The New Deal and the New New Deal : a Comparative Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

ISFIRE an Exclusive Interview With: Islamic Nancereview.Co

Special Focus on Risk and Trust in Islamic Banking & Finance ISFIRE An Exclusive Interview with: islamicnancereview.co DATO’ ADNAN ALIAS Volume 4 - Issue 4 | November 2014 - £20 CEO, IBFIM A Special Report on GLOBAL ISLAMIC FINANCE AWARDS 2014 Sponsored by: Published by: ibm.com edbizconsulting.com EDBIZ CORPORATION Product Development Shari’a Advisory Edbiz Consulting (London) Edbiz Research & Analysis Edbiz Corporation Consulting (Pakistan) Publications Training & Conferences Our products and services are underpinned by a common goal: promoting and advocating the ethical values inherent in Islamic nance Edbiz Consulting is a truly unique, international Islamic nance think tank, committed to engendering the value proposition that Islamic nance serves to oer in the global nancial markets. Edbiz Consulting provides multiple services that balance the dual purpose of developing thought leadership in this niche industry and strengthening the Islamic nance capacity for businesses and banks. Our client base is diverse and includes nancial institutions, governments, education providers, established businesses and entrepreneurs. Global Islamic Finance ISFIRE Report islamicnancereview.co 2015 ISLAMIC FINANCE LEADERSHIP PROGRAMME www.edbizconsulting.com ’ala Wa’d Gha l Ju rar M Visit us on: www.gifr.net afu ai ak sa at anking Mud r R c B a ib an ic at Mu ra a B ba Zak amlat b m r Ri Taw a Z l a isa ar a fu l a ru M k a Is M q a ar Is u t k r la a e ha m d M T G - c ic a u d F e n ’ i r a a n i m R a W a b n l a c l n l e a u i a ’ t f I R u s a -

Why We Worry Top-Down and Invest Bottom-Up

“Remember that there is nothing stable in human affairs; therefore avoid undue elation in prosperity or undue depression in adversity.” —Socrates, 399 B.C. “In the economy, an act, a habit, an institution, a law, gives birth not only to an effect, but to a series of effects. Of these effects, the first only is immediate; it manifests itself simultaneously with its cause— it is seen. The others unfold in succession— they are not seen: it is well for us if they are foreseen.” —Frederic Bastiat, That Which Is Seen, That Which Is Unseen , 1850 “Res nolunt diu male administrari . Things refuse to be mismanaged long. Though no checks to a new evil appear, the checks exist, and will appear.” —Ralph Waldo Emerson, 1844 “Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, and one by one.”—Charles Mackay, Extraordinary Popular Delusions and the Madness of Crowds , 1912 2014 ANNUAL REPORT _______________________________________________________ For further information, contact Chris Ridenour at (574) 293-2077 or via email at [email protected] 1 Why We Worry Top-Down and Invest Bottom-Up “A rising tide lifts all ships” is bandied about in our profession like a shuttlecock at a garden party badminton game. It seems that whenever an analogy is that simple and quaint, there must be a catch. And there is: the waves. In their endless repetition they mask the invisible but prodigious ebb and flood tides. The daily headlines are almost always about the waves, particularly, even if unnoticed, when the tide is rising. -

Apartment Buildings in New Haven, 1890-1930

The Creation of Urban Homes: Apartment Buildings in New Haven, 1890-1930 Emily Liu For Professor Robert Ellickson Urban Legal History Fall 2006 I. Introduction ............................................................................................................................. 1 II. Defining and finding apartments ............................................................................................ 4 A. Terminology: “Apartments” ............................................................................................... 4 B. Methodology ....................................................................................................................... 9 III. Demand ............................................................................................................................. 11 A. Population: rise and fall .................................................................................................... 11 B. Small-scale alternatives to apartments .............................................................................. 14 C. Low-end alternatives to apartments: tenements ................................................................ 17 D. Student demand: the effect of Yale ................................................................................... 18 E. Streetcars ........................................................................................................................... 21 IV. Cultural acceptance and resistance .................................................................................. -

C H a P T E R 24 the Great Depression and the New Deal

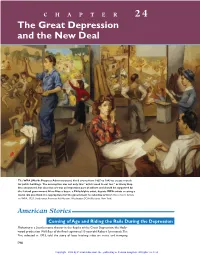

NASH.7654.CP24.p790-825.vpdf 9/23/05 3:26 PM Page 790 CHAPTER 24 The Great Depression and the New Deal The WPA (Works Progress Administration) hired artists from 1935 to 1943 to create murals for public buildings. The assumption was not only that “artists need to eat too,” as Harry Hop- kins announced, but also that art was an important part of culture and should be supported by the federal government. Here Moses Soyer, a Philadelphia artist, depicts WPA artists creating a mural. Do you think it is appropriate for the government to subsidize artists? (Moses Soyer, Artists on WPA, 1935. Smithsonian American Art Museum, Washington DC/Art Resource, New York) American Stories Coming of Age and Riding the Rails During the Depression Flickering in a Seattle movie theater in the depths of the Great Depression, the Holly- wood production Wild Boys of the Road captivated 13-year-old Robert Symmonds.The film, released in 1933, told the story of boys hitching rides on trains and tramping 790 NASH.7654.CP24.p790-825.vpdf 9/23/05 3:26 PM Page 791 CHAPTER OUTLINE around the country. It was supposed to warn teenagers of the dangers of rail riding, The Great Depression but for some it had the opposite effect. Robert, a boy from a middle-class home, al- The Depression Begins ready had a fascination with hobos. He had watched his mother give sand- Hoover and the Great Depression wiches to the transient men who sometimes knocked on the back door. He had taken to hanging around the “Hooverville” shantytown south of Economic Decline the King Street railroad station, where he would sit next to the fires and A Global Depression listen to the rail riders’ stories. -

5 the Da Vinci Code Dan Brown

The Da Vinci Code By: Dan Brown ISBN: 0767905342 See detail of this book on Amazon.com Book served by AMAZON NOIR (www.amazon-noir.com) project by: PAOLO CIRIO paolocirio.net UBERMORGEN.COM ubermorgen.com ALESSANDRO LUDOVICO neural.it Page 1 CONTENTS Preface to the Paperback Edition vii Introduction xi PART I THE GREAT WAVES OF AMERICAN WEALTH ONE The Eighteenth and Nineteenth Centuries: From Privateersmen to Robber Barons TWO Serious Money: The Three Twentieth-Century Wealth Explosions THREE Millennial Plutographics: American Fortunes 3 47 and Misfortunes at the Turn of the Century zoART II THE ORIGINS, EVOLUTIONS, AND ENGINES OF WEALTH: Government, Global Leadership, and Technology FOUR The World Is Our Oyster: The Transformation of Leading World Economic Powers 171 FIVE Friends in High Places: Government, Political Influence, and Wealth 201 six Technology and the Uncertain Foundations of Anglo-American Wealth 249 0 ix Page 2 Page 3 CHAPTER ONE THE EIGHTEENTH AND NINETEENTH CENTURIES: FROM PRIVATEERSMEN TO ROBBER BARONS The people who own the country ought to govern it. John Jay, first chief justice of the United States, 1787 Many of our rich men have not been content with equal protection and equal benefits , but have besought us to make them richer by act of Congress. -Andrew Jackson, veto of Second Bank charter extension, 1832 Corruption dominates the ballot-box, the Legislatures, the Congress and touches even the ermine of the bench. The fruits of the toil of millions are boldly stolen to build up colossal fortunes for a few, unprecedented in the history of mankind; and the possessors of these, in turn, despise the Republic and endanger liberty. -

The Skyscraper Curse Th E Mises Institute Dedicates This Volume to All of Its Generous Donors and Wishes to Thank These Patrons, in Particular

The Skyscraper Curse Th e Mises Institute dedicates this volume to all of its generous donors and wishes to thank these Patrons, in particular: Benefactor Mr. and Mrs. Gary J. Turpanjian Patrons Anonymous, Andrew S. Cofrin, Conant Family Foundation Christopher Engl, Jason Fane, Larry R. Gies, Jeff rey Harding, Arthur L. Loeb Mr. and Mrs. William Lowndes III, Brian E. Millsap, David B. Stern Donors Anonymous, Dr. John Bartel, Chris Becraft Richard N. Berger, Aaron Book, Edward Bowen, Remy Demarest Karin Domrowski, Jeff ery M. Doty, Peter J. Durfee Dr. Robert B. Ekelund, In Memory of Connie Th ornton Bill Eaton, Mr. and Mrs. John B. Estill, Donna and Willard Fischer Charles F. Hanes, Herbert L. Hansen, Adam W. Hogan Juliana and Hunter Hastings, Allen and Micah Houtz Albert L. Hunecke, Jr., Jim Klingler, Paul Libis Dr. Antonio A. Lloréns-Rivera, Mike and Jana Machaskee Joseph Edward Paul Melville, Matthew Miller David Nolan, Rafael A. Perez-Mera, MD Drs. Th omas W. Phillips and Leonora B. Phillips Margaret P. Reed, In Memory of Th omas S. Reed II, Th omas S. Ross Dr. Murray Sabrin, Henri Etel Skinner Carlton M. Smith, Murry K. Stegelmann, Dirck W. Storm Zachary Tatum, Joe Vierra, Mark Walker Brian J. Wilton, Mr. and Mrs. Walter F. Woodul III The Skyscraper Curse And How Austrian Economists Predicted Every Major Economic Crisis of the Last Century M ARK THORNTON M ISESI NSTITUTE AUBURN, ALABAMA Published 2018 by the Mises Institute. Th is work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivs 4.0 International License. http://creativecommons.org/licenses/by-nc-nd/4.0/ Mises Institute 518 West Magnolia Ave. -

Chapter 18: Roosevelt and the New Deal, 1933-1939

Roosevelt and the New Deal 1933–1939 Why It Matters Unlike Herbert Hoover, Franklin Delano Roosevelt was willing to employ deficit spending and greater federal regulation to revive the depressed economy. In response to his requests, Congress passed a host of new programs. Millions of people received relief to alleviate their suffering, but the New Deal did not really end the Depression. It did, however, permanently expand the federal government’s role in providing basic security for citizens. The Impact Today Certain New Deal legislation still carries great importance in American social policy. • The Social Security Act still provides retirement benefits, aid to needy groups, and unemployment and disability insurance. • The National Labor Relations Act still protects the right of workers to unionize. • Safeguards were instituted to help prevent another devastating stock market crash. • The Federal Deposit Insurance Corporation still protects bank deposits. The American Republic Since 1877 Video The Chapter 18 video, “Franklin Roosevelt and the New Deal,” describes the personal and political challenges Franklin Roosevelt faced as president. 1928 1931 • Franklin Delano • The Empire State Building 1933 Roosevelt elected opens for business • Gold standard abandoned governor of New York • Federal Emergency Relief 1929 Act and Agricultural • Great Depression begins Adjustment Act passed ▲ ▲ Hoover F. Roosevelt ▲ 1929–1933 ▲ 1933–1945 1928 1931 1934 ▼ ▼ ▼ ▼ 1930 1931 • Germany’s Nazi Party wins • German unemployment 1933 1928 107 seats in Reichstag reaches 5.6 million • Adolf Hitler appointed • Alexander Fleming German chancellor • Surrealist artist Salvador discovers penicillin Dali paints Persistence • Japan withdraws from of Memory League of Nations 550 In this Ben Shahn mural detail, New Deal planners (at right) design the town of Jersey Homesteads as a home for impoverished immigrants. -

Stopping Contagion with Bailouts: Microevidence from Pennsylvania Bank Networks During the Panic of 1884

16-03 | March 30, 2016 Stopping Contagion with Bailouts: Microevidence from Pennsylvania Bank Networks During the Panic of 1884 John Bluedorn International Monetary Fund [email protected] Haelim Park Office of Financial Research [email protected] The Office of Financial Research (OFR) Working Paper Series allows members of the OFR staff and their coauthors to disseminate preliminary research findings in a format intended to generate discussion and critical comments. Papers in the OFR Working Paper Series are works in progress and subject to revision. Views and opinions expressed are those of the authors and do not necessarily represent official positions or policy of the OFR or Treasury. Comments and suggestions for improvements are welcome and should be directed to the authors. OFR working papers may be quoted without additional permission. Stopping Contagion with Bailouts: Microevidence from Pennsylvania Bank Networks During the Panic of 1884 John Bluedorn1 International Monetary Fund Haelim Park2 Office of Financial Research March 30, 2016 Forthcoming in the Journal of Banking and Finance Abstract Using a newly constructed historical dataset on the Pennsylvania state banking system, detailing the amounts of “due-froms” on a debtor-bank-by-debtor-bank basis, we investigate the effects of the Panic of 1884 and subsequent private sector-orchestrated bailout of systemically important banks (SIBs) on the broader banking sector. We find evidence that Pennsylvania banks with larger direct interbank exposures to New York City changed the composition of their asset holdings, shifting from loans to more liquid assets and reducing their New York City correspondent deposits in the near-term. -

Academic Search Complete

Academic Search Complete Pavadinimas Prenumerata nuo Prenumerata iki Metai nuo Metai iki 1 Technology times 2021-04-01 2021-12-31 20140601 20210327 2 Organization Development Review 2021-04-01 2021-12-31 20190101 3 PRESENCE: Virtual & Augmented Reality 2021-04-01 2021-12-31 20180101 4 Television Week 2021-04-01 2021-12-31 20030310 20090601 5 Virginia Declaration of Rights and Cardinal Bellarmine 2021-04-01 2021-12-31 6 U.S. News & World Report: The Report 2021-04-01 2021-12-31 20200124 7 Education Journal Review 2021-04-01 2021-12-31 20180101 8 BioCycle CONNECT 2021-04-01 2021-12-31 20200108 9 High Power Computing 2021-04-01 2021-12-31 20191001 10 Economic Review (Uzbekistan) 2021-04-01 2021-12-31 20130801 11 Civil Disobedience 2021-04-01 2021-12-31 12 Appeal to the Coloured Citizens of the World 2021-04-01 2021-12-31 13 IUP Journal of Environmental & Healthcare Law 2021-04-01 2021-12-31 14 View of the Revolution (Through Indian Eyes) 2021-04-01 2021-12-31 15 Narrative of Her Life: Mary Jemison 2021-04-01 2021-12-31 16 Follette's Platform of 1924 2021-04-01 2021-12-31 17 Dred Scott, Plaintiff in Error, v. John F. A. Sanford 2021-04-01 2021-12-31 18 U.S. News - The Civic Report 2021-04-01 2021-12-31 20180928 20200117 19 Supreme Court Cases: The Twenty-first Century (2000 - Present) 2021-04-01 2021-12-31 20 Geophysical Report 2021-04-01 2021-12-31 21 Adult Literacy 2021-04-01 2021-12-31 2000 22 Report on In-Class Variables: Fall 1987 & Fall 1992 2021-04-01 2021-12-31 2000 23 Report of investigation : the Aldrich Ames espionage case / Permanent Select Committee on Intelligence,2021-04-01 U.S. -

Franklin Roosevelt's Advisory System: the Institutionalization of the Executive Office of the Esidentpr

University of Nebraska at Omaha DigitalCommons@UNO Student Work 7-1-1974 Franklin Roosevelt's advisory system: The institutionalization of the Executive office of the esidentPr James C. Rowling University of Nebraska at Omaha Follow this and additional works at: https://digitalcommons.unomaha.edu/studentwork Recommended Citation Rowling, James C., "Franklin Roosevelt's advisory system: The institutionalization of the Executive office of the President" (1974). Student Work. 488. https://digitalcommons.unomaha.edu/studentwork/488 This Thesis is brought to you for free and open access by DigitalCommons@UNO. It has been accepted for inclusion in Student Work by an authorized administrator of DigitalCommons@UNO. For more information, please contact [email protected]. FRANKLIN ROOSEVELT*S ADVISORY SYSTEM: THE INSTITUTIONALIZATION OF THE EXECUTIVE OFFICE OF THE PRESIDENT A Thesis Presented to the Department of Political Science and the Faculty of the Graduate College University of Nebraska at Omaha In Partial Fulfillment of the Requirements for the Degree Master of Arts by James C. Rowling July, 197^ 1 UMI Number: EP73126 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a complete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. UMI EP73126 Published by ProQuest LLC (2015). Copyright in the Dissertation held by the Author. Microform Edition © ProQuest LLC. All rights reserved. This work is protected against unauthorized copying under Title 17, United States Code ProQuest LLC. -

The Rising Thunder El Nino and Stock Markets

THE RISING THUNDER EL NINO AND STOCK MARKETS: By Tristan Caswell A Project Presented to The Faculty of Humboldt State University In Partial Fulfillment of the Requirements for the Degree Master of Business Administration Committee Membership Dr. Michelle Lane, Ph.D, Committee Chair Dr. Carol Telesky, Ph.D Committee Member Dr. David Sleeth-Kepler, Ph.D Graduate Coordinator July 2015 Abstract THE RISING THUNDER EL NINO AND STOCK MARKETS: Tristan Caswell Every year, new theories are generated that seek to describe changes in the pricing of equities on the stock market and changes in economic conditions worldwide. There are currently theories that address the market value of stocks in relation to the underlying performance of their financial assets, known as bottom up investing, or value investing. There are also theories that intend to link the performance of stocks to economic factors such as changes in Gross Domestic Product, changes in imports and exports, and changes in Consumer price index as well as other factors, known as top down investing. Much of the current thinking explains much of the current movements in financial markets and economies worldwide but no theory exists that explains all of the movements in financial markets. This paper intends to propose the postulation that some of the unexplained movements in financial markets may be perpetuated by a consistently occurring weather phenomenon, known as El Nino. This paper intends to provide a literature review, documenting currently known trends of the occurrence of El Nino coinciding with the occurrence of a disturbance in the worldwide financial markets and economies, as well as to conduct a statistical analysis to explore whether there are any statistical relationships between the occurrence of El Nino and the occurrence of a disturbance in the worldwide financial markets and economies. -

Friday, June 21, 2013 the Failures That Ignited America's Financial

Friday, June 21, 2013 The Failures that Ignited America’s Financial Panics: A Clinical Survey Hugh Rockoff Department of Economics Rutgers University, 75 Hamilton Street New Brunswick NJ 08901 [email protected] Preliminary. Please do not cite without permission. 1 Abstract This paper surveys the key failures that ignited the major peacetime financial panics in the United States, beginning with the Panic of 1819 and ending with the Panic of 2008. In a few cases panics were triggered by the failure of a single firm, but typically panics resulted from a cluster of failures. In every case “shadow banks” were the source of the panic or a prominent member of the cluster. The firms that failed had excellent reputations prior to their failure. But they had made long-term investments concentrated in one sector of the economy, and financed those investments with short-term liabilities. Real estate, canals and railroads (real estate at one remove), mining, and cotton were the major problems. The panic of 2008, at least in these ways, was a repetition of earlier panics in the United States. 2 “Such accidental events are of the most various nature: a bad harvest, an apprehension of foreign invasion, the sudden failure of a great firm which everybody trusted, and many other similar events, have all caused a sudden demand for cash” (Walter Bagehot 1924 [1873], 118). 1. The Role of Famous Failures1 The failure of a famous financial firm features prominently in the narrative histories of most U.S. financial panics.2 In this respect the most recent panic is typical: Lehman brothers failed on September 15, 2008: and … all hell broke loose.