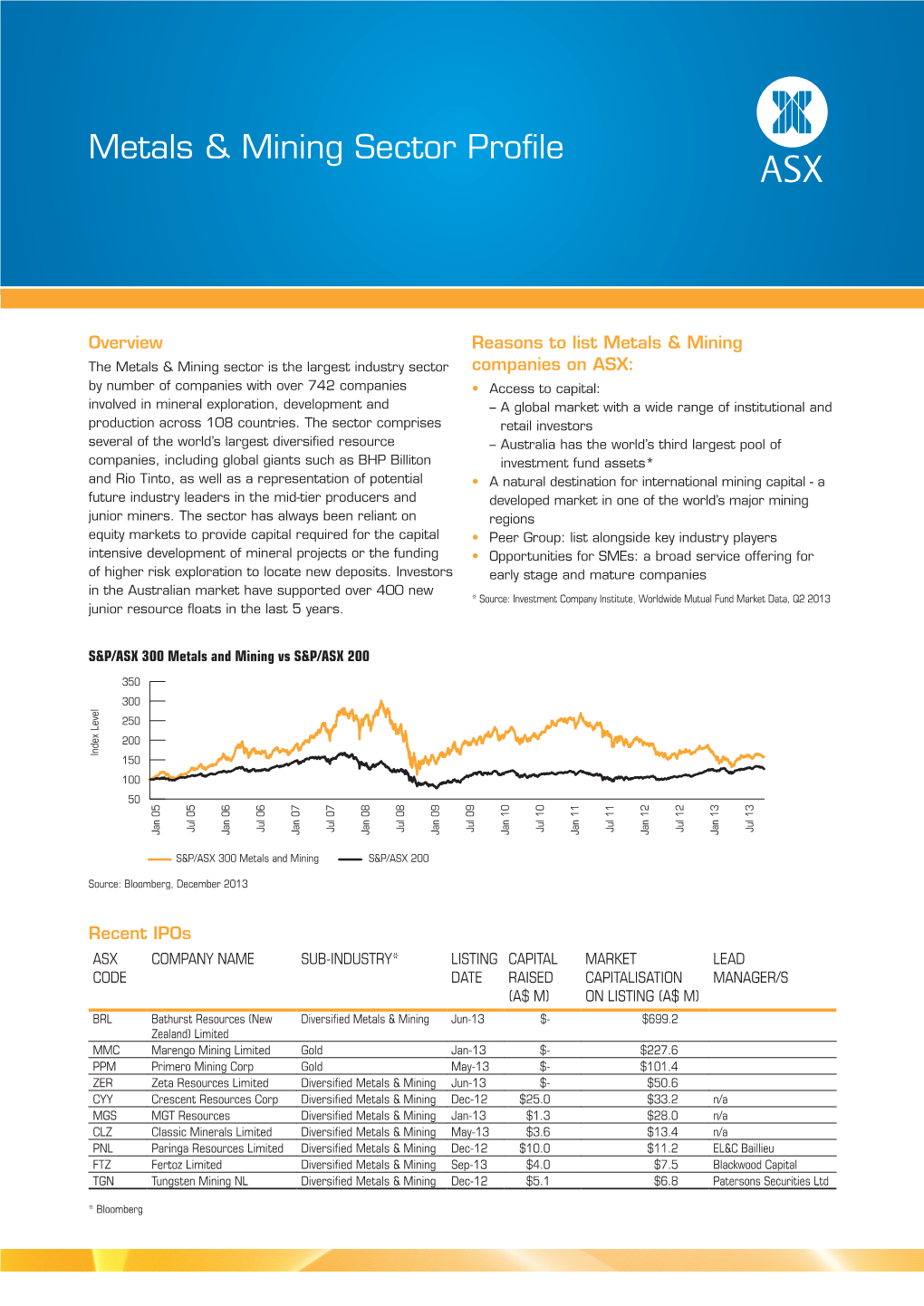

Metals & Mining Sector Profile

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Capital Expenditure Project Listing

CAPITAL EXPENDITURE PROJECT LISTING 1 January 1993 to 31 December 2016 NEDBANK GROUP ECONOMIC UNIT 07 February 2017 NOTES: Definition: The schedule is a listing of capital projects announced in the Republic of South Africa. It includes: Only projects valued at R20 million or more. Projects of an expansionary nature, i.e. capex which allows for an increase in the level of output, rather than pure replacement investment which involves the replacement of worn-out or outdated capital goods necessary for the continued operation and the maintenance of current output levels. The exceptions are: investment in equipment or machinery which reduces the harmful effects of pollution, and technological upgrading of equipment and machinery. Projects funded by both the private and public sectors. Projects reflecting direct foreign involvement. The listing is compiled on a sectoral basis, conforming to the Standard Industrial Classification. Limitations: Any analysis of the data needs to take account of the limitations outlined below: The schedule highlights significant areas of investment expenditure and not the absolute total value of all capital investment undertaken in the country. It serves as a rough guide to the general direction in which investment is moving and as an indication of the level of confidence in the economy. The full extent of replacement capital expenditure is not captured as mainly expansionary capital expenditure are published and recorded. In certain sectors a reliable indication of investment activity is not possible as typical investments are not large enough to be included in the schedule, even though the total capital expenditure in the sector may be substantial. -

Market Opener Advisor on 1300 651 898 Or [email protected]

Need more information? Contact your State One Market Opener advisor on 1300 651 898 or [email protected] Please see disclaimer at end of Wednesday 18 January 2017 document. Markets Today’s Stock Watch SFE 200 Futures (9.30am AEDST) 5642 -9 -0.2 NZX 50 7063 -0.1 -0.0 Wesfarmers Ltd (WES) DJIA Futures 19743 0 0.0 Anticipating $135M - $140M interim EBIT for the group’s S&P 500 Futures 2263 -10 -0.4 resources business, approximately in line with 1H FY 2016 and NASDAQ Futures 5040 -21 -0.4 greater than previous guidance. December quarter Curragh coal production increased 22.5% from the previous quarter, to 3.2Mt, Local Markets Commentary although the gain was largely due to adverse weather during the September quarter. For the year, metallurgical coal output fell The Australian market opens mid-week trade on 14.4% to 7.2Mt and steaming coal 1.9% to 3.4Mt. Bengalla largely negative leads. attributable coal production rose 2.7% to 3.4Mt. US equities markets traded for the first time this week. Incitec Pivot (IPL) In overnight commodities trade, gold and WTI Expecting to receive $US35.1M in damages related to delays for crude continued higher. Copper extended the Louisiana, US Waggaman ammonia plant. Monday’s fall. Iron ore turned lower. RCR Tomlinson (RCR) / Pilbara Minerals (PLS) The $A gained further after appreciating to $138M - $148M EPC contract secured by RCR for PLS’s WA ~US75.45c early yesterday evening. Pilgangoora lithium-tantalum project. Locally today, a monthly consumer sentiment report is due from Westpac and the Melbourne Institute, Integrated Research (IRI) 10.30am AEDST. -

Small and Mid-Cap Resources March 2017 Review

Small and Mid-Cap Resources March 2017 Review The Momentum Continues - 2017 to be a Good Year WHO IS IIR? Independent Investment Research, “IIR”, is an independent investment research house based in Australia and the United States. IIR specialises in the analysis of high quality commissioned research for Brokers, Family Offices and Fund Managers. IIR distributes its research in Asia, United States and the Americas. IIR does not participate in any corporate or capital raising activity and therefore it does not have any inherent bias that may result from research that is linked to any corporate/ capital raising activity. IIR was established in 2004 under Aegis Equities Research Group of companies to provide investment research to a select group of retail and wholesale clients. Since March 2010, IIR (the Aegis Equities business was sold to Morningstar) has operated independently from Aegis by former Aegis senior executives/shareholders to provide clients with unparalleled research that covers listed and unlisted managed investments, listed companies, structured products, and IPOs. IIR takes great pride in the quality and independence of our analysis, underpinned by high caliber staff and a transparent, proven and rigorous research methodology. INDEPENDENCE OF RESEARCH ANALYSTS Research analysts are not directly supervised by personnel from other areas of the Firm whose interests or functions may conflict with those of the research analysts. The evaluation and appraisal of research analysts for purposes of career advancement, remuneration and promotion is structured so that non-research personnel do not exert inappropriate influence over analysts. Supervision and reporting lines: Analysts who publish research reports are supervised by, and report to, Research Management. -

Equity Financing for Africa

ASX – Equity Financing for Africa There are now over 210 ASX mining and exploration companies with 1,200 projects in Africa spread across 36 countries. Over $5.6 billion has been raised through follow-on raisings by ASX listed companies for projects in Africa over the last 5 years. Source: IntierraLive August 2013 Mining Companies by Stage of Projects Number of Listed Mining Companies in Africa Diversified HKE 11 7% Producer 17% JSE 54 LSE & AIM 99 TSX & TSXV 192 Explorer 76% ASX 218 Source: IntierraLive, August 2013 Source: Intierralive, August 2013 • Over 210 ASX listed companies with assets in Africa • 1,200 projects spread across 36 African nations. • Of these projects, 37% are at grass-roots stage, 34% at exploration stage, and 29% are at advanced exploration stage ASX – Equity Financing for Africa Top 100 Stocks ASX COMPANY NAME COMPANY MARKET SECTOR* CODE TYPE^ CAPITALISATION (A$)* BHP BHP Billiton Limited Diversified $100,750,749,963 Diversified Metals & Mining RIO Rio Tinto Limited Producer $22,820,684,166 Diversified Metals & Mining NCM Newcrest Mining Limited Producer $7,565,463,283 Gold AAI Alcoa Inc. Diversified $7,274,558,272 Aluminium AWC Alumina Limited Diversified $2,764,132,230 Aluminum ZIM Zimplats Holdings Limited Producer $915,996,392 Precious Metals & Minerals LYC Lynas Corporation Ltd Producer $735,300,484 Diversified Metals & Mining AQA Aquila Resources Limited Producer $733,011,906 Coal & Consumable Fuels PDN Paladin Energy Ltd Producer $732,539,332 Coal & Consumable Fuels AGO Atlas Iron Limited Producer $677,740,214 -

2016 ASX Listed Mining Companies

2016 ASX Listed Mining Companies 3D Resources Limited Attila Resources Limited Boral Limited. A1 Consolidated Gold Limited Audalia Resources Limited Boss Resources Limited Abm Resources Nl Augur Resources Limited Botswana Metals Limited Accent Resources Nl Aurelia Metals Limited Bougainville Copper Limited Activex Limited Auroch Minerals Ltd Breaker Resources Nl Adelaide Resources Limited Aurora Minerals Limited Brickworks Limited Admiralty Resources Nl. Aus Tin Mining Ltd Brighton Mining Group Limited Aeon Metals Limited. Ausgold Limited Brockman Mining Limited Aeris Resources Limited Ausmon Resources Limited Broken Hill Prospecting Limited Agrimin Limited Ausquest Limited Bulletin Resources Limited Aguia Resources Limited Ausroc Metals Ltd Burey Gold Limited Alacer Gold Corp. Austral Gold Limited Burrabulla Corporation Limited Alara Resources Limited Australasian Resources Limited Buxton Resources Limited Alchemy Resources Limited Australia New Agribusiness & Chemical Buymyplace.Com.Au Limited Alcoa Inc. Group Ltd Cabral Resources Limited Alicanto Minerals Limited Australia United Mining Limited Caeneus Minerals Ltd Alkane Resources Limited Australian Bauxite Limited. Cannindah Resources Limited Alliance Resources Limited Australian Mines Limited Canyon Resources Limited Alloy Resources Limited Australian Pacific Coal Limited Cape Lambert Resources Limited Alt Resources Limited Australian Vanadium Limited Capital Mining Limited Altech Chemicals Ltd Avalon Minerals Limited Capral Limited Altona Mining Limited Avanco Resources Limited -

Chinese Mining Activity in Latin America: a Review of Recent Findings by IACOB KOCH-WESER*

CHINA AND LATIN AMERICA REPORT Chinese Mining Activity in Latin America: A Review of Recent Findings BY IACOB KOCH-WESER* Summary Findings A comprehensive review of China’s global mining activity is necessarily complex and multi-disciplinary. Mining is after ver the past decade, China has rapidly emerged all an activity, not an economic sector per se, like oil and gas. as the world’s leading consumer and importer of Although iron ore accounts for the bulk of China’s metals Ominerals. Minerals are used in a growing number imports in both value and volume terms, a diverse set of non- of applications, from simple steel tubes in China’s sprawling ferrous metals, each with unique dynamics, also figures into the infrastructure projects, to wires and magnets in high-technol- equation. At the macro-level, mining has to do with why and ogy gadgets destined for export. Under the aegis of China’s how China acquires natural resources—an issue that pertains official “Going-Out” strategy, China’s global mining activity to energy and agriculture as well. Mineral extraction can raise has also surged. Conservative data from China’s Ministry of broader questions about China’s industrial policy, resource use, Commerce (MOFCOM) indicates that mining accounted for engagement in foreign trade, investment, and capital markets, a fifth of China’s non-financial outbound investment from and not least, its relations with resource-rich economies. 2003–2012 (see Figure 1). Estimates based on individual This review draws selectively from the literature to explore a deals are far higher (see Appendix Table 1). -

Annual Report 2017

Base Resources Limited Annual Report 2017 Delivering BASE RESOURCES LIMITED ANNUAL REPORT 2017 baseresources.com.au 1 Contents Introduction 02 04 06 Base Resources’ (ASX & AIM: BSE) successful development of the Kwale Mineral Sands Project in southern Kenya and demonstrated track Highlights Chairman’s letter Operation record of delivering operational, safety and community development summary achievements, provides a solid foundation to grow a contemporary mid- tier resources company. 8 14 16 An optimised life of mine production profile, highly efficient operation and strong cash generation has Base Resources well placed to capitalise on an Sustainability in Business Corporate and improving commodity market and renewed investor interest in the sector. practice development finance With tenure secured and a near-mine exploration program underway, mine life extension now presents a significant opportunity for further 18 20 24 value creation. Marketing and Resources and Corporate Demonstrated mine development capability provides the basis to deliver sales reserves directory further shareholder value from acquisition opportunities. 25 95 Consolidated Additional financial shareholder statements information FORWARD LOOKING STATEMENTS Certain statements made in or Kwale Project, provisions and ing statements as a result of, any liability arising from fault, in connection with this Annual contingent liabilities and tax and among other factors, changes in negligence or negligent misstate- Report contain or comprise regulatory developments. economic -

Capital Expenditure Project Listing

CAPITAL EXPENDITURE PROJECT LISTING 1 January 1993 to 31 December 2015 NEDBANK GROUP ECONOMIC UNIT 16 March 2016 Comment: mixed-use development in Sedibeng worth R4,0 billion, the Menlyn Maine development precinct in The year 2015 was one of the most difficult for the South African economy, with weak global and Pretoria, worth R1,8 billion, and the final phase of the luxurious Umhlanga Pearl Sky in Durban, worth local demand, historically low global commodity prices, loadshedding, a sharp depreciation of the R1,3 billion. rand, as well as rising input costs, among other factors, weighing negatively on economic activity. These also hurt both consumer and business confidence. Although firms remained very cautious The transport, storage and communication sector announced 21 projects accounting for 25% of of committing to large-capacity expansion programmes, there was some improvement in capital the total and amounting to R21,3 billion, up from R8,9 billion in 2014. Most of the projects in this expenditure plans. Nedbank's Capital Expenditure Project Listing shows an increase in both sector involve the rehabilitation and construction of roads. The biggest project recorded in the second the number and value of projects announced in 2015. The projects amounted to R152,4 billion, up half was the Maluti-A-Phofung special economic zone (SEZ), worth R4,8 billion, which involves the from R58,6 billion in 2014. construction of a new 1 000 ha SEZ near Harrismith, which will provide road and rail logistics. It will Nedbank schedule: R billion (constant 2015 prices) Actual growth in capital formation % also act as a handling facility for the Gauteng–Durban port corridor and link it to the Bloemfontein– 1000 20 Cape Town corridor. -

PCF Resources Thermometer January 2019 Contents

PCF Resources Thermometer January 2019 Contents SECTION PAGE Executive Summary 3 PCF Group 150 4 Consensus Commodity Price Forecasts 8 Gold Thermometer 9 Copper Thermometer 16 Nickel Thermometer 22 Zinc Thermometer 27 Iron Ore Thermometer 32 PCF Capital Group PCF Corporate Advisory MinesOnline.com FutureGold Liam Twigger Graeme Testar Mike Sperinck Garth Ziegler Managing Director Director Technical Director Manager • Public market takeovers • Structured debt and hybrid • Web-based platform • World first regulated crypto • Corporate mergers and funding connecting buyers and sellers asset backed by cash, gold acquisitions • Mezzanine, convertible and of mining projects royalties and gold streams • General corporate advice commodity loans • ~ 4,000 users from over 100 • To operate via a registered countries Managed Investment Scheme • Asset acquisitions and • Access to non bank funding divestment network • Unique E-Newsletter • Providing dynamic funding to promoting new projects advance gold projects towards • Equity capital raising • Development project finance • Unparalleled global production • Corporate restructuring • Debt sizing distribution capacity • Security token offering • Strategic and technical reviews • Cash and short term investment scheduled for Q1 2019 solutions • 40% + successful sales ratio • Indicative valuations • Financial models PCF Resources Thermometer 2 Executive Summary We are pleased to present the January 2019 edition of the PCF Resources Thermometer. At the close of 31 December 2018, the value of the PCF150 was A$417 billion, up ~A$21 billion or ~5% from November, and the value of the PCF150C was C$235 billion, up ~C$12 billion or ~5% from October. Over the course of the calendar year, the market value of the PCF150 increased marginally by ~A$1 billion. -

Annual Financial Results for FY2015

ASX, AIM and Media Release 22 September 2015 Annual Financial Results for FY2015 Highlights First full year of production delivers strong operating results: o Revenue of $145.5 million ($29.1 million in FY2014) o Average revenue per tonne of ilmenite, rutile and zircon sold of $309 (US$256) o Operating costs per tonne of ilmenite, rutile and zircon produced of $124 (US$103 per tonne) o Average cost per tonne of ilmenite, rutile and zircon sold of $155 (US$130 per tonne). o Kwale Operations EBITDA1 of $62.6 million ($7.1 million in FY2014) and Group EBITDA of $54.8 million ($0.5 million loss in FY2014). Net loss of $16.0 million or 2.85 cents per share (loss of $14.1 million or 2.50 cents per share in FY2014). Cash flow from operations of $38.2 million (outflows of $3.6 million in FY2014). Closing unrestricted cash of $40.9 million and restricted cash of $6.5 million at 30 June 2015 ($20.9 million unrestricted cash and $5.4 million restricted cash at 30 June 2014). Base continues to progress the refinancing of the Kwale Project Debt Facility with the objective of securing a repayment profile more appropriate to the prevailing product price environment, and to ensure a robust financial footing from which to grow the business. Confirmations of credit approval have been received from the majority of lenders, with remaining lender’s credit approval processes still in progress. Completion of the refinancing is subject to the agreement of final terms and execution of documentation. -

Small and Mid-Cap Resources June 2017 Review

Small and Mid-Cap Resources June 2017 Review Investor interest to continue through 2017 WHO IS IIR? Independent Investment Research, “IIR”, is an independent investment research house based in Australia and the United States. IIR specialises in the analysis of high quality commissioned research for Brokers, Family Offices and Fund Managers. IIR distributes its research in Asia, United States and the Americas. IIR does not participate in any corporate or capital raising activity and therefore it does not have any inherent bias that may result from research that is linked to any corporate/ capital raising activity. IIR was established in 2004 under Aegis Equities Research Group of companies to provide investment research to a select group of retail and wholesale clients. Since March 2010, IIR (the Aegis Equities business was sold to Morningstar) has operated independently from Aegis by former Aegis senior executives/shareholders to provide clients with unparalleled research that covers listed and unlisted managed investments, listed companies, structured products, and IPOs. IIR takes great pride in the quality and independence of our analysis, underpinned by high caliber staff and a transparent, proven and rigorous research methodology. INDEPENDENCE OF RESEARCH ANALYSTS Research analysts are not directly supervised by personnel from other areas of the Firm whose interests or functions may conflict with those of the research analysts. The evaluation and appraisal of research analysts for purposes of career advancement, remuneration and promotion is structured so that non-research personnel do not exert inappropriate influence over analysts. Supervision and reporting lines: Analysts who publish research reports are supervised by, and report to, Research Management. -

Gresham Group 150

GRESHAM GROUP 150 Darren Martin July 2013 Gresham Advisory Partners [email protected] +61 8 9486 7077 +61 412 144 719 ASX RESOURCES - GRESHAM GROUP 150 After presenting the soft indicators last month, we’re only presenting hard facts for FY13 in the July edition of ‘Gresham Group 150’ , a ranking of the top 150 ASX listed resources companies (excluding oil and gas), by market capitalisation. The fortunes of the resources sector were in stark contrast to the ASX All Ordinaries for the twelve months to 30 June 2013. Whilst the ASX All Ordinaries was up 15.5% the ASX/S&P 200 Resources Index fell 9.3% (Gresham Group 150 down 13% for the year). The market value of the Gresham Group 150 constituents started the financial year at $367 billion, rose to $416 billion in January and then fell away to finish at $319 billion - down 13% for the year. In this edition we have ranked the performance of the Gresham Group 150 companies by share price and market capitalisation for the 12 month period to 30 June 2013 (only includes companies currently in the Gresham Group 150 and excludes dividends/capital returns). The star performer for the year was Sirius (+3,547%), with only 21 other companies providing positive share price appreciation and 31 companies market capitalisation appreciation during the year. Separately, we have prepared a rise and fall table comparing each company’s rank at 30 June 2013 vs 30 June 2012. Some of the movements will be driven by members of the FY13 valedictory list on page 9.