Chinese Cross-Listing Lixian

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The World's Biggest Hotel Companies. Old Trends and New Tendencies

MISCELLANEA GEOGRAPHICA – REGIONAL STUDIES ON DEVELOPMENT Vol. 19 • No. 4 • 2015 • pp. 26-33 • ISSN: 2084-6118 • DOI: 10.1515/mgrsd-2015-0020 The world’s biggest hotel companies. Old trends and new tendencies Abstract Many hotels are owned by a few dozen so-called hotel chains or hotel Andrzej Kowalczyk systems. The rapid growth of big hotel companies can be regarded as proof of the entrance of hotel systems into the globalisation phase. Since 2006, companies from the People’s Republic of China (PRC) have been among the world’s top hotel systems. This year can be considered Department of Geography of Tourism & Recreation as the symbolic beginning of a new stage in the history of the largest Institute of Socio-Economic Geography & Spatial Management hotel systems. This paper shows two main trends. On the one hand, the Faculty of Geography & Regional Studies processes that could be observed in the market of the major global hotel University of Warsaw Poland systems from the 1990s are still discernible (for example, the position of e-mail: [email protected] the so-called hotel megasystems). On the other hand, new trends have come to the fore in recent years, notably the emergence of systems from the People’s Republic of China among the world’s largest hotel systems. Keywords Hospitality • hotel megasystems • Chinese hotel chains Received: 30 September 2014 © University of Warsaw – Faculty of Geography and Regional Studies Accepted: 18 August 2015 Introduction A large proportion of hotels worldwide are owned by a few systems, non-cash settlements, launching new services for clients dozen so-called chains or systems, many of which operate and new technological solutions in catering, and so on. -

Potential Opportunities from One of the Fastest Growing Major Global Healthcare Markets1

KURE 3/31/2018 China Healthcare: Potential Opportunities From One Of The Fastest Growing Major Global Healthcare Markets1 An Overview of the KraneShares MSCI All China Health Care Index ETF (Ticker: KURE) 1. Major healthcare markets defined as top five global markets by the World Health Organization. Data from the World Health Organization as of 12/31/2015. Retrieved 3/31/2018 [email protected] 1 Introduction to KraneShares About KraneShares Krane Funds Advisors, LLC is the investment manager for KraneShares ETFs. Our suite of China focused ETFs provides investors with solutions to capture China’s importance as an essential element of a well-designed investment portfolio. We strive to provide innovative, first to market strategies that have been developed based on our strong partnerships and our deep knowledge of investing. We help investors stay up to date on global market trends and aim to provide meaningful diversification. Krane Funds Advisors, LLC is majority owned by China International Capital Corporation (CICC). 2 Investment Strategy: KURE seeks to measure the performance of MSCI China All Shares Health Care 10/40 Index. The Index is a free float adjusted market capitalization weighted index designed to track the equity market performance of Chinese companies engaged in the health care sector. The KURE securities in the Index include all types of publicly issued shares of Chinese issuers, which are listed in Mainland China, Hong Kong and United States. Issuers eligible for inclusion must be classified under the Global Industry Classification Standard (GICS) as engaged in the healthcare sector. The issuers included in the Underlying Index may include small-cap, mid-cap and large-cap companies. -

Information on the Proposed Candidates for Election at The

Information on the proposed candidates for election at the Extraordinary General Meeting on 10 December 2018 Following completion of a previously announced transaction of shares in the Company by a consortium led by Jin Jiang International Holdings Co., Ltd., including SINO-CEE Fund, through its joint acquisition vehicle Aplite Holdings AB (the “Consortium”), the Consortium holds 50.21 percent of the shares and votes in the Company. The Consortium has requested that the Board of Directors summons an Extraordinary General Meeting, which will be held on 10 December 2018. The below information regarding the candidates proposed for election at the Extraordinary General Meeting by the Consortium has been provided to the Company by the Consortium. MA MINGJU Nationality: Chinese Born: 1961 Education: Senior accountant with a master's degree in business administration from the Asia International Open University (Macau). Shares: 0 Mr. Ma joined Jinjiang International Holdings Co., Ltd. in 2005, and formerly served as Supervisor of Shanghai Jin Jiang International Hotels (Group) Company Limited and Director of Jinjiang Inn Co., Ltd. Mr. Ma is now Vice President and General Manager of Finance Business Division of Jinjiang International Holdings Co., Ltd., Chairman of Shanghai Jinjiang International Investment and Management Co,. Ltd., CEO of Shanghai Jin Jiang International Hotels (Group) Company Limited, Supervisor of Shanghai Jin Jiang International Hotels Development Co., Ltd., Director of Shanghai Jin Jiang International Industrial Investment Co., Ltd., Director of Beijing Kunlun Hotel Co., Ltd., and Chairman of Jin Jiang International Finance Co., Ltd. JIN CHEN Nationality: Chinese Born: 1971 Education: Master degrees in LLM both from China University of Politics and Law in Beijing and University of Warwick in the UK, as well as an MBA (International) from University of Hong Kong. -

Inside This Issue

1 December 23, 2014 – Issue 122 INSIDE THIS ISSUE China Green Food Expo to be Held in Nanchang China Green Food Expo to be The seventh China Green Food Expo is to be held in Nanchang, Held in Nanchang Jiangxi province. Companies from more than 30 provinces will attend the Expo with thousands of attendees to the event. Jan-Oct China Health Insurance The event is co-held by Ministry of Commerce and Jiangxi local Premium Exceeded CNY 130bn government. CFDA: Cosmeceuticals Should not The Expo tends to promote the economic rise of middle area of Promote Itself as Medicines the country and the opening-up of Jiangxi province. The event will include the food expo and a cooperation seminar joined by Shi Jiazhuang to Crack Down on state-run companies with local food providers and vendors. Illegal Health Food and Cosmetics The Expo mainly features low-carbon industry and green food. It will cover six indoor exhibiting rooms with food companies from Amorepacific Taps Surging more than 30 provinces. Overseas vendors from Australia, Demand for Midrange Beauty America, Russia and Thailand will also bring food to the local Products consumers who will attend the expo. (Source: Food Safety Daily) China Nepstar: A Bitter Pill For Investors Jan-Oct China Health Insurance Premium Exceeded CNY 130bn Herbal Berberine Boosts Brown Fat Activity Premium income of health insurance exceeded CNY 136.656 billion in the first 10 months of this year, growing 45.25% year on year, according to China Insurance Regulatory Commission. Premium income of life insurance companies grew 19.36% year on year. -

Federico J. González

THE CONVERSATION Radisson Hotel Group FEDERICO J. GONZÁLEZ The hotel group’s Chairman of the Global Steering Committee tells Andy Hoskins about his company’s transformation and its grand aspirations ighteen months have passed since “Jinjiang is very focused on hotels whereas segment that are competing against each Federico J. González joined the [current owners] HNA are more dispersed other in the same town or neighbourhood. E Radisson Hotel Group and he has in different sectors, so I think you can Our investors and hotel owners know they already overseen a re-brand of the two expect to see significant growth across all won't be competing against another Radisson arms of the company (based in Brussels our brands in China,” says González. in the same segment in the same town.” and Minneapolis) and implemented a And in a world of big brand mergers and If the group has a weakness it is perhaps five-year plan to “transform the company acquisitions, could Radisson and Jinjiang up its relatively uneven distribution of brands, in terms of revenue and reputation”. the ante? “I think so. We have a very strong, with Radisson Blu and Park Plaza strong in Previously known as the Carlson Rezidor aggressive five-year growth plan but that is Europe, for example, while Radisson hotels Hotel Group, the change of title brought the without factoring in any acquisitions. There and Country Inn and Suites are abundant Radisson name – its best-known brand – is already a significant amount of revenue across North America. to the fore, ditching the incongruous and profit potential in the existing business. -

Corporate 300 Ranking

HOTELS’325/HOTELS’325/HOTELS’325/HOTELS’325/HOTELS’325/HOTELS’325/HOTELS’325 TELS’325/HOTELS’325/HOTELS’325/HOTELS’325/HOTELS’325/HOTELS’325/HOTELS’325/HO 325/HOTELS’325/HOTELS’325/HOTELS’325/HOTELS’325/HOTELS’325/HOTELS’325/HOTELS HOTELS’325/HOTELS’325/HOTELS’325/HOTELS’325/HOTELS’325/HOTELS’325/HOTELS’325CORPORATE 300 RANKING Rank Company Rooms Hotels Rank Company Rooms Hotels 2007 Headquarters 2007 2007 2007 Headquarters 2007 2007 2006 2006 2006 2006 2006 2006 1 IHG (InterContinental Hotels Group) 585,094 3,949 31 IBEROSTAR Hotels & Resorts 31,000 97 1 Windsor, England 556,246 3,741 30 Palma de Mallorca, Spain 32,000 100 2 Wyndham Hotel Group 550,576 6,544 32 Millennium & Copthorne Hotels plc 29,987 111 2 Parsippany, N.J. USA 543,234 6,473 32 London, England 29,408 111 3 Marriott International 537,249 2,999 33 Tharaldson Lodging Cos. 28,878 372 3 Washington, D.C. USA 513,832 2,832 34 Fargo, N.D. USA 26,246 351 4 Hilton Hotels Corp. 502,116 3,000 34 Club Méditerranée 28,000 80 4 Beverly Hills, Calif. USA 501,478 2,935 33 Paris, France 28,027 80 5 Accor 461,698 3,871 35 Shangri-La Hotels and Resorts 26,434 55 5 Paris, France 486,512 4,121 35 Hong Kong, China 23,956 49 6 Choice Hotels International 452,027 5,570 36 Columbia Sussex Corp. 24,809 71 6 Silver Spring, Md. USA 435,000 5,376 29 Fort Mitchell, Ky. -

China Digest

China Digest China by numbers Round-up of business news, current issues, • 13,548 meters - combined height of and M&A analysis skyscrapers built in China in 2014 • 3 – number of world’s 10 tallest buildings Q1 2015 built in Wuxi city in 2014 • 7% - share of global freshwater in China In the news … (vs. 20% of world population) • 7 - of China’s ten most polluted cities are Subsidies cut for non-electric vehicles [Auto] in Hebei province The Ministry of Finance reports it is to reduce subsidies for traditional vehicles in • 30,000 - number of TV drama episodes an effort to boost the country’s renewable energy vehicle market. A program to build made in China annually charging infrastructure will also be accelerated. Aside from helping reduce urban pollution levels, the subsidy cut could encourage take-up of electric and hybrid • 14 - number of countries bordering China vehicles and boost domestic manufacturers such as BYD. (Caixin) • 648 million - China's online population • 280 million - number of people in China Growth of China O&G consumption to slow in 2015 [Energy] without safe drinking water China’s oil & gas consumption is expected to see slower growth this year, with falling • $1,831 - President Xi Jinping’s monthly global crude prices providing an opportunity for more energy sector reforms, salary according to the Economic and Technology Research Institute of the country’s • $1.2billion - annual US drug exports to largest O&G producer, China National Petroleum Corp. Chinese oil demand will China grow 3% year-on-year to 534 million metric tons in 2015, compared to growth of • $119.6 billion - China's actual use of 3.3% (to 516 million tons) in 2014, it said. -

Interview with Beijing Tong Ren Tang/Science Arts

[ Interview ] Mr Tan Lee Huak, owner of Science Arts Co Pte Ltd. Interview with Beijing Tong Ren Tang/Science Arts eijing Tongrentang, was founded in Kangxi 8. It is a famous time-honored brand in the Traditional Chinese Medicine industry. Science Arts collaborated Bwith Beijing Tong Ren Tang in 2004 and brought this well established brand to Singapore. Beijing Tong Ren Tang has a long Beijing Tong Ren Tang has outlets in many countries in the Asia history, being founded in the Kangxi Pacific. Its headquaters is in Beijing, China. The company has period, in 1669. Can you share with collaborated with more than 20 distributors worldwide. They us how the collaboration between have stores in the UK, Australia, Canada and countries in the Asia Pacific. Beijing Tong Ren Tang and Science It has also partnered with various distributors and companies in different Arts came about? countries. In Malaysia, they have partnered with “Hai Ou” to distibute their products. Here in Singapore, Science Arts is its sole distributor. Science Arts and Beijing Tong Ren Tang went into a collaboration in 2004. 1146 ■ Volume 11 > Number 16 > 2007 www.asiabiotech.com [ Interview ] What is Science Arts history and Science Arts have been around for 30 odd years. It was set up how did it come about? by a group of young passionate fresh graduates from The Chinese High School in the 1960s. The collaboration with Beijing Tong Ren Tang is 51% stakes held by Science Arts and 49% belongs to Beijing Tong Ren Tang. What are some of the measures that The side effects of most of our products are minimal. -

Healthcare Sector

19 August 2013 Sector Weekly Healthcare Sector Healthcare Sector Weekly Dose Valuation summary Company Ticker CCY Px Mkt ––––– P/E ––––– EPS CAGR –––– PEG –––– –––– P/B –––– –––– ROE –––– This weekly product is designed to provide investors with key sector cap '13E '14E '15E ('12E -'15E) '13E '14E '15E '13E '14E '15E '13E '14E '15E updates and our attempt to identify (USD) (x) (x) (x) (%) (x) (x) (x) (x) (x) (x) (%) (%) (%) stock implications and insights. Shandong Weigao Group Medical 1066 -HK HKD 8.09 1,965 24.2 19.9 16.4 22 1.1 0.9 0.7 2.9 2.6 2.3 12.1 13.2 14.3 Polymer Co. Ltd. Class H Topics this week: Bribery investigation, China Shineway Pharmaceutical 2877 -HK HKD 12.72 1,356 11.8 10.5 9.4 12 1.0 0.9 0.8 1.8 1.7 1.5 16.0 16.3 16.5 H7N9 resurfacing, NDRC might adjust Group Limited originator drug px, June ’13 hospital United Laboratories International 3933 -HK HKD 2.92 613 18.3 13.0 10.6 26 0.7 0.5 0.4 0.7 0.7 0.7 3.8 5.2 6.1 patient traffic data Holdings Ltd. Sinovac Biotech Ltd. SVA -US USD 4.61 254 -26.3 -43.9 46.1 2.3 2.6 2.7 -8.7 -6.0 5.9 Companies mentioned: Weigao (1066-HK), Shineway (2877.HK) and The China Nepstar Chain Drugstore NPD -US USD 1.58 156 21.3 Ltd. Sponsored ADR United Labs (3933.HK), Sinovac (SVA.O) and Nepstar (NPD.N) Source: Factset/Bloomberg SAIC anti-bribery investigation to begin: The State Administration for Industry and Commerce (SAIC) has initiated a round of bribery investigation that is expected to last 3 months until November ‘13. -

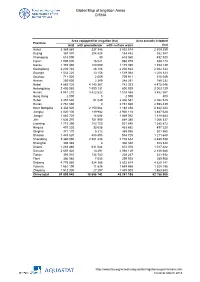

Global Map of Irrigation Areas CHINA

Global Map of Irrigation Areas CHINA Area equipped for irrigation (ha) Area actually irrigated Province total with groundwater with surface water (ha) Anhui 3 369 860 337 346 3 032 514 2 309 259 Beijing 367 870 204 428 163 442 352 387 Chongqing 618 090 30 618 060 432 520 Fujian 1 005 000 16 021 988 979 938 174 Gansu 1 355 480 180 090 1 175 390 1 153 139 Guangdong 2 230 740 28 106 2 202 634 2 042 344 Guangxi 1 532 220 13 156 1 519 064 1 208 323 Guizhou 711 920 2 009 709 911 515 049 Hainan 250 600 2 349 248 251 189 232 Hebei 4 885 720 4 143 367 742 353 4 475 046 Heilongjiang 2 400 060 1 599 131 800 929 2 003 129 Henan 4 941 210 3 422 622 1 518 588 3 862 567 Hong Kong 2 000 0 2 000 800 Hubei 2 457 630 51 049 2 406 581 2 082 525 Hunan 2 761 660 0 2 761 660 2 598 439 Inner Mongolia 3 332 520 2 150 064 1 182 456 2 842 223 Jiangsu 4 020 100 119 982 3 900 118 3 487 628 Jiangxi 1 883 720 14 688 1 869 032 1 818 684 Jilin 1 636 370 751 990 884 380 1 066 337 Liaoning 1 715 390 783 750 931 640 1 385 872 Ningxia 497 220 33 538 463 682 497 220 Qinghai 371 170 5 212 365 958 301 560 Shaanxi 1 443 620 488 895 954 725 1 211 648 Shandong 5 360 090 2 581 448 2 778 642 4 485 538 Shanghai 308 340 0 308 340 308 340 Shanxi 1 283 460 611 084 672 376 1 017 422 Sichuan 2 607 420 13 291 2 594 129 2 140 680 Tianjin 393 010 134 743 258 267 321 932 Tibet 306 980 7 055 299 925 289 908 Xinjiang 4 776 980 924 366 3 852 614 4 629 141 Yunnan 1 561 190 11 635 1 549 555 1 328 186 Zhejiang 1 512 300 27 297 1 485 003 1 463 653 China total 61 899 940 18 658 742 43 241 198 52 -

Completing the Deal

termsheet April 2018 Issue 24 Completing the Deal industry insight An Interview with Dr Fintan Walton, Are Traditional Chinese Medicines Founder and Chief Executive of PharmaVentures and Plant Extract Treatments the Basis of New Licensing and M&A As Fintan Walton, the Founder and CEO of PharmaVentures, puts it himself, Growth? he was “fortunate enough to be able to enter the world of pharmaceuticals Eric Liu when the explosion of biotechnology Business Analyst, PharmaVentures Limited took off in the 1970’s and 1980s”. He Traditional Chinese Medicines (TCMs) are gaining was educated at Trinity College, Dublin interest worldwide. However despite being as a geneticist and entered the world practised by significant numbers of people in more of biotechnology in the UK by joining Celltech, the first biotech than 140 countries, the absence of robust evidence of efficacy in Europe, in the early 1980s. What Fintan finds fascinating about and safety in conventional clinical trials remains a key challenge that period was that the technology being developed enabled in mainstream commercial adoption, through licensing and M&A scientists to really understand the basis of disease and hence, transactions. Against this backdrop 2017 was a milestone year. The come up with truly break-through medicines as more and more University of Oxford opened its first Chinese Medicine Research biotech companies emerged worldwide. “Their research led to Centre on 6th December, which is one of the first research centres inventions and so the opportunity to license patents and do deals in the West that solely focuses on the study of herbal extracts became a real driver in the biotech industry”. -

The Neolithic Ofsouthern China-Origin, Development, and Dispersal

The Neolithic ofSouthern China-Origin, Development, and Dispersal ZHANG CHI AND HSIAO-CHUN HUNG INTRODUCTION SANDWICHED BETWEEN THE YELLOW RIVER and Mainland Southeast Asia, southern China1 lies centrally within eastern Asia. This geographical area can be divided into three geomorphological terrains: the middle and lower Yangtze allu vial plain, the Lingnan (southern Nanling Mountains)-Fujian region,2 and the Yungui Plateau3 (Fig. 1). During the past 30 years, abundant archaeological dis coveries have stimulated a rethinking of the role ofsouthern China in the prehis tory of China and Southeast Asia. This article aims to outline briefly the Neolithic cultural developments in the middle and lower Yangtze alluvial plain, to discuss cultural influences over adjacent regions and, most importantly, to examine the issue of southward population dispersal during this time period. First, we give an overview of some significant prehistoric discoveries in south ern China. With the discovery of Hemudu in the mid-1970s as the divide, the history of archaeology in this region can be divided into two phases. The first phase (c. 1920s-1970s) involved extensive discovery, when archaeologists un earthed Pleistocene human remains at Yuanmou, Ziyang, Liujiang, Maba, and Changyang, and Palaeolithic industries in many caves. The major Neolithic cul tures, including Daxi, Qujialing, Shijiahe, Majiabang, Songze, Liangzhu, and Beiyinyangying in the middle and lower Yangtze, and several shell midden sites in Lingnan, were also discovered in this phase. During the systematic research phase (1970s to the present), ongoing major ex cavation at many sites contributed significantly to our understanding of prehis toric southern China. Additional early human remains at Wushan, Jianshi, Yun xian, Nanjing, and Hexian were recovered together with Palaeolithic assemblages from Yuanmou, the Baise basin, Jianshi Longgu cave, Hanzhong, the Li and Yuan valleys, Dadong and Jigongshan.