Rights Issue Prospectus

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Sustainable Investing for a Changing World Annual Report 2016 About Schroders

Sustainable investing for a changing world Annual Report 2016 About Schroders At Schroders, asset management is our only business and our goals are completely aligned with those of our clients: the creation of long-term value to assist them in meeting their future financial requirements. We have responsibility for £397.1 billion As responsible investors and signatories (€465.2 billion/$490.6 billion) on behalf to the UN’s Principles for Responsible of institutional and retail investors, Investment (PRI) we consider the long-term financial institutions and high net worth risks and opportunities that will affect the clients from around the world, invested resilience of the assets in which we invest. across equities, fixed income, multi-asset, This approach is supported by our alternatives and real estate. Environmental, Social and Governance (ESG) Policy and our Responsible Real Estate Investment Policy. Presence in 41 offices P 27 countries globally £397.1 bn assets 4,100+ under management employees and administration 15% 15% 4% 4% 10% 10% 39% 39% 40% 40% 21% 21% by client by client By product domicile domicile By product 21% 21% 25% 25% 25% 25% United KingdomUnited Kingdom Asia Pac ific Asia Pacific uities uities ultiasset ultiasset urope iddleurope ast and iddle frica ast and fricamericas mericas Wealth manaementWealth manaementied income ied income merin maretmerin debt commoditiesmaret debt andcommodities real estate and real estate Source: Schroders, as at 31 December 2016 1 The companies and sectors mentioned herein are for illustrative purposes only and are not to be considered a recommendation to buy or sell. % W P X AA AAA 2016 has shown that the social and environmental backdrop facing companies is changing quickly and pressures are coming to a head. -

Chronology, 1963–89

Chronology, 1963–89 This chronology covers key political and economic developments in the quarter century that saw the transformation of the Euromarkets into the world’s foremost financial markets. It also identifies milestones in the evolu- tion of Orion; transactions mentioned are those which were the first or the largest of their type or otherwise noteworthy. The tables and graphs present key financial and economic data of the era. Details of Orion’s financial his- tory are to be found in Appendix IV. Abbreviations: Chase (Chase Manhattan Bank), Royal (Royal Bank of Canada), NatPro (National Provincial Bank), Westminster (Westminster Bank), NatWest (National Westminster Bank), WestLB (Westdeutsche Landesbank Girozentrale), Mitsubishi (Mitsubishi Bank) and Orion (for Orion Bank, Orion Termbank, Orion Royal Bank and subsidiaries). Under Orion financings: ‘loans’ are syndicated loans, NIFs, RUFs etc.; ‘bonds’ are public issues, private placements, FRNs, FRCDs and other secu- rities, lead managed, co-managed, managed or advised by Orion. New loan transactions and new bond transactions are intended to show the range of Orion’s client base and refer to clients not previously mentioned. The word ‘subsequently’ in brackets indicates subsequent transactions of the same type and for the same client. Transaction amounts expressed in US dollars some- times include non-dollar transactions, converted at the prevailing rates of exchange. 1963 Global events Feb Canadian Conservative government falls. Apr Lester Pearson Premier. Mar China and Pakistan settle border dispute. May Jomo Kenyatta Premier of Kenya. Organization of African Unity formed, after widespread decolonization. Jun Election of Pope Paul VI. Aug Test Ban Take Your Partners Treaty. -

ARAMARK HOLDINGS CORPORATION (Exact Name of Registrant As Specified in Its Charter) ______

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 ___________________________________________ FORM 10-Q ___________________________________________ x QUARTERLY REPORT PURSUANT TO SECTION 13 or 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Quarterly Period Ended March 28, 2014 OR ¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission File Number 001-36223 ___________________________________________ ARAMARK HOLDINGS CORPORATION (Exact name of registrant as specified in its charter) ___________________________________________ Delaware 20-8236097 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification Number) ARAMARK Tower 1101 Market Street Philadelphia, Pennsylvania 19107 (Address of principal executive offices) (Zip Code) (215) 238-3000 (Registrant’s telephone number, including area code) ___________________________________________ Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨ Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that registrant was required to submit and post such files). Yes x No ¨ Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. -

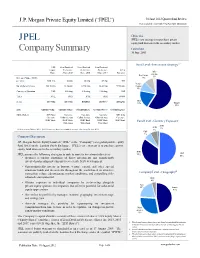

JPEL Company Summary

J.P. Morgan Private Equity Limited (“JPEL”) 30 June 2012 Quarter End Review Professional Investors Only – Not For Public Distribution Objective JPEL JPEL’s core strategy is to purchase private equity fund interests in the secondary market. Company Summary Launched 30 June 2005 Fund Level - Investment Strategy1,2 US$ Zero Dividend Zero Dividend Zero Dividend Eqqyuity Preference Preference Preference JPEL IfInfra- Share Share 2013 Share 2015 Share 2017 Warrants structure Real Estate 3% Net Asset Value (“NAV”) 9% per share US$ 1.14 68.05p 65.31p 69.25p N/A Venture No. of shares in issue 380.35 mm 63.16 mm 67.08 mm 30.41 mm 57.90 mm Capital 10% Currency of Quotation US$ £ Sterling £ Sterling £ Sterling US$ Ticker JPEL JPEZ JPZZ JPSZ JPWW Sedol B07V0H2 B07V0R2 B00DDT8 B5N4JV7 B60XDY5 DbtDebt 19% Buyout 59% ISIN GB00B07V0H27 GB00B07V0R25 GG00B00DDT81 GG00B5N4JV75 GG00B60XDY53 Market Makers ABN Amro Cazenove Cazenove Cazenove ABN Amro Cazenove Collins Stewart Collins Stewart Collins Stewart Cazenove HSBC Bank HSBC Bank HSBC Bank HSBC Bank HSBC Bank Fund Level - Currency Exposure1 Winterflood Winterflood Winterflood AED AUD 1% All figures as at 30 June 2012. NAV Figures are based based on unaudited net asset values as at 30 June 2012 . 7% GBP 7% Company Description J.P. Morgan Private Equity Limited (“JPEL” or the “Company”) is a global private equity fund listed on the London Stock Exchange. JPEL’s core strategy is to purchase private equity fund interests in the secondary market. EUR 35% USD JPEL pursues the following strategies to seek to meet its investment objectives 50% •Acquires secondary portfolios of direct investments and siggynificantly invested partnership investments to accelerate NAV development. -

Limited Partnerships and Private Equity Alexander Corrie

Limited Partnerships and Private Equity Alexander R. Corrie The concept of the limited partnership is not entirely new to Jamaica, as legislation has provided for the creation of these entities for over 150 years. However, the Partnerships (Limited) Act, 1853 has been found wanting in a number of key respects, particularly as it relates to the necessities and intricacies of the modern commercial landscape. The newly enacted Partnership (Limited) Act, 2017 has introduced a new regime, which includes several novel forms of limited partnerships as well as a more defined set of rules which govern their formation and operation. Many of these rules facilitate the effective utilization of the limited partnership as an investment vehicle. For many years, the limited liability company has been the vehicle of choice for most entrepreneurs seeking to operate businesses, as well as for many investors using that structure to acquire, hold and sell assets. This is due in no small part to liability protection, separate legal personality and other benefits afforded to shareholders under the company law regime. In contrast, the suitability and effectiveness of a traditional partnership as an investment vehicle is limited, as each individual partner potentially faces unlimited personal liability for the debts of the partnership. Unlike traditional partnerships, which are comprised simply of partners, a limited partnership consists of general partners and limited partners, and there must be at least one person in each category. There is a clear delineation between these roles, whereby general partners are responsible for the firm’s management, while limited partners are forbidden from taking part in the management of the partnership business and do not have the power to bind the firm. -

Morningstar Report

Report as of 02 Oct 2021 Threadneedle Monthly Extra Income Fund Retail Income GBP Morningstar® Category Morningstar® Benchmark Fund Benchmark Morningstar Rating™ Category_EUCA000916 Morningstar UK Moderately 20% ICE BofA Sterling Corp&Coll TR QQQ Adventurous Target Allocation NR GBP EUR, 80% FTSE AllSh TR GBP Used throughout report Investment Objective Performance The Fund aims to provide a monthly income with prospects 172 for capital growth over the long term. It looks to provide 154 an income yield higher than the FTSE All-Share Index over 136 rolling 3-year periods, after the deduction of charges. The 118 Fund is actively managed, and invests in a combination of 100 company shares and bonds; typically, between 70-80% in 82 UK company shares and 20%-30% in bonds. 2016 2017 2018 2019 2020 2021-08 12.39 6.59 -5.45 19.10 -5.17 11.72 Fund - - - - 4.52 9.96 Benchmark 13.23 10.00 -6.37 15.67 5.25 9.54 Category Risk Measures Trailing Returns % Fund Bmark Cat Quarterly Returns % Q1 Q2 Q3 Q4 3Y Alpha -4.50 3Y Sharpe Ratio 0.33 3 Months 1.16 0.35 0.46 2021 2.78 4.59 - - 3Y Beta 1.30 3Y Std Dev 14.34 6 Months 6.14 5.16 5.16 2020 -20.71 10.08 -0.11 8.77 3Y R-Squared 89.79 3Y Risk abv avg 1 Year 17.92 15.22 15.32 2019 6.46 2.75 4.10 4.59 3Y Info Ratio -0.54 5Y Risk abv avg 3 Years Annualised 3.80 6.62 6.12 2018 -4.05 8.69 -0.28 -9.09 3Y Tracking Error 5.57 10Y Risk abv avg 5 Years Annualised 4.71 7.20 6.49 2017 3.91 2.73 -0.15 0.01 Calculations use Morningstar UK Moderately Adventurous Target Allocation NR GBP 10 Years Annualised 8.86 8.92 8.05 -

Annual Report and Accounts 2018 01 Overview Performance Highlights for the Year to 31 March 2018

3i Group plc Overview Governance Introduction 01 Chairman’s introduction 58 Performance highlights 02 Board of Directors and Executive Committee 60 Chairman’s statement 02 Nominations Committee report 65 Chief Executive’s statement 04 Audit and Compliance Committee report 66 Action 08 Valuations Committee report 70 Directors’ remuneration report 73 Our business Relations with shareholders 83 Our business at a glance 10 Additional statutory and corporate governance information 84 Our business model 12 Our strategic objectives 14 Audited financial statements Key performance indicators 16 Private Equity 18 Consolidated statement of comprehensive income 92 Infrastructure 25 Consolidated statement of financial position 93 Performance, risk and sustainability Consolidated statement of changes in equity 94 Consolidated cash flow statement 95 Financial review 29 Company statement of financial position 96 Investment basis 35 Company statement of changes in equity 97 Reconciliation of Investment basis and IFRS 39 Company cash flow statement 98 Alternative Performance Measures 43 Significant accounting policies 99 Risk management 44 Notes to the accounts 104 Principal risks and mitigations 47 Independent Auditor’s report 139 Sustainability 52 Portfolio and other information 20 Large investments 148 Strategic report: Portfolio valuation – an explanation 150 pages 2 to 56. Information for shareholders 152 Directors’ report: pages Glossary 154 58 to 72 and 83 to 90. For definitions of our financial terms, used throughout this report, please see Directors’ remuneration our glossary on pages 154 to 156. report: pages 73 to 82. Consistent with our approach since the introduction of IFRS 10 in 2014, the financial data presented in the Overview and Strategic report is taken from the Investment basis financial statements. -

RRP Sector Assessment

OrbiMed Asia Partners III, LP Fund (RRP REG 51072) OWNERSHIP, MANAGEMENT, AND GOVERNANCE A. The Fund Structure 1. The Asian Development Bank (ADB) proposes to invest in OrbiMed Asia Partners III, LP Fund (OAP III), which is a Cayman Islands exempted limited partnership seeking to raise up to $500 million in capital commitments. It is managed by OrbiMed Asia GP III, LP (the general partner), a Cayman Islands exempted limited partnership. The sole limited partner of the general partner is OrbiMed Advisors III Limited, a Cayman Islands exempted company. OrbiMed Advisors LLC (the investment advisor), a registered investment advisor with the United States (US) Securities and Exchange Commission, will provide investment advisory services to OAP III. This structure is illustrated in the figure below. Table 1 shows the ultimate beneficial owners (UBOs) of the general partner and the investment advisor. Table 1: Ultimate Beneficial Owners of the General Partner and the Investment Advisor (ownership stake, %) Name Investment Advisor General Partner Sven H. Borho (~10–25%) (~8%) Alexander M. Cooper (~8%) Carl L. Gordon (~10–25%) (~8%) (also Director) Geoffrey C. Hsu (<5%) (~8%) Samuel D. Isaly (~50–75%) (~8%) W. Carter Neild (<5%) (~8%) (also Director) Jonathan T. Silverstein (~5–10%) (~8%) (also Director) Sunny Sharma (~8%) (also Officer) Evan D. Sotiriou (~8%) David G. Wang (~8%) (also Officer) Jonathan Wang (~8%) (also Officer) Sam Block III (~8%) Source: OrbiMed Group. 2 2. Investors. The fund held a first closing of approximately $233.5 million on 1 March 2017, and a second closing of approximately $137.6 million on 26 April 2017. -

Form 3 FORM 3 UNITED STATES SECURITIES and EXCHANGE COMMISSION OMB APPROVAL Washington, D.C

SEC Form 3 FORM 3 UNITED STATES SECURITIES AND EXCHANGE COMMISSION OMB APPROVAL Washington, D.C. 20549 3235- OMB Number: 0104 INITIAL STATEMENT OF BENEFICIAL OWNERSHIP OF Estimated average burden hours per SECURITIES 0.5 response: Filed pursuant to Section 16(a) of the Securities Exchange Act of 1934 or Section 30(h) of the Investment Company Act of 1940 1. Name and Address of Reporting Person* 2. Date of Event 3. Issuer Name and Ticker or Trading Symbol Requiring Statement Sotera Health Co [ SHC ] GTCR INVESTMENT XI (Month/Day/Year) LLC 11/20/2020 4. Relationship of Reporting Person(s) to 5. If Amendment, Date of Original Issuer Filed (Month/Day/Year) (Last) (First) (Middle) (Check all applicable) 300 NORTH LASALLE STREET, X Director X 10% Owner 6. Individual or Joint/Group Filing SUITE 5600 Officer (give Other (specify (Check Applicable Line) title below) below) Form filed by One Reporting Person (Street) X Form filed by More than One CHICAGO IL 60654 Reporting Person (City) (State) (Zip) Table I - Non-Derivative Securities Beneficially Owned 1. Title of Security (Instr. 4) 2. Amount of Securities 3. Ownership 4. Nature of Indirect Beneficial Beneficially Owned (Instr. Form: Direct Ownership (Instr. 5) 4) (D) or Indirect (I) (Instr. 5) Common Stock, $0.01 par value per share ("Common 79,286,597(1) I See Footnote(2)(3)(4) Stock") Table II - Derivative Securities Beneficially Owned (e.g., puts, calls, warrants, options, convertible securities) 1. Title of Derivative Security (Instr. 4) 2. Date Exercisable and 3. Title and Amount of Securities 4. 5. -

Limited Partnership: Business, Government, Civil Society (Ngos) and the Public in the Extractive Industry Transparency Initiative (EITI)

Institute for International Economic Policy Working Paper Series Elliott School of International Affairs The George Washington University Limited Partnership: Business, Government, Civil Society (NGOs) and the Public in the Extractive Industry Transparency Initiative (EITI) IIEPWP201028 Susan Ariel Aaronson George Washington University Jennifer Brinkerhoff George Washington University October 2009 Institute for International Economic Policy 1957 E St. NW, Suite 502 Voice: (202) 994‐5320 Fax: (202) 994‐5477 Email: [email protected] Web: www.gwu.edu/~iiep Limited Partnership: Business, Government, Civil Society (NGOs) and the Public in the Extractive Industry Transparency Initiative (EITI) 1 PAAD711 Limited Partnership: Business, Government, Civil Society and the Public in the Extractive Industry Transparency Initiative (EITI) Nigeria is awash in oil; Mali is flush with gold reserves; and Peru has abundant copper. These resources belong to the people, and thus, Nigerians, Malians, and Peruvians should benefit from their extraction and sale. But in many resource rich developing countries, policymakers lack the skills, will, or expertise to effectively manage the funds derived from these resources. Officials may funnel mining or petrodollars to their allies and families to stay in power. In some nations with weak institutions, a lack of accountability and transparency about resource revenues can exacerbate poor governance, and lead to corruption, conflict, and inequality (Karl, 1997, Ross: 2001; and Auty: 2001). Meanwhile, citizens of these resource rich countries have little say over how the revenues are spent or invested. This affliction is known as the resource curse (Lederman and Maloney: 2007, and Sachs and Warner: 1995). Extractive industry companies, civil society activists, and some developing county policymakers have collaborated to help people from resource rich nations such as Nigeria govern more effectively. -

Limited Partnerships

INTELLECTUAL PROPERTY AND TRANSACTIONAL LAW CLINIC LIMITED PARTNERSHIPS INTRODUCTORY OVERVIEW A limited partnership is a business entity comprised of two or more persons, with one or more general partners and one or more limited partners. A limited partnership differs from a general partnership in the amount of control and liability each partner has. Limited partnerships are governed by the Virginia Revised Uniform Partnership Act,1 which is an adaptation of the 1976 Revised Uniform Limited Partnership Act, or RULPA, and its subsequent amendments. HOW A LIMITED PARTNERSHIP IS FORMED To form a limited partnership in Virginia, a certificate of limited partnership must be filed with the Virginia State Corporation Commission. This is different from general partnerships which require no formal recording with the Commonwealth. The certificate must state the name of the partnership,2 and, the name must contain the designation “limited partnership,” “a limited partnership,” “L.P.,” or “LP;” which puts third parties on notice of the limited liability of one or more partners. 3 Additionally, the certificate must name a registered agent for service of process, state the Post Office mailing address of the company, and state the name and address of every general partner. The limited partnership is formed on the date of filing of the certificate unless a later date is specified in the certificate.4 1 VA. CODE ANN. § 50, Ch. 2.2. 2 VA. CODE ANN. § 50-73.11(A)(1). 3 VA. CODE ANN. § 50-73.2. 4 VA. CODE ANN. § 50-73.11(C)0). GENERAL PARTNERS General partners run the company's day-to-day operations and hold management control. -

SCHEDULE 13D Decibel Therapeutics, Inc

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 13D Under the Securities Exchange Act of 1934 Decibel Therapeutics, Inc. (Name of Issuer) Common Stock (Title of Class of Securities) 24343R106 (CUSIP Number) OrbiMed Advisors LLC OrbiMed Capital GP VIII LLC OrbiMed Genesis GP LLC OrbiMed Capital LLC 601 Lexington Avenue, 54th Floor New York, NY 10022 Telephone: (212) 739-6400 (Name, Address and Telephone Number of Person Authorized to Receive Notices and Communications) February 17, 2021 (Date of Event which Requires Filing of this Statement) If the filing person has previously filed a statement on Schedule 13G to report the acquisition that is the subject of this Schedule 13D, and is filing this schedule because of §§240.13d-1(e), 240.13d-1(f) or 240.13d-1(g), check the following box. ☐ Note: Schedules filed in paper format shall include a signed original and five copies of the schedule, including all exhibits. See §240.13d-7(b) for other parties to whom copies are to be sent. * The remainder of this cover page shall be filled out for a Reporting Person’s initial filing on this form with respect to the subject class of securities, and for any subsequent amendment containing information which would alter disclosures provided in a prior cover page. The information required on the remainder of this cover page shall not be deemed to be “filed” for the purpose of Section 18 of the Securities Exchange Act of 1934 (“Act”) or otherwise subject to the liabilities of that section of the Act but shall be subject to all other provisions of the Act (however, see the Notes).