2020 Half Year Results Presentation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Full Year Statutory Accounts

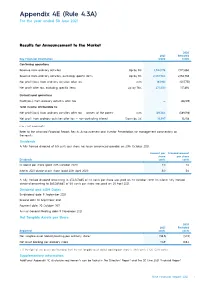

Appendix 4E (Rule 4.3A) For the year ended 30 June 2021 Results for Announcement to the Market 2020 2021 Restated Key Financial Information $’000 $’000 Continuing operations Revenue from ordinary activities Up by 8% 2,342,178 2,172,060 Revenue from ordinary activities, excluding specific items Up by 8% 2,332,984 2,156,785 Net profit/(loss) from ordinary activities after tax n/m 183,961 (507,751) Net profit after tax, excluding specific items Up by 76% 277,530 157,694 Discontinued operations Profit/(loss) from ordinary activities after tax — (66,189) Total income attributable to: Net profit/(loss) from ordinary activities after tax — owners of the parent n/m 169,364 (589,198) Net profit from ordinary activities after tax — non-controlling interest Down by 4% 14,597 15,258 n/m = not meaningful Refer to the attached Financial Report, Results Announcement and Investor Presentation for management commentary on the results. Dividends A fully franked dividend of 5.5 cents per share has been announced payable on 20th October 2021. Amount per Franked amount share per share Dividends cents cents Dividend per share (paid 20th October 2020) 2.0 2.0 Interim 2021 dividend per share (paid 20th April 2021) 5.0 5.0 A fully franked dividend amounting to $34,107,865 of 2.0 cents per share was paid on 20 October 2020. An interim fully franked dividend amounting to $85,269,663 of 5.0 cents per share was paid on 20 April 2021. Dividend and AGM Dates Ex-dividend date: 9 September 2021 Record date: 10 September 2021 Payment date: 20 October 2021 Annual General Meeting date: 11 November 2021 Net Tangible Assets per Share 2020 2021 Restated Reported cents cents Net tangible asset (deficit)/backing per ordinary share 1 (38.3) (40.9) Net asset backing per ordinary share 114.9 108.4 1. -

Streaming Yujin Luo Final

The Streaming War During the Covid-19 Pandemic Yujin Luo The Streaming War During the Covid-19 Pandemic 2 home, which is the ideal condition for The Covid-19 pandemic has drastically binge-watching. disrupted all business sectors. The arts, culture, and entertainment industries have To understand how the pandemic is shaping been hit exceptionally hard since the virus’ the streaming industry, it is important to first outbreak in January. In response to the understand its pre-Covid and current status. crisis, businesses have taken immediate The following analysis will divide the actions: transitioning to remote work, timeline into before 2020 and in 2020 based canceling and postponing live events on Covid-19’s first outbreak in January nationwide, shutting down entertainment 2020. venues, etc., resulting in lost revenues from sales, merchandising, advertising, and The Streaming Industry’s Pre-Covid promotions. Unfortunately, the Covid-19 State of the Major Players in the pandemic’s impacts are far more Streaming War permanent for an audience-oriented industry that requires a high level of Early adopters and fast followers used to be engagement. The business model might be the main audiences of streaming services, fundamentally changed and there will or in other words, streaming used to be a certainly be a shift in how content is niche add-on to traditional TV. Now, it is produced and consumed. transitioning to a new stage as a mainstream element in the entertainment While lockdowns and social distancing industry. The major streaming services from measures to contain the pandemic have before Covid are shown in the table below, had a huge impact on the traditional movie except for HBO Max, Peacock, and Quibi industry, the video streaming model seems (RIP) that just launched in 2020. -

Ofve' NEW RESIDENTIALCHANNEL LINEUP Effective 2/1 6/16

Odessa, TX CABLEOfVE' NEW RESIDENTIALCHANNEL LINEUP Effective 2/1 6/16 ECONOMY STAN DARD/ D I G ITAL VALU E PACK* xDigital Standard Cable includes Economy. Value Pack Channels noted in yellow. Additional fee applies. 3 455 ABC.KMID Women's Programming Fomily Programming "too7 .ll 'r,t'¡., I 7 cBs-KosA 1260 Animal Planet 100 1 100 Lifetime 260 B 475 FOX-KPEJ 1262 National Geographic Wild 102 1 102 LMN 262 9 1 009 NBC.KWES 103 OWN 263 1263 Discovery Channel Channel 13 1013 PB5-KPBT "t04 1 104 Bravo 26s 1265 Science Channel 16 1016 MyNetwork-KOSA 108 WE 266 1266 Hallmark 268 1264 Hallmark Movies & Mysteries 17 CW-KWES 112 lnvestigation DiscoverY 114 Oxygen 270 1270 Food Network 1B 1018 Univision-KUPB 1"16 Discovery Life 272 1272 HGTV 20 Telemundo-KTLE 274 1274 History Channel 2',! Galavision Sports 276 1276 H2 (Viceland) 22 UniMas 133 1 133 ESPN 277 1277 National Geographic Ch. '134 "t134 25 MeTV-KWWT ESPN2 241 Travel Channel 135 ESPN News 26 Decades 136 ESPNU Ch il dren's Proqra m m i n q 27 Movies 1 NBC Sports 137 137 300 1 300 Sprout 52 God's Learning Channel-KMLM "t39 ',t39 1 CBS Sports 302 1302 Disney Channel 56 Goverment Access 140 FCS Atlantic 304 Disney XD '141 72 Leased Access FCS Central 307 1307 FreeForm FCS Pacific 7B C-SPAN 142 311 Discovery Family 146 1146 FOX Sports 1 79 C-SPAN2 313 Disney Jr. 144 1 144 FOX Sports 2 Boomerang BO BYU 316 1 FOX Sports SW 155 155 317 1317 Cartoon Network 82 INSP 157 1157 NFL Network TBN 1 Golf Channel B4 158 158 News 85 EWTN 160 1 160 Outdoor €hannel 333 TheWeather Channel 161 ESPN Classic B6 -

1 Transcript of 2019 Nine Entertainment AGM Sydney

1 Transcript of 2019 Nine Entertainment AGM Sydney, November 12, 2019 Chairman Peter Costello Good morning ladies and gentleman. As your Chairman, it's my pleasure to welcome you to the 2019 AGM of Nine Entertainment Company. My name is Peter Costello. Before opening the meeting, I refer you to the disclaimer here on the screen behind me and available through our ASX lodgement. It is now shortly after 10am and I am advised that this is a properly constituted meeting. There's a quorum of at least two shareholders present so I declare the 2019 Annual General Meeting open. Unless there are any objections, I propose to take the Notice of Meeting as read. Copies of the Notice of Meeting are available from the registration desk outside should you require them. Let me now introduce the people who are with us this morning. To my immediate left is Rachel Launders, our General Counsel and Company Secretary. Then Hugh Marks, our Chief Executive Officer, who will address the meeting a little later. Next to Hugh is Nick Falloon, the Independent, Non-Executive Director and Deputy Chair and Member of the People and Remuneration Committee. Then we have Patrick Alloway, Independent, Non-Executive Director and a member of the Audit and Risk Management Committee. Next to Patrick is Sam Lewis, Independent, Non-Executive Director, Chair of the Audit and Risk Committee and a Member of the People and Remuneration Committee. Then we have Mickie Rosen, Independent, Non-Executive Director. At the far end, we have Catherine West, Independent, Non-Executive Director, the Chair of the People and Remuneration Committee and a member of the Audit and Risk Committee. -

2020 Full Year Results Announcement

27 August 2020 ASX Markets Announcement Office ASX Limited 20 Bridge Street Sydney NSW 2000 2020 FULL YEAR RESULTS ANNOUNCEMENT Attached is a copy of the ASX release relating to the 2020 Full Year Financial Results for Nine Entertainment Co. Holdings Limited Rachel Launders Company Secretary Authorised for release: Nine Board sub-committee Further information: Nola Hodgson Victoria Buchan Head of Investor Relations Director of Communications +61 2 9965 2306 +61 2 9965 2296 [email protected] [email protected] nineforbrands.com.au Nine Sydney - 1 Denison Street, North Sydney, NSW, 2068 ABN 60 122 203 892 NINE ENTERTAINMENT CO. FY20 FINAL RESULTS 27 August 2020: Nine Entertainment Co. (ASX: NEC) has released its FY20 results for the 12 months to June 2020. On a Statutory basis, Nine reported Revenue of $2.2b and a Net Loss of $575m, which included a post-tax Specific Item cost of $665m, largely relating to impairment of goodwill. On a pre AASB16 and Specific Item basis, Nine reported Group EBITDA of $355m, down 16% on the Pro Forma results in FY19 for its Continuing Businesses. On the same basis, Net Profit After Tax and Minority Interests was $160m, down 19%. Key takeaways include: • Audience growth across all key platforms – Metro Publishing, Stan, 9Now, Radio and FTA • Strong growth from digital video businesses o $51m EBITDA improvement at Stan1, with current active subscribers of 2.2m o 36% EBITDA growth at 9Now1 to $49m, with market leading BVOD revenue share of ~50% • Ad markets heavily impacted by COVID-19 from March 2020 • Nine was quick to mitigate the associated fallout with o $225m cost-out program – cash basis, CY20 o Including increasing and expediting previous cost initiatives • 40% growth in digital EBITDA to $166m ($178m post AASB16) • Evolution of Metro Media business to consumer focus, with reader revenue now accounting for almost 60% of total revenue • Strong balance sheet, with (wholly-owned) leverage ratio <1X 1 like-basis, pre AASB16 Hugh Marks, Chief Executive Officer of Nine Entertainment Co. -

Comcast Channel Lineup

• Basi.c Service , $ 14.99 Equipment and Options (prices per month) The minimum level of service available and is required before you HOTV Equipment Charge~ ... .., ...............•.........$ 7.00 can subscribe to additional services, HO OVR Service .................•........................$ 15.95 SO DVR Service ..................................•........$ 8.95 Starter Cable , $ 55.99 Digital/Analog Converter . .. .....................•........$ 3.20 Includes Starter Cable channels plus OCT & Remote. Analog Converter for Basic Service Only ......•............ " .$ 1.00 Digital/Analog Remote Control . .•.......•.. ,... .$ 0.20 Digital Preferred ,,,,, $ 16.95 This package can be added to Starter Cable and includes the Installation and Service' channels in Digital Classic. Home Installation (Wired) ......., .......•........ , .$ 23.99 Home InstaiJation (Unwired) ............................•... .$ 33.99 Digital Preferred Plus Package , $ 107.99 Additional Connection at Time of Imliallnstall , $ 12.99 Includes the channels in Starter Cable. Digital Classic, and HBO Additional Connection Requiring Separate Trip ..........•.....$ 20.99 and STARZl. Move Outlet ........................................•. , ..$ 16.99 Upgrade of Services _.......•.. , ..$ 14.99 Digital Premier Package , ,.$ 127,99 Downgrade of Services ,... .. , ..........•.........•....$ 10.95 Includes the channels in Starter Cable, Digital Classic, Sports Change of Service or Equipment Activation ........•......•.....$ 1.99 Entertainment Tier, HBO, Showtime, Cinemax and Starzl. Connect VCR at Time of InitiallnstaiJ $ 5.99 Connect VCR Requiring Separate Trip .................•......$ 12.99 Digital Premium Services. ,,,,, $ 19.99 Hourly Service Charge. .........,.. $ 30.99 Premium services can be added to any Digital package, Select Service Call Trip Charge ........ $ 27.20 from HBO, Showtime, Cinemax, The Movie Channel, STARZI Administrative Fee for Delinquent Accounts at 30 Days $ 5.95 or E(1core. Administrative Fee for Delinquent Accounts at 60 Days ,$ 5.95 Additional Late Fee Every 30 Days After. -

MUSIC & VIDEO MULTIPLEX SERVICES MOVIE LOVERS Stingray Music

MUSIC & VIDEO CH PROGRAMMING MOVIE LOVERS 890 MTV2 HD 891 CMT Music CH PROGRAMMING 892 MTV Classic 294 STARZ HD 414 STARZ ENCORE 893 BET Soul 400 IFC HD Westerns E 415 894 NickMusic 404 STARZ ENCORE E HD STARZ ENCORE Westerns W 405 STARZ ENCORE W HD 416 STARZ E HD 406 STARZ ENCORE Action E HD StingRay Music 417 STARZ W HD 407 STARZ ENCORE Action W CH PROGRAMMING 418 STARZ Edge E HD 408 STARZ ENCORE Classic E 419 STARZ Edge W 901 Adult Alternative 927 Kids Stuff 409 STARZ ENCORE Classic W What Do I Do When... 420 STARZ In Black HD 902 Alt Rock Classics 928 Latino Tropical 410 STARZ ENCORE Suspense E 421 STARZ Kids & Family HD 903 Bluegrass 929 Latino Urbana 411 STARZ ENCORE Suspense W MY CABLE IS OUT 422 STARZ Comedy HD 904 Broadway 930 Maximum Party Do you have more than 1 television hooked up to 412 STARZ ENCORE Black E HD 423 STARZ Cinema HD 905 Chamber Music 931 Nothing But 90’s cable? 413 STARZ ENCORE Black W 906 Classic Rock 932 No Fences If there is a cable outage, all tv’s will be out. If 907 Classic R&B & Soul 933 Pop Adult one tv is working, it may be a problem with the televi- 908 Classic Masters 934 Pop Classics sion or a wire in the house. 909 Country Classics 935 Retro Latino MULTIPLEX SERVICES Do you have a DVD player? 910 Dance Clubbin 936 Rock If so, it may be turned on. Turn the device off. -

April 2009 Bulletinfeature Articles | Interviews | News | Book Reviews | Calendar L 2009 Meteorological Services E 58 (2) - APRI

Vol. 58 (2) - April 2009 BulletinFeature articles | Interviews | News | Book reviews | Calendar www.wmo.int 2009 L Meteorological services 58 (2) - APRI E VOLUM for transportation Meteorology and marine transportation 111 Weather monitoring and etin forecasting services for BULL provincial highways and MO railways in China W 118 World Meteorological Organization 7bis, avenue de la Paix - Case postale 2300 - CH-1211 Geneva 2 - Switzerland Tel.: +41 (0) 22 730 81 11 - Fax: +41 (0) 22 730 81 81 E-mail: [email protected] - Website: www.wmo.int Weather and climate change ISSN 0042-9767 implications for surface transportation in the USA 84 Meteorological services to aviation 94 Meteorology for travellers 104 Weather affects the operation of the transportation systems that we all rely on ... Climate, on the other hand, affects transportation infrastructure. M. McGuirk et al. Bulletin The journal of the Contents World Meteorological Organization In this issue .......................................................................................... 80 Volume 58 (2) - Avril 2009 World Climate Conference-3 .............................................................. 82 Secretary-General M. Jarraud Weather and climate change implications for surface Deputy Secretary-General Hong Yan transportation in the USA by Marjorie McGuirk, Scott Shuford, Assistant Secretary-General J. Lengoasa Thomas C. Peterson and Paul Pisano ............................................................... 84 The WMO Bulletin is published quarterly (January, April, July, October) in English, French, Meteorological services to aviation by Chi Ming Shun, Ian Lisk, Russian and Spanish editions. Carr McLeod and Kevin L. Johnston ............................................................ 94 Editor Hong Yan Associate Editor Judith C.C. Torres Meteorology for travellers by S.T. Christopher ........................................ 104 Editorial board Hong Yan (Chair) Meteorology and marine transportation by Peter Dexter and J. -

Engineers Australia Sydney Division Water Engineering Panel

Engineers Australia Sydney Division Water Engineering Panel REAL-TIME QUANTITATIVE RAINFALL FORECASTING WHERE ARE WE AND WHERE ARE WE HEADING Abstract: Weather prediction and specifically forecasting rainfall in the near term has made significant strides in the last decade. This has largely been due to advances in science and computer power, with several agencies commanding supercomputers in the top 50 in the world. However, rainfall still remains one of the most difficult parameters to forecast even out to 12 hours. The intrinsic problems with forecasting rainfall over other such parameters such as temperature and winds, is its often very chaotic nature both temporally and geographically. Even with global supercomputers modelling at greater resolutions, few are capable of providing the pinpoint accuracy often required by rainfall sensitive industries and projects. The aim of this talk is to provide an industry-wide overview on current science and forecasting techniques with regard to rainfall, with a special focus on the very latest techniques for trying to improve and correct forecast data provided by the global computer models. The example of the Chatswood Integrated Flood Control and Stormwater Reuse Scheme shall be used as a case study of how such techniques may be applied to vastly enhance rainfall forecasting accuracy. In addition, the talk will touch on how these forecast techniques can be used across the industry as a whole, as well as a quick look into expected future developments. Speaker Bio: Martin Palmer spent nine years in the British Royal Navy as a Warfare Officer, specialising as a Meteorologist, Oceanographer and Hydrographic Surveyor. -

Hulu Website Table of Contents

Hulu Website Table of Contents Hulu Website.................................................................................................................................................. 4 Pages........................................................................................................................................................... 5 /.................................................................................................................................................................. 9 all-my-children............................................................................................................................................10 american-dad............................................................................................................................................. 11 arrested-development................................................................................................................................ 12 bec..............................................................................................................................................................13 better-off-ted...............................................................................................................................................14 beverly-hills-cop-iii......................................................................................................................................15 bones..........................................................................................................................................................16 -

New Zealand Weather and Climate News Courtesy of Metservice

New Zealand weather and climate news Courtesy of MetService Library MetService focus Enjoy that sunshine - there's a wintry snap looming MetService has issued snowfall warnings for Milford Rd tomorrow while Tuesday will see more road snow, including on the Desert Rd. Westland and ... 832 lightning strikes in 24 hours as storm batters New Zealand There were 832 strikes recorded over both land and sea in the 24 hours from 8.15am on Wednesday, according to MetService. Of those, 368 occurred ... Snow and ice close South Island highways after wild weather Over the country, MetService issued snowfall warnings for six highways - Napier-Taupo Rd, Desert Rd, Lewis Pass, Arthur's Pass, Milford Rd and ... West coast towns left off draft Metservice website map Otago Daily Times Metservice communications meteorologist Lewis Ferris said although Greymouth and Hokitika were not on the current beta homepage map, people ... Scientists receive funding Alexandra's scientific community is making headway and two local organisations have been part of successful grants in this year's Ministry of Business, Innovation and Employment Endeavour Fund. Bodeker Scientific is part of a consortium led by Victoria University that has been granted $10,273,285 for a five-year project on extreme events and the emergence of climate change. Spring cold-snap likely to last for rest of week MetService meteorologist Tui McInnes said "as exciting as it would be" to have the southern stratospheric warming affecting local weather, its effects ... Southerly winds moving over country set to 'pack a punch' Stuff.co.nz ... the day, the front was expected to deliverwinds of up to 55 kmh and gusts of up to 85kmh, according to MetService meteorologist Tui McInnes. -

OTT Streaming Wars: Raise Or Fold

OTT Streaming Wars: Raise or Fold How Data is Reshuffling the Cards of the M&E Industry Content 01 02 03 OTT Streaming Media Players Efficient Data Use Shakes-up the Need Data Increases M&E Industry Integration for Competitivity Survival OTT is fast becoming the main The core business of media and In fact, 67% of all interviewees form of content consumption entertainment companies is declared data to be business now challenged critical for survival Multiplication of services drives fragmentation Content is King, but DATA Data as key lever for OTT business emerges as key sucess factor Streaming Wars’ players race for subscribers Advertising-based model accelerates the industry's entry into a new era Consolidation and new opportunities for aggregators 2 OTT Streaming Wars 04 05 06 Two Out of Three Best Practices of Conclusion: Players Reach Leaders Help Raise the Only Basic Levels Overcome Maturity Stakes or Fold of Data Maturity Challenges Fully leveraging the power of data Decide to set data at the core The direction is set towards requires work on multiple streams of the strategy across the full a Data-powered Media & at the same time CxO suite Entertainment Industry Despite data being business Build an environment of trust and Acceleration is required to critical, two out of three media integrate it in the brand promise stay relevant and attractive for and entertainment companies subscribers, content providers reach only a basic level of Address users not audiences or advertisers data-maturity. Work on culture and skill sets to Becoming