Privatization Processes As Ideological Moments: the Block Sales of Large-Scale State Enterprises in Turkey in the 2000S

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Günlük Bülten 12 Ağustos 2021 Piyasalarda Son Görünüm* USD/TL EUR/TRY EUR/USD BIST-100 Gram Altın Gösterge Tahvil 8,6314 10,1510 1,1744 1.411 485,9 18,27

Günlük Bülten 12 Ağustos 2021 Piyasalarda Son Görünüm* USD/TL EUR/TRY EUR/USD BIST-100 Gram Altın Gösterge Tahvil 8,6314 10,1510 1,1744 1.411 485,9 18,27 Yurt içinde bugün TCMB faiz kararı takip edilecek Haftalık Getiriler (%) 1,5 1,2 ● TCMB’nin politika faizini sabit tutması bekleniyor 1,0 0,7 0,4 ● ABD’de yıllık enflasyon, %5,4 düzeyinde yatay seyretti 0,5 ● ABD Senatosu, 3,5 trilyon $’lık harcama paketini onayladı 0,0 -0,5 Küresel çapta, ABD'de tüketici fiyatları temmuz ayında aylık bazda -1,0 %0,5 artış gösterdi. Haziran ayında aylık enflasyon %0,9 -1,5 -1,5 düzeyinde gerçekleşmiş idi. Bu temmuz ayı gerçekleşmesi ile, yıllık -2,0 -1,7 enflasyon da %5,4 düzeyinde yatay seyretti. Yıllık çekirdek enflasyon Dolar/TL Euro/TL Gram Altın BIST-100 Gösterge Tahvil ise, %4,5'ten %4,3'e geriledi. ABD‘de özellikle enflasyon ve işgücü piyasasına yönelik veriler, Fed'in varlık alımlarında azaltıma Veriler (Bugün) Önceki Beklenti başlayabileceği tarih açısından kritik öneme sahip. TCMB Faiz Kararı (%) 19,0 19,0 Euro Bölgesi Sanayi Bölgesi ABD Senatosu, Başkan Biden'ın ekonomik reform takviminde -1,0 0,2 (Haziran, aylık % değişim, m.a.) bulunan 3,5 trilyon $ tutarındaki bütçe taslağına 50'ye karşı 49 oy ile onay verdi. Tasarının, ABD hükümetinin sosyal ve çevresel konulara yönelik daha fazla harcama yapmasına imkan tanıyacağı Yatırımcı Takvimi için tıklayınız belirtiliyor. Küresel çapta günlük vaka sayıları 7 günlük ortalamalar Devlet Tahvili Getirileri bazında artış eğilimini sürdürürken, ABD'de ve Avrupa'da, aşı (%) 11/08 10/08 2020 olmayanlara yönelik kısmi zorlayıcı tedbirler yürürlüğe giriyor. -

WOOD's Winter in Prague

emerging europe conference WOOD’s Winter in Prague Tuesday 5 December to Friday 8 December 2017 Please join us for our flagship event - now in its6th year - spanning 4 jam-packed days. We expect to host over 160 companies representing more than 15 countries. Click here & For more information please contact your WOOD sales representative: Tuesday: Energy, Industrials and Materials Register Warsaw +48 222 22 1530 Wednesday: TMT and Utilities Now! Prague +420 222 096 453 Thursday: Consumer, Healthcare and Real Estate London +44 20 3530 7685 Friday: Diversified and Financials [email protected] Invited Companies by country Bolded confirmed Austria Hungary Kruk LUKOIL Aygaz AT & S ANY LPP Luxoft BIM Atrium Budapest Stock Exchange Mabion M.video Bizim Toptan BUWOG Gedeon Richter mBank Magnit Brisa DO&CO Graphisoft Park Medicalgorithmics MMK Cimsa Erste Group Bank MOL Group Orange Polska Moscow Exchange Coca-Cola Icecek Immofinanz OTP Bank Pfleiderer Group Mostotrest Dogus Otomotiv OMV Waberer’s PGE MTS Erdemir PORR Wizz Air PGNiG NLMK Garanti Raiffeisen Bank Iraq PKN Orlen Norilsk Nickel Halkbank Strabag DNO PKO BP NovaTek Is REIT Telekom Austria Genel Energy PKP Cargo O’KEY Isbank Uniqa Kazakhstan PLAY PIK Kardemir Vienna Insurance Group KMG EP Prime Car Management Polymetal International Koc Holding Warimpex Nostrum Oil & Gas PZU Polyus Lokman Hekim Croatia Steppe Cement Synthos Raven Russia Migros Ticaret Podravka Lithuania Tauron Rosneft Otokar Czech Republic Siauliu Bankas Warsaw Stock Exchange Rostelecom Pegasus Airlines CEZ Poland -

I, No:40 Sayılı Tebliği'nin 8'Nci Maddesi Gereğince, Hisse Senetleri

Sermaye Piyasas Kurulu’nun Seri :I, No:40 say l Teblii’nin 8’nci maddesi gereince, hisse senetleri Borsada i"lem gören ortakl klar n Kurul kayd nda olan ancak Borsada i"lem görmeyen statüde hisse senetlerinin Borsada sat "a konu edilebilmesi amac yla Merkezi Kay t Kurulu"u’na yap lan ba"vurulara ait bilgiler a"a da yer almaktad r. Hisse Kodu S ra Sat "a Konu Hisse Ünvan Grubu Yat r mc n n Ad -Soyad Nominal Tutar Tsp Sat " No Ünvan (TL)* 5"lemi K s t ** ** ADANA 1 ADANA Ç5MENTO E TANER BUGAY SANAY55 A.;. A GRUBU 2.235,720 ALTIN 2 ALTINYILDIZ MENSUCAT E 5SMA5L AYÇ5N VE KONFEKS5YON 0,066 FABR5KALARI A.;. ARCLK 3 ARÇEL5K A.;. E C5HAT YÜKSEKEL 31,344 ARCLK 4 ARÇEL5K A.;. E ERSAN OYMAN 19,736 ARCLK 5 ARÇEL5K A.;. E FER5DE SEZ5K 0,214 ARCLK 6 ARÇEL5K A.;. E F5L5Z EYÜPOHLU 209,141 ARCLK 7 ARÇEL5K A.;. E HANDE YED5DAL 28,180 ARCLK 8 ARÇEL5K A.;. E HAYRETT5N YAVUZ 0,206 ARCLK 9 ARÇEL5K A.;. E 5HSAN ERSEN 1.259,571 ARCLK 10 ARÇEL5K A.;. E 5RFAN ATALAY 195,262 ARCLK 11 ARÇEL5K A.;. E KEZ5BAN ONBE; 984,120 ARCLK 12 ARÇEL5K A.;. E RAFET SALTIK 23,514 ARCLK 13 ARÇEL5K A.;. E SELEN TUNÇKAYA 29,110 ARCLK 14 ARÇEL5K A.;. E YA;AR EMEK 1,142 ARCLK 15 ARÇEL5K A.;. E ZEYNEP ÖZDE GÖRKEY 2,351 ARCLK 16 ARÇEL5K A.;. E ZEYNEP SEDEF ELDEM 2.090,880 ASELS 17 ASELSAN ELEKTRON5K E ALAETT5N ÖZKÜLAHLI SANAY5 VE T5CARET A.;. -

TÜRKİYE İŞ BANKASI A.Ş. U.S.$5,000,000,000 Global Medium

TÜRKİYE İŞ BANKASI A.Ş. U.S.$5,000,000,000 Global Medium Term Note Program Under this U.S.$5,000,000,000 Global Medium Term Note Program (the "Program"), Türkiye İş Bankası A.Ş., a Turkish banking institution organized as a public joint stock company registered with the Istanbul Trade Registry under number 431112 (the "Bank" or the "Issuer"), may from time to time issue notes (the "Notes") denominated in any currency agreed between the Issuer and the relevant Dealer (as defined below). Notes may be issued in bearer or registered form (respectively "Bearer Notes" and "Registered Notes"). The maximum aggregate nominal amount of all Notes from time to time outstanding under the Program will not exceed U.S.$5,000,000,000 (or its equivalent in other currencies calculated as described in the Program Agreement described herein), subject to increase as described herein. The Notes may be issued on a continuing basis to: (a) one or more of the Dealers specified under "Overview of the Group and the Program" and any additional Dealer appointed under the Program from time to time by the Issuer (each a "Dealer" and together the "Dealers"), which appointment may be for a specific issue or on an ongoing basis, and/or (b) one or more investors purchasing Notes directly from the Issuer. References in this Base Prospectus to the "relevant Dealer" shall, in the case of an issue of Notes being (or intended to be) subscribed by more than one Dealer, be to all Dealers agreeing to subscribe such Notes. An investment in Notes issued under the Program involves certain risks. -

En-Isbank2009.Pdf

Contents Presentation 1 İşbank at the onset of 2010 2 Turkey’s Bank 4 İşbank since 1924 5 İşbank’s Vision, Objectives, and Strategy 6 Pioneering Activities 7 İşbank’s Financial Indicators and Shareholder Structure 8 Chairman’s Message 12 CEO’s Message 18 İşbank’s transformation journey: Customer Centric Transformation (MOD) 20 The Economic Outlook in 2009 26 İşbank in 2009 49 Subsidiaries 54 Corporate Social Responsibility at İşbank 60 Annual Report Compliance Opinion Management and Corporate Governance at İşbank 62 Board of Directors & Auditors 64 Executive Committee 66 Organization Chart 68 Managers of Internal Systems 68 Information About the Meetings of the Board of Directors 69 İşbank Committees 71 Human Resources Functions at İşbank 72 Information on the Transactions Carried out with İşbank’s Risk Group 72 Activities for which Support Services are Received in Accordance with the Regulation on Procurement of Support Services for Banks and Authorization of Organizations Providing this Service 73 İşbank’s Dividend Distribution Policy 74 Agenda of the Annual General Meeting 75 Report of the Board of Directors 76 Auditors’ Report 77 Dividend Distribution Proposal 78 Corporate Governance Principles Compliance Report Financial Information and Assessment on Risk Management 89 Audit Committee’s Assessments on the Operation of Internal Control, Internal Audit and Risk Management Systems, and Their Activities in the Reported Period 91 Independent Auditors’ Report 92 Unconsolidated Financial Statements 102 Financial Highlights and Key Ratios -

Turkish Airlines Aviation

GENEL-PUBLIC March 8, 2018 Equity Research Turkish Airlines Aviation Company update Europeans are back Strong demand continue to support industry. Turkish Airlines recorded 15.5% YoY O&D pax growth, resulting in overall 8.4% BUY YoY international pax growth in 2017. In the same year, although foreign arrivals to Turkey recovered much by 27.8% YoY almost in Share price: TL17.37 all regions, European arrivals stayed flattish in 2017. Our conversations with Association of Turkish Travel Agencies claimed Target price: TL21.60 that summer bookings from Western Europe has jumped much by 60% YoY for 2018. Furthermore, summer bookings from domestic Expected Events tourist figures jumped to 6 million versus 5 million in previous year. We now estimate Turkish Airlines will carry 42.2 mn international March THY February-18 traffic passenger and 33.1 mn domestic passenger, overall resulting to April, 9th Market traffic results (March) 9.7% YoY passenger growth and improvement of 2.9 ppt in load factor to 82.1% in 2018E vs 79.1% in 2017. Although we revised up our revenue estimate of 2018E much by 6.7%, we cut down EBITDA margin estimate by 1ppt on the back of upward revision in our oil estimates and ex-fuel CASK by 5.9% after 4Q17 results Key Data performing worse than our estimates. Accordingly, we project THY to generate 13.2% revenue and 9.9% EBITDA CAGR over our Ticker THYAO forecast period (2017-2019E). Share price (TL) 17.37 There is still room for improvement on our assumptions. The 52W high (TL) 19.57 shares have gained 10.7% so far this year outperforming the 52W low (TL) 5.38 benchmark BIST 100 index by 9.4 percentage points. -

Market Watch Monday, March 01, 2021 Agenda

Market Watch Monday, March 01, 2021 www.sekeryatirim.com.tr Agenda 01 M onday 02 Tuesday 03 Wednesday 04 Thursday 05 Friday Turkstat, 4Q20 GDP Growth Germany, January TurkStat, February inflation CBRT, February Germany, Janu- retail sales inflation assess- ary factory orders China, February Caixin non-mfg. China, February Caixin mfg. PMI ment Germany, February PMI U.S., February Germany and Eurozone, Febru- unemployment data U.S., jobless non-farm payrolls ary Markit mfg. PMI Germany and Eurozone, Febru- ary Markit non-mfg. PMI claims and unemploy- Eurozone, February ment rate Germany, February CPI CPI Eurozone, February PPI U.S., January factory orders U.S., February U.S., February Markit mfg. PMI U.S., February ADP employment average hourly change earnings U.S., February ISM manufactur- ing index U.S., February Markit non-mfg. PMI U.S., January construction U.S., February ISM non- spending manufacturing index Outlook Major global stock markets closed lower on Friday, amid the rise in US Treasury yields, which has increased concerns over rising inflation and the Fed derailing its currently accommodative policy. Global risk appetite has Volume (mn TRY) BIST 100 relatively weakened, despite Fed Chair Powell’s statements suggesting that inflation was likely to remain below the targeted value, and that the 1.551 major central bank would maintain its current policy. Having moved in 1.518 1.488 parallel to the course of major international stock markets, the BIST100 48.000 1.483 1.471 1.600 also shed 1.13% to close at 1,471.39 on Friday, after a volatile day in 40.000 1.500 trading. -

Market Watch Tuesday, August 08, 2017 Agenda

Market Watch Tuesday, August 08, 2017 www.sekeryatirim.com.tr Agenda 07 Monday 08 Tuesday 09 Wednesday 10 Thursday 11 Friday Germany, June industrial TurkStat, June industrial U.S., June wholesale U.S., jobless claims CBRT, June balance of production production inventories U.S., July PPI payments U.S., July CPI Outlook: Major stock markets have advanced to new highs, and the BIST100 has Volume (mn TRY) BIST 100 also tested new record-highs, closing up 1.1% at 109,781 on Monday. Total trading volume in the market was at TRY 6.6bn. Today, market participants 109.781 will follow TurkStat’s June industrial production release; there are no other 10.000 110.000 108.545 major data announcements. Asian markets have seen mixed trading this 8.000 morning, and the European stock markets are expected to open slightly 107.154 108.000 106.525 down. We expect the BIST to maintain its uptrend in parallel to rising global 6.000 106.147 risk appetite, although we caution that the likelihood of profit taking rises 106.000 after swift upsurges. We expect the BIST to open positively today, refresh- 4.000 4.912 4.958 ing its new record highs. RESISTANCE: 110,000 /111,200 SUP- 5.418 104.000 4.667 2.000 4.667 PORT: 109,100/108,600. 0 102.000 1-Aug 2-Aug 3-Aug 4-Aug 7-Aug Money Market: The Lira was positive yesterday, gaining 0.14% against the USD to close at 3.5295. Additionally, the currency depreciated by 0.07% against the basket composed of $0.50 and €0.50. -

Premailer Middle East 2021

Bonds, Loans Shangri-La Bosphorus, Istanbul & Sukuk Turkey 2021 Turkey’s largest capital markets event www.bondsloansturkey.com 93% 50+ 20% 250+ DIRECTOR LEVEL OR ABOVE REGIONAL & INTERNATIONAL SOVEREIGN, CORPORATE & INDUSTRY EXPERT SPEAKERS BANKS ATTENDED FI BORROWERS Bonds, Loans & Sukuk Turkey has become the meeting point of all important players in finance through the correct mix of its participants, and its reliability with continuity of successful organisations in the last consecutive years Selahattin BİLGEN, IGA Airport PLATINUM SPONSOR GOLD SPONSOR BRONZE SPONSORS WELCOME TO THE ANNUAL MEETING PLACE FOR TURKEY’S FINANCE PROFESSIONALS Bonds, Loans & Sukuk Turkey is the country’s largest capital markets event. It is the only event to combine discussions across the Bond, Loans and Sukuk markets, making it a “must attend” event for the country’s leading CEOs, CFOs and Treasurers. With over 65% of the audience representing issuers and borrowers and over 93% being director level or above, it is the place where live deals are discussed and mandates are won each year. As a speaker, I had a dynamic discussion which was a great experience. Overall, the organisation was great and attracted an invaluable list of attendees. Orhan Kaya, ICBC Turkey SAVE YOURSELF SHOWCASE YOUR INCREASE TIME AND MONEY EXPERTISE IN THE REGION AWARENESS get the attendee list 2 weeks by presenting a case study by taking an exhibition space before the event so you can to a room full of potential and demonstrating your pre-arrange meetings. clients. products and services. WIN MORE INCREASE YOUR BUSINESS BRANDS PRESENCE packages include a number through the numerous of staff passes so you can branding opportunities cover more clients. -

Karabük İli Çevresel Durum Raporu

Sayfa İÇİNDEKİLER No (A)KARABÜK İLİ ÇEVRESEL DURUM DEĞERLENDİRMESİ BÖLÜM I 2 COĞRAFİ KAPSAM 2 1.1 Karabük İli Coğrafi Durumu 3 1.2. Karabük İli Topoğrafyası 4 1.3. İklim 7 1.4. Ormanlar, Çayır ve Meralar 8 BÖLÜM II 9 SU/ATIKSU 9 2.1. SU KAYNAKLARI 9 2.1.1. İçme Suyu Kaynakları ve Barajlar 9 2.1.2. Yeraltı Su Kaynakları 9 2.1.3. Akarsular 9 2.1.4. Göller ve Göletler 10 2.2. SU KAYNAKLARININ KULLANIMI 11 2.3. SU KAYNAKLARININ DURUMU 12 2.3.1. İçme suyu kaynaklarında mevcut durum 12 2.3.2. Akarsularda Mevcut durum 27 2.4. ATIK SU SİSTEMİ, KANALİZASYON 30 2.5. KARABÜK İLİNDE SU KİRLİLİĞİNİN DEĞERLENDİRİLMESİ 37 BÖLÜM III 56 HAVA 56 3.1. ISINMADA KULLANILAN YAKITLAR 56 3.2.KARABÜK İLİ SANAYİ GRUPLANDIRILMASI 56 3.3. TRAFİKTEN KAYNAKLANAN EMİSYONLAR 64 3.4. HAVAYI KİRLETİCİ GAZLAR VE KAYNAKLARI 65 3.5.1. Partikül Madde (PM) ve SO2 Emisyonları 65 3.5. KARABÜK İLİNDE HAVA KİRLİLİĞİNİN DEĞERLENDİRİLMESİ 67 BÖLÜM IV 69 TOPRAK 69 4.1. KARABÜK İLİNDE PESTİSİT KULLANIMI 73 4.2 KARABÜK İLİNDE TOPRAK KİRLİLİĞİNİN DEĞERLENDİRİLMESİ 74 BÖLÜM V 78 ATIKLAR 78 5.1. KATI ATIKLAR 78 5.1.1. Ambalaj Atıkları 78 5.1.2. Tehlikeli Atıklar 81 5.1.3. Tıbbi Atıklar 82 5.1.4. Pil ve Aküler 83 5.1.5. Bitkisel Atık Yağlar 84 5.2 KATI ATIKLARIN DEPOLANMASI 84 5.3 KARABÜK İLİNDEKİ ATIK DURUMU VE DEĞERLENDİRİLMESİ 88 (B) BARTIN İLİ ÇEVRESEL DURUM DEĞERLENDİRMESİ BÖLÜM I 94 COĞRAFİ KAPSAM 94 1.1. -

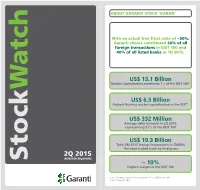

2Q 2015, Representing 21% of the BIST 100

ABOUT GARANTI STOCK ‘GARAN’ With an actual free float ratio of ~50%, Garanti shares constituted 20% of all foreign transactions in BIST 100 and 40% of all listed banks in 1H 2015. US$ 13.1 Billion Market Capitalization constitutes 7% of the BIST 100* Watch US$ 6.5 Billion Highest floating market capitalization in the BIST* US$ 332 Million Average daily turnover in 2Q 2015, representing 21% of the BIST 100 US$ 19.3 Billion Total 6M 2015 foreign transactions in GARAN The most traded stock by foreigners 2Q 2015 INVESTOR RELATIONS Stock ~ 10% Highest weight in the BIST 100 Note: Currency conversion is based on US$/TL CBRT ask rate. * As of June 30, 2015 GARANTI FINANCIAL HIGHLIGHTS Garanti Market Shares* Jun-15 QoQ ∆ In the first half of 2015, Garanti Total Performing Loans 11.8% reached consolidated total TL Loans 10.8% asset of US$ 99.9 billion and FC Loans 14.1% Credit Cards - Issuing (Cumulative) 19.1% consolidated net profit of Credit Cards - Acquiring (Cumulative) 20.4% US$ 777.7 million. Consumer Loans** 14.0% Total Customer Deposits 11.4% TL Customer Deposits 9.3% FC Customer Deposits 14.1% SELECTED FINANCIALS* Customer Demand Deposits 13.5% Mutual Funds 11.0% Total Assets Total Performing Loans * Figures are based on bank-only financials for fair comparison with sector. Sector US$ 99.9 Billion US$ 60.0 Billion figures are based on BRSA weekly data for commercial banks only. ** Including consumer credit cards and other Total Deposits Shareholders’ Equity Garanti with Numbers* US$ 54.7 Billion US$ 10.5 Billion Dec-14 Mar-15 Jun-15 -

2Ç2021 Kar Tahminleri

ARAŞTIRMA BÖLÜMÜ 16 Temmuz 2021 2Ç2021 KAR TAHMİNLERİ BANKACILIK SEKTÖRÜ 2Ç21T/ 2Ç21T/ 6A21T/ Bilanço Net Dönem Karı *Kesin/ 2Ç21T 1Ç21 4Ç20T 3Ç20 2Ç20 1Ç20 2Ç20 1Ç20 6A21T 6A20 6A20 Açıklama (Mn TL) Tahmini Değ.% Değ.% Değ.% Tarihi Finans Akbank 2.036 2.027 1.848 1.523 1.586 1.310 28,3% 0,4% 4.063 2.896 40,3% 28.07.2021 K Garanti Bankası 2.596 2.529 1.111 1.896 1.600 1.631 62,2% 2,6% 5.124 3.231 58,6% 29.07.2021 K İş Bankası (C) 1.739 1.854 1.627 2.149 1.579 1.456 10,2% -6,2% 3.593 3.035 18,4% 6.08.2021 T T. Halk Bankası 65 59 510 315 950 825 -93,1% 10,7% 124 1.775 -93,0% 13.08.2021 T Vakıflar Bankası 635 750 669 1.100 1.525 1.716 -58,3% -15,3% 1.385 3.241 -57,3% 9.08.2021 K Yapı ve Kredi Bank. 1.844 1.453 765 1.854 1.331 1.129 38,5% 26,9% 3.296 2.461 34,0% 30.07.2021 K TSKB 233 226 207 204 168 154 38,2% 3,0% 459 322 42,4% 4.08.2021 T Finans Toplam 9.148 8.897 6.736 9.040 8.740 8.222 4,7% 2,8% 18.045 16.962 6,4% Kaynak: Ziraat Yatırım, Banka Finansalları, T: Tahmini, a.d.: Anlamlı Değil Tahminlerimizde Etkili Olan Faktörler BDDK’nın açıklamış olduğu aylık verilere göre Bankacılık sektörü karı 2021 yılının Nisan-Mayıs döneminde, bir önceki yılın aynı dönemine göre %30,3, bir önceki çeyreğin ilk iki ayına göre de %9,4 oranında düşüş kaydetmiş ve 8,4 milyar TL seviyesinde gerçekleşmiştir.