2020 Review of Shareholder Activism

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Lessons from COVID-19: Etfs As a Source of Stability

Lessons from COVID-19: ETFs as a Source of Stability Barbara Novick Samara Cohen Jason Warr Stephen Fisher Vice Chairman Co-Head of ETF & EMEA Head of ETF Global Public Policy Index Investing & Index Investing Markets and Markets Investments Sander van Samantha Rajat Tiwari Midori Takasaki Nugteren Merwin ETF & Index Global Public Policy ETF & Index Head of Markets Investing Investing Advocacy for ETF & Index Investing Introduction ETFs did not increase market volatility; instead, they were a source of stability as investors increasingly turned to ETFs Exchange-traded funds (ETFs) proved their resilience in the to efficiently rebalance holdings, hedge portfolios and first part of 2020. Unprecedented market volatility resulting manage risk. However, as we look back at this period of from the COVID-19 pandemic presented ETFs with the market volatility, we recognize that there are still areas most significant test they have faced since the 2008 global where additional improvements can be made to bolster the financial crisis (GFC). As liquidity in underlying markets strength and resiliency of the ETF market. In this ViewPoint, deteriorated during the selloff, especially in fixed income, we examine ETF performance through April 2020 and offer ETFs continued to trade efficiently, playing a leading role in recommendations to further strengthen the ETF ecosystem price discovery for investors and banks as they gave and benefit investors. transparency to the values at which investors were prepared to exchange risk. Key observations and recommendations 1. ETFs faced two tests in the first part of 2020: 4. While ETFs were resilient during the COVID-19 unprecedented market volatility and the most crisis, there are some areas that can be improved extreme conditions in the bond market since the to further enhance their ability to add stability to GFC. -

Annual Report and Accounts 2013 Annual Report and Accounts 2013

Annual Report and Accounts 2013 Annual Report and Accounts 2013 Brewin Dolphin Holdings PLC, 12 Smithfield Street, London EC1A 9BD T 020 7246 1000 F 020 3201 3001 W brewin.co.uk E [email protected] Brewin Dolphin provides a range of investment management, financial advice and execution only services in the UK and Eire. “Our priorities are clear. They are to reinforce our high standard of service to clients and ensure an improved return to shareholders. Discretionary Investment Management is currently the core of our business model and our mission is to provide a compelling and consistent offering, relevant to all our clients. Over the past decade we have evolved from a stockbroker into a private client investment manager. Our evolution must continue as we strive to become the leading provider of personal Discretionary Wealth Management in the UK.” David Nicol, Chief Executive Investment proposition • Strong client relationships with a long-term track record of personalised service • Growth market with good long-term prospects • New management team with clear goals and a strategy to achieve them • Our strategy will generate value for all stakeholders We are already creating value in 2013 • Total income grew by 9% to £283.7m • Adjusted profit before tax grew by 22% to £52.3m • Adjusted profit margin increased from 16.5% to 18.5% • Discretionary funds under management (FUM) grew by 17% to £21.3bn • Adjusted earnings per share (EPS) grew by 19.2% to 14.9p (2012: 12.5p) • Full year dividend increased by 20% to 8.6p • Total Shareholder Return was 63% Contents Business review Section 1 Business review Financial Highlights 02 Business Highlights 03 Chairman’s Statement 04 Overview of the Business and Strategy 06 Strategic Report 08 A. -

Fund Selection

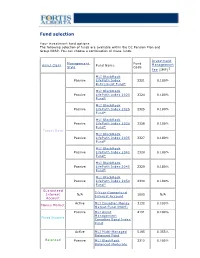

Fund selection Y our investment fund options The following selection of funds are available within the DC Pension Plan and Group RRSP. You can choose a combination of these funds. Investment Management Fund Asset Class Fund Name Management Style Code Fee (IMF)1 MLI BlackRock Passive LifeP ath Index 2321 0.180% Retirement Fund* MLI BlackRock Passive LifeP ath Index 2020 2324 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2025 2325 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2030 2326 0.180% Fund* Target Date MLI BlackRock Passive LifeP ath Index 2035 2327 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2040 2328 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2045 2329 0.180% Fund* MLI BlackRock Passive LifeP ath Index 2050 2330 0.180% Fund* Guaranteed 5-Y ear Guaranteed Interest N/A 1005 N/A Interest Account Account Active MLI Canadian Money 3132 0.100% Money Market Market Fund (MAM) Passive MLI Asset 4191 0.100% Management Fixed Income Canadian Bond Index Fund Active MLI Multi-Managed 5195 0.355% Balanced Fund Balanced Passive MLI BlackRock 2312 0.105% Balanced Moderate Index Fund Active MLI Canadian Equity 7011 0.210% Fund Canadian Passive MLI Asset 7132 0.100% Equity Management Canadian Equity Index Fund Active MLI U.S. Diversified 8196 0.375% Grow th Equity (Wellington) Fund U.S. Equity Passive MLI BlackRock U.S. 8322 0.090% Equity Index Fund* Active MLI MFS MB 8162 0.280% International Equity International Fund Equity Passive MLI BlackRock 8321 0.160% International Equity Index Fund* 1 IMFs shown do not include applicable taxes. -

MCERA May 5, 2021 Regular Board Meeting Agenda Page 1 of 4 B

AGENDA REGULAR BOARD MEETING MARIN COUNTY EMPLOYEES’ RETIREMENT ASSOCIATION (MCERA) One McInnis Parkway, 1st Floor Retirement Board Chambers San Rafael, CA May 5, 2021 – 9:00 a.m. This meeting will be held via videoconference pursuant to Executive Order N-25-20, issued by Governor Newsom on March 12, 2020, Executive Order N-29-20, issued by Governor Newsom on March 17, 2020, and Executive Order N-35-20, issued by Governor Newsom on March 21, 2020. Instructions for watching the meeting and/or providing public comment, as well as the links for access, are available on the Watch & Attend Meetings page of MCERA’s website. Please visit https://www.mcera.org/retirementboard/agendas-minutes/watchmeetings for more information. The Board of Retirement encourages a respectful presentation of public views to the Board. The Board, staff and public are expected to be polite and courteous, and refrain from questioning the character or motives of others. Please help create an atmosphere of respect during Board meetings. EVENT CALENDAR 9 a.m. Regular Board Meeting CALL TO ORDER ROLL CALL MINUTES April 14, 2021 Board meeting A. OPEN TIME FOR PUBLIC EXPRESSION Note: The public may also address the Board regarding any agenda item when the Board considers the item. Open time for public expression, from three to five minutes per speaker, on items not on the Board Agenda. While members of the public are welcome to address the Board during this time on matters within the Board’s jurisdiction, except as otherwise permitted by the Ralph M. Brown Act (Government Code Sections 54950 et seq.), no deliberation or action may be taken by the Board concerning a non-agenda item. -

Finding the Opportunity In

Finding the ESG disclosures: the bedrock of the opportunity sustainable finance agenda in ESG Executive summary To be successful, the development of sustainable finance in Europe needs to be grounded in access to high quality and meaningful ESG disclosures. While the quality and reliability of ESG data has improved considerably, so has the sophistication of investors and their needs for improved ESG disclosure. Investors find the most value in ESG disclosures when sustainability is embedded in the DNA of the firm as part of their competitive advantage to create long-term value. Companies that create societal value should benefit from changing policy and consumer trends, resulting in more sustainable cash flows, a lower cost of capital and higher valuations. While no standardised reporting framework can ever fully capture and reflect this. Reporting standards should, however, ensure that we move away from boilerplate disclosures and box-ticking approaches to consider the ESG risks and opportunities that are material to each company, industry and sector. While numerous standards already exist in this space, no single regulatory standard provides a comprehensive framework for companies to disclose in a way that would meet investors’ needs. Greater convergence in reporting could fill the gaps in accessing core ESG metrics that investors rely on to develop their ESG screening tools and assessment methodologies. Convergence in ESG reporting standards would also enable such data to be audited, which is becoming increasingly important to investors who base capital allocation decisions on such information. Beyond these core metrics, we need to connect ESG disclosures with real world outcomes, both adverse impacts as well as opportunities for transition. -

Group Retirement Program Investment Options for Members

Net Worth Employee Benefits Inc. Group Retirement Program Investment Options for Members January 1st 2020 20 Holly Street Toronto, Ontario M4S 3B1 Tel: 416-588-2808 h Toll Free: 1-866-258-4788 h Fax: 416-597-5768 h e-mail: [email protected] VMware Group Retirement Program Overview VMware recognizes the importance of sound financial retirement planning. The VMware Group Deferred Profit Sharing Plan and VMware Group Registered Retirement Savings Plan reflect VMware’s commitment to helping its members to prepare for their financial retirement. Details of the program are set out below: The VMware Group Retirement Program is a voluntary program, composed of a Group Deferred Profit Sharing Plan (DPSP) and a Group Registered Retirement Savings Plan (RRSP). Effective Date The Program was effective April 1, 1996 Eligibility You are eligible to join this program if you are a full time employee and work a minimum of 20 hours per week. Investment Direction Members will direct the investment of their account balances under each of the plans, using the investment options available under the program. Changes to your investment options can be made at any time, free of fees, by calling Manulife at 1-888-727-7766, or by logging in at www.manulife.ca\GRO Default If investment directions are not provided, a member’s account balance will be invested in the appropriate Retirement Date Fund. The appropriate Retirement Date Fund will be determined using the normal retirement date of age 65 Basic Contributions You can make a basic contribution of 1% to 6% of your earnings*to the VMware Group RRSP. -

Arbitrage Pricing Theory∗

ARBITRAGE PRICING THEORY∗ Gur Huberman Zhenyu Wang† August 15, 2005 Abstract Focusing on asset returns governed by a factor structure, the APT is a one-period model, in which preclusion of arbitrage over static portfolios of these assets leads to a linear relation between the expected return and its covariance with the factors. The APT, however, does not preclude arbitrage over dynamic portfolios. Consequently, applying the model to evaluate managed portfolios contradicts the no-arbitrage spirit of the model. An empirical test of the APT entails a procedure to identify features of the underlying factor structure rather than merely a collection of mean-variance efficient factor portfolios that satisfies the linear relation. Keywords: arbitrage; asset pricing model; factor model. ∗S. N. Durlauf and L. E. Blume, The New Palgrave Dictionary of Economics, forthcoming, Palgrave Macmillan, reproduced with permission of Palgrave Macmillan. This article is taken from the authors’ original manuscript and has not been reviewed or edited. The definitive published version of this extract may be found in the complete The New Palgrave Dictionary of Economics in print and online, forthcoming. †Huberman is at Columbia University. Wang is at the Federal Reserve Bank of New York and the McCombs School of Business in the University of Texas at Austin. The views stated here are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of New York or the Federal Reserve System. Introduction The Arbitrage Pricing Theory (APT) was developed primarily by Ross (1976a, 1976b). It is a one-period model in which every investor believes that the stochastic properties of returns of capital assets are consistent with a factor structure. -

Lazard Global Managed Volatililty Fund Commentary

Lazard Global Managed Volatility Fund AUG Commentary 2021 Market Overview e global equity markets continued their historic recovery with a seventh straight monthly gain in August. Momentum was strong as many indices posted multiple all-time highs during the month. e United States, overcoming a decline in consumer condence, continued to lead the major equity markets. Federal Reserve Chairman Jerome Powell calmed investors’ fear of a sharp curtailment in the central bank’s stimulus programs while indicating that economic strength was sufficient for the Fed to consider a modest reduction in its bond repurchase program. e euro area reported surprisingly strong GDP growth for the second quarter, outpacing most major economies, including those of China and the United States. Corporate earnings in Europe recovered further as vaccinations increased and the economy continued to reopen. European sell-side analysts raised their earnings estimates at a historically high rate. Japan also posted a positive month but trailed other markets; its economy grew more than expected in the second quarter, counteracting the effects of the spike in COVID-19 cases that had caused a sell-off in July. e spike will likely temper growth in the third quarter. e favorable economic news and low interest rates benetted the emerging markets, which outpaced the developed markets in August. Sector performance showed only modest dispersion in August, with every sector except materials posting a positive return. Financials were the strongest sector for the month and have taken leadership from energy for the year. Global factor performance was also relatively muted in the month. Risk measures showed mixed results as lower beta stocks and stocks with higher volatility over the past year outperformed. -

Financial Disclosure Report

Filing ID #10019886 financial DiScloSure report Clerk of the House of Representatives • Legislative Resource Center • 135 Cannon Building • Washington, DC 20515 filer information name: Brian Deters Status: Congressional Candidate State/District: IL18 filing information filing type: Candidate Report filing Year: 2017 filing Date: 02/14/2018 period covered: 01/01/2017– 01/31/2018 ScheDule a: aSSetS anD "unearneD" income asset owner Value of asset income income income type(s) current Year to preceding filing Year AXA ⇒ $1,001 - $15,000 Tax-Deferred 1290 VT Equity Income AXA ⇒ $1,001 - $15,000 Tax-Deferred AXA 500 Managed Volatility AXA ⇒ $1,001 - $15,000 Tax-Deferred AXA Balanced Strategy AXA ⇒ $1,001 - $15,000 Tax-Deferred AXA Franklin Small Cap Value Managed Volatility AXA ⇒ $15,001 - $50,000 Tax-Deferred AXA Global Equity Managed Volatility AXA ⇒ $1,001 - $15,000 Tax-Deferred AXA International Managed Volatility AXA ⇒ $1,001 - $15,000 Tax-Deferred AXA Large Cap Value Managed Volatility asset owner Value of asset income income income type(s) current Year to preceding filing Year AXA ⇒ $1,001 - $15,000 Tax-Deferred AXA Templeton Global Equity Managed Volatility AXA ⇒ $15,001 - $50,000 Tax-Deferred EQ/Core Bond Index AXA ⇒ $1,001 - $15,000 Tax-Deferred EQ/MFS International Growth AXA ⇒ $1,001 - $15,000 Tax-Deferred Intermediate Government Bond AXA ⇒ $1,001 - $15,000 Tax-Deferred Quality Bond Plus Caterpillar Inc 401K ⇒ SP $50,001 - Tax-Deferred Bond Fund $100,000 Caterpillar Inc 401K ⇒ SP $50,001 - Tax-Deferred Bond Index Fund $100,000 Caterpillar Inc 401K ⇒ SP $100,001 - Tax-Deferred Caterpillar Stock Fund $250,000 Caterpillar Inc 401K ⇒ SP $15,001 - $50,000 Tax-Deferred International Equity Broad Index Fund Caterpillar Inc 401K ⇒ SP $50,001 - Tax-Deferred International Equity Fund $100,000 Caterpillar Inc 401K ⇒ SP $100,001 - Tax-Deferred Stable principal Fund $250,000 Caterpillar Inc 401K ⇒ SP $100,001 - Tax-Deferred U.S. -

Invesco Canadian Balanced Account MANAGED ACCOUNTS Valued Client (On Or After March 17, 2012) · As of August 31, 2021

Invesco Canadian Balanced Account MANAGED ACCOUNTS Valued Client (on or after March 17, 2012) · as of August 31, 2021 Account Details How This Account Works Inception date: October 22, 2002 THIS ACCOUNT IS LINKED TO THE PERFORMANCE OF THE INVESCO CANADIAN PREMIER BALANCED FUND. When you invest in this account, you do not acquire an interest in this designated fund or purchase any units or legal Asset class: Canadian Balanced interest in any security. Designated Fund Details Performance Fund name: Invesco Canadian Premier Balanced Fund Growth of $10,000 over 10 years for Invesco Canadian Premier Balanced Fund ± Objective: Invesco Canadian Premier Balanced Fund $20,000 seeks to generate capital growth and income by $18,000 investing mainly in: Canadian equities with strong growth potential and high-quality Canadian $16,000 government and corporate fixed-income securities and Foreign equities and highquality U.S. government and $14,000 corporate fixed-income securities. $12,000 Inception date: July 15, 1992 AUM: $475.81 million $10,000 MER (audited): 2.59% $8,000 Number of Positions: 294 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 Number of Bond Positions: 217 Number of Equity Positions: 75 Lead manager: Jason Holzer Compound Returns of Invesco Canadian Balanced Account (%) Co-manager(s): Richard Nield, Avi Hooper, Matthew Product 1 mth 3 mth 6 mth YTD 1 yr 3 yr 5 yr 10 yr Inception Brill, Howard Greene, Mark Uptigrove InnoVision Valued Client (2.00%*) 0.65 3.62 6.53 6.50 11.22 3.68 2.15 3.65 3.79 Managed by: Invesco Canada Ltd. -

Brewin Dolphin Holdings PLC Annual Report and Accounts 2015 Accounts and Report Annual

Brewin Dolphin Holdings PLC Holdings Dolphin Brewin Annual Report and Accounts 2015 Brewin Dolphin Holdings PLC Annual Report and Accounts 2015 Contents Overview 34 Corporate Responsibility 82 Directors’ Responsibilities 96 Consolidated Cash 02 Highlights 40 Resources and Relationships 83 Independent Auditor’s Report Flow Statement 04 Chairman’s Statement 97 Company Cash Flow Statement Governance Financial Statements 98 Notes to the Financial Strategic Report 44 Chairman’s Introduction 90 Consolidated Income Statement Statements 08 Business Overview to Governance 91 Consolidated Statement of 10 Business Model 46 Directors and their Biographies Comprehensive Income Additional Information 12 Market Environment 48 Corporate Governance Report 92 Consolidated Balance Sheet 148 Five Year Record Continuing 14 Our Strategy 53 Board Risk Committee Report 93 Consolidated Statement of Operations (unaudited) 16 Chief Executive’s Statement 56 Audit Committee Report Changes in Equity 149 Appendix – Calculation of KPIs 20 Measuring Our Performance 62 Nomination Committee Report 94 Company Balance Sheet 150 Glossary 23 Results 64 Directors’ Remuneration Report 95 Company Statement of Changes 151 Shareholder Information 30 Principal Risks and Uncertainties 80 Other Statutory Information in Equity 152 Branch Address List Brewin Dolphin Holdings PLC Annual Report and Accounts 2015 Overview Brewin Dolphin provides a range of investment management and financial advice services in the Strategic Report United Kingdom, Channel Islands and the Republic of Ireland. -

LAZARD GROUP LLC (Exact Name of Registrant As Specified in Its Charter)

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2008 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to 333-126751 (Commission File Number) LAZARD GROUP LLC (Exact name of registrant as specified in its charter) Delaware 51-0278097 (State or Other Jurisdiction of Incorporation (I.R.S. Employer Identification No.) or Organization) 30 Rockefeller Plaza New York, NY 10020 (Address of principal executive offices) Registrant’s telephone number: (212) 632-6000 Securities Registered Pursuant to Section 12(b) of the Act: None Securities Registered Pursuant to Section 12(g) of the Act: None Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐ Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒ Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐ Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.