ACI Main Presentation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Saxo Bank's BEST EXECUTION POLICY

SAXO BANK’S BEST EXECUTION POLICY SAXO BANK’S BEST EXECUTION POLICY THE SPECIALIST IN TRADING AND INVESTMENT Page 1 of 6 Page 1 of 6 SAXO BANK’S BEST EXECUTION POLICY 2.2 The trading conditions for the above products 1 INTRODUCTION are available on Saxo Bank’s different web- sites. 1.1 This policy is issued pursuant to, and in com- pliance with, EU Directive 2004/39/EC of 21 3 SAXO BANK’S APPROACH TO BEST EXE- April 2004 on Markets in Financial Instruments CUTION ("MiFID") and the Danish legislation imple- menting MiFID (the "Rules") that applies to 3.1 When executing orders Saxo Bank will take all Saxo Bank. reasonable steps to obtain the best possible result under the circumstances for the client 1.2 This policy provides an overview of how Saxo taking into account price, costs, speed, likeli- Bank executes orders on behalf of clients, the hood of execution and settlement, size, nature factors that can affect the timing of execution or any other consideration relevant to the exe- and the way in which market volatility plays a cution of the order ("Best Execution"). part in handling orders when buying or selling a financial instrument. 3.2 When considering the best executing factors, Saxo Bank takes into account: 1.3 This policy applies to Saxo Bank's execution of orders on behalf of retail clients and profes- the characteristics of the client order; sional clients as defined by the Rules. the characteristics of the financial instru- ments that are subject to that order (in 1.4 Where Saxo Bank provides a quote to a client particular in relation to OTC financial in- or negotiates the terms of an Over-the-Counter struments); and ("OTC") transaction with Saxo Bank as coun- the characteristics of the execution ven- terparty, Saxo Bank will normally not be acting ues to which that order can be directed. -

Annual Report

Annual Report 2006–2007 Group of Thirty 30 Group of Thirty, Washington, DC Copies of this paper are available from: Group of Thirty 1726 M Street, N.W., Suite 200 Washington, DC 20036 Tel.: (202) 331-2472, Fax (202) 785-9423 E-mail: [email protected] WWW: http://www.group30.org Annual Report 2006–2007 Published by Group of Thirty© Washington, DC 2008 Table of Contents I. Introduction ..................................................................................... 5 II. The Group of Thirty Membership ................................................... 7 III. The Work of the Group of Thirty in FY2006 and FY2007 ........... 13 Plenary Sessions .......................................................................... 13 International Banking Seminars ................................................. 13 Study Group Activities ................................................................ 14 Publications ................................................................................. 16 IV. The Finances of the Group .......................................................... 19 Annex 1. Past Membership of the Group of Thirty .......................... 31 Annex 2. Schedule of Meetings and Seminars: .............................. 33 Annex 3. International Banking Seminars ...................................... 35 Annex 4. Plenary Sessions ............................................................... 37 Annex 5. The Group of Thirty (G30) Study on Reinsurance and International Financial Markets ............................................ -

Institutional Investor

R +R Research + Rankings The 2015 Tech 50 repeating in the No. 1 position, brought his company from nowhere to the top of the global exchange world in part because, he says, “technology enabled us to scale quickly.” It also can fail. ICE’s three-and-a-half-hour outage on July 8 was only the latest to affect a major mar- Racers ket platform — and demonstrate the importance of two other differentiating qualities: resiliency and recovery. Catherine Bessant (No. 2), global technology and operations executive at Bank of America Corp., frets that the technology world at large is “moving at to the the speed of the consumer, not the speed of the enterprise.” The answer? “The best and brightest talent.” Bessant believes that “in conjunction with advanced- state thinking, financial services is mag- netic for tech people.” But that means competing against Apple, Google and other name brands. Edge The Tech 50 ranking was compiled The global financial technology elite sets itself apart by understanding by Institutional Investor editors and the strategic and societal implications of high-tech advances and staff, with nominations and input from industry participants and experts. Four pushing innovation at Silicon Valley–like speed. primary sets of attributes were evalu- ated: achievements and contributions over the course of a career; scope and complexity of responsibilities; influence GROUNDED AS IT IS IN INFOR- applications and system performance as and leadership inside and outside the mation and money — and components of corporate strategy. These organization; and pure technological information about money leaders think big about the global or innovation. -

J.P. Morgan's Expression of Interest to Act As Global Co-Ordinator And

CONFIDENTIAL J.P. Morgan’s expression of interest to act as Global Co-ordinator and Bookrunner in connection with the Íslandsbanki IPO J.P. Morgan is pleased to express its interest to act as Global Co-ordinator and Bookrunner in connection with the sale process of the Icelandic State Financial Investments’ holdings in Íslandsbanki. J.P. Morgan is a leading global investment bank with a market capitalisation of $427bn and total assets of $3.4trn (December 2020). J.P. Morgan’s global headquarters are in New York, while our European headquarters are in London. We have a strong presence and track record in the Nordic region and our commitment to the region is evidenced by our local offices across the region. J.P. Morgan offers ISFI a full range of investment banking services and will provide first class advice in connection with the sale process of its holdings in Íslandsbanki. We are a global leader in areas such as equity and equity linked capital markets, debt capital markets, M&A advisory, ratings advisory and equity and debt sales, research and trading. J.P. Morgan team for Íslandsbanki Senior project leadership and sponsorship Andreas Lindh, Co-Head of EMEA FIG Stefan Weiner, Head of Northern Europe ECM Kari Hallgrimsson, Senior Country Sponsorship Nordic FIG Advisory European ECM Christian Kornhoff, Executive Director Vittorio Rivaroli, Executive Director Filiph Nilsson, Analyst Emese Pavlik, Associate Kim-Jonas Pellikka, Analyst Vincent Collan, Analyst FIG DCM Ratings Advisory Kiran D. Karia, Executive Director Jens Rasmussen, Executive Director J.P. Morgan contact details Andreas Lindh Registered address: Full legal name: Taunustor 1 J.P. -

February 2019

The definitive source of news and analysis of the global fintech sector | February 2019 www.bankingtech.com SUPERSTRUCTURES Fintech reaches new heights CASE STUDY: CITIZENS BANK US heavyweight pivots for digital era FOOD FOR THOUGHT: CAREER CHOICES The Venn diagram of doom FINTECH FUTURES IN THIS ISSUE THEM US Contents NEWS 04 The latest fintech news from around the globe: the good, the bad and the ugly. 18 Banking Technology Awards The glamour, the winners and the celebrations. 23 Focus: intraday liquidity Are banks ready to meet the ECB’s latest expectations? 24 Interview: Pavel Novak, Zonky P2P lender on a “mission possible”. 26 Focus: data How DNB uses data to reconnect with customers. 30 Analysis: openfunds Admirable data standardisation efforts for the funds industry. 32 Case study: Citizens Bank US’s 13th largest bank embraces digital era. 38 Food for thought Making career choices and the Venn diagram of doom. They struggle with Fintech complexity. We see straight to your goal. We leverage proprietary knowledge and technology to solve complex regulatory challenges, create new products 40 Comment What would a recession mean for fintech? and build businesses. Our unique “one fi rm” approach brings to bear best-in-class talent from our 32 offi ces worldwide—creating teams that blend global reach and local knowledge. Looking for a fi rm that can help keep 42 Interview: Javier Santamaría, EPC your business moving in the right direction? Visit BCLPlaw.com to learn more. Happy one year anniversary, SEPA Instant Credit Transfer! REGULARS 44 -

TAKARÉK SZÁRMAZTATOTT BEFEKTETÉSI ALAP Tájékoztató És Kezelési Szabályzat

DIÓFA ALAPKEZELŐ ZRT. TAKARÉK SZÁRMAZTATOTT BEFEKTETÉSI ALAP Tájékoztató és Kezelési Szabályzat Közzététel időpontja: 2018. május. 2. Hatálybalépés időpontja: 2018. június 1. Tartalom Tájékoztató ...................................................................................................................................... 11 A Tájékoztatóban és Kezelési Szabályzatban használt fogalmak, rövidítések ...................................................11 I. A befektetési alapra vonatkozó információk .................................................................................................20 1. A befektetési alap alapadatai .............................................................................................................................20 1.1. A befektetési alap neve ..............................................................................................................................20 1.2. A befektetési alap rövid neve ....................................................................................................................20 1.3. A befektetési alap székhelye ......................................................................................................................20 1.4. A befektetési alapkezelő neve ...................................................................................................................20 1.5. A letétkezelő neve .......................................................................................................................................20 1.6. A forgalmazó -

Bad Bank Resolutions and Bank Lending by Michael Brei, Leonardo Gambacorta, Marcella Lucchetta and Bruno Maria Parigi

BIS Working Papers No 837 Bad bank resolutions and bank lending by Michael Brei, Leonardo Gambacorta, Marcella Lucchetta and Bruno Maria Parigi Monetary and Economic Department January 2020 JEL classification: E44, G01, G21 Keywords: bad banks, resolutions, lending, non-performing loans, rescue packages, recapitalisations BIS Working Papers are written by members of the Monetary and Economic Department of the Bank for International Settlements, and from time to time by other economists, and are published by the Bank. The papers are on subjects of topical interest and are technical in character. The views expressed in them are those of their authors and not necessarily the views of the BIS. This publication is available on the BIS website (www.bis.org). © Bank for International Settlements 2020. All rights reserved. Brief excerpts may be reproduced or translated provided the source is stated. ISSN 1020-0959 (print) ISSN 1682-7678 (online) Bad bank resolutions and bank lending Michael Brei∗, Leonardo Gambacorta♦, Marcella Lucchetta♠ and Bruno Maria Parigi♣ Abstract The paper investigates whether impaired asset segregation tools, otherwise known as bad banks, and recapitalisation lead to a recovery in the originating banks’ lending and a reduction in non-performing loans (NPLs). Results are based on a novel data set covering 135 banks from 15 European banking systems over the period 2000–16. The main finding is that bad bank segregations are effective in cleaning up balance sheets and promoting bank lending only if they combine recapitalisation with asset segregation. Used in isolation, neither tool will suffice to spur lending and reduce future NPLs. Exploiting the heterogeneity in asset segregation events, we find that asset segregation is more effective when: (i) asset purchases are funded privately; (ii) smaller shares of the originating bank’s assets are segregated; and (iii) asset segregation occurs in countries with more efficient legal systems. -

Building the #1 Bank in Europe on Solid Fundamentals and Values

Building the #1 Bank in Europe on Solid Fundamentals and Values A Strong Bank for ISP 2018-2021 Business Plan a Digital World February 6, 2018 MIL-BVA362-03032014-90141/VR Disclaimer This presentation includes certain forward looking statements, projections, objectives and estimates reflecting the current views of the management of the Company with respect to future events. Forward looking statements, projections, objectives, estimates and forecasts are generally identifiable by the use of the words “may,” “will,” “should,” “plan,” “expect,” “anticipate,” “estimate,” “believe,” “intend,” “project,” “goal” or “target” or the negative of these words or other variations on these words or comparable terminology. These forward-looking statements include, but are not limited to, all statements other than statements of historical facts, including, without limitation, those regarding the Company’s future financial position and results of operations, strategy, plans, objectives, goals and targets and future developments in the markets where the Company participates or is seeking to participate. Due to such uncertainties and risks, readers are cautioned not to place undue reliance on such forward-looking statements as a prediction of actual results. The Group’s ability to achieve its projected objectives or results is dependent on many factors which are outside management’s control. Actual results may differ materially from (and be more negative than) those projected or implied in the forward-looking statements. Such forward-looking information involves risks and uncertainties that could significantly affect expected results and is based on certain key assumptions. All forward-looking statements included herein are based on information available to the Company as of the date hereof. -

OFFERING CIRCULAR SAXO BANK A/S EUR 2,000,000,000 Senior

OFFERING CIRCULAR SAXO BANK A/S EUR 2,000,000,000 Senior Note and Subordinated Note Programme Under this EUR 2,000,000,000 Senior Note and Subordinated Note Programme (the “Programme”), Saxo Bank A/S (the “Issuer”) may from time to time issue notes (the “Notes”). Notes may be (i) senior notes (“Senior Notes”) or (ii) dated subordinated notes (in Danish: kapitalbeviser) (“Subordinated Notes”), as indicated in the relevant Pricing Supplement (as defined below). Notes may be denominated in any currency agreed between the Issuer and the relevant Dealer (as defined below). The maximum aggregate nominal amount of all Notes from time to time outstanding under the Programme will not at any time exceed EUR 2,000,000,000 (or its equivalent in other currencies calculated as described in the Programme Agreement described herein), subject to increase as described herein. The Notes may be issued on a continuing basis to one or more of the Dealers specified under “Overview of the Programme” and any additional Dealer appointed under the Programme from time to time by the Issuer (each a “Dealer” and together the “Dealers”), which appointment may be for a specific issue or on an ongoing basis. References in this Offering Circular to the “relevant Dealer” shall, in the case of an issue of Notes being (or intended to be) subscribed by more than one Dealer, be to all Dealers agreeing to subscribe such Notes. This offering circular (the “Offering Circular”) has not been approved as a prospectus for the purposes of the Prospectus Directive. When used in this Offering Circular, “Prospectus Directive” means Directive 2003/71/EC (as amended, including by Directive 2010/73/EU), and includes any relevant implementing measure in a relevant Member State of the EEA (as defined below). -

The Digital Banking Imperative Vision: the Digital Banking Strategy Playbook by Peter Wannemacher and Jacob Morgan March 21, 2017

FOR EBUSINESS & CHANNEL STRATEGY PROFESSIONALS The Digital Banking Imperative Vision: The Digital Banking Strategy Playbook by Peter Wannemacher and Jacob Morgan March 21, 2017 Why Read This Report Key Takeaways In the age of the customer, banks will either Banks Will Either Reinvent Themselves Or Be reinvent themselves or be forgotten — reduced Forgotten to what one executive calls “dumb money pipes.” Banks are relevant to customers today, but digital Digital business leaders will need to make tough disruption, disintermediation, and changing choices and take bold actions over the next regulations threaten to reduce some banks to five to 10 years to stave off the serious threats low-margin utilities, without relevance in people’s that banks face. This report outlines Forrester’s everyday lives. vision of digital banking’s future, one dominated Successful Banks Will Enable Customers’ by firms, both banks and non-banks, which Financial Well-Being predict and anticipate people’s financial needs to While banks today vary in the quality of their provide personalized experiences that are simple, digital offerings, their product sets, services, ubiquitous, empowering, and reassuring. and business models are mainly all the same. This will start to change, and banking itself will begin to fracture as individual banks find new revenue streams, explore new business models, and establish new brand positioning. But all successful banks will have a common attribute at their core: enabling financial well-being for customers. Ecosystems Will Be Mission-Critical Gone are the days when banks could essentially go it alone in serving their customers’ needs. Digital banking strategies should focus on building financial ecosystems to provide more relevant and expansive services. -

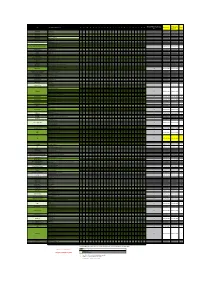

Updated As of 01/06/2017 Changes Highlighted in Yellow

NEW QUARTER TOTAL PDship per Previous Quarter Firm Legal Entity Holding Dealership AT BE BG CZ DE DK ES FI FR GR HU IE IT LV LT NL PL PT RO SE SI SK UK Current Quarter Changes Bank March 2016) ABLV Bank ABLV Bank, AS 1 bank customer bank customer 0 Abanka Vipa Abanka Vipa d.d. 1 bank customer bank customer 0 ABN Amro ABN Amro Bank N.V. 3 bank inter dealer bank inter dealer 0 Alpha Bank Alpha Bank S.A. 1 bank customer bank customer 0 Allianz Group Allianz Bank Bulgaria AD 1 bank customer bank customer 0 Banca IMI Banca IMI S.p.A. 3 bank inter dealer bank inter dealer 0 Banca Transilvania Banca Transilvania 1 bank customer bank customer 0 Banco BPI Banco BPI + 1 bank customer bank customer 0 Banco Comercial Português Millenniumbcp + 1 bank customer bank customer 0 Banco Cooperativo Español Banco Cooperativo Español S.A. + 1 bank customer bank customer 0 Banco Santander S.A. + Banco Santander / Santander Group Santander Global Banking & Markets UK 6 bank inter dealer bank inter dealer 0 Bank Zachodni WBK S.A. Bank Millennium Bank Millennium S.A. 1 bank customer bank customer 0 Bankhaus Lampe Bankhaus Lampe KG 1 bank customer bank customer 0 Bankia Bankia S.A.U. 1 bank customer bank customer 0 Bankinter Bankinter S.A. 1 bank customer bank customer 0 Bank of America Merrill Lynch Merrill Lynch International 9 bank inter dealer bank inter dealer 0 Barclays Barclays Bank PLC + 17 bank inter dealer bank inter dealer 0 Bayerische Landesbank Bayerische Landesbank 1 bank customer bank customer 0 BAWAG P.S.K. -

List of Market Makers and Authorised Primary Dealers Who Are Using the Exemption Under the Regulation on Short Selling and Credit Default Swaps

Last update 11 August 2021 List of market makers and authorised primary dealers who are using the exemption under the Regulation on short selling and credit default swaps According to Article 17(13) of Regulation (EU) No 236/2012 of the European Parliament and of the Council of 14 March 2012 on short selling and certain aspects of credit default swaps (the SSR), ESMA shall publish and keep up to date on its website a list of market makers and authorised primary dealers who are using the exemption under the Short Selling Regulation (SSR). The data provided in this list have been compiled from notifications of Member States’ competent authorities to ESMA under Article 17(12) of the SSR. Among the EEA countries, the SSR is applicable in Norway as of 1 January 2017. It will be applicable in the other EEA countries (Iceland and Liechtenstein) upon implementation of the Regulation under the EEA agreement. Austria Italy Belgium Latvia Bulgaria Lithuania Croatia Luxembourg Cyprus Malta Czech Republic The Netherlands Denmark Norway Estonia Poland Finland Portugal France Romania Germany Slovakia Greece Slovenia Hungary Spain Ireland Sweden Last update 11 August 2021 Austria Market makers Name of the notifying Name of the informing CA: ID code* (e.g. BIC): person: FMA ERSTE GROUP BANK AG GIBAATWW FMA OBERBANK AG OBKLAT2L FMA RAIFFEISEN CENTROBANK AG CENBATWW Authorised primary dealers Name of the informing CA: Name of the notifying person: ID code* (e.g. BIC): FMA BARCLAYS BANK PLC BARCGB22 BAWAG P.S.K. BANK FÜR ARBEIT UND WIRTSCHAFT FMA BAWAATWW UND ÖSTERREICHISCHE POSTSPARKASSE AG FMA BNP PARIBAS S.A.