4 Grade IV 102187 NIRUPAM NATH NIDHU BHUSAN NATH 98,MONTALI,MAHISHASAN,KARIMGANJ,ASSAM,788781 9854532604 03-01-2000 29-11-2020 5 Grade IV 102253 LAKHYA JYOTI HAZARIKA JATIN HAZARIKA NH-15,BRAHMAJAN,BRAHMAJAN,BISWANATH,ASSAM,784172 8638045134 26-10-1991 06-12-2020 6 Grade IV 102458 NABAJIT SAIKIA LATE CENIRAM SAIKIA PANIGAON,PANIGAON,PANIGAON,LAKHIMPUR,ASSAM,787052 9127451770 31-12-1994 07-12-2020 7 Grade IV 102516 BABY MISSONG TANKESWAR MISSONG KAITONG,KAITONG ,KAITONG,DHEMAJI,ASSAM,787058 6001247428 04-10-2001 05-12-2020 8 Grade IV 103091 MADHYA MONI SAIKIA BOLURAM SAIKIA Near Gosaipukhuri Namghor,Gosaipukhuri,Adi alengi,Lakhimpur,Assam,787054 8011440485 01-01-1987 07-12-2020 9 Grade IV 103220 JAHAN IDRISH AHMED MUKSHED ALI HAZARIKA K B ROAD,KHUTAKATIA,JAPISAJIA,LAKHIMPUR,ASSAM,787031 7002409259 01-01-1988 01-12-2020 10 Grade IV 103270 NIHARIKA KALITA ARABINDA KALITA 006,GUWAHATI,KAHILIPARA,KAMRUP -

Reactive Energy 07-12-2020 to 03-01-2021

भ रत सरक र Government of India SPEED POST/FAX Ministry of Power वि饍युत म車त्र लय Ph : 0364-2534077 उत्तर पूिी क्षेत्रीय ुतवि饍य ससमतत Fax: 0364-2534040 North Eastern Regional Power Committee Email: [email protected] एन ई आर पी सी कॉम्पतलेटस, डⴂग प रम ओ, ल प ल ङ, सश쥍लⴂग-७९३००६, मेघ लय website: www.nerpc.nic.in NERPC Complex, Dong Parmaw, Lapalang, Shillong - 793006, Meghalaya No. NERPC/COM/REACTIVE/2020/3779-3801 February 01, 2020 To, 1. CMD, TSECL, Bidyut Bhawan, Agartala - 799001. 2. Engineer-in-Chief (P&ED), Govt. of Mizoram, New Secretariat Complex, Khatla, Aizawl-796001. 3. Director (Dist.), MePDCL, Lumjingshai, Short Round Road, Shillong-793001. 4. Chief General Manager (Comml.), APDCL, Bijuli Bhawan, Paltan Bazar, Guwahati-781 001. 5. Chief Engineer (P), W. E Zone, Deptt. of Power, Govt. of Arunachal Pradesh, Vidyut Bhawan, Itanagar- 791 111. 6. Managing Director, MSPDCL, Secure Office Bldg Complex, 3rd Floor, South Block, Near 2nd MR Gate, Imphal – 01 7. Chief Engineer (Power), Dept. of Power, Govt. of Nagaland, Kohima-797001. 8. ED (Comml.), NEEPCO, Brookland Compound, Lower New Colony, Shillong-793003. 9. ED, NERLDC, POSOCO, Dongtieh Lower Nongrah, Lapalang, Shillong-793006. 10. GM (Comml.),NHPC, NHPC Office Complex, Sector 33,Faridabad, Haryana-121003 04 weeks) | विषय:एबीटी रेजीम के तहत दिन 車क 07.12.2020 से 03.01.2021( क ररए啍टटि एनजी क लेख Sub: Reactive Energy under ABT regime-for the period 07.12.2020 to 03.01.2021(04 weeks) - Reg महोिय, Sir, दिन 車क 07.12.2020 से 03.01.2021 (04 weeks) की अिधि क ररए啍टटि एनजी लेख 啍जसमे पलू और दहति ररयⴂ के बीच िेय / प्र 啍ततयो嵍य वििरणⴂ को इसके स थ भेज ज रह हℂ | ररए啍टटि एनजी के प्रभ र/ भुगत न IEGC-April 2010 के उपब車ि 6.6(2) के अनुस र श ससत हⴂगे जो कक 1 अप्रेल 2020 से 15.0 पैसे/केिीएआरएच होग,इसके ब ि प्रतत िषष 0.5 पैसे पररकसलत ककय ज एग जबतक कक अꅍयथ आयोग 饍ि र स車शोधित न ककय ज ए | The statement of Reactive Energy account giving details of payables/receivables with the pool and between beneficiaries in rupees for the period 07.12.2020 to 03.01.2021 (04 weeks) is sent herewith. -

Karbi Anglong Substate BSAP

BIODIVERSITY STRATEGY AND ACTION PLAN FOR KARBI-ANGLONG A PROJECT UNDERTAKEN AS PART OF THE NATIONAL BIODIVERSITY STRATEGY AND ACTION PLAN Prepared By [A society for Biodiversity Conservation in North East India] “EVER GREEN” Samanwoy Path (survey) PO: Beltola, Guwahati – 781 028 ASSAM :: INDIA e-mail: [email protected] Website: www.aaranyak.com 1 Chapter-1 Introduction Earth’s plants, animals, and micro-organisms interacting with one another and with the physical environment in ecosystems form the foundation of sustainable development. Biotic resources from this wealth of life support human livelihoods and aspirations and make it possible to adapt to changing needs and environments. The current unabated erosion of the diversity of species, genes and ecosystems taking place will undermine progress towards a sustainable society. In fact, the continuing loss of biodiversity is a telling measure of the imbalance between human needs and wants and nature’s capacity. Biodiversity is the variety and variability of plant and animal species on our planet. Diversity itself has a particular value and importance. There are three broad levels of biodiversity: genetic variation within species (and number of individuals within a species); the variety of species within a habitat or ecosystem; and the variety of habitats on the planet. Biodiversity has ethical, social, scientific, aesthetic and economic value distinct from that of biological resources. Its total economic value is made up of several components, but is extremely difficult to estimate because of the lack of information and uncertainty. The general economic case for biodiversity conservation in developing countries is nevertheless strong. Some loss of biodiversity is unavoidable, but there is little doubt that the current rate of loss in socially excessive and reflects a significant under-valuation of biodiversity. -

Language, Part IV B(I)(A)-C-Series, Series-4, Assam

CENSUS OF INDIA 1991 SERIES 04 - ASSAM PART IV B(i)(a) - C-Series LANGUAGE Table C-7 State, Districts, Circles and Towns DIRECTORATE OF CENSUS OPERATIONS, ASSAM Registrar General of India (tn charge of the Census of India and vital statistics) Office Address: 2-A. Mansingh Road. New Delhi 110011. India Telephone: (91-11) 338 3761 Fax: (91-11) 338 3145 Email: [email protected] Internet: http://www.censusindia.net Registrar General of India's publications can be purchased from the following: • The Sales Depot (Phone: 338 6583) Office of the Registrar General of India 2-A Mansingh Road New Delhi 110 011, India • Directorates of Census Operations in the capitals of all states and union territories in India • The Controller of Publication Old Secretariat Civil Lines Delhi 110054 • Kitab Mahal State Emporium Complex, Unit No.21 Saba Kharak Singh Marg New Delhi 110 001 • Sales outlets of the Controller of Publication aU over India • Census data available on the floppy disks can be purchased from the following: • Office of the Registrar i3enerai, india Data Processing Division 2nd Floor. 'E' Wing Pushpa Shawan Madangir Road New Delhi 110 062, India Telephone: (91-11) 608 1558 Fax: (91-11) 608 0295 Email: [email protected] o Registrar General of India The contents of this publication may be quoted citing the source clearly PREFACE This volume contains data on language which was collected through the Individual Slip canvassed during 1991 Censlis. Mother tongue is a major social characteristic of a person. The figures of mother tongue were compiled and grouped under the relevant language for presentation in the final table. -

List of Candidates Called for Preliminary Examination for Direct Recruitment of Grade-Iii Officers in Assam Judicial Service

LIST OF CANDIDATES CALLED FOR PRELIMINARY EXAMINATION FOR DIRECT RECRUITMENT OF GRADE-III OFFICERS IN ASSAM JUDICIAL SERVICE. Sl No Name of the Category Roll No Present Address Candidate 1 2 3 4 5 1 A.M. MUKHTAR AHMED General 0001 C/O Imran Hussain (S.I. of Ploice), Convoy Road, Near Radio Station, P.O.- CHOUDHURY Boiragimath, Dist.- Dibrugarh, Pin-786003, Assam 2 AAM MOK KHENLOUNG ST 0002 Tipam Phakey Village, P.O.- Tipam(Joypur), Dist.- Dibrugarh(Assam), Pin- 786614 3 ABBAS ALI DEWAN General 0003 Vill: Dewrikuchi, P.O.:-Sonkuchi, P.S.& Dist.:- Barpeta, Assam, Pin-781314 4 ABDIDAR HUSSAIN OBC 0004 C/O Abdul Motin, Moirabari Sr. Madrassa, Vill, PO & PS-Moirabari, Dist-Morigaon SIDDIQUEE (Assam), Pin-782126 5 ABDUL ASAD REZAUL General 0005 C/O Pradip Sarkar, Debdaru Path, H/No.19, Dispur, Ghy-6. KARIM 6 ABDUL AZIM BARBHUIYA General 0006 Vill-Borbond Part-III, PO-Baliura, PS & Dist-Hailakandi (Assam) 7 ABDUL AZIZ General 0007 Vill. Piradhara Part - I, P.O. Piradhara, Dist. Bongaigaon, Assam, Pin - 783384. 8 ABDUL AZIZ General 0008 ISLAMPUR, RANGIA,WARD NO2, P.O.-RANGIA, DIST.- KAMRUP, PIN-781365 9 ABDUL BARIK General 0009 F. Ali Ahmed Nagar, Panjabari, Road, Sewali Path, Bye Lane - 5, House No.10, Guwahati - 781037. 10 ABDUL BATEN ACONDA General 0010 Vill: Chamaria Pam, P.O. Mahtoli, P.S. Boko, Dist. Kamrup(R), Assam, Pin:-781136 11 ABDUL BATEN ACONDA General 0011 Vill: Pub- Mahachara, P.O. & P.S. -Kachumara, Dist. Barpeta, Assam, Pin. 781127 12 ABDUL BATEN SK. General 0012 Vill-Char-Katdanga Pt-I, PO-Mohurirchar, PS-South Salmara, Dist-Dhubri (Assam) 13 ABDUL GAFFAR General 0013 C/O AKHTAR PARVEZ, ADVOCATE, HOUSE NO. -

Violence and Search for Peace in Karbi Anglong, Assam

Violence and Peace in Karbi Anglong, Assam Violence and Search © North Eastern Social Research Centre, Guwahati, 2008 Tom Mangattuthazhe is Director, Mission Home, Manja P.O, Karbi Anglong (Dt) for Peace in Assam [email protected] Karbi Anglong, Assam www.missionhomemanja.com Published by: North Eastern Social Research Centre, 110 Kharghuli Road (lst floor) Guwahati 781004 Assam, India Tom Mangattuthazhe Tel. (+91-361) 2602819 Fax: (+91-361) 2732629 (Attn NESRC) Email: [email protected] www.creighton.edu/CollaborativeMinistry/NESRC Cover design : North Eastern Social Research Centre Kazimuddin Ahmed Guwahati Panos South Asia 110 Kharghuli Road (first floor) 2008 Guwahati 781004 TAble of ConTenTs Acknowledgements Chapter Page This publication is the result of the efforts of many people. Acknowledgements I would like first of all, to recognise and thank all the members of the Peace Team: Mr. John Phangcho, Mr. Borsali Teron, Mr. 1. The Background of Karbi Anglong 1 Anil Ekka, Miss. Sarah Phangchopi as well as the youth who 2. The Background of the Conflicts 9 have committed themselves to working for a just peace in the 3. A Way out of the Conflicts 21 context explored here in. Their efforts and daily struggles are invaluable in their own right, and are the principal source of our 4. Participatory Rural Appraisal of Manja 31 learning and inspiration. Without them this publication would 5. Search for Peace with Justice 44 be meaningless. Appendix-1 : I acknowledge next the fine work of Henry Martin Institute, Chronology of Events after the Karbi-Dimasa Conflict Began 57 Hyderabad and their valuable technical help in realising this project. -

Conflict Mapping and Peace Processes in North East India Conflict Mapping and Peace Processes in Northeast India

Conflict Mapping And Peace Processes in North East India Conflict Mapping and Peace Processes in Northeast India © North Eastern Social Research Centre 2008 Published by: North Eastern Social Research Centre 110 Kharghuli Road (1st floor) Guwahati 781004 Assam, India Edited by : Tel. (0361) 2602819 Fax: (91-361) 2732629 (Attn NESRC) Lazar Jeyaseelan Email: [email protected] Website : www.creighton.edu/CollaborativeMinistry/NESRC Cover page designed by: Kazimuddin Ahmed Panos South Asia 110 Kharghuli Road (1st floor) Guwahati 781001 Assam, India Printed at : Saraighat Laser Print North Eastern Social Research Centre Guwahati III IV Dedication Acknowledgement Dr. Lazar Jeyaseelan who had accepted the responsibility of edit- ing this book phoned and told me on 12th April 2007 that he had done what he could, that he was sending the CD to me and that This volume comes out of the efforts of some civil society organisations that wanted to go beyond relief and charity to explore I should complete this work. He must have had a premonition avenues of peace. Realising that a better understanding of the issues because he died of a massive heart attack two days later during involved in conflicts and peace building was required, they encouraged a public function at Makhan Khallen village, Senipati District, some students and other young persons to do a study of a few areas Manipur. of tension. The peace fellowships were advertised and the applicants were interviewed. Those appointed for the task were guided by Dr Jerry Born at Madhurokkanmoi in Tamil Nadu on 24th June Thomas, Dr L. Jeyaseelan and Dr Walter Fernandes. -

Sarva Siksha Abhijan Assam Prathamic Siksha Achani Parisad,Assam

SARVA SIKSHA ABHIJAN ASSAM PRATHAMIC SIKSHA ACHANI PARISAD,ASSAM WRITEUP OF ANNUAL WORK PLAN & BUDGET - 2003 - 2004 [JU LY,2003 TO MARCH,2004 ] DISTRICT :: KARBI ANGLONG KARBI ANGLONG AUTONOMOUS COUNCIL, DIPHU KARBi ANGLONG DISTRICT AT A GLANCE INTRUDUCTION : Karbi Anglong is. one of the higgest districts of Assam, predcniinaiitly inhabited by scheduled tribe pofuildtion. scatteied in different pads of thinly populated 2752 villages v.:th 3033 numbers of habitations The total area of the district is bounded by Nagaon and Golaghat distncis in the north To the South, It is bounded by ,'v^eghalaya and Noi1h Cachar Hills Autonomous Council. Golaghat and the state of Nagairti. ' are standing in the east. To the west it is bounded by Meghalaya and Nagaon district. - iiis'ifCt W'!!’' oensi hopn'o; fo: Cu'i't;"' ha: ■■■ ■ - ; ' , ■ - ■ ' ■■ I'lt'/ilu !•' Area(As per 2001 Census) Urban 10.434 Sq.Krn 10,397 Sci.Km 37 Sq. km. 2. a) Population As per 1991 census Parameters Total ■ 1 * Ryral . 1 r ' . Urban . l . ' j o t e l j Rural! Urban Populatif>R 6,62,723 3,92,257 70,4f)6 3.12,320 NA NA SC Population 27,991 25,9t3 2.0 7B n a NA NA ST Population 3.41.718 3.19,207 22,511 M A NA NA Male 3,47.607 3,08,543 39.11'v'i ^.22.599 NA NA Female 3,15,116 2,83,714 31,402 3.89,721 NA NA Literate ” 2,37,788 1.95,568 42,220 3,92,589 NA NA Total workers 2,52,123 2,30,265 21,858 NA NA NA S'.S ( K.uhl 1. -

District: Karbi Anglong Merit List of Class

MERIT LIST OF CLASS- V STUDENT'S QUALIFIED FOR SCHOLARSHIP UNDER "CHIEF MINISTER'S SPECIAL SCHOLARSHIP SCHEME" FOR THE YEAR 2018 DISTRICT: KARBI ANGLONG Sl. Block Name of Examination Roll No Medium Name of Candidate Sex Name of Guardian Name of School where Total marks scored No Centre from Appeared out of 100 (in) Numerical Words 1 Amri Amguri H. School 51500004 Assamese Bhanumoti Das Girl Santosh Das No.2 Ouguri LP School 64 Sixty Four 2 Amri Amguri H. School 51500005 Assamese Bidyasing Ronghang Boy Rajib Ronghang Amguri LP School 60 Sixty 3 Amri Amguri H. School 51500006 Assamese Bihuti Amsi Girl Rinu Amsi Pumakuchi LP School 51 Fifty One 4 Amri Amguri H. School 51500007 Assamese Bristi Amsi Girl Dipankar Das Amguri LP School 52 Fifty Two 5 Amri Amguri H. School 51500008 Assamese Dipa Puma Girl Nameswar Puma Amguri LP School 66 Sixty Six 6 Amri Amguri H. School 51500009 Assamese Dipanjali Das Basumatary Girl Dibjyoti Das Amguri LP School 68 Sixty Eight 7 Amri Amguri H. School 51500010 Assamese Dipu Kholar Boy Joidan Kholar Pumakuchi LP School 55 Fifty Five 8 Amri Amguri H. School 51500011 Assamese Jatin Malang Boy Nande Malang Baulagog Jr. Basic LP 56 Fifty Six School 9 Amri Amguri H. School 51500015 Assamese Manisha Beypi Girl Sarthe Bey Baulagog Jr. Basic LP 58 Fifty Eight School 10 Amri Amguri H. School 51500018 Assamese Rakesh Chakraborty Boy Chittranjan No.2 Ouguri LP School 51 Fifty One Chokraborty 11 Amri Amguri H. School 51500020 Assamese Ronsita Mithi Girl Komal Mithi Pumakuchi LP School 60 Sixty 12 Amri Amguri H. -

The Hybrid in Rongbong Terang: a Literary Case Study

www.TLHjournal.com The Literary Herald ISSN: 2454-3365 An International Refereed English e-Journal Impact Factor: 2.24 (IIJIF) The Hybrid in Rongbong Terang: a literary case study Dhrijyoti Kalita Research Scholar M.A. (English) Delhi University Communities are more than mere social constructions. They have their own, pure individual narratives and never for once would they relent to dilute them. In this paper, I propose that although hybridization as a social act has always had been a perpetual process among the communities, yet its encounter at the inception especially in the postcolonial scene, is far from congenial, rather intimidating. “Diaspora, displacement, relocation”, the fear of cultural invasion and overhaul and the endless strife for identity preservation constitute the hybrid. In this case, I examine two texts of Rongbong Terang written in Assamese, viz. ‘Jak Herowa Pakshi’ (lit. Trans. ‘Birds of the lost flock’) and ‘Mirbin’ respectively based on the Singhason Hill conflict between the Karbi and the Kuki communities and the counter-cultural struggles of the Longnit-Langparpan valley people of Karbi Anglong. My objective here is to posit how the hybrid, blended with modernity, has led to a subculture of disenchantment, despair, intense and bland turbulence and digression within a small community like the Karbis. These texts of Rongbong Terang portray nothing more than a “shared culture” of violence and dismay while evoking all throughout the postcolonial spirit of Anderson’s “imagined communities”. The question to be asked here is, “Who is representing whom and why?” as modernity also gatecrashes the wits of uncomplicated minds resulting into a severe imbalance in the traditional but peaceful narrative. -

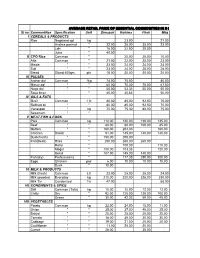

Sl No Commodities Specification Unit Dimapur Kohima Phek Mkg I

AVERAGE RETAIL PRICE OF ESSENTIAL COMMODITIES IN 8 C Sl no Commodities Specification Unit Dimapur Kohima Phek Mkg I CEREALS & PRODUCTS Rice Nagaland spl kg 23.00 21.00 Andhra parimol " 22.00 25.00 25.00 23.00 Lahi " 18.00 22.50 20.00 Juha " 40.00 II CPO Rice Common " 20.00 20.00 10.00 Atta Common " 21.00 22.00 25.00 23.00 Maida " " 23.00 24.00 24.00 24.00 Suji " " 23.00 24.00 25.00 28.00 Bread Sliced 400gm. pkt 18.00 20.00 20.00 20.00 III PULSES Arahar dal Common 1kg 74.00 75.00 80.00 Masur dal " " 60.00 70.00 70.00 67.50 Naga dal " " 50.00 53.33 55.00 50.00 Soya bean " 40.00 40.83 50.00 IV OILS & FATS M.oil Common 1 ltr 80.00 85.00 92.50 75.00 Refined oil " " 80.00 85.00 92.50 70.00 Vanaspati " kg 70.00 75.00 80.00 75.00 Sesamum " " V MEAT,FISH & EGGS Pork Common kg 110.00 120.00 130.00 125.00 Beef " " 80.00 80.00 100.00 85.00 Mutton " " 160.00 203.33 160.00 Chicken Broiler " 91.00 135.00 140.00 140.00 Duck(fresh) " " 150.00 200.00 Fish(fresh) Hilsa " 250.00 260.00 260.00 Rohu " 100.00 110.00 Mogur " 100.00 103.33 120.00 Borali " 107.00 145.00 140.00 Fish(dry) Pothi(assam) " 177.33 280.00 200.00 Eggs Chicken pair 6.00 10.00 10.00 10.00 Duck " 10.00 VI MILK & PRODUCTS Milk (fresh) Common Ltr 23.00 25.00 25.00 24.00 Milk (powder) Everyday kg 210.00 220.00 225.00 230.00 Milk Tin Condensed Tin 47.00 58.00 VII CONDIMENTS & SPICE Salt Common (Tata) kg 10.00 12.00 12.00 12.00 Chilly Dry " 92.00 125.00 120.00 100.00 Green " 30.00 42.33 50.00 45.00 VIII VEGETABLES Potato Common kg 22.00 24.00 15.00 11.00 Onion " " 35.00 37.00 40.00 25.00 Brinjal -

Regions of Assam

REGIONS OF ASSAM Geographically Assam is situated in the north-eastern region of the Indian sub- continent. It covers an area of 78,523 sq. kilometres (approximate). Assam – the gateway to north-east India is a land of blue hills, valleys and rivers. Assam has lavishly bestowed upon unique natural beauty and abundant natural wealth. The natural beauty of Assam is one of the most fascinating in the country with evergreen forests, majestic rivers, rich landscape, lofty green hills, bushy grassy plains, rarest flora and fauna, beautiful islands and what not. The capital of Assam is Dispur and the state emblem is one-hoed rhino. Assam is bounded by Manipur, Nagaland and Myanmar in the east and in the rest by West Bengal in the north by Bhutan and Arunachal Pradesh and in the route by Mizoram, Tripura, Bangladesh and Meghalaya. Literacy rate in Assam has seen upward trend and is 72.19 percent as per 2011 population census. Of that, male literacy stands at 77.85 percent while female literacy is at 66.27 percent. As per details from Census 2011, Assam has population of 3.12 Crores, an increase from figure of 2.67 Crore in 2001 census. Total population of Assam as per 2011 census is 31,205,576 of which male and female are 15,939,443 and 15,266,133 respectively. In 2001, total population was 26,655,528 in which males were 13,777,037 while females were 12,878,491. The total population growth in this decade was 17.07 percent while in previous decade it was 18.85 percent.