Minibond Program) DATED DUE Date of Delivery February 15, 2023

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Up to EUR 3,500,000.00 7% Fixed Rate Bonds Due 6 April 2026 ISIN

Up to EUR 3,500,000.00 7% Fixed Rate Bonds due 6 April 2026 ISIN IT0005440976 Terms and Conditions Executed by EPizza S.p.A. 4126-6190-7500.7 This Terms and Conditions are dated 6 April 2021. EPizza S.p.A., a company limited by shares incorporated in Italy as a società per azioni, whose registered office is at Piazza Castello n. 19, 20123 Milan, Italy, enrolled with the companies’ register of Milan-Monza-Brianza- Lodi under No. and fiscal code No. 08950850969, VAT No. 08950850969 (the “Issuer”). *** The issue of up to EUR 3,500,000.00 (three million and five hundred thousand /00) 7% (seven per cent.) fixed rate bonds due 6 April 2026 (the “Bonds”) was authorised by the Board of Directors of the Issuer, by exercising the powers conferred to it by the Articles (as defined below), through a resolution passed on 26 March 2021. The Bonds shall be issued and held subject to and with the benefit of the provisions of this Terms and Conditions. All such provisions shall be binding on the Issuer, the Bondholders (and their successors in title) and all Persons claiming through or under them and shall endure for the benefit of the Bondholders (and their successors in title). The Bondholders (and their successors in title) are deemed to have notice of all the provisions of this Terms and Conditions and the Articles. Copies of each of the Articles and this Terms and Conditions are available for inspection during normal business hours at the registered office for the time being of the Issuer being, as at the date of this Terms and Conditions, at Piazza Castello n. -

Lecture 5 an Introduction to European Put Options. Moneyness

Lecture: 5 Course: M339D/M389D - Intro to Financial Math Page: 1 of 5 University of Texas at Austin Lecture 5 An introduction to European put options. Moneyness. 5.1. Put options. A put option gives the owner the right { but not the obligation { to sell the underlying asset at a predetermined price during a predetermined time period. The seller of a put option is obligated to buy if asked. The mechanics of the European put option are the following: at time−0: (1) the contract is agreed upon between the buyer and the writer of the option, (2) the logistics of the contract are worked out (these include the underlying asset, the expiration date T and the strike price K), (3) the buyer of the option pays a premium to the writer; at time−T : the buyer of the option can choose whether he/she will sell the underlying asset for the strike price K. 5.1.1. The European put option payoff. We already went through a similar procedure with European call options, so we will just briefly repeat the mental exercise and figure out the European-put-buyer's profit. If the strike price K exceeds the final asset price S(T ), i.e., if S(T ) < K, this means that the put-option holder is able to sell the asset for a higher price than he/she would be able to in the market. In fact, in our perfectly liquid markets, he/she would be able to purchase the asset for S(T ) and immediately sell it to the put writer for the strike price K. -

Evidence from SME Bond Markets

Temi di discussione (Working Papers) Asymmetric information in corporate lending: evidence from SME bond markets by Alessandra Iannamorelli, Stefano Nobili, Antonio Scalia and Luana Zaccaria September 2020 September Number 1292 Temi di discussione (Working Papers) Asymmetric information in corporate lending: evidence from SME bond markets by Alessandra Iannamorelli, Stefano Nobili, Antonio Scalia and Luana Zaccaria Number 1292 - September 2020 The papers published in the Temi di discussione series describe preliminary results and are made available to the public to encourage discussion and elicit comments. The views expressed in the articles are those of the authors and do not involve the responsibility of the Bank. Editorial Board: Federico Cingano, Marianna Riggi, Monica Andini, Audinga Baltrunaite, Marco Bottone, Davide Delle Monache, Sara Formai, Francesco Franceschi, Salvatore Lo Bello, Juho Taneli Makinen, Luca Metelli, Mario Pietrunti, Marco Savegnago. Editorial Assistants: Alessandra Giammarco, Roberto Marano. ISSN 1594-7939 (print) ISSN 2281-3950 (online) Printed by the Printing and Publishing Division of the Bank of Italy ASYMMETRIC INFORMATION IN CORPORATE LENDING: EVIDENCE FROM SME BOND MARKETS by Alessandra Iannamorelli†, Stefano Nobili†, Antonio Scalia† and Luana Zaccaria‡ Abstract Using a comprehensive dataset of Italian SMEs, we find that differences between private and public information on creditworthiness affect firms’ decisions to issue debt securities. Surprisingly, our evidence supports positive (rather than adverse) selection. Holding public information constant, firms with better private fundamentals are more likely to access bond markets. Additionally, credit conditions improve for issuers following the bond placement, compared with a matched sample of non-issuers. These results are consistent with a model where banks offer more flexibility than markets during financial distress and firms may use market lending to signal credit quality to outside stakeholders. -

Mortgage-Backed Securities & Collateralized Mortgage Obligations

Mortgage-backed Securities & Collateralized Mortgage Obligations: Prudent CRA INVESTMENT Opportunities by Andrew Kelman,Director, National Business Development M Securities Sales and Trading Group, Freddie Mac Mortgage-backed securities (MBS) have Here is how MBSs work. Lenders because of their stronger guarantees, become a popular vehicle for finan- originate mortgages and provide better liquidity and more favorable cial institutions looking for investment groups of similar mortgage loans to capital treatment. Accordingly, this opportunities in their communities. organizations like Freddie Mac and article will focus on agency MBSs. CRA officers and bank investment of- Fannie Mae, which then securitize The agency MBS issuer or servicer ficers appreciate the return and safety them. Originators use the cash they collects monthly payments from that MBSs provide and they are widely receive to provide additional mort- homeowners and “passes through” the available compared to other qualified gages in their communities. The re- principal and interest to investors. investments. sulting MBSs carry a guarantee of Thus, these pools are known as mort- Mortgage securities play a crucial timely payment of principal and inter- gage pass-throughs or participation role in housing finance in the U.S., est to the investor and are further certificates (PCs). Most MBSs are making financing available to home backed by the mortgaged properties backed by 30-year fixed-rate mort- buyers at lower costs and ensuring that themselves. Ginnie Mae securities are gages, but they can also be backed by funds are available throughout the backed by the full faith and credit of shorter-term fixed-rate mortgages or country. The MBS market is enormous the U.S. -

Pinnacle Notes Frequently Asked Questions 18

PINNACLE NOTES FREQUENTLY ASKED QUESTIONS 18 DECEMBER 20081 These Frequently Asked Questions have been prepared by Pinnacle Performance Limited for the distributors of the Pinnacle notes in Singapore in response to questions about the Pinnacle notes generally. Any questions from investors should be raised with the institution that sold them the Pinnacle notes in Singapore. Please read the important notice at the end of this document. 1. What are the Pinnacle notes? The Pinnacle notes are the Series 1, 2, 3, 5, 6, 7, 8, 9, 10, 11, 12, 15 and 16 notes issued by Pinnacle Performance Limited (the "Issuer"). Some of the Pinnacle notes are equity- linked notes and some are credit-linked notes. The Pinnacle equity-linked notes and the Pinnacle credit-linked notes are together referred to in this document as the "Pinnacle notes". 2. What are the Pinnacle equity-linked notes? The Pinnacle equity-linked notes (the "Pinnacle equity-linked notes") are the Series 8, 11, 12, 15 and 16 notes issued by the Issuer. An equity-linked note is, in general terms, a structured note where the return and/or interest on the note is determined by reference to, amongst other things, the performance of one or more shares or share indices. Investors in a Series of Pinnacle equity-linked notes should also refer to the Frequently Asked Questions in relation to Pinnacle equity-linked notes dated 14 November 2008 for further information. A copy of these Frequently Asked Questions is available on the website referred to in the important notice below. 3. What are the Pinnacle credit-linked notes? The Pinnacle credit-linked notes (the "Pinnacle credit-linked notes") are the Series 1, 2, 3, 5, 6, 7, 9 and 10 notes issued by the Issuer. -

The Promise and Peril of Real Options

1 The Promise and Peril of Real Options Aswath Damodaran Stern School of Business 44 West Fourth Street New York, NY 10012 [email protected] 2 Abstract In recent years, practitioners and academics have made the argument that traditional discounted cash flow models do a poor job of capturing the value of the options embedded in many corporate actions. They have noted that these options need to be not only considered explicitly and valued, but also that the value of these options can be substantial. In fact, many investments and acquisitions that would not be justifiable otherwise will be value enhancing, if the options embedded in them are considered. In this paper, we examine the merits of this argument. While it is certainly true that there are options embedded in many actions, we consider the conditions that have to be met for these options to have value. We also develop a series of applied examples, where we attempt to value these options and consider the effect on investment, financing and valuation decisions. 3 In finance, the discounted cash flow model operates as the basic framework for most analysis. In investment analysis, for instance, the conventional view is that the net present value of a project is the measure of the value that it will add to the firm taking it. Thus, investing in a positive (negative) net present value project will increase (decrease) value. In capital structure decisions, a financing mix that minimizes the cost of capital, without impairing operating cash flows, increases firm value and is therefore viewed as the optimal mix. -

Straddles and Strangles to Help Manage Stock Events

Webinar Presentation Using Straddles and Strangles to Help Manage Stock Events Presented by Trading Strategy Desk 1 Fidelity Brokerage Services LLC ("FBS"), Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917 690099.3.0 Disclosures Options’ trading entails significant risk and is not appropriate for all investors. Certain complex options strategies carry additional risk. Before trading options, please read Characteristics and Risks of Standardized Options, and call 800-544- 5115 to be approved for options trading. Supporting documentation for any claims, if applicable, will be furnished upon request. Examples in this presentation do not include transaction costs (commissions, margin interest, fees) or tax implications, but they should be considered prior to entering into any transactions. The information in this presentation, including examples using actual securities and price data, is strictly for illustrative and educational purposes only and is not to be construed as an endorsement, or recommendation. 2 Disclosures (cont.) Greeks are mathematical calculations used to determine the effect of various factors on options. Active Trader Pro PlatformsSM is available to customers trading 36 times or more in a rolling 12-month period; customers who trade 120 times or more have access to Recognia anticipated events and Elliott Wave analysis. Technical analysis focuses on market action — specifically, volume and price. Technical analysis is only one approach to analyzing stocks. When considering which stocks to buy or sell, you should use the approach that you're most comfortable with. As with all your investments, you must make your own determination as to whether an investment in any particular security or securities is right for you based on your investment objectives, risk tolerance, and financial situation. -

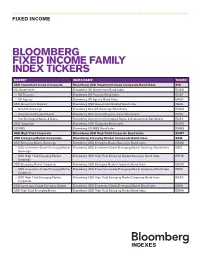

Bloomberg Fixed Income Family Index Tickers

///////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////// FIXED INCOME BLOOMBERG FIXED INCOME FAMILY INDEX TICKERS MARKET INDEX NAME TICKER USD Investment Grade Composite Bloomberg USD Investment Grade Composite Bond Index BIG US Government Bloomberg US Government Bond Index BUSG » US Treasury Bloomberg US Treasury Bond Index BUSY » US Agency Bloomberg US Agency Bond Index BAGY USD Government Related Bloomberg USD Government Related Bond Index BGRL » Non-US Sovereign Bloomberg Non-US Sovereign Bond Index BNSO » Government Regional/Local Bloomberg Government Regional/Local Bond Index BRGL » Gov Developed Banks & Supra Bloomberg Government Developed Banks & Supranational Bond Index BDEV USD Corporate Bloomberg USD Corporate Bond Index BUSC US MBS Bloomberg US MBS Bond Index BMBS USD High Yield Corporate Bloomberg USD High Yield Corporate Bond Index BUHY USD Emerging Market Composite Bloomberg Emerging Market Composite Bond Index BEM USD Emerging Market Sovereign Bloomberg USD Emerging Market Sovereign Bond Index BEMS » USD Investment Grade Emerging Market Bloomberg USD Investment Grade Emerging Market Sovereign Bond Index BEIS Sovereign » USD High Yield Emerging Market Bloomberg USD High Yield Emerging Market Sovereign Bond Index BEHS Sovereign USD Emerging Market Corporate Bloomberg USD Emerging Market Corporate Bond Index BEMC » USD Investment Grade Emerging Market Bloomberg USD Investment Grade Emerging Market Corporate Bond Index BIEM Corporate -

Derivative Securities

2. DERIVATIVE SECURITIES Objectives: After reading this chapter, you will 1. Understand the reason for trading options. 2. Know the basic terminology of options. 2.1 Derivative Securities A derivative security is a financial instrument whose value depends upon the value of another asset. The main types of derivatives are futures, forwards, options, and swaps. An example of a derivative security is a convertible bond. Such a bond, at the discretion of the bondholder, may be converted into a fixed number of shares of the stock of the issuing corporation. The value of a convertible bond depends upon the value of the underlying stock, and thus, it is a derivative security. An investor would like to buy such a bond because he can make money if the stock market rises. The stock price, and hence the bond value, will rise. If the stock market falls, he can still make money by earning interest on the convertible bond. Another derivative security is a forward contract. Suppose you have decided to buy an ounce of gold for investment purposes. The price of gold for immediate delivery is, say, $345 an ounce. You would like to hold this gold for a year and then sell it at the prevailing rates. One possibility is to pay $345 to a seller and get immediate physical possession of the gold, hold it for a year, and then sell it. If the price of gold a year from now is $370 an ounce, you have clearly made a profit of $25. That is not the only way to invest in gold. -

Options Glossary of Terms

OPTIONS GLOSSARY OF TERMS Alpha Often considered to represent the value that a portfolio manager adds to or subtracts from a fund's return. A positive alpha of 1.0 means the fund has outperformed its benchmark index by 1%. Correspondingly, a similar negative alpha would indicate an underperformance of 1%. Alpha Indexes Each Alpha Index measures the performance of a single name “Target” (e.g. AAPL) versus a “Benchmark (e.g. SPY). The relative daily total return performance is calculated daily by comparing price returns and dividends to the previous trading day. The Alpha Indexes were set at 100.00 as of January 1, 2010. The Alpha Indexes were created by NASDAQ OMX in conjunction with Jacob S. Sagi, Financial Markets Research Center Associate Professor of Finance, Owen School of Management, Vanderbilt University and Robert E. Whaley, Valere Blair Potter Professor of Management and Co-Director of the FMRC, Owen Graduate School of Management, Vanderbilt University. American- Style Option An option contract that may be exercised at any time between the date of purchase and the expiration date. At-the-Money An option is at-the-money if the strike price of the option is equal to the market price of the underlying index. Benchmark Component The second component identified in an Alpha Index. Call An option contract that gives the holder the right to buy the underlying index at a specified price for a certain fixed period of time. Class of Options Option contracts of the same type (call or put) and style (American or European) that cover the same underlying index. -

Chapter 3 Fixed Income Securities

Chapter 3 Fixed Income Securities Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. • Fixed-income securities. • Stocks. • Real assets (capital budgeting). Part C Determination of risk-adjusted discount rates. Part D Introduction to derivatives. Main Issues • Fixed-Income Markets • Term Structure of Interest Rates • Interest Rate Risk • Inflation Risk • Credit Risk Chapter 3 Fixed Income Securities 3-1 1 Fixed-Income Markets Definition: Fixed-income securities are financial claims with promised cash flows of fixed amount paid at fixed dates. Classification of Fixed-Income Securities: 1. Treasury Securities: • U.S. Treasury securities (bills, notes, bonds). • Bunds, JGBs, U.K. Gilts ... 2. Federal Agency Securities: • Securities issued by federal agencies (FHLB, FNMA ...). 3. Corporate Securities: • Commercial paper. • Medium-term notes (MTNs). • Corporate bonds ... 4. Municipal Securities. 5. Mortgage-Backed Securities. 6. ... Fall 2006 c J. Wang 15.401 Lecture Notes 3-2 Fixed Income Securities Chapter 3 Overview of Fixed-income Markets Composition of U.S. Debt Markets (2005) Market value % (in trillion dollars) Treasury 4.17 16.5 Corporate 4.99 19.7 Mortgage 5.92 23.4 Agency 2.60 10.3 Munies 2.23 8.8 Asset-Backed 1.96 7.7 Money Market 3.47 13.7 Total 25.33 Current Trends T. Corp. MBS Agency ABS Munies MM Total 1995 3.31 1.94 2.35 0.84 0.32 1.29 1.18 11.23 1996 3.44 2.12 2.49 0.93 0.40 1.30 1.39 12.01 1997 3.44 2.36 2.68 1.02 0.54 1.32 1.69 13.05 1998 3.34 2.71 2.96 1.30 0.73 1.40 1.98 14.42 1999 3.27 3.05 3.33 1.62 0.90 1.46 2.34 15.96 2000 2.95 3.36 3.56 1.85 1.07 1.48 2.66 16.95 2001 2.97 3.84 4.13 2.15 1.28 1.60 2.57 18.53 2002 3.20 4.09 4.70 2.29 1.54 1.73 2.55 20.15 2003 3.57 4.46 5.31 2.64 1.69 1.89 2.53 22.10 2004 3.94 3.70 5.47 2.75 1.83 2.02 2.87 23.58 2005 4.17 4.99 4.92 2.60 1.96 2.23 3.47 25.33 15.401 Lecture Notes c J. -

Managing Fixed Income Late in the Credit Cycle: Navigating the Path Forward

INCOME INVESTING Managing fixed income late in the credit cycle: navigating the path forward nuveen knows Highlights • While we are clearly in the late stage of the credit cycle, we don’t think a recession is imminent and believe investors should feel comfortable investing in credit 2Q19 markets throughout the rest of 2019. • We believe investors should focus on higher-quality issues with improving credit fundamentals, while seeking to diversify across industries and geographies. • Nuveen’s sector specialist teams are finding attractive opportunities in U.S. credit sectors, including high yield, but they are increasingly diversifying into other higher-income areas, such as emerging market debt and leveraged loans. • Active management can add value in any environment, but we believe it is especially beneficial at the current stage of the credit cycle. The multi-trillion-dollar question for investors: How late are we in the credit cycle, and what are the portfolio implications? That’s the question we most often hear from our clients. And while there are few certainties in life or markets, we feel confident in our answer: We are clearly in the late stage of the credit cycle. But “late” doesn’t mean “done,” and credit cycles don’t die of old age. Rather, a combination of fundamentals and sentiment bring about their demise, and even in their later stages, savvy investors can find opportunities not only to protect their investments, but to position their portfolios for an emphasis on income as the cycle turns. Nuveen believes most investors should be comfortable investing in the credit markets throughout the rest of 2019.