Case Studies of Two Alternative to Roading Projects

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Powerco CPP – Portfolio Overview Document

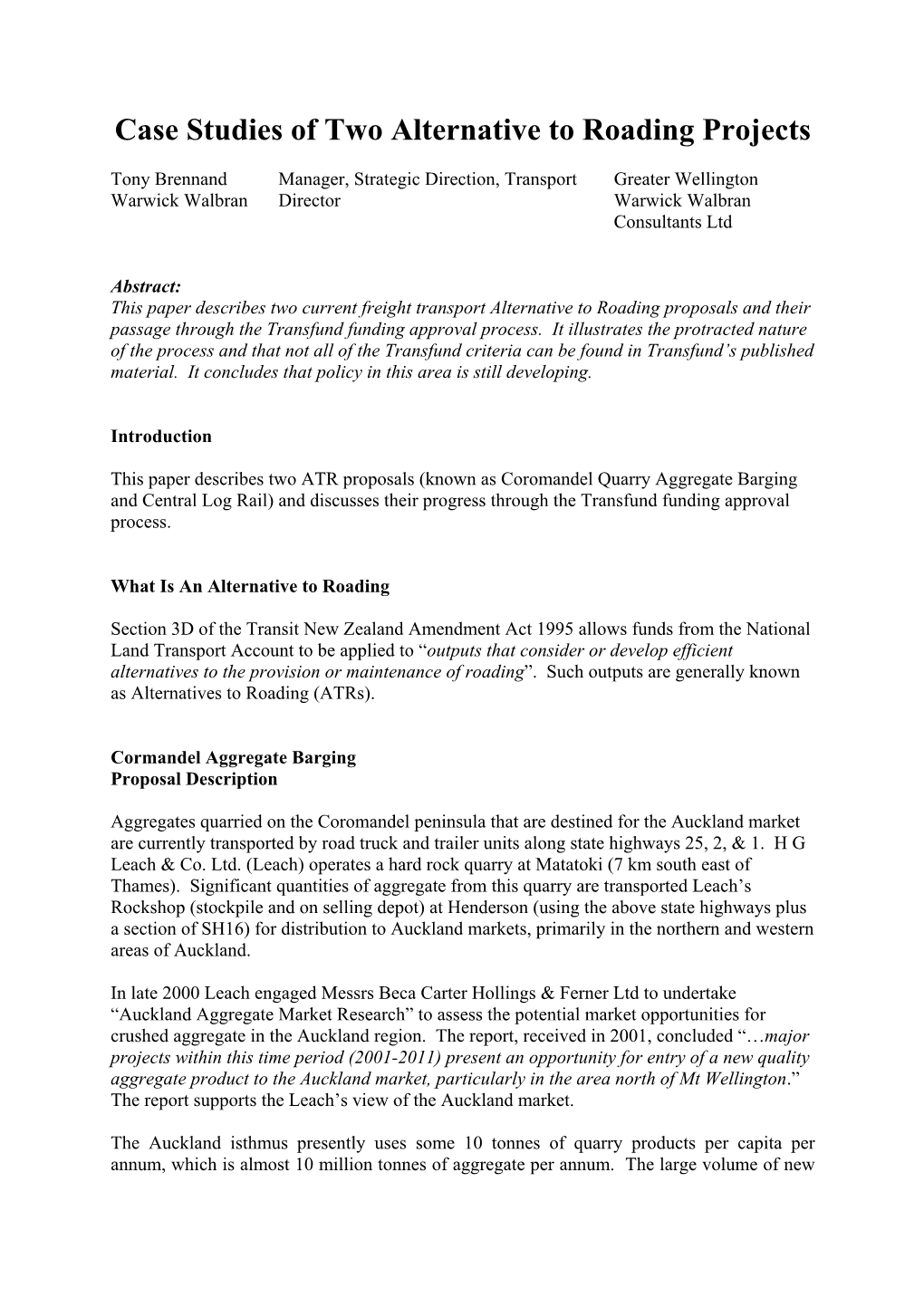

POD G14 Kaimarama-Whitianga Sub-transmission Enhancement Powerco CPP – Portfolio Overview Document Kaimarama – Whitianga Sub-transmission Portfolio Name Enhancement Expenditure Class Capex Expenditure Category Growth & Security As at Date 12 June 2017 CPP Period Project Expenditure Forecast 1,2 Pre CPP FY19 FY20 FY21 FY22 FY23 Post CPP Total Total Pre-Internal Cost Capitalisation and Efficiency Adjustments 3 $0.0 $0.2 $0.2 $1.3 $2.0 $2.2 $0.0 $5.9 $5.9 (2016 Constant NZ$(M)) Post-Internal Cost Capitalisation and Efficiency Adjustments $0.0 $0.2 $0.2 $1.4 $2.1 $2.2 $0.0 $6.1 $6.1 (2016 Constant NZ$(M)) Description The 66kV subtransmission network that supplies Whitianga, Coromandel (and Tairua under contingency) cannot meet Powerco security of Project need overview supply standards due to capacity constraints during high load periods. Coromandel is supplied on a spur off a hard tee connection at Kaimarama and does not have its own dedicated 66kV supply circuit. Historically, the area has always been exposed to long duration outages particularly during extreme weather conditions. Proposed solution Powerco propose to install a new, ≈4km, 110kV-capable underground cable between Kaimarama & Whitianga on road reserve of State Project solution overview Highway 25. This will resolve the capacity constraint between Kaimarama and Whitianga supplying load to the three substations. It will also create a new dedicated 66kV circuit for Coromandel through the removal of the hard tee connection at Kaimarama. The existing 66kV bus 1 Forecast expenditure is based on Powerco’s financial year (i.e. FY19 is for the period April 2018 through March 2019). -

Annual Report DRAFT

2014/2015 Annual Report DRAFT Unaudited Version Table of Contents Message from the mayor Introduction Your Council - Mayor and Elected Members 5 Community Development Activity Group 85 What is the Annual Report 6 Economic Development Activity 88 Council's Vision, Values and Outcomes 7 Social Development Activity 91 Performance Overview Stormwater Activity Group 94 Highlights from the Thames Community Board Stormwater Activity 96 Area 10 Land Drainage Activity 97 Highlights from the Coromandel/Colville Wastewater Activity Group 99 Community Board Area 12 Wastewater Activity 102 Highlights from the Mercury Bay Community Land Use Activity Group 105 Board Area 13 Land Use Management Activity 107 Highlights from the Tairua/Pauanui Community Board Area 14 LIMS Activity 109 Highlights from the Whangamata Community Natural and Cultural Heritage Activity 111 Board Area 15 Water Supply Activity Group 113 Overview of Our Financial Performance 17 Water Supply Activity 115 Independent Auditor’s Report 23 Solid Waste Activity Group 119 Our services Solid Waste Activity 121 Introduction 29 Financial Statements Community Leadership Activity Group 33 Guide to Financial Statements 126 District Leadership Activity 34 Statement of Compliance 128 Local Advocacy 37 Statement of Comprehensive Revenue and Planning for the Future Activity Group 39 Expense 129 Strategic Planning Activity 41 Statement of Financial Position 130 Land Use Planning Activity 43 Statement of Changes in Equity 131 Hazard Management Activity 45 Statement of Cash Flows 132 Healthy and Safe -

Saving the Old Kopu Bridge

Saving the Old Kopu Bridge Business Management Plan 2016 Thames Heritage Festival Open Day 13 March 2016. Sereena Burton photo A Bridge to the Future Promoting heritage protection, tourism and prosperity Local icon Cycleway link Tourism feature Transport history Engineering history International significance Presented by the Historic Kopu Bridge Society May 2016 Table of Contents 1 Executive Summary ............................................................................................................ 4 2 Letters of Support ............................................................................................................... 5 3 Introduction ...................................................................................................................... 17 3.1 Purpose...................................................................................................................... 17 3.2 Why the Kopu Bridge matters to all of us ................................................................. 17 3.3 Never judge a book by its cover!............................................................................... 18 4 Old Kopu Bridge ................................................................................................................ 19 4.1 Historical Overview ................................................................................................... 19 4.2 Design ........................................................................................................................ 21 5 Future of the -

5 Day Pacific Coast Highway Highlights of the Trip

5 Day Pacific Coast Highway The Journey The Pacific Coast Highway offers you spectacular views along the east coast of New Zealand's North Island. It links the Coromandel, Bay of Plenty & Whakatane and Eastland with Auckland in the north and Hawke's Bay in the south. You’ll find it easy to navigate along the Pacific Coast Highway as it is well signposted. You can take in memorable experiences such as the sunrise over the Pacific Ocean, with the sun’s rays casting over the superb white sand beaches that stretch along the highway. If you are a wine buff or foodie, your senses will be overloading with some of the world's best seafood, innovative cuisine and award winning wines on offer. While in the Coromandel, take the time to enjoy a maui winery haven at Mercury Bay Winery and wake up amongst the vines. The regions you will travel through also have plenty of cultural highlights including buildings from another era and ancient Maori pa sites. The arts are also alive in this vibrant region, with talented local artists’ work on display. *PLEASE note that campervan drop off location for this route is Auckland Highlights of the trip Cathedral Cove Hot Water Beach East Cape Tairawhiti Museum Hawke's Bay Day 1 Auckland to Coromandel Town There are two routes to Thames. The fast way whisks you along the motorway and over the Bombay Hills, then across the serene, green Hauraki Plains to Waitakaruru. The slower, scenic route winds Distance: through farmland to the village of Clevedon before leading you around the edge of the Firth of Thames. -

Monday 24Th June 2019

SCHOOL WEEKLY NEWSLETTER: - Monday 24th June 2019 Kia ora koutou katoa, With only two weeks to go until the end of term two we still have lots to finish before the break. This Friday we have our senior Rippa team heading to Hamilton for the Waikato Triangular Tournament, two teams will be heading to Paeroa College for the Ki O Rahi and Tapuwae tournament and our Junior Epro 8 team will head to Katikati College for the finals series. Good luck to all participants, remember to play hard, play fair and represent your school and yourself with mana. Tomorrow we take on Matatoki School at basketball. This is a fun game organised for both schools to build relationships and friendly competition amongst each other. Kia kaha! As you are aware the teachers are currently voting to either accept or reject the governments latest collective agreement offer. Voting closes tomorrow. We are hoping to report a positive conclusion to this continuing dispute. I can confirm we have had our annual school audit of accounts and am happy to report that the annual financial statements presented fairly, this means they were free of misstatement or fraud and that there was no risk. Thank You A big thank you to Steve Walmsley for helping with the new ropes that have been added to the maypole. Kids are enjoying having this back in action. Three Way Conferences Thursday 4th July A letter has been sent home today to remind you about the three-way conferences. A chance for your child to share their learning with you. -

Roamtraveladventures.Com Sat 05 Mar AUCKLAND

a guided adventure for active women Sat 05 Mar AUCKLAND - THAMES Our adventure starts this morning, with a pickup at Auckland Airport (please arrive by 10.30am) before journeying south across the Bombay Hills and on to Miranda for a spot of bird-watching. The Firth of Thames offers migratory wading birds a massive 8,500 hectares of wide inter-tidal flats and attracts thousands of birds each year. Some fly all the way from the Arctic circle whilst others fly up from the braided rivers of the South Island. There are some easy walking tracks through the mud-flats and an interesting Information Centre where we can eat a picnic lunch whilst learning about this amazing natural occurrence. Our first two nights will be spent in the southwestern end of the Coromandel Peninsula in the town of Thames. Surrounded by impressive bush-clad ranges and the Firth of Thames, a heritage rich in gold and kauri and some interesting shops to poke around in. After dinner we will take a stroll along the foreshore and hopefully witness one of Thames’ legendary sunsets (weather permitting of course!) Sun 06 Mar THAMES Today we will explore the township with a local guide taking in the historic buildings and landscape. There will also be time to enjoy some of the shorter walking tracks near Thames. Native bush, Kauri forests, the singsong of birds, chattering crickets, gold mining history, tunnels and scenery awaits us. Later relax by the pool at our accommodation. Mon 07 Mar HAHEI – WHITIANGA We say haere ra to Thames and begin our circumnavigation of the Coromandel Peninsula. -

New Zealand Council Future Proofs Network with A10 ADC Appliances

CASE STUDY New Zealand Council Future Proofs Network with A10 ADC Appliances Company • Thames-Coromandel District Council (TCDC) “A10’s unique Application Delivery Partition (ADP) feature has been highly Industry beneficial, allowing us to utilise their device as load-balancer on our LAN, • Government as well as being a perimeter device.“ Critical Issues Shiv Singh • A district council in New Zealand in need of Thames-Council District Council upgrading an old load balancing solution, Networking Engineer which was unable to meet increasing demands and support new services, causing worries about performance, security, and The Thames-Coromandel District Council (TCDC) in the North Island of New Zealand is overall manageability. seated in the town of Thames. It is located in the region around the Firth of Thames and Selection Criteria Coromandel Peninsula, to the southeast of Auckland. It is the first District council to be • High performance that can manage formed in New Zealand, being constituted in 1975. As of June 2012 the population of the growing traffic volumes to ensure TCDC district is estimated at 27,000. availability and performance of mission- Thames-Coromandel District Council (TCDC) in New Zealand has created a fast, reliable future- critical online services proofed network for interacting with and servicing its various communities. The main drivers • Success of the proof of concept (POC) of this efficient technology are two application delivery controllers from A10 Networks, whose proving the A10 ADCs’ ability to quickly integrate into the existing network benefits include enabling Council’s web pages to load five times faster than before. environment Situation Results TCDC manages social, economic, cultural and environmental matters for a diverse • Quick and efficient deployment due to the community on the East Coast of New Zealand’s North Island. -

Information Sheet on EAA Flyway Network Sites

Information Sheet on EAA Flyway Network Sites Information Sheet on EAA Flyway Network Sites (SIS) – 2013 version Available for download from http://www.eaaflyway.net/nominating-a-site.php#network Categories approved by Second Meeting of the Partners of the East Asian-Australasian Flyway Partnership in Beijing, China 13-14 November 2007 - Report (Minutes) Agenda Item 3.13 Notes for compilers: 1. The management body intending to nominate a site for inclusion in the East Asian - Australasian Flyway Site Network is requested to complete a Site Information Sheet. The Site Information Sheet will provide the basic information of the site and detail how the site meets the criteria for inclusion in the Flyway Site Network. 2. The Site Information Sheet is based on the Ramsar Information Sheet. If the site proposed for the Flyway Site Network is an existing Ramsar site then the documentation process can be simplified. 3. Once completed, the Site Information Sheet (and accompanying map(s)) should be submitted to the Flyway Partnership Secretariat. Compilers should provide an electronic (MS Word) copy of the Information Sheet and, where possible, digital versions (e.g. shapefile) of all maps. ------------------------------------------------------------------------------------------------------------------------------ 1. Name and contact details of the compiler of this form: Full name: KEITH WOODLEY EAAF SITE CODE FOR OFFICE USE ONLY: Institution/agency: Pukorokoro Miranda Naturalists’ Trust Address : 283 East Coast Road RD3 Pokeno 2473 E A A F 0 1 9 Telephone:09 2322781 Fax numbers: E-mail address:[email protected] 2. Date this sheet was completed: October 2014 1 Information Sheet on EAA Flyway Network Sites 3. -

Ramsar Wetlands Information Sheet

RAMSAR WETLANDS INFORMATION SHEET 1. Country: New Zealand 2. Date: 20 November 1991 3. Ref: NZ005 4. Name and Address of Compiler: Helen Neale, Conservation Officer, Department of Conservation, Private Bag 3072, Hamilton, NEW ZEALAND. 5. Name of Wetland: FIRTH OF THAMES 6. Date of Ramsar Designation: 29 January 1990 7. Geographical Co-ordinates: 175°23'E 037°13'S 8. General Location: (e.g administrative region and nearest large town.) Located approximately 52km south east of Auckland in the North Island at the northern boundary (direct line). 9. Area: (in hectares) 7800 hectares approximately. 10. Wetland Type: (see attached classification, alos approved by Montreux Rec. C.4.7) A B D E F G H I J Q 11. Altitude: (average and/or maximum and minimum) -1.1 to 2.1 m from mean sea level. 12. Overview: (general summary, in two or three sentences of the wetlands's principle characteristics) The Firth of Thames is an internationally important feeding ground for up to 25,000 birds at any one time, most of which are migratory. The Firth is one of New Zealand's three most important coastal stretches for wading birds and is listed as a wetland of international importance under the Ramsar Convention. 13. Physical Features:(e.g. geology; geomorphology; origins - natural or artificial; hydrology; soil type; water quality; water depth; water permanence; fluctuations in water level; tidal variations; catchment area; downstream area; climate) The Firth of Thames lies in the northern part of the Hauraki graben bounded by fault lines along the Hunua and Coromandel ranges. -

Coromandel Town Whitianga Hahei/Hotwater Tairua Pauanui Whangamata Waihi Paeroa

Discover that HOMEGROWN in ~ THE COROMANDEL good for your soul Produce, Restaurants, Cafes & Arts moment OFFICIAL VISITOR GUIDE REFER TO CENTRE FOLDOUT www.thecoromandel.com Hauraki Rail Trail, Karangahake Gorge KEY Marine Reserve Walks Golf Course Gold Heritage Fishing Information Centres Surfing Cycleway Airports Kauri Heritage Camping CAPE COLVILLE Fletcher Bay PORT JACKSON COASTAL WALKWAY Stony Bay MOEHAU RANGE Sandy Bay Fantail Bay PORT CHARLES HAURAKI GULF Waikawau Bay Otautu Bay COLVILLE Amodeo Bay Kennedy Bay Papa Aroha NEW CHUM BEACH KUAOTUNU Otama Shelly Beach MATARANGI BAY Beach WHANGAPOUA BEACH Long Bay Opito Bay COROMANDEL Coromandel Harbour To Auckland TOWN Waitaia Bay PASSENGER FERRY Te Kouma Te Kouma Harbour WHITIANGA Mercury Bay Manaia Harbour Manaia 309 Cooks Marine Reserve Kauris Beach Ferry CATHEDRAL COVE Landing HAHEI COROMANDEL RANGE Waikawau HOT WATER COROGLEN BEACH 25 WHENUAKITE Orere 25 Point TAPU Sailors Grave Rangihau Square Valley Te Karo Bay WAIOMU Kauri TE PURU TAIRUA To Auckland Pinnacles Broken PAUANUI 70km KAIAUA Hut Hills Hikuai DOC PINNACLES Puketui Tararu Info WALK Shorebird Coast Centre Slipper Island 1 FIRTH (Whakahau) OF THAMES THAMES Kauaeranga Valley OPOUTERE Pukorokoro/Miranda 25a Kopu ONEMANA MARAMARUA 25 Pipiroa To Auckland Kopuarahi Waitakaruru 2 WHANGAMATA Hauraki Plains Maratoto Valley Wentworth 2 NGATEA Mangatarata Valley Whenuakura Island 25 27 Kerepehi Hikutaia Kopuatai HAURAKI 26 Waimama Bay Wet Lands RAIL TRAIL Whiritoa To Rotorua/ Netherton Taupo PAEROA Waikino Mackaytown WAIHI 2 OROKAWA -

Coromandel Harbour the COROMANDEL There Are Many Beautiful Places in the World, Only a Few Can Be Described As Truly Special

FREE OFFICIAL VISITOR GUIDE www.thecoromandel.com Coromandel Harbour THE COROMANDEL There are many beautiful places in the world, only a few can be described as truly special. With a thousand natural hideaways to enjoy, gorgeous beaches, dramatic rainforests, friendly people and fantastic fresh food The Coromandel experience is truly unique and not to be missed. The Coromandel, New Zealanders’ favourite destination, is within an hour and a half drive of the major centres of Auckland and Hamilton and their International Airports, and yet the region is a world away from the hustle and bustle of city life. Drive, sail or fly to The Coromandel and bunk down on nature’s doorstep while catching up with locals who love to show you why The Coromandel is good for your soul. CONTENTS Regional Map 4 - 5 Our Towns 6 - 15 Our Region 16 - 26 Walks 27 - 32 3 On & Around the Water 33 - 40 Other Activities 41 - 48 Homegrown Cuisine 49 - 54 Tours & Transport 55 - 57 Accommodation 59 - 70 Events 71 - 73 Local Radio Stations 74 DISCLAIMER: While all care has been taken in preparing this publication, Destination Coromandel accepts no responsibility for any errors, omissions or the offers or details of operator listings. Prices, timetables and other details or terms of business may change without notice. Published Oct 2015. Destination Coromandel PO Box 592, Thames, New Zealand P 07 868 0017 F 07 868 5986 E [email protected] W www.thecoromandel.com Cover Photo: Northern Coromandel CAPE COLVILLE Fletcher Bay PORT JACKSON Stony Bay The Coromandel ‘Must Do’s’ MOEHAU RANG Sandy Bay Fantail Bay Cathedral Cove PORT CHARLES Hot Water Beach E The Pinnacles Karangahake Gorge Waik New Chum Beach Otautu Bay Hauraki Rail Trail Gold Discovery COLVILLE plus so much more.. -

Shaw Cup & Fleming Shield Tournament

THAMES VALLEY RUGBY FOOTBALL UNION SHAW CUP & FLEMING SHIELD 2021 Aim: To provide an opportunity for as many Year 8 and below students as possible to experience the enjoyment of rugby and to play in a tournament under specific rules and conditions. Dates: Saturday 31st July – Rhodes Park, Thames. Saturday 7th August – Sports Park, Whitianga. Saturday 21st August – Boyd Park, Te Aroha. Grades: There will be two grades of competition: • Shaw Cup (Year 7 and below students) • Fleming Shield (Year 8 and below students) Only one team may be entered in each grade from the regions listed below of the Thames Valley Rugby Football Union (TVRFU) Inc. The Year Groups specified for each competition must be met by ALL players on the official date of the first day. Shaw Cup - Player eligibility: • Must be a Year 7 or below Student as of the 1st January 2021. • There are NO Secondary School Students eligible to play. • There is NO weight limit. • Must attend a school located within the TVRFU Provincial Boundaries or are registered before the 3rd July 2021 to a club affiliated to the Thames Valley Rugby Football Union. • Any player attending Thames Valley Schools that play Hockey, Soccer, Netball, Rugby league etc. are eligible to play in the Shaw Cup and Fleming Shield Tournament. Fleming Shield - Player eligibility: • Must be a Year 8 or below Student as of the 1st January 2021. • There are NO Secondary School Students eligible to play. • There is NO weight limit. • Must attend a school located within the TVRFU Provincial Boundaries or are registered before the 3rd July 2021 to a club affiliated to the Thames Valley Rugby Football Union.