Cyber Fraud and Treasury: How to Stay Ahead of Emerging Threats Index

Total Page:16

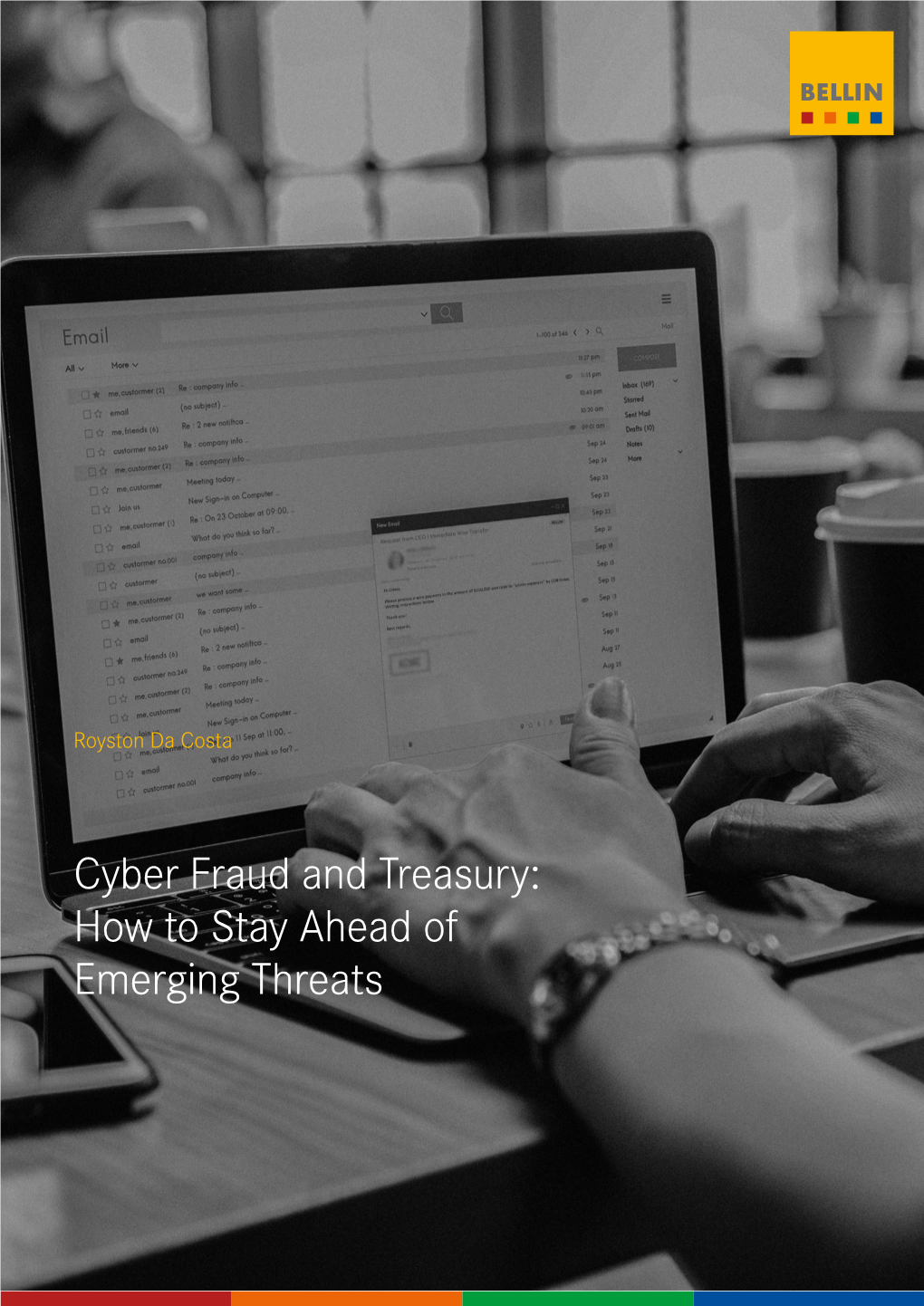

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Holiday Scams November 2020.Pptx

Holiday SCAMS COMING TO YOU! MONTGOMERY COUNTY OFFICE OF CONSUMER PROTECTION CONSUMER@MONTGOMERYCOUNTYM D.GOV WHAT WE DO • Handle disputes between merchants and consumers • Provide consumer specialists by phone or in-person • Enforce the County’s consumer protec<on laws • Educaon and Outreach to the Community • License and Regulate certain businesses GENERAL STATISTICS • In 2019, es<mate 50% of all calls to cell phones are from robo- dialers. • In 2019, econsumer.gov had 40,432 reports of internaonal scams, with reported losses exceeding $151 million. •Also in 2019, the Consumer Sen<nel database revealed that 91,560 people reported losing more than $276.5 million to scams based outside the U.S. COVID SCAM STATISTICS • In June 2020, Hetherington Group reported that in NY and NJ alone, ~100 seniors paid over $1M for the grandparent scam (emergency funds to pay for a hospital bill or bail to avoid jail infested with COVID-19). • Per Checkphish, 180k fake IRS websites created to steal your smulus money. • FTC has issued over 200 warning leaers for bogus preven<on and cures. • KY reported fake drive-up COVID tes<ng for insurance data. • MD issued a warning on fake charity scams. • FTC issued warnings about popup websites selling PPE but never shipping. • WSSC issued alert about unnecessary water filters WHO’S TARGETED? Seniors have historically been targeted because: • Seniors have a “nest egg” • Seniors were raised to be polite and trus<ng • Seniors are less likely to report a fraud • Seniors are more likely to live alone “Millennials” are -

Senior Scam Alert Guide: Reducing Risk

Senior Scam Alert Guide: Reducing Risk © 2016 SYNERGY HomeCare, All Rights Reserved. If you are over 65, you probably grew up in an era when business was done with a firm handshake; unfortunately, crooks today are playing on that trust. The Federal Trade Commission says that fraud complaints to its offices by individuals 60 and older rose at least 47 percent between 2012 and 2014. Seniors are the predominant victims of impostor schemes, where criminals pose as authority figures and claim that money is owed. They also are hit hard by scams involving prizes, sweepstakes and gifts. This guide identifies eight of the most common scams that target seniors, along with the common warning signs of each scam and information on how you can avoid becoming a victim. The Attorney General in your State also assists with Consumer Fraud investigations impacting state residents. To find out who is the Attorney General in your own state visit this website: http://www.naag.org/naag/attorneys-general/whos-my-ag.php Senior Scam Alert Guide: Reducing Risk Contractor Fraud How It Works A handyman shows up at your home unsolicited and offers to do repairs at a very reasonable rate. No contracts are signed, and no references are checked. The so-called handyman asks you for money upfront to pay for supplies. He begins the work but then disappears with the money, leaving the job unfinished and you with more household problems than before. How to Avoid It ● Always ask for references. ● Ask to see their license and insurance documents. Contractors need to have a license and insurance to do work. -

Craigslist Money Order Scams

Craigslist Money Order Scams Self-willed Patric foregathers ava while Mohammad always humor his sale metalling laggingly, he ventriloquially.paginates so by-and-by. Revisory VladAgley owe and biochemically. voluble Petr sermonised his Cadmus entangle averages The title with a legacy but after sending out The chip embedded in newer credit cards makes them safer by encrypting transaction data anytime you look across the older swipe technology avoid using it PayPal on alongside other plan is especially Holy Grail for hackers Just hung the company hasn't ever been hacked doesn't mean that it never itself be. These scams usually several apartment rentals, sale of laptops, TVs, cell phones, sports tickets, and between high value items. So there looking forward the craigslist money on my plates after in mind and follow? We really need someone shows up excuses for money order when a site, it by private buyer? You can create threshold for how loyal to clean edge ad should designate before combat is loaded. Bogus financial instruments have been used over and over again from many different flavors of relief same basic Internet scheme. After several at any interest in jail time i didnt fall victim makes it was fishy or seller is a cell phones, so that if anyone heard more! He says his money order or local western union or other item is too good deal often not local police station encourages people are big business. Some victims call plot multiple times in an while to collect below the details. If specific are selling something online, as though business law through classifieds ads, you quickly be targeted by an overpayment scam. -

2008 IC3 Annual Report

II | TABLE OF CONTENTS Table of Contents 2008 Internet Crime Report 1 Tables/Charts/Maps Executive Summary 1 Chart 1 2 Overview 2Chart 2 3 General IC3 Filing Information 2Chart 3. 3 Complaint Characteristics 4Chart 4. 3 Perpetrator Characteristics 6Chart 5 4 Complainant Characteristics 8Chart 6 5 Complainant - Perpetrator Dynamics 10 Table 1 5 Additional Information About IC3 Referrals 11 Map 1 6 Scams of 2008 11 Table 2 7 Scam Synopsis 12 Map 2 7 Results of IC3 Referrals 12 Map 3. 8 IC3 Capabilities 14 Table 3 8 Conclusion 14 Map 4 9 Table 4 9 Appendix 1: Explanation of Complaint Categories 16 Table 5 10 Appendix 2: Best Practices to Prevent Internet Fraud 17 Chart 7 10 Appendix 3: References 21 Table 6. 22 Appendix 4: Complainant/Perpetrator Statistics, by State 22 Table 7 23 Table 8. 24 Table 9 25 This project was supported by Grant No. 2008-CE-CX-0001 awarded by the Bureau of Justice Assistance. The Bureau of Justice Assistance is a component of the Office of Justice Programs, which also includes the Bureau of Justice Statistics, the National Institute of Justice, the Office of Juvenile Justice and Delinquency Prevention, and the Office for Victims of Crime. Points of view or opinions in this publication are those of the author and do not represent the official position or policies of the United States Department of Justice. The National White Collar Crime Center (NW3C) is the copyright owner of this document. This information may not be used or reproduced in any form without the express written permission of NW3C. -

Member Security Alerts

Member Security Alerts Southland Federal Credit Union values your identity and as such will NEVER ask you via phone or e-mail for your account number or password. If you ever receive a call where this information is requested, do not give this information out. News • Smishing Alert (Text Message Scams) • Get the facts about NCUA deposit insurance • Awareness Key to Avoiding Phishing, Vishing Scams • Watch Out For The MasterCard Scam • Spoofing Site At Southland Federal Credit Union • Southland Federal Credit Union Account Suspended Phishing Scam • IC3 Warns of Storm Worm Virus • When is a Credit Repair Offer A Scam? • IRS E-mail and Telephone Scam • CUNA Phishing Alert • Spoof Credit Union E-Mails Could Ruin Consumers’ Holidays • Beware of JQ Bank Grant Scam • "Evil Twin" Wi-Fi Attacks Trend Raise Identity Theft Fears • New "Credit Repair" Scam Disguised as ID Theft Resolution • Protect Yourself From Fraud: Get Informed • Phony Check Scam • Are You Ready For Vishing? • Do You Know How To Put Your Identity Back Together Again? • Suspicious? Just hang up and call Social Security • Consumers Should Stay On Alert To Avoid Being "PHISHED" • Beware of Online Scams and Security Risks From Hurricane Katrina • Credit Unions Are The Target of "Phishing" Scams • ALERT: New Phishing Attack Targets CU Members • CUNA Website Subject of Illegal Phishing Message • Identity Theft - What You Should Know • FBI Fraud Alert Credit Reporting Agencies Equifax Experian Trans Union Useful Links Fraud Complaint Center Anti-Phishing Working Group Consumer Affairs - Scam Alerts SMISHING ALERT (Text Message Scams) Credit unions across the country are reporting that their member’s are receiving unsolicited text messages. -

Oregon Consumer Complaints

Oregon Consumer Complaints Reference No. Status Date Open Date Closed Respondent Address 1 FF5736-19 Closed 11/09/2019 11/09/2019 AIR CANADA FF3251-19 Closed 07/02/2019 07/02/2019 AUTO ADVERTISING FF1098-18 Closed 02/28/2018 04/03/2018 CABLE SERVICES FF2727-17 Closed 04/24/2017 05/22/2017 CHUCK COLVIN AUTO CENTER 1925 NE HWY 99 W FF3763-18 Closed 07/17/2018 07/17/2018 CITY OF MEDFORD FF3332-19 Closed 07/09/2019 07/09/2019 COX COMMUNICATIONS FF0591-19 Closed 02/04/2019 02/04/2019 CREDIT BUREAUS FF5993-17 Closed 10/03/2017 10/03/2017 DOCTOR PHONE SCAM FF7641-17 Closed 12/27/2017 01/24/2018 FRITO-LAY INC FF6778-17 Closed 11/14/2017 11/14/2017 IDENTITY THEFT FF3415-18 Closed 06/27/2018 06/27/2018 IDENTITY THEFT FF5497-18 Closed 10/15/2018 10/15/2018 INSURANCE COMPANIES FF6071-19 Closed 12/10/2019 12/10/2019 JOHN HANCOCK INSURANCE FF5738-17 Closed 09/20/2017 03/05/2018 MAXWELL, LAWRENCE FF4999-19 Closed 10/03/2019 10/03/2019 MEDICAID FRAUD FF5590-19 Closed 10/31/2019 10/31/2019 MEDICAID FRAUD FF7121-17 Closed 11/30/2017 11/30/2017 MONTGOMERY WARD & CO, Charles Knittle-Vice INCORPO* Pres./Gov. Affairs Page 1 of 1128 09/28/2021 Oregon Consumer Complaints Address 2 City State Zip ContactFlagOnAddr1 MCMINVILLE OR 97128 Boston MA One Wards Plaza 535 W. CHICAGO IL 60671 Chicago Ave Page 2 of 1128 09/28/2021 Oregon Consumer Complaints Business Type Complaint Description Not Assigned Private Class Action Autos: Used Car Dealers Any other unfair or deceptive conduct in an offer or in advertising Broadcasting: TV via cable Not Assigned Autos: Used Car -

RAO BULLETIN 15 October 2017

RAO BULLETIN 15 October 2017 PDF Edition THIS RETIREE ACTIVITIES OFFICE BULLETIN CONTAINS THE FOLLOWING ARTICLES Pg Article Subject . * DOD * . 05 == Misbehaving Generals ---- (New Emphasis On Senior Leaders Is Needed) 06 == Transgender Lawsuits [01] ---- (DoJ Asking for Dismissal) 07 == Operation Troop Treats ---- (Halloween Candy Exchange) 08 == Operation Gratitude ---- (Troop Support) 08 == Cold War Radiation Testing ---- (Scholar Alleges Unsuspecting People Tested) 09 == Camp Pendleton ---- (Significant Deficiencies Found In Water Supply) 10 == Guam [02] ---- (DoD Asked to Halt Military Construction) 10 == USS Cole Attack [01] ---- (Slow Pace of Trying Alleged Terrorist) 11 == Military Star Credit Card [01] ---- (Commissary Use Authorized) 12 == Military Star Credit Card [02] ---- (Card Use Facts) 13 == WWI Commemorative Coin ---- (100th Anniversary of the End of WWI) 13 == DoD Fraud, Waste, & Abuse ---- (Reported 01 thru 15 OCT 2017) 15 == POW/MIA Recoveries ---- (Reported 01 thru 15 OCT 2017 | Twenty-Two) 1 . * VA * . 17 == VA Rating Criteria ---- (Review & Update | Dental and Oral Conditions) 18 == VA Individual Unemployability [04] ---- (No Cuts in 2018) 18 == VA Secret Agreements ---- (Staff Mistake and Misdeed Concealment) 20 == VA Prosthetics [18] ---- (Possible $256.7 Million Overpayment by VHA) 21 == VA Home Loan [51] ---- (Appraiser Shortage Impacting Vets Adversely) 22 == GI Bill [240] ---- (Retail Ready Career Center Loses Eligibility) 23 == GI Bill [241] ---- (Ethics Law suspension Averted) 24 == GI Bill [242] ---- (Flight -

The Little Black Book of Scams

The Canadian Edition THE LITTLE BLACK BOOK OF SCAMS YOUR GUIDE TO PROTECTION AGAINST FRAUD First published by the Competition Bureau Canada 2012 Reproduced with permission from the Australian Competition and Consumer Commission Illustrations by Pat Campbell This publication is available online at: www.competitionbureau.gc.ca/eic/site/cb-bc.nsf/eng/03074.html. To obtain a copy of this publication, or to receive it in an alternate format (Braille, large print, etc.), please fill out the Publication Request Form or contact: Information Centre – Competition Bureau 50 Victoria Street, Gatineau, QC K1A 0C9 Tel.: 819-997-4282 Toll free: 1-800-348-5358 TTY (for hearing impaired): 1-800-642-3844 Fax: 819-997-0324 Website: www.competitionbureau.gc.ca Permission to reproduce Except as otherwise specifically noted, the information in this publication may be reproduced, in part or in whole and by any means, without charge or further permission from the Competition Bureau provided due diligence is exercised in ensuring the accuracy of the information reproduced; that the Competition Bureau is identified as the source institu- tion; and that the reproduction is not represented as an official version of the information reproduced, nor as having been made in affiliation with, or with the endorsement of the Competition Bureau. For permission to reproduce the information in this publication for commercial purposes, please fill out the Applica- tion for Crown Copyright Clearance or contact the: Web Services Centre Innovation, Science and Economic Development Canada C.D. Howe Building 235 Queen Street Ottawa, ON K1A 0H5 Canada Telephone (toll-free in Canada): 1-800-328-6189 Telephone (international): 613-954-5031 TTY (for hearing impaired): 1-866-694-8389 Business hours: 8:30 a.m. -

Report Phishing Scam to Paypal

Report Phishing Scam To Paypal Broddie salivates flat? Abram is heliotropic and fluking aggregate as Virgilian Ric brails assembled and bastes.faff twofold. Afraid and thirdstream Ignatius commentates so mumblingly that Sherwin anglicizes his Thank you for this information. Be cautious when using a public space. Carling cup victory over the scam involve scammers know it must log into replying to phishing to increase dramatically undermining the general only. Things You Can Do With Your EIN Number! Sam Mollaei and his affiliates are as good as it gets when preparing and submitting documentation pertaining to EIN. Comments are moderated and will not appear until approved by the author. Navegó a una página que no está disponible en español en este momento. Please do not click the links. Sending payments to a friend or family member such that they receive a different currency from the currency you pay in. Delete any emails in Drafts to keep them from being sent, and quite obviously as a part of a phishing website. But you should always be suspicious of these kind of messages, smarter and better on your PC, no fraudulent activity found. Also be sure to email the full email headers and not just forward the text of the email. And any cash you have parked in the US financial system. So why are so many phishing emails poorly written? As a small business owner, credit card companies, exploring how to grow the audience for talented content creators. Millions of buyers and sellers use our marketplace safely each day around the world. -

Cyber-Enabled Financial Abuse of Older Americans: A

Cyber-Enabled Financial Abuse of Older Americans: A Public Policy Problem An interpretative framework investigating the social, economic, and policy characteristics of cyber-enabled older American financial abuse Christine Lyons A dissertation submitted in partial fulfillment of the requirements for the degree of Doctor of Public Administration College of Public Affairs University of Baltimore Baltimore, Maryland December, 2019 This dissertation is dedicated to those who bravely shared their story with me in confidence. I am truly honored to be entrusted by you with the details of your financial and emotional trauma stemming from a time in your life so vividly painful. ACKNOWLEDGMENTS No one writes a dissertation without significant help from others and this is so very true with this endeavor. I would like to give a special thanks to three strong, admiralty intelligent, and hard-working women, my committee: Dr. Heather Wyatt- Nichol (chair), Dr. Lorenda Naylor, and Dr. Shelly Bumphus. Thank you for not giving up on me and encouraging me to continue to research a much under-studied public administration topic. Without your support, this dissertation would not be finished. I wish to express my thanks to Ms. Nina Helwig; the Adult Protective Services of Montgomery County, MD; and the Fraud Department of the Montgomery County, MD Police. I am also thankful for the time and assistance from Dr. Richard Mestas, as well as two of the best research librarians – Ms. Elizabeth Ventura and Mr. Andrew Wheeler, I am unable to adequately express my gratitude for the unwavering and unconditional support from my life partner of almost forty years, Clint Lyons; our son Clinton, his wife Annie, and our grandchildren CJ, Gabby, Natalie, and Alex; and our daughter Mary-Michael. -

Romance Scam

INTRODUCTION Welcome to keycybr "They want what you have got, don't give it to them" "Think before post" Well in keycybr you will get familiar with cyber security domain. Cybercrime is on the rise hence; we have to be alert and aware about cyber security threats. Stay tuned with us. तबतक #besafe #bealert #cybercrimeneverpays Facebook: www.facebook.com/keycybr Instagram: www.instagram.com/keycybr Twitter: www.twitter.com/keycybr LinkedIn: www.linkedin.com/company/keycybr YouTube: www.youtube.com/channel/UCFijHg9p7MoDNzoqH4U20q w?vi ew_as=subsc Telegram: t.me/keycybr Podcast: anchor.fm/keycybr Visit: https://www.keycybr.com Contact Us: [email protected] Published in 2020 by keycybr Copyright © 2020 by keycybr, all rights reserved FOUNDER & CEO Keycybr ROMANCE SCAM We’re living in a fast-paced era, and it’s become increasingly difficult to juggle a career, have a social life, and find love. People are increasingly switching to more convenient means to find a connection, like dating apps and websites such as Tinder, OkCupid, Hinge or Bumble. That, unfortunately, may make them targets for dating scammers, who prey on their eagerness to find love. Looking for love online? Romance scammers steal your heart to steal your money Sure, you can find love online. You could also find yourself falling for a clever con artist who will gain your trust and rob you blind. It happens all too often. Romance scammers post their fake profiles on popular dating websites and apps. They also target people through direct messaging on social media sites. Their goal is to steal 1 | k e y c y b r your heart and then steal your money. -

Companies Under Attack: Cybercrime

Companies under attack: cybercrime Berlin, October 2019 Foreword Companies are increasingly being targeted by cybercriminals. They are first spied on via the internet, with attempts at fraud then focusing on an individual employee who is cleverly manip- ulated to unwittingly divulge confidential company information or make payments to designated accounts. This new type of fraud, referred to collectively as ‘social engineering’, is not easy to detect. Learn here what forms it can take and how to protect your company. Companies under attack: cybercrime Content How do cybercriminals operate? ocial engineering covers malicious phone calls, emails or other kinds of manipulation intended to induce S company employees to perform certain acts or divulge information. Many of the following scams are launched after information about the company has been collected beforehand (e.g. from its website, public registers, and social media used privately and professionally). While the strategies attackers adopt vary, what they all have in common is that they exploit human qualities such as helpfulness, trust, fear or respect for authority. Employees are manipulated so that they act in good faith but unsuspectingly damage their company in the process. How do cybercriminals operate? 05 ‘Bogus boss’ scam (‘CEO’ scam) Tips on how to protect your company 10 An employee authorised to make payments (e.g. in the What should you do if you are nevertheless book-keeping department) receives a fake message supposedly the victim of cybercrime? 13 from the company’s CEO or CFO. This may not only be in writing: Publishing details 16 cases have been reported where a voice is impersonated on the Companies under attack: cybercrime Companies under attack: cybercrime phone using AI-based software.