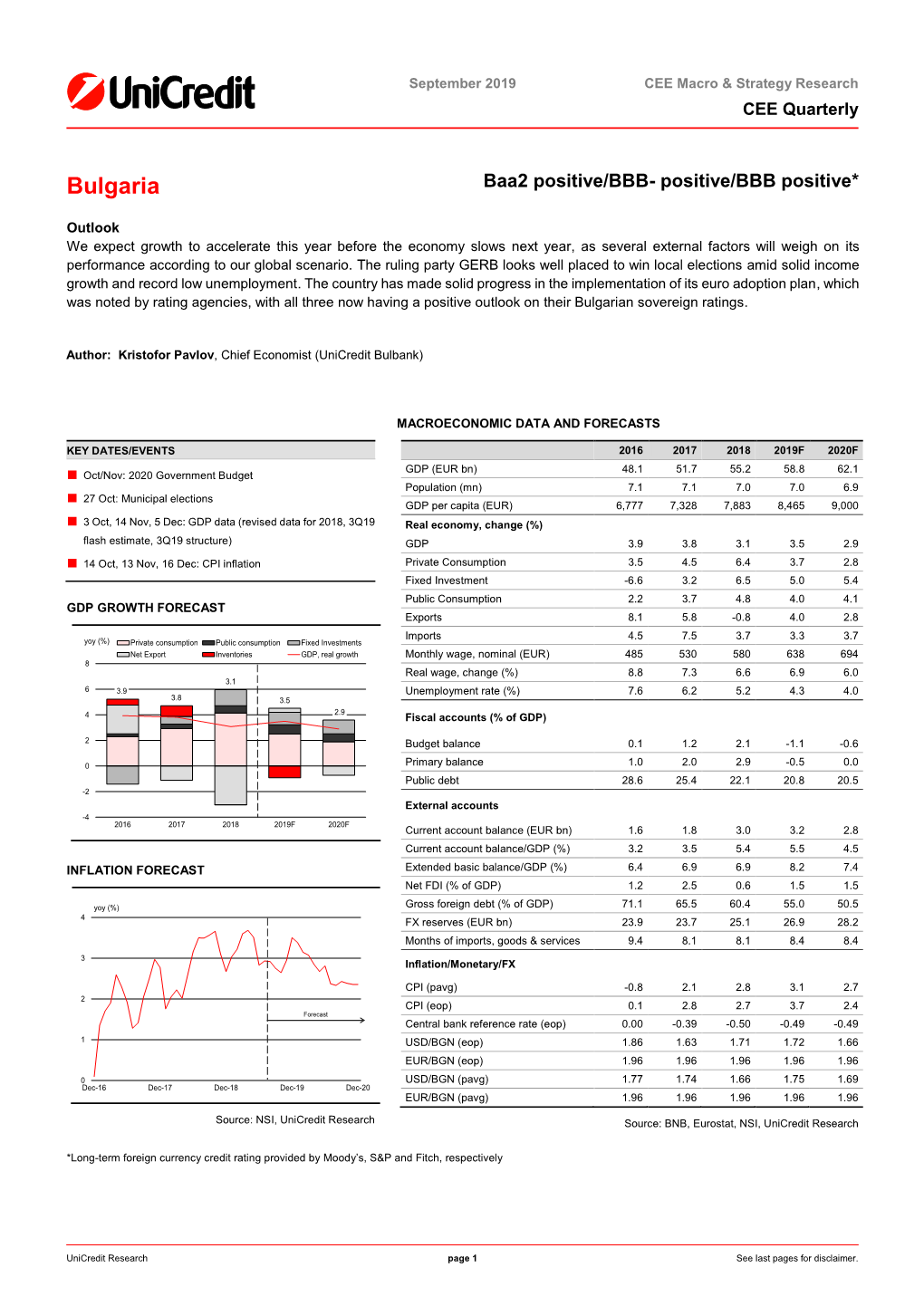

Bulgaria Baa2 Positive/BBB- Positive/BBB Positive*

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Magnitsky Law and the Rico

SSRG International Journal of Economics and Management Studies Volume 8 Issue 7, 6-20, July, 2021 ISSN: 2393 – 9125 /doi:10.14445/23939125/IJEMS-V8I7P102 © 2021 Seventh Sense Research Group® The Magnitsky Law and The Rico Law - The Guarantee For The Fight Against Corruption And The Mafia In Bulgaria And The European Union - The Example of The Attempts To Steal Private Land Through Concession, Theft of Land And Theft of Land Through State Structures Lord Prof. PhD PhD Momtchil Dobrev-Halachev Scientific Research Institute Dobrev & Halachev.JSC., Sofia.Bulgaria Received Date: 17 May 2021 Revised Date: 22 June 2021 Accepted Date: 05 July 2021 Abstract - Lord prof PhD PhD Momtchil Dobrev- The fight against the mafia and corruption in Bulgaria Halachev and Prof. Mariola Garibova-DObreva and in the European Commission and the European Union developed 2006 “Theory of degree of democracy” and does not yield results because the mafia is at the highest “Theory of degree of justice / injustice /” based on their state and European level and does what it wants. This practice in court, prosecutor's office, state. Prof. Momchil mafia holds courts, prosecutors and all kinds of state Dobrev has been creating Theory of Corruption, "Theory institutions and the latter carry out its orders. of the Mafia," Theory of Mafia "," Financial Banking Resource Technological Mafia Materialism "since 2003" 1.1 Introduce the Problem The problem with the mafia and corruption in Bulgaria Keywords - Crise, mafia, corruption, Magnitsky law, and in the European Union and the European Commission RICO law, finance. is huge. We have repeatedly applied evidence of the scale . -

Zornitsa Markova the KTB STATE

Zornitsa Markova THE KTB STATE Sofia, 2017 All rights reserved. No part of this book may be reproduced or express written consent from Iztok-Zapad Publishing House. transmitted in any form or by any means without first obtaining © Zornitsa Markova, 2017 © Iztok-Zapad Publishing House, 2017 ISBN 978-619-01-0094-2 zornitsa markova THE KTB STATE CHRONICLE OF THE LARGEST BANK FAILURE IN BULGARIA — THE WORKINGS OF A CAPTURED STATE THAT SOLD OUT THE PUBLIC INTEREST FOR PRIVATE EXPEDIENCY CONTENTS LIST OF ABBREVIATIONS AND ACRONYMS / 12 EDITOR’S FOREWORD / 13 SUMMARY / 15 READER’S GUIDE TO THE INVESTIGATION / 21 1. HISTORICAL BACKGROUND / 23 DEVELOPMENTS IN THE BULGARIAN BANKING SECTOR THAT PRE-DATE KTB ..........................................................25 Headed for a Banking Crisis .................................................................................................. 26 Scores of Banks Close Their Doors................................................................................... 29 First Private Bank — Backed by the Powerful, Favoured by the Government ......................................................... 33 Criminal Syndicates and Their Banks — the Birth of a State within the State ...........................................................................35 A Post-Crisis Change of Players ..........................................................................................37 A FRESH START FOR THE FLEDGLING KTB ..................................................... 40 KTB SALE ..........................................................................................................................................42 -

“Citizens for European Development of Bulgaria” and Slavi Trifonov's

GENERAL ELECTIONS IN BULGARIA 11TH JULY 2021 Boyko Borissov's “Citizens for European Elections monitor European Development of Bulgaria” Corinne Deloy and Slavi Trifonov's “Such a People Exist” neck and neck after the parliamentary elections RESULT Citizens for European Development of Bulgaria (GERB, Turnout was low. It totalled 38.0%. There are several which means "shield" in Bulgarian), led by former Prime reasons for this: the holidays, the increase in the number Minister (2009-2013, 2014-2017 and 2017-2021) Boyko of voting machines which may have discouraged some Borissov, and Such a People Exist (Ima takuv narod, voters, especially the older ones, but also, and above ITN), a populist party founded by singer and TV all, the weariness of Bulgarians with their political class. presenter Slavi Trifonov finished in a tight race in the 11 Finally, the high abstention rate is also the result of a July parliamentary elections in Bulgaria. ITN won decline in vote buying according to Parvan Simeonov, 24.08% of the vote and 65 MPs, while GERB won director of the Gallup International Institute in Bulgaria. 23.51% of the vote and 63 MPs. The Socialist Party (BSP) led by Korneliya Ninova took 13.51% of the vote, followed by the liberal coalition Democratic Bulgaria led by Hristo Ivanov, which includes 3 parties (Yes Bulgaria, Democrats for a Strong Bulgaria and the Greens), which won 12.56%. The Movement for Rights and Freedoms (DPS), a party representing the Turkish minority, led by Mustafa Karadayi, obtained 10.66% of the vote. Finally, the coalition Get up Bulgaria ! Mafia, get out! (Izpravi se BG! Moutri van!) of former ombudsman Maya Manolova and the Poisoned Trio (the name given by journalist Sasho Dikov to the trio comprising lawyer Nikolai Hadjigenov, sculptor Velislav Minekov and public relations specialist and former radio journalist Arman Babikyan) secured 5.06% of the vote and will be represented in the next National Assembly (Narodno sabranie), the only chamber of the Parliament. -

SGI Country Report 2020 for Bulgaria

Bulgaria Report Georgy Ganev, Maria Popova, Frank Bönker (Coordinator) Sustainable Governance Indicators 2020 © vege - stock.adobe.com Sustainable Governance SGI Indicators SGI 2020 | 2 Bulgaria Report Executive Summary Bulgaria saw a drift downward in terms of the quality of its governance structure in 2019. The junior partner in the ruling coalition, a grouping of three xenophobic nationalistic parties, has for all practical purposes fallen apart. The effort to stay in power itself is largely what has held the ruling coalition under Prime Minister Boyko Borissov together. Media freedom continues to deteriorate; major gaps in the anti-corruption framework and its effectiveness have been uncovered; a personal-data leak affecting more than half of Bulgaria’s citizens was allowed by a government agency, with no effective investigation or consequences following; and party financing has been changed in a way that clearly allows for widespread development of illicit dependencies. Public protests erupted over a seemingly technical issue, the appointment of a new prosecutor general. This drift took place against the background of continued relatively good economic performance, featuring moderately high growth rates, a small budget surplus and decreasing public debt, a record-high employment rate and low unemployment rates. The external trade balance has slightly improved, but in a context of decreases in both exports and imports. Structurally, Bulgaria still faces serious challenges in terms of the population’s skill levels and the economy’s innovation capacity and productivity. The country continues to lag severely with regard to public and private research and innovation funding. Other serious problems include the relatively low-skilled labor force, and the economic exclusion of people with low educational attainment and some minority groups. -

Summary of the Annual Report of the Work of the Ombudsman

Summary of the Annual Report of the Work of 2019 the Ombudsman “I promise that the Ombudsman will be where the citizens’ problems are and I will not spare an effort to defend the principle that all human beings are born free and equal in dignity and rights!” Assoc.Prof. Diana Kovacheva, Ombudsman of the Republic of Bulgaria March 2020 Table of Contents Introduction ................................................................................................................................... 3 Actions and results ......................................................................................................................... 6 Key events and initiatives in 2019 .................................................................................................. 8 2019 in numbers .......................................................................................................................... 15 Chapter One. The Ombudsman Protecting the Citizens’ Rights .................................................... 21 1. Reception desk of the Ombudsman ......................................................................................... 22 2. Consumer rights ....................................................................................................................... 24 3. Social rights .............................................................................................................................. 30 4. Rights of persons with disabilities ........................................................................................... -

Summary of the Annual Report of the Work of the Ombudsman 2018

„What we promise is to spare no energy, enthusiasm or will to perform even better this year and help even more people!“ Maya Manolova, Ombudsman of the Republic of Bulgaria SUMMARY OF THE ANNUAL REPORT OF THE WORK OF THE OMBUDSMAN 2018 March 2019 Contents Introduction ..................................................................................... 3 A Year of Achievements ....................................................................... 5 Priorities for 2018 .............................................................................. 6 Campaigns and Initiatives in 2018 .......................................................... 6 The Year 2018 in Figures (Statistics) ...................................................... 13 CHAPTER ONE. The Ombudsman Protecting Citizens’ Rights ........................ 19 1. Ombudsman’s Reception .................................................................. 20 2. Rights of Persons with Disabilities ....................................................... 21 3. Rights of the Child .......................................................................... 26 4. Consumer Rights ............................................................................ 29 5. Social Rights ................................................................................. 31 6. Right to education .......................................................................... 34 7. Right to healthcare ......................................................................... 37 8. Right to property and economic freedom -

The Parliamentary Elections Reveal The

GENERAL ELECTIONS IN BULGARIA 4th April 2021 The parliamentary elections reveal European Elections monitor the extreme fragmentation of the Bulgarian political scene: the Corinne Deloy composition of the government will be difficult and the risk of instability high Results It is hard to say who won the 4 April parliamentary The coalition Stand up Bulgaria! Get the bandits out! elections in Bulgaria, which were seen as a referendum (Izpravi se BG! Moutri van!) of former ombudswoman on Boïko Borissov, the outgoing Prime Minister, who has Maya Manolova and the Poisoned Trio (the name given led Bulgaria since 2009, weakened by several corruption by journalist Sasho Dikov to the trio comprising lawyer scandals and who had to face numerous demonstrations Nikolai Hadjigenov, sculptor Velislav Minekov and of discontent in 2020. Although his party, the Citizens public relations specialist and former radio journalist for the European Development of Bulgaria (GERB), Arman Babikyan) with 4.74% of the vote thus enters which ran in coalition with Rumen Hristov's Union of parliament. Democratic Forces (SDS), came out on top with 26.14% of the vote, they nevertheless recorded a decline Finally, the Movement for Rights and Freedoms (DPS), a compared to the previous election on 26 March 2017. party representing the Turkish minority, led by Mustafa The Socialist Party (BSP) led by Korneliya Ninova Karadayi, obtained 10.34% of the votes. collapsed: it received 15.02% of the vote and lost its In total, six parties will be represented in Parliament. status as the first opposition party, coming only in third place. Bulgarians living abroad voted for the party "Such a People Exist", to which they gave 29.83% of their The protest parties that led the 2020 demonstrations votes. -

Download/Print the Study in PDF Format

GENERAL ELECTIONS IN BULGARIA 11TH JULY 2021 Bulgarians go to the polls again on European Elections monitor 11 July to elect their MPs Corinne Deloy ANALYSIS 3.4 million Bulgarians are again being called to the polls Prime Minister called his rivals "cowards" accusing them on 11 July to elect the 240 members of the National of being "afraid" of taking office. Assembly (Narodno sabranie), the single chamber of "Our party does not have the necessary number of deputies Parliament. The parliamentary elections of 4 April failed to or partners to lead a stable government," said Slavi produce a stable government majority. Trifonov, who refused any alliance with traditional parties. The “Citizens for the European Development of Bulgaria” "The support offered to us comes from political factions (GERB), the party of outgoing Prime Minister Boyko that are harmful, greedy and proven to be compromised. Borisov, won 25.8% of the vote and 75 seats. "There is What they are offering is not support but dependence," Such a People" (Ima takuv narod, ITN), a populist party he said. Socialist Kornelia Ninova was no more fortunate founded by singer and TV presenter Slavi Trifonov, came in forming a government capable of running the country. second with 17.4% of the vote (51 seats). It was followed by Kornelia Ninova's Socialist Party (BSP), which secured The failure to come to agreement paved the way for a 14.79% of the vote and 43 deputies; the “Movement for new legislative election. Bulgarian electoral law provides Rights and Freedoms” (DPS), a party representing the for only three attempts to form a government after the Turkish minority led by Mustafa Karadayi, secured 10.36% elections. -

Parliamentary Elections Aftermath in Bulgaria | April 2021

PARLIAMENTARY ELECTIONS AFTERMATH IN BULGARIA: UNCERTAINTY & TURMOIL REIGN Results & possible scenarios 14 April 2021 Over a week has passed since Bulgaria’s parliamentary elections (held on 4 April), but the country remains at a political impasse, with the results showing no clear path to a new government and a new election remaining a distinct possibility. The only certainty is that a period of relative political stability is seemingly at an end, with a fragmented parliament and an opposition united only by their unwillingness to enter a coalition with the conservative former ruling party, GERB. Below we take a more detailed look at the election results and chart potential paths forward. ELECTION RESULTS Prior to the election, most polls predicted victory for long-time Prime Minister Boyko Borissov’s GERB party (Civil Movement for European Development of Bulgaria) with a low turnout among an electorate fatigued by years of government scandals1, the outbreak of mass protests and a response to the COVID-19 pandemic seen as disastrous by many. However, voter turnout was higher than expected (at 40.18% or 2,621,909 voters, it was consistent with recent elections), with long queues of voters forming in spite of the pandemic, particularly at polling stations abroad. Despite winning more votes than any other party, GERB is being depicted as the loser of these elections, since its share has dropped from a stable one-third to 26% of the vote. This is not only the party’s worst performance in over a decade but also brings an end to the GERB ruling hegemony and, rumours suggest, could even lead to a split within the party. -

Bulgaria Political Briefing: OVERVIEW of the POLITICAL 2019 YEAR for BULGARIA Evgeniy Kandilarov

ISSN: 2560-1601 Vol. 24, No. 1 (BG) Dec 2019 Bulgaria political briefing: OVERVIEW OF THE POLITICAL 2019 YEAR FOR BULGARIA Evgeniy Kandilarov 1052 Budapest Petőfi Sándor utca 11. +36 1 5858 690 Kiadó: Kína-KKE Intézet Nonprofit Kft. [email protected] Szerkesztésért felelős személy: Chen Xin Kiadásért felelős személy: Huang Ping china-cee.eu 2017/01 OVERVIEW OF THE POLITICAL 2019 YEAR FOR BULGARIA The political 2019 for Bulgaria was quite dynamic. During the year Bulgarian ruling party GERB has undergone serious problems and scandals that have undermined its political rating. Corruption scandals, clashes among the ruling coalition, criticism from Bulgarian President Rumen Radev and sharp attacks from the main opposition political force – BSP, represent only some of the problems faced by GERB and its Government. Despite some speculations at the beginning of the year that the government may not be able to complete its term due to a number of political scandals as well as a result of the possible lost in the elections that took place during the year, the situation at the end of the year shows relatively stable political position of the ruling governmental coalition. Bulgaria continues to be governed by the Third Government of the Prime Minister Boyko Borisov (also called the Government of Boyko Borisov III or Cabinet "Borisov III"). This is the ninety-sixth government of the Republic of Bulgaria, elected by the 44th National Assembly on May 4, 2017. The cabinet, headed by Boyko Borisov is a coalition formed by the Borisov’s right-wing party GERB and the so called United Patriots which is a nationalist electoral alliance formed by three political parties: IMRO – Bulgarian National Movement (IMRO), the National Front for the Salvation of Bulgaria (NFSB) and Attack. -

Republic of Bulgaria Council of Ministers Central Coordination Unit

Republic of Bulgaria Council of Ministers Central Coordination Unit Directorate National Focal Point STRATEGIC REPORT ON THE IMPLEMENTATION OF THE EEA FINANCIAL MECHANISM AND THE NORWEGIAN FINANCIAL MECHANISM 2009-2014 IN BULGARIA January – December 2016 Glossary of acronyms AA Audit Authority CA Certifying Authority CCU Central Coordination Unit CoE Council of Europe CoM Council of Ministers DPP Donor Programme Partner DSs Donor states EEA FM European Economic Area Financial Mechanism FBRNL Fund for Bilateral Relations at National Level FMO Financial Mechanism Office FO Fund Operator MCS Management and Control System MoU Memorandum of Understanding MRDPW Ministry of Regional Development and Public Works NAMRB National Association of Municipalities in the Republic of Bulgaria NGO Non‐governmental organization NFM Norwegian Financial Mechanism NFP National Focal Point PO Programme operator PDP Pre‐defined project TA Technical Assistance pps Purchasing Power Standards 2 1 EXECUTIVE SUMMARY The political, economic and social situation in Bulgaria in 2016 has been comparatively stable following a three‐year period of political turbulences and uncertainty. This allowed stakeholders in the management of EEA and Norway grants to perform their responsibilities and tasks during the crucial last full year of implementation in a more predictable and less risky environment. There were local elections in autumn of 2016 that were considered a risk for the projects with municipalities as project promoters but such risk did not occur. The Presidential elections that took place in November 2016 due to their nature were not expected to have a direct influence at the level of programmes and projects. Although the subsequent processes that were triggered had such potential, it was revealed in the beginning of 2017. -

POLIT-BAROMETER Compromising Statements and Smutty PR

ANALYSE DEMOCRACY AND HUMAN RIGHTS The upcoming campaign for the local elections will be ex- tremely intense, and full of POLIT-BAROMETER compromising statements and smutty PR. Year 19, Issue 3 July – September, 2019 GERB controls practically all of the local government in the country after its major elec- Georgi Karasimeonov (Ed.) tion success four years ago. The divisions in BSP after the European elections seem to have temporarily died down and the party is emerging rel- atively consolidated for the local votes. FRIEDRICH-EBERT-STIFTUNG – POLIT-BAROMETER DEMOCRACY AND HUMAN RIGHTS POLIT-BAROMETER Year 19, Issue 3 July – September, 2019 CONTENTS Contents 1. THE POLITICAL SITUATION 2 1.1 Internal policy .......................................................................................................... 2 1.2 Foreign and European policies .......................................................................... 5 1.3 Migration .................................................................................................................. 6 2. STATE AND DEVELOPMENT OF THE MAJOR POLITICAL PARTIES 8 2.1 Social Democratic and other centre-left parties .......................................... 8 2.2 Centre-right parties ............................................................................................... 9 2.3 Centrist parties ........................................................................................................ 10 2.4 Nationalist parties .................................................................................................