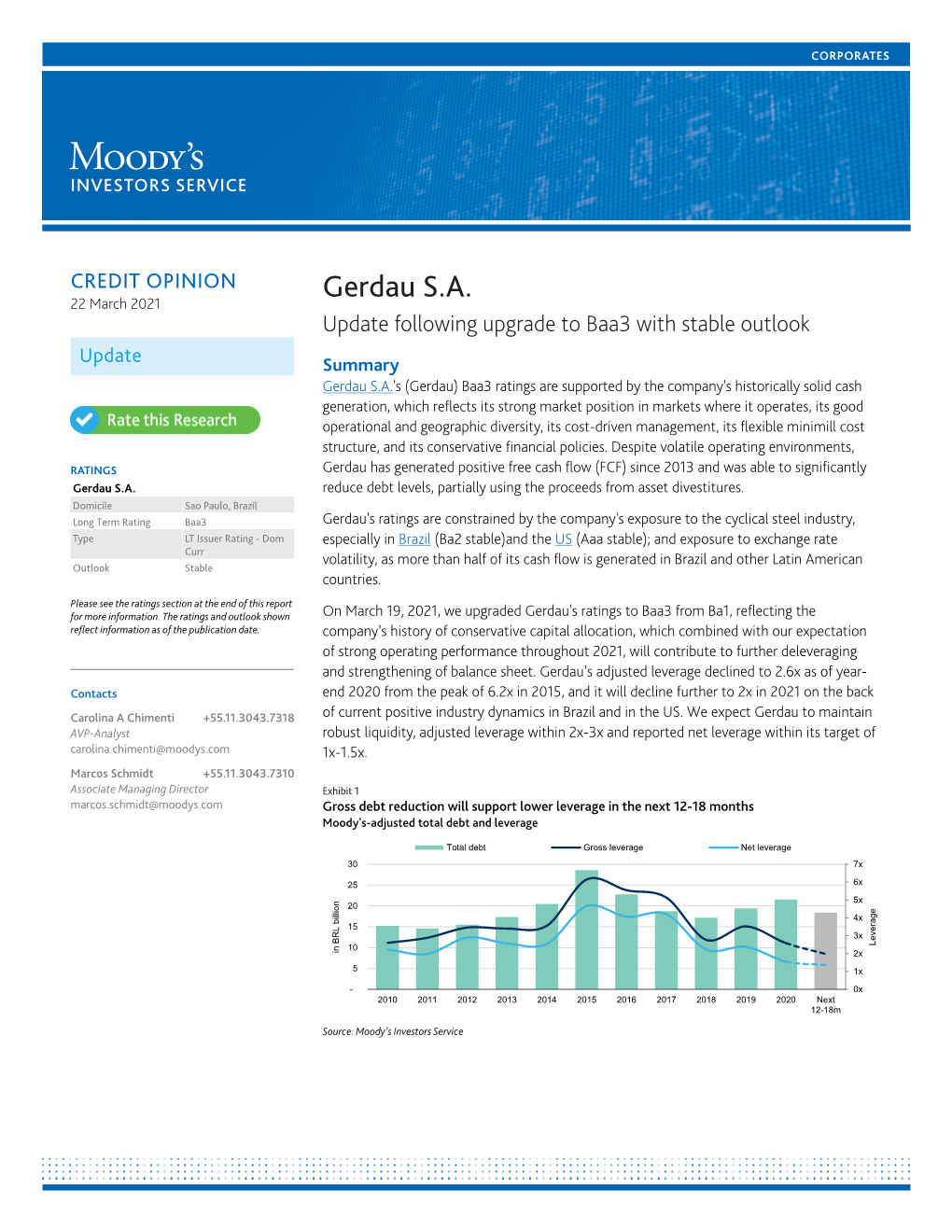

Gerdau S.A. 22 March 2021 Update Following Upgrade to Baa3 with Stable Outlook

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Integrated Report 2020

ABOUT THIS MATERIAL Contact channels Questions, suggestions or comments about this publication can be made on the Investor Relations website at (www.banco.bradesco/ri) or sent via email: [email protected] We can also be found on social networks: Facebook Instagram Linkedin YouTube Twitter ABOUT THIS MATERIAL Contents Message from the Chairman of the Board of Directors 6 Message from the CEO 8 2020 in Figures 10 Performance during Covid-19 16 About this Material 20 Materiality 22 Our DNA 24 Our Strategic Positioning 26 Business Model 30 Much more than a Bank 35 Sustainability at Bradesco 42 Solid and Transparent Governance 50 Integrity and Ethics 53 Risk Management 56 Generating Value 62 Results in a Challenging Year 64 Focus on the Client 76 Technology and Innovation 91 People: Our Team 102 Investing in the Future 122 Eco-efficiency 128 Investor Relations 131 BRADESCO Integrated Report | Shortened Version 2020 ABOUT THIS MATERIAL 4 Introduction It’s impossible to talk about a year like Despite the uncertainties in 2020, we 2020 without weighing the impacts also delivered strong results for the brought on by an unprecedented Organization, including a growth in our pandemic that modified the way we view quarterly net income throughout the our relationships with work, with people year, an expanded loan portfolio and and with the planet. a significant increase in the number of transactions through our digital This sudden collapse in all things we had channels – a situation that emphasizes considered normal paved the way for us the importance of providing the most to see the world in a different light. -

Remote E-Vote

REMOTE E-VOTE USINAS SIDERÚRGICAS DE MINAS GERAIS S.A. – USIMINAS CNPJ 60.894.730/0001-05 NIRE: 313.000.1360-0 Publicly-Held Company Annual Shareholders Meeting to be held on April 29th, 2021 REMOTE E-VOTE FOR RESOLUTIONS OBJECT OF THE ANNUAL SHAREHOLDERS’ MEETING 1. Name or corporate name of the shareholder (with no abbreviations) 2. CNPJ or CPF of the shareholder 2.1. E-mail address of the shareholder to receive communications from the Company related to the E-Vote 3. Guidelines to fill in the Remote E-Vote If you opt to exercise the remote E-voting right, under the terms of articles 21-A and following of CVM Ruling nº 481/2009, the shareholder shall fill in this Remote E-Vote (“E-Vote”), that shall only be considered valid and the votes expressed herein will be counted for the quorum of the Shareholders’ Meeting, if the following instructions are observed: (i) all pages need to be initialed; and (ii) the last page shall be signed by the shareholder or by its legal representative(s), as the case may be, and under the terms of the law in force. It shall not be required the certification of the signatures on the E-Vote, nor the Hague apostille, notarization or consularization, being required, however, the sworn translation of the documents sent attached to the E-Vote that are drawn up in a foreign language. The term for the receipt of the E-Vote duly filled in ends on April 22nd, 2021 (inclusive), according to the instructions below. -

Institutional Presentation

Institutional Presentation 3Q19 Classification of Information: Public AGENDA Usiminas Pillars of Usiminas’ Management People Clients Results Governance and Highlights Classification of Information: Public Appendix Usiminas at a Glance Company Overview Geographic Footprint ✓ Usiminas is one of the largest flat steel producers in Brazil, with operations in several segments of the value chain, such as mining and logistics, capital goods, service and distribution centers and customized solutions ✓ Two steel plants strategically located along Brazil’s main industrial axis, with sales force present in the main regions of the country IPATINGA Belo Horizonte Itabria Porto TUBARÃO ✓ First Brazilian steel company certified by ISO 9001 Itaúna ✓ Founder of the most enduring environmental education project in the private sector since 1984 Mining Steel São Paulo Porto ITAGUÁ Steel Processing Porto CUBATÃO Capital Goods Shareholding Structure (% of total capital, except otherwise indicated) Financial Highlights (in R$mm, except otherwise indicated) Voting Capital Preferred Shares LTM 2015 2016 2017 2018 3Q19 Nippon Group; Nippon Group; 1.0% 0.6% Ternium/Tenaris Net Revenues 10,186 8,454 10,734 13,737 14,503 Others; Group; 1.8% Growth YoY (13%) (17%) 27% 28% 6% 23.2% Nippon Group; Adjusted EBITDA 291 660 2,186 2,693 2,335 31.4% Margin 3% 8% 20% 20% 16% Ternium/Tenaris Net Income (3,685) (577) 315 829 510 Group; 7.3% Margin Usiminas (36%) (7%) 3% 6% 4% Pension Fund; Total Debt 7,886 6,942 6,656 5,854 5,855 Others; 4.8% Ternium/Tenaris 97.6% Cash and Equivalents -

Securities and Exchange Commission Form 6-K

22/04/2019 siddf2018_6k.htm - Generated by SEC Publisher for SEC Filing 6-K 1 siddf2018_6k.htm FORM 6-K SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 6-K Report of Foreign Private Issuer Pursuant to Rule 13a-16 or 15d-16 of the Securities Exchange Act of 1934 For the month of April, 2019 Commission File Number 1-14732 COMPANHIA SIDERÚRGICA NACIONAL (Exact name of registrant as specified in its charter) National Steel Company (Translation of Registrant's name into English) Av. Brigadeiro Faria Lima 3400, 20º andar São Paulo, SP, Brazil 04538-132 (Address of principal executive office) Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F. Form 20-F ___X___ Form 40-F _______ Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934. Yes _______ No ___X____ https://www.sec.gov/Archives/edgar/data/1049659/000129281419001386/siddf2018_6k.htm 1/144 22/04/2019 siddf2018_6k.htm - Generated by SEC Publisher for SEC Filing (CONVENIENCE TRANSLATION INTO ENGLISH FROM THE ORIGINAL PREVIOUSLY ISSUED IN PORTUGUESE) Annual Financial Statements – December 31, 2018 – CIA SIDERURGICA NACIONAL Version: 1 Table of Contents Company Information Capital Breakdown 1 Parent Company Financial Statements Balance Sheet – Assets 2 Balance Sheet – Liabilities 3 Statement of Income 4 Statement of Comprehensive Income 5 Statement -

UNITED STATES DISTRICT COURT SOUTHERN DISTRICT of NEW YORK in RE BANCO BRADESCO S.A. SECURITIES LITIGATION Civil Case No. 1:16

Case 1:16-cv-04155-GHW Document 45 Filed 10/21/16 Page 1 of 92 UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK IN RE BANCO BRADESCO S.A. Civil Case No. 1:16-cv-04155 (GHW) SECURITIES LITIGATION AMENDED CLASS ACTION COMPLAINT JURY TRIAL DEMANDED Case 1:16-cv-04155-GHW Document 45 Filed 10/21/16 Page 2 of 92 TABLE OF CONTENTS Page I. INTRODUCTION ...............................................................................................................2 II. JURISDICTION AND VENUE ..........................................................................................9 III. PARTIES ...........................................................................................................................10 A. Lead Plaintiff .........................................................................................................10 B. Defendants .............................................................................................................10 1. Banco Bradesco S.A. ................................................................................ 10 2. The Individual Defendants ........................................................................ 12 C. Relevant Non-Parties .............................................................................................13 IV. BACKGROUND ...............................................................................................................16 A. Bradesco Accesses the U.S. Capital Markets ........................................................16 B. Operation -

Abc Brasil Daycoval Linx Sabesp Aes Tiete E Dimed

LISTA DAS EMPRESAS ELEGÍVEIS - CARTEIRA DO ISE 2017 PERÍODO BASE 2016 ABC BRASIL DAYCOVAL LINX SABESP AES TIETE E DIMED LOCALIZA SANEPAR ALFA INVEST DIRECIONAL LOCAMERICA SANTANDER BR ALIANSCE DURATEX LOG-IN SANTOS BRP ALPARGATAS ECORODOVIAS LOJAS AMERIC SAO CARLOS ALUPAR ELETROBRAS LOJAS MARISA SAO MARTINHO AMBEV S/A ELETROPAULO LOJAS RENNER SARAIVA LIVR ANIMA EMBRAER LOPES BRASIL SCHULZ AREZZO CO ENERGIAS BR M.DIASBRANCO SENIOR SOL ARTERIS EQUATORIAL MAGAZ LUIZA SER EDUCA B2W DIGITAL ESTACIO PART MAGNESITA SA SID NACIONAL BANCO PAN ETERNIT MARCOPOLO SIERRABRASIL BANRISUL EUCATEX MARFRIG SLC AGRICOLA BBSEGURIDADE EVEN METAL LEVE SMILES BMFBOVESPA EZTEC MILLS SOMOS EDUCA BR BROKERS FER HERINGER MINERVA SPRINGS BR INSURANCE FERBASA MRV SUL AMERICA BR MALLS PAR FIBRIA MULTIPLAN SUZANO PAPEL BR PHARMA FLEURY MULTIPLUS TAESA BR PROPERT FORJA TAURUS NATURA TARPON INV BRADESCO GAFISA ODONTOPREV TECHNOS BRADESPAR GENERALSHOPP OI TECNISA BRASIL GERDAU OUROFINO S/A TEGMA BRASILAGRO GERDAU MET P.ACUCAR-CBD TELEF BRASIL BRASKEM GOL PARANA TEMPO PART BRF SA GRAZZIOTIN PARANAPANEMA TEREOS CCR SA GRENDENE PARCORRETORA TIM PART S/A CCX CARVAO GUARARAPES PDG REALT TIME FOR FUN CELESC HELBOR PETROBRAS TOTVS CEMIG HYPERMARCAS PETRORIO TRACTEBEL CESP IDEIASNET PINE TRAN PAULIST CETIP IGUATEMI PLASCAR PART TRISUL CIA HERING IMC S/A PORTO SEGURO TRIUNFO PART CIELO INDS ROMI PORTOBELLO TUPY COELCE IOCHP-MAXION POSITIVO INF ULTRAPAR COMGAS ITAUSA PROFARMA UNICASA COPASA ITAUUNIBANCO PRUMO UNIPAR COPEL JBS QGEP PART USIMINAS COSAN JHSF PART QUALICORP V-AGRO COSAN LOG JSL RAIADROGASIL VALE CPFL ENERGIA KEPLER WEBER RANDON PART VALID CSU CARDSYST KLABIN S/A RENOVA VIAVAREJO CVC BRASIL KROTON RODOBENSIMOB WEG CYRELA REALT LE LIS BLANC ROSSI RESID WHIRLPOOL DASA LIGHT S/A RUMO LOG. -

GERDAU S.A. (Exact Name of Registrant As Specified in Its Charter)

U.S. SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 to FORM 20-F [ ] REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR [X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 1999 Commission file number 1-14878 GERDAU S.A. (Exact Name of Registrant as Specified in its Charter) Federative Republic of Brazil (Jurisdiction of Incorporation or Organization) N/A (Translation of Registrant's name into English) Av. Farrapos 1811 Porto Alegre, Rio Grande Do Sul - Brazil CEP 90220-005 (Address of principal executive offices) (Zip code) Securities registered pursuant to Section 12(b) of the Act: Title of Each Class Name of Each Exchange in Which Registered Preferred Shares, no par value per share, each represented by American Depositary Shares New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: None Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None The total number of issued shares of each class of stock of GERDAU S.A. as of December 31, 1999 was: 19,691,010,193 Common Shares, no par value per share 37,054,842,993 Preferred Shares, no par value per share Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Report Sustainability 2010 Annual Sustainability Report

CEMIG’SCEMIG’S MAIN MAININDICATORS INDICATORS Financial dataFinancial (Economic data Dimension(Economic –Dimension in R$) are –consolidated in R$) are consolidated according to according the IFRS. toThe the other IFRS. data The refer other to data the controllingrefer to the company controlling company (holding) Cemig(holding) – Companhia Cemig – CompanhiaEnergética deEnergética Minas Gerais de Minas S.A. andGerais its S.A.whole and subsidiaries: its whole subsidiaries: Cemig Distribuição Cemig Distribuição S.A. (Cemig S.A.D) and (Cemig Cemig D) and Cemig Geração e TransmissãoGeração e Transmissão (Cemig GT) (Cemigin accordance GT) in accordancewith the GRI with – Global the GRI Reporting – Global Initiative Reporting methodology. Initiative methodology.1 1 2008 20082009 20092010 2010 GeneralGeneral Data Data Number of ConsumersNumber of Consumers– thousand 2– thousand2 6,602 6,6026,833 6,8337,065 7,065 Number of employeesNumber of employees 10,422 10,4229,746 9,7468,859 8,859 MunicipalitiesMunicipalities serviced serviced 774 774774 774774 774 Concession ConcessionArea – Km2 3Area – Km2 3 567,478 567,478567,478 567,478567,740 567,740 Saifi – NumberSaifi of– outgagesNumber of(EU28) outgages (EU28) 6.53 6.536.76 6.766.56 6.56 Saidi – HoursSaidi of outgages – Hours of (EU29) outgages (EU29) 13.65 13.6514.09 14.0913.00 13.00 Number of plantsNumber in ofoperation plants in4 operation4 63 63 65 65 66 66 Installed capacityInstalled – MW capacity (EU1) 5– MW (EU1)5 6,691 6,6916,716 6,7166,896 6,896 TransmissionTransmission lines – Km (EU4)lines -

STATE-OWNED ENTERPRISES in BRAZIL: HISTORY and LESSONS by Aldo Musacchio and Sergio G

Workshop on State-Owned Enterprises in the Development Process Paris, 4 April 2014 OECD Conference Centre, Room 4 STATE-OWNED ENTERPRISES IN BRAZIL: HISTORY AND LESSONS by Aldo Musacchio and Sergio G. Lazzarini This paper serves as background material for the Workshop on SOEs in the Development Process taking place in Paris on 4 April 2014. It was prepared by Aldo Musacchio and Sergio G. Lazzarini working as consultants for the OECD Secretariat. The opinions and views expressed and arguments employed herein are those of the author and do not necessarily reflect or represent the official views of the OECD or of the governments of its member countries. STATE-OWNED ENTERPRISES IN BRAZIL: HISTORY AND LESSONS Aldo Musacchio Harvard Business School and NBER Sergio G. Lazzarini Insper Prepared for The Working Party on State-Ownership and Privatisation Practices OECD (Revised version, February 28, 2014) INTRODUCTION Despite decades of liberalization and privatization in many countries, state ownership and state-led business activity remains widespread (Christiansen, 2011). Governments still often use state-owned enterprises (SOEs) to promote local development and invest in sectors in which private investment is scant. Many SOEs endured over the years and turned into large corporations partnering with market investors and competing on a global scale against private multinationals. The forms of ownership and control governments use in the set of surviving SOEs is, however, poorly understood. Beyond the traditional wholly-owned SOEs, governments also intervene to support specific industries by propping up privately held enterprises (i.e., “national champions”). These private firms receive government support in the form of minority equity investments, direct subsidized loans from development banks, and equity and debt purchases by sovereign wealth funds. -

Faculty & Research Working Paper

Faculty & Research Working Paper Bi-Regional Private Sector Networks: Harnessing the Potential of the Private Sector in European Union and Latin America and Caribbean _______________ Lourdes CASANOVA 2006/61/ST BI-REGIONAL PRIVATE SECTOR NETWORKS 1 Harnessing the Potential of the Private Sector in European Union and Latin America and Caribbean By Lourdes Casanova* March 2006 * Lecturer in Comparative Management, Strategy Department, INSEAD, Boulevard de Constance, 77305 Fontainebleau Cedex, France, [email protected] A working paper in the INSEAD Working Paper Series is intended as a means whereby a faculty researcher's thoughts and findings may be communicated to interested readers. The paper should be considered preliminary in nature and may require revision. Printed at INSEAD, Fontainebleau, France. Kindly do not reproduce or circulate without permission. 1 The funding of the Inter American Development Bank is gratefully acknowledged. 1. Introduction There is a long history of successful private partnerships between members of the European Union and countries in the Latin American and Caribbean (LAC) regions. Starting from the colonial era, private firms have exploited the mutual commercial synergies of these two regions. These economic bonds were strengthened and facilitated by close cooperation on the social and political arenas. For example, many of the leaders of the independence movements in Latin America went to France to study the principles of the French revolution. There have also been significant migrations of populations in both directions over the last centuries. Latin American Napoleon Civic Code is more familiar to European firms than the British Common Law system followed in US and many parts of Asia. -

RESULTS 2020 Summary

2020 RESULTS OF OVERCOMING YEAR A SUSTAINABILITY REPORT Summary 1 2 3 FOREWORD CORPORATE CORPORATE FINANCIAL PROFILE GOVERNANCE PERFORMANCE 4 5 6 7 8 STRATEGY PEOPLE COMMUNITY ENVIRONMENT GRI CONTENT INDEX SUSTAINABILITY REPORT | 2020 FOREWORD Message from the Board of Directors ear 2020 ended a decade that tested Usiminas’ resilience in several ways. We Y have closed the period with results that show a quick and effective reaction ca- pacity. Supported by the Board of Directors, Usiminas’ Executive Board took the lead in an effective work to meet and react to the extraordinary demands brought by the pandemic. The Board of Directors’ agenda, on the other hand, has been adapted to this challenging scenario. 29 meetings were held, whether in person or via video con- ference, to approve urgent matters. The Board has quickly approved the shutdown of the blast furnaces during the crisis – and later it approved them to gradually resume operations. Another 2020 issue was the corporate restructuring of Usiminas Mecâni- ca, which now focuses on providing services only to Usiminas companies. The Company’s good results, despite all hurdles, allow us to embark in this new de- cade looking to the future and build the company’s perpetuity. We are strongly en- gaged in Environmental, Social and Governance (ESG) matters, in line with the long- term sustainability strategy. 3 SUSTAINABILITY REPORT | 2020 We have strengthened measures that began to gain momentum over the past years. In For the second year in a row, per the Executive Board’s initiative, the Company’s report 2018, we created an independent integrity department reporting to the Board of Direc- has been improved according to the Global Reporting Initiative (GRI) standards, which tors, which enhanced Usiminas’ governance level. -

Parcerias Com Setor Privado Ajudam Copasa a Crescer

Partnerships with the private sector help Copasa grow Cesar Felicio, de Belo Horizonte August 21, 2009 Text: A- A+ Print After seven years of losses, Copasa, a state-owned company from the Brazilian state of Minas Gerais, recorded a net income of R$241 million in the first semester this year and entered into the first partnerships with private companies to expand its operations. Copasa acquired 20% of a company created by Foz do Brazil, formerly Odebrecht Engenharia Ambiental. The Special Purpose Entity (SPE) will construct and operate for a period of 15 years facilities for water catchment and treatment of effluents from the pipe factory under construction by Vallourec & Sumitomo in Jeceaba, Minas Gerais. The acquisition of the stake was relatively cheap—R$20 million—but is nonetheless strategically important. "We agreed to become Odebrecht’s partner in the search for other private clients, in operations similar to the one in Jeceaba, and also to take part in future water and sewage concession auctions," said Márcio Nunes, who began his career in the electricity sector and, since 2005, has been Copasa’s CEO. According to Nunes, the partnership with Foz do Brasil is not Copasa’s only partnership with private companies; it has a similar agreement with Cowan, a Minas Gerais State construction company. Copasa also hopes to enter into long-term service agreements with steel industries that, in general, collect water and treat effluents on their own. Copasa has already started negotiating with Usiminas, whose main steel plant is located in Ipatinga, Minas Gerais. A Usiminas spokesperson informed Valor that it has not decided to outsource the activity yet and that, right now, there are no negotiations in progress.