Monster Beverage (MNST)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

BRAIN on Drugs 101 GATEWAY

BRAIN on DRUGs 101 GATEWAY. TRENDS . Markeng Recognion 2012 1 LT. Ed Moses, Rered 1 Ojecves • Recite number one cancer killer of women {#6 CDC source on slide} • List the three main areas of the brain in order of alcohol impairment {#36 Dr. John Duncan OK U • Idenfy the age of brain maturity {#37 Dr. Daniel Amen of www.amenclinics.com} 2 Target Markeng….Children 3 Our Children Targeted Parents Unaware In the lile world in which children have their existence, whosoever brings them up, there is nothing so finely perceived and so finely felt, as injusce. Charles Dickens 4 More Women Die every year due to Lung Cancer than Breast Cancer *2007 70,880 women died from Lung Cancer, while 40,460 women died from Breast Cancer. *Estimated by American Cancer Society 5 Smoking Rate vs. Cancer Rate About 24yrs #1 7th 6 7 8 Success trends cause Markeng Change Internal Medicine News 11/1/06 Cigaree Nicone Levels Increase 10% in 6 Years . Reports Commissioner Paul J. Cote Jr., of Massachuses Dept. of Public Health one of only 3 states that require tobacco co. to report yearly nicone yields 9 9 ‘07 Camel Ads • Pink Camels for Girls? 10 10 And the latest… VIRGINIA SLIMS “PURSE PACKS” 11 Camel Exoc Blends A few years ago, R.J. Reynolds introduced Camel Exotic Blends in a range of flavors, featuring unusual packaging that was bright and alluring. In 2006, RJR pulled this line of flavored cigarettes after signing a settlement with 39 state AG’s to stop marketing flavored cigarettes. -

A Bibliographical Guide to the Study of the Troubadours and Old Occitan Literature

A Bibliographical Guide to the Study of the Troubadours and Old Occitan Literature Robert A. Taylor RESEARCH IN MEDIEVAL CULTURE Bibliographical Guide to the Study of the Troubadours and Old Occitan Literature Medieval Institute Publications is a program of The Medieval Institute, College of Arts and Sciences Bibliographical Guide to the Study of the Troubadours and Old Occitan Literature Robert A. Taylor MEDIEVAL INSTITUTE PUBLICATIONS Western Michigan University Kalamazoo Copyright © 2015 by the Board of Trustees of Western Michigan University All rights reserved Manufactured in the United States of America This book is printed on acid-free paper. Library of Congress Cataloging-in-Publication Data Taylor, Robert A. (Robert Allen), 1937- Bibliographical guide to the study of the troubadours and old Occitan literature / Robert A. Taylor. pages cm Includes index. Summary: "This volume provides offers an annotated listing of over two thousand recent books and articles that treat all categories of Occitan literature from the earli- est enigmatic texts to the works of Jordi de Sant Jordi, an Occitano-Catalan poet who died young in 1424. The works chosen for inclusion are intended to provide a rational introduction to the many thousands of studies that have appeared over the last thirty-five years. The listings provide descriptive comments about each contri- bution, with occasional remarks on striking or controversial content and numerous cross-references to identify complementary studies or differing opinions" -- Pro- vided by publisher. ISBN 978-1-58044-207-7 (Paperback : alk. paper) 1. Provençal literature--Bibliography. 2. Occitan literature--Bibliography. 3. Troubadours--Bibliography. 4. Civilization, Medieval, in literature--Bibliography. -

Coca-Cola: a Powerful Brand – an Effective Marketing Strategy

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by eLibrary National Mining University Zaloznykh K., Kaimashnikova K. T.V. Kogemyakina, research supervisor Kriviy Rih Economic Institute of National Vadim Hetman Economic University of Kyiv COCA-COLA: A POWERFUL BRAND – AN EFFECTIVE MARKETING STRATEGY Branding is one of the most important aspects of any business, large or small, retail or business to business. It's important to spend time investing in researching, defining, and building your brand. An effective brand strategy gives you a major edge in increasingly competitive markets. To succeed in branding you must understand the needs and wants of your customers and prospects. You do this by integrating your brand strategies through your company at every point of public contact. Brand looks like the relationship between a product and its customer. A strong brand is invaluable as the battle for customers intensifies day by day. Brand is the source of a promise to your consumer. It's a foundational piece in your marketing communication and one you do not want to be without. For the last several years, when we ask people to think about a successful brand, we often ask them to think of Coca-Cola because, well, Coke is it. That’s why we decide to investigate the world’s powerful brand – coca - cola. The Coca-Cola Company is the world's largest beverage company, largest manufacturer, distributor and marketer of non-alcoholic beverage concentrates and syrups in the world, and one of the largest corporations in the United States. -

Sustainability Report Monster Beverage Corporation

2020 SUSTAINABILITY REPORT MONSTER BEVERAGE CORPORATION FORWARD-LOOKING STATEMENT This Report contains forward-looking statements, within the meaning of the U.S. federal securities laws as amended, regarding the expectations of management with respect to our plans, objectives, outlooks, goals, strategies, future operating results and other future events including revenues and profitability. Forward-look- ing statements are generally identified through the inclusion of words such as “aim,” “anticipate,” “believe,” “drive,” “estimate,” “expect,” “goal,” “intend,” “may,” “plan,” “project,” “strategy,” “target,” “hope,” and “will” or similar statements or variations of such terms and other similar expressions. These forward-looking statements are based on management’s current knowledge and expectations and are subject to certain risks and uncertainties, many of which are outside of the control of the Company, that could cause actual results and events to differ materially from the statements made herein. For additional information about the risks, uncer- tainties and other factors that may affect our business, please see our most recent annual report on Form 10-K and any subsequent reports filed with the Securities and Exchange Commission, including quarterly reports on Form 10-Q. Monster Beverage Corporation assumes no responsibility to update any forward-looking state- ments whether as a result of new information, future events or otherwise. 2020 SUSTAINABILITY REPORT #UNLEASHED TABLE OF CONTENTS LETTER FROM THE CO-CEOS 1 COMPANY AT A GLANCE 3 INTRODUCTION 5 SOCIAL 15 PRODUCT RESPONSIBILITY 37 ENVIRONMENTAL 45 GOVERNANCE 61 CREDITS AND CONTACT 67 INTRODUCTION MONSTER BEVERAGE CORPORATION LETTER FROM THE CO-CEOS As Monster publishes its first Sustainability Report, we cannot ignore the impact of the COVID-19 pandemic. -

ENERGY DRINK Buyer’S Guide 2007

ENERGY DRINK buyer’s guide 2007 DIGITAL EDITION SPONSORED BY: OZ OZ3UGAR&REE OZ OZ3UGAR&REE ,ITER ,ITER3UGAR&REE -ANUFACTUREDFOR#OTT"EVERAGES53! !$IVISIONOF#OTT"EVERAGES)NC4AMPA &, !FTERSHOCKISATRADEMARKOF#OTT"EVERAGES)NC 777!&4%23(/#+%.%2'9#/- ENERGY DRINK buyer’s guide 2007 OVER 150 BRANDS COMPLETE LISTINGS FOR Introduction ADVERTISING EDITORIAL 1123 Broadway 1 Mifflin Place The BEVNET 2007 Energy Drink Buyer’s Guide is a comprehensive compilation Suite 301 Suite 300 showcasing the energy drink brands currently available for sale in the United States. New York, NY Cambridge, MA While we have added some new tweaks to this year’s edition, the layout is similar to 10010 02138 our 2006 offering, where brands are listed alphabetically. The guide is intended to ph. 212-647-0501 ph. 617-715-9670 give beverage buyers and retailers the ability to navigate through the category and fax 212-647-0565 fax 617-715-9671 make the tough purchasing decisions that they believe will satisfy their customers’ preferences. To that end, we’ve also included updated sales numbers for the past PUBLISHER year indicating overall sales, hot new brands, and fast-moving SKUs. Our “MIA” page Barry J. Nathanson in the back is for those few brands we once knew but have gone missing. We don’t [email protected] know if they’re done for, if they’re lost, or if they just can’t communicate anymore. EDITORIAL DIRECTOR John Craven In 2006, as in 2005, niche-marketed energy brands targeting specific consumer [email protected] interests or demographics continue to expand. All-natural and organic, ethnic, EDITOR urban or hip-hop themed, female- or male-focused, sports-oriented, workout Jeffrey Klineman “fat-burners,” so-called aphrodisiacs and love drinks, as well as those risqué brand [email protected] names aimed to garner notoriety in the media encompass many of the offerings ASSOCIATE PUBLISHER within the guide. -

Energy Drinks: Harmful Or Helpful?

ENERGY DRINKS: HARMFUL OR HELPFUL? Caffeine: An Overview If someone asked how much caffeine you consume each day could you give them an accurate answer? Manufacturers are not currently required to list the caffeine content of foods or beverages on nutrition labels, so it can be difficult to determine how much caffeine you have each day. Most of us know that excessive intake of caffeine may cause a racing heart rate and headaches, but did you know that it can also cause anxiety, increased blood pressure, heart palpitations, insomnia and, in extreme cases, nausea and vomiting (1)? People are sensitive to caffeine at all different levels, but the general guideline is to try to consume less than 300mg caffeine (equivalent to about 3, 8oz. cups of coffee) daily. Although some of these symptoms sound fairly miserable, the good news is that in small to moderate amounts, caffeine has actually been shown to increase concentration and mental alertness (2). To maximize the benefits of caffeine and minimize side effects, it is best to spread out your caffeine intake throughout the day. Large caffeine doses in short periods of time only add to an “energy boost” followed by a “crash”. Check out the Caffeine Ranges for Common Beverages table to get a better idea of what your average caffeine intake may be. Caffeine Ranges for Common Beverages* Beverage Serving Size Caffeine Range (mg) Coffee, drip 8 fluid oz. 104-192 Tea, brewed 8 fluid oz. 20-90 Iced Tea 8 fluid oz. 9-50 Soft Drinks 8 fluid oz. 20-40 Cocoa Beverage 8 fluid oz. -

Strategic Analysis of the Coca-Cola Company

STRATEGIC ANALYSIS OF THE COCA-COLA COMPANY Dinesh Puravankara B Sc (Dairy Technology) Gujarat Agricultural UniversityJ 991 M Sc (Dairy Chemistry) Gujarat Agricultural University, 1994 PROJECT SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF BUSINESS ADMINISTRATION In the Faculty of Business Administration Executive MBA O Dinesh Puravankara 2007 SIMON FRASER UNIVERSITY Summer 2007 All rights reserved. This work may not be reproduced in whole or in part, by photocopy or other means, without permission of the author APPROVAL Name: Dinesh Puravankara Degree: Master of Business Administration Title of Project: Strategic Analysis of The Coca-Cola Company. Supervisory Committee: Mark Wexler Senior Supervisor Professor Neil R. Abramson Supervisor Associate Professor Date Approved: SIMON FRASER UNIVEliSITY LIBRARY Declaration of Partial Copyright Licence The author, whose copyright is declared on the title page of this work, has granted to Simon Fraser University the right to lend this thesis, project or extended essay to users of the Simon Fraser University Library, and to make partial or single copies only for such users or in response to a request from the library of any other university, or other educational institution, on its own behalf or for one of its users. The author has further granted permission to Simon Fraser University to keep or make a digital copy for use in its circulating collection (currently available to the public at the "lnstitutional Repository" link of the SFU Library website <www.lib.sfu.ca> at: ~http:llir.lib.sfu.calhandle/l8921112>)and, without changing the content, to translate the thesislproject or extended essays, if technically possible, to any medium or format for the purpose of preservation of the digital work. -

Energy Drinks Presentation Part 2

What’s All The Buzz About?? Lois Bisson BSN, RN Michelle Keith BSN, RN, NCSN Chris Mancini BSN, RN, NCSN Barbara Schuster BSN, RN, NCSN Caffeine Extracted from the raw fruit of over 60 species of coffee plants. Also extracted from tea, kola nuts and cocoa. It is the main byproduct of guarana Use: 1. Strong cardiovascular stimulant 2. Pain reliever Caffeine continued... Most widely used psychoactive substance in the world and the only one that is currently legal! Currently, youth are consuming more caffeine than adults on a milligram per kilogram basis Caffeine continued... FDA limits caffeine in soft drinks to 0.02 percent (10mg/oz.) but there are no limits for ED’s Most ED’s exceed the soft drink restriction, with caffeine amounts nearly 9-28mg/oz. Children should consume no more than 150mg per day Chocolate=5-20mg Caffeine continued... Lethal dose in humans approximately 10gm, however death has been reported at 6.5mg Well absorbed with 99% of absorption occurring in the GI tract. Easily distributed throughout the body, and crosses the blood-brain barrier Children may experience more pronounced effects due to slower drug metabolism Caffeine continued... In 1993, a Canadian study showed: 25.3% of children aged 11-18 admitted to caffeine doping to enhance sport performance. 37.4% of 16-18 year olds admitted to caffeine doping to enhance sport performance Catchy Names... 5 hour energy Stacker 2 Kick Start PimpJuice 6 hour energy Nirtro 2 go Battery Energy Red Devil Redbull Shot Redline Full Throttle Rockstar Monster Vital 4 U Rip It BAWLS Hit Man SoBe Advertised to.. -

Sheet1 Page 1 Name of Drink Caffeine (Mg) 5 Hour Energy 60

Sheet1 Name of drink Size (mL) Caffeine (mg) 5 Hour Energy 60 Equivalent of a cup of coffee Amp Energy (Original) 710 213 Amp Energy (Original) 473 143 Amp Energy Overdrive 473 142 Amp Energy Re-Ignite 473 158 Amp Energy Traction 473 158 Bawls Guarana 473 103 Bawls Guarana Cherry 473 100 Bawls Guarana G33K B33R 296 80 Bawls Guaranexx Sugar Free 473 103 Beaver Buzz Black Currant Energy 355 188 Beaver Buzz Citrus Energy 355 188 Beaver Buzz Green Machine Energy 473 200 Big Buzz Chronic Energy 473 200 BooKoo Energy Citrus 710 360 BooKoo Energy Wild Berry 710 360 Cheetah Power Surge Diet 710 None? Frank's Energy Drink 500 160 Frank's Energy Drink Lime 250 80 Frank's Energy Drink Pineapple 250 80 Full Throttle Unleaded 473 141 Hansen's Energy Pro 246 39 Hardcore Energize Bullet Blue Rage 85.7 300 Hype Energy Pro (Special Edition) 355 114 Hype Energy MFP 473 151 Inked Chikara 473 151 Inked Maori 473 151 Jolt Endurance Shot 60 200 Jolt Orange Blast 695 220 Lost (Original) 473 160 Lost Five-O 473 160 Mini Thin Rush (6 Hour) 60 200 Monster (Original) 710 246 Monster Assault 473 164 Monster Energy (Original) 473 170 Monster Khaos 710 225 Monster Khaos 473 150 Monster M-80 473 164 Monster MIXXD 473 Monster Reduced Carb 473 140 NOS (Original) 473 200 NOS (Original)(Bottle) 650 343 NOS Fruit Punch 473 246.35 Premium Green Tea Energy 355 119 Premium Iced Tea Energy 355 102 Premium Pink Energy 355 120 Red Bull 250 80 Red Bull 355 113.6 Page 1 Sheet1 Red Rain 250 80 Rocket Shot 54 50 Rockstar Burner 473 160 Rockstar Burner 710 239 Rockstar Diet 473 160 -

Mark Alan Smith Formatted Dissertation

Copyright by Mark Alan Smith 2019 The Dissertation Committee for Mark Alan Smith Certifies that this is the approved version of the following Dissertation: To Burn, To Howl, To Live Within the Truth: Underground Cultural Production in the U.S., U.S.S.R. and Czechoslovakia in the Post World War II Context and its Reception by Capitalist and Communist Power Structures. Committee: Thomas J. Garza, Supervisor Elizabeth Richmond-Garza Neil R. Nehring David D. Kornhaber To Burn, To Howl, To Live Within the Truth: Underground Cultural Production in the U.S., U.S.S.R. and Czechoslovakia in the Post World War II Context and its Reception by Capitalist and Communist Power Structures. by Mark Alan Smith. Dissertation Presented to the Faculty of the Graduate School of The University of Texas at Austin in Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy The University of Texas at Austin May, 2019 Dedication I would like to dedicate this work to Jesse Kelly-Landes, without whom it simply would not exist. I cannot thank you enough for your continued love and support. Acknowledgements I would like to thank my dissertation supervisor, Dr. Thomas J. Garza for all of his assistance, academically and otherwise. Additionally, I would like to thank the members of my dissertation committee, Dr. Elizabeth Richmond-Garza, Dr. Neil R. Nehring, and Dr. David D. Kornhaber for their invaluable assistance in this endeavor. Lastly, I would like to acknowledge the vital support of Dr. Veronika Tuckerová and Dr. Vladislav Beronja in contributing to the defense of my prospectus. -

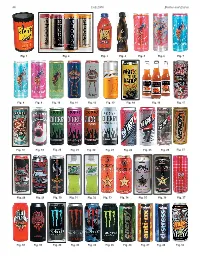

Bottles and Extras Fall 2006 44

44 Fall 2006 Bottles and Extras Fig. 1 Fig. 2 Fig. 3 Fig. 4 Fig. 5 Fig. 6 Fig. 7 Fig. 8 Fig. 9 Fig. 10 Fig. 11 Fig. 12 Fig. 13 Fig. 14 Fig. 16 Fig. 17 Fig. 18 Fig. 19 Fig. 20 Fig. 21 Fig. 22 Fig. 23 Fig. 24 Fig. 25 Fig. 26 Fig. 27 Fig. 28 Fig. 29 Fig. 30 Fig. 31 Fig. 32 Fig. 33 Fig. 34 Fig. 35 Fig. 36 Fig. 37 Fig. 38 Fig. 39 Fig. 40 Fig. 42 Fig. 43 Fig. 45 Fig. 46 Fig. 47 Fig. 48 Fig. 52 Bottles and Extras March-April 2007 45 nationwide distributor of convenience– and dollar-store merchandise. Rosen couldn’t More Energy Drink Containers figure out why Price Master was not selling coffee. “I realized coffee is too much of a & “Extreme Coffee” competitive market,” Rosen said. “I knew we needed a niche.” Rosen said he found Part Two that niche using his past experience of Continued from the Summer 2006 issue selling YJ Stinger (an energy drink) for By Cecil Munsey Price Master. Rosen discovered a company named Copyright © 2006 “Extreme Coffee.” He arranged for Price Master to make an offer and it bought out INTRODUCTION: According to Gary Hemphill, senior vice president of Extreme Coffee. The product was renamed Beverage Marketing Corp., which analyzes the beverage industry, “The Shock and eventually Rosen bought the energy drink category has been growing fairly consistently for a number of brand from Price Master. years. Sales rose 50 percent at the wholesale level, from $653 million in Rosen confidently believes, “We are 2003 to $980 million in 2004 and is still growing.” Collecting the cans and positioned to be the next Red Bull of bottles used to contain these products is paralleling that 50 percent growth coffee!” in sales at the wholesale level. -

Ankle Complex Musculature Adaptations After Energy Drinks Consumption in Healthy Young Adult

4 International Journal of ijpefs212 PHYSICAL EDUCATION, FITNESS AND SPORTS RESEARCH ARTICLE RESEARCH RESEARCH ARTICLE RESEARCH Ankle complex musculature adaptations after Energy Drinks 10.34256/ DOI: consumption in healthy young adult Martín G. Rosario PT, PhD, CSFI, ATRIC* , Clare Hanrahan SPT , Lauren Basye SPT and Ashley Correa SPT a Texas Woman’s University, School of Physical Therapy, Dallas, Texas *Corresponding author Ph: (214) 689-7712 ; Email: [email protected] DOI: https://doi.org/10.34256/ijpefs2124 Received: 15-03-2021, Revised: 12-04-2021; Accepted: 16-04-2021; Published: 27-04-2021 Abstract: Over the past few years, energy drink consumption has increased among students aged 18–34 years. Energy drinks alter the balance, reduce blood flow and interfere with neuromuscular activation in the lower extremities. We attempted to determine which specific additive of three different drinks (red bull, rockstar, and bang) could contribute to changes in muscle activation of the ankle complex. Twenty healthy young adults aged 22–28 years were included in this study and allocated among 3 groups, red bull, rockstar, and bang. Neuromuscular data were obtained from EMG sensors positioned on the anterior tibialis and gastrocnemius before completing the four balance tasks. Each participant completed all the tasks before and after the 16-ounce Edrink. ANOVA was performed to compare the data before and after the beverage. Statistical significance was set at P <0.05. A trend was observed in red bull and bang groups revealing a faster anterior tibial activity and prolong activation for gastrocnemius. The rockstar group also showed a more rapid activation trend and shorter response during all tasks for the gastrocnemius.