Inventory Reduction Led to Considerable Sales Decline in The

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Automotive Industry Weekly Digest

Automotive Industry Weekly Digest 25-29 January 2021 IHS Markit Automotive Industry Weekly Digest - Jan 2021 WeChat Auto VIP Contents [OEM Highlights] Great Wall to reshape brand image with new models 3 [OEM Highlights] VW begins sales of ID.4 CROZZ in China 4 [Sales Highlights] Chinese new vehicle sales contract 2% during 2020; demand rebound expected in 2021 6 [Sales Highlights] VW Group reports sales decline of 9.1% in China during 2020 8 [Technology and Mobility Highlights] Huawei develops smart roads in Wuxi that communicate with driverless vehicles 10 [Technology and Mobility Highlights] Geely teams up with Tencent to develop smart car technologies 10 [Supplier Trends and Highlights] DENSO collaborate with AEVA to develop next-generation FMCW lidar system 12 [Supplier Trends and Highlights] Freudenberg Sealing Technologies develops new DIAvent valves for safer lithium-ion batteries 12 [GSP] India/Pakistan Sales and Production Commentary -2020.12 14 [VIP ASSET] Stellantis: Scale Creates Opportunity 16 [VIP ASSET] Stellantis expects scale to support strong brand stable, investment into new tech 17 Confidential. ©2021 IHS Markit. All rights reserved. 2 IHS Markit Automotive Industry Weekly Digest - Jan 2021 WeChat Auto VIP [OEM Highlights] Great Wall to reshape brand image with new models IHS Markit perspective Implications Great Wall has delivered satisfactory sales results during 2020 despite the disruption from the coronavirus disease 2019 (COVID-19) pandemic. The automaker's sales rose by 5% to more than 1.11 million vehicles during 2020 on the back of strong demand for its new models, including the Haval H6 and the Pao pickup. The sales volumes of 1.11 million units exceeded the company’s target set for the year, which was 1.02 million units. -

GREAT WALL MOTOR COMPANY LIMITED (A Joint Stock Company Incorporated in the People’S Republic of China with Limited Liability) (Stock Code: 2333)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. 長 城 汽 車 股 份 有 限 公 司 * GREAT WALL MOTOR COMPANY LIMITED (a joint stock company incorporated in the People’s Republic of China with limited liability) (Stock Code: 2333) ANNOUNCEMENT OF AUDITED ANNUAL RESULTS FOR THE YEAR ENDED 31 DECEMBER 2019 The board of directors (the “Board”) of Great Wall Motor Company Limited (the “Company”) is pleased to announce the audited results of the Company and its subsidiaries for the year ended 31 December 2019. This announcement, containing the full text of the 2019 Annual Report of the Company, is prepared with reference to the relevant requirements of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited in relation to preliminary announcements of Annual Results. The Company’s 2019 Annual Report will be available for viewing on the websites of The Stock Exchange of Hong Kong Limited at www.hkexnews.hk and of the Company at www.gwm.com.cn. Printed version of the Company’s 2019 Annual Report will also be delivered to the Company’s shareholders. By order of the Board Great Wall Motor Company Limited Xu Hui Company Secretary IMPORTANT NOTICE I. The Board, the Supervisory Committee and the directors, supervisors and senior management of the Company warrant that the contents of this annual report are true, accurate and complete and do not contain any false representations, misleading statements or material omissions, and jointly and severally take legal liability for its contents. -

Corporate, Social and Responsibility Report

(a joint stock company Incorporated in the People's Republic of China with limited liability) H Share Stock Code: 2333 A Share Stock Code: 601633 2 019 Corporate, Social and Responsibility Report * For identification purpose only CONTENTS About This Report 02 Message from Executives 04 A Close Look at Great Wall Motor 06 Corporate Governance 22 Responsibility Management 30 Product Responsibility 34 Responsibility for Employees 49 Social Responsibility 53 Environmental Responsibility 63 ESG Reporting Guide 72 Feedback Form 78 CSR Report 2019 1 About This Report About This Report I. REPORTING PERIOD: V. DEFINITIONS IN THE REPORT This report is the 9th annual corporate social responsibility report issued by Great Wall Motor Company “Great Wall Motor” or Great Wall Motor Company Limited Limited since 2011. This report covers the period from 1 January 2019 to 31 December 2019, with the “Company” or “we” certain information extending to the previous or subsequent years where appropriate. the “Group” the Company and its subsidiaries II. SCOPE OF REPORT: “Great Wall Holdings” Baoding Great Wall Holdings Company Limited (the indirect The scope of report covers the Company and its subsidiaries. Some contents involve Baoding Great Wall controlling shareholder of the Company) and its subsidiaries Holdings Co., Ltd and its subsidiaries. Please refer to the annual report of Great Wall Motor Company Limited for detailed corporate information. VI. NOTE TO THE REPORT III. CONTENTS OF REPORT: Data in this report are sourced from the Company’s audit report, annual report or other statistical documents. This report contains uncertainties about future plan or forecast. This report has not been This report discloses the Company’s information on economic, social and environmental performance reviewed by any independent source and investors are advised to be aware of the risks involved. -

Press Release

Press Release GREAT WALL MOTOR'S Q3 TOTAL OPERATING REVENUE ROSE BY 23.64% YOY TO RMB26.214 BILLION 23 October 2020 – A pick-up truck and SUV market leader in China, Great Wall Motor Company Limited (“Great Wall Motor” or the “Company”, H share stock code: 2333, A share stock code: 601633, together with its subsidiaries, the “Group”) announced that for the three months from 1 July 2020 to 30 September 2020 (the “Third Quarter”), the Group achieved an unaudited total operating revenue prepared in accordance with China Accounting Standards for Business Enterprises of RMB26,214,265,815.68, up by 23.64 per cent year-on-year; net profit attributable to shareholders of the Company increased by 2.91 per cent year-on-year to RMB1,441,071,262.11. Great Wall Motor's satisfactory business performance in the Third Quarter was mainly attributable to continued strong sales performance. The total automobile sales volume in the Third Quarter amounted to 285,593 units, up by 23.86 per cent year-on-year. For the nine months ended 30 September 2020, the Group's total operating revenue and net profit attributable to shareholders of the Company amounted to RMB62,143,459,463.53 and RMB2,587,213,985.01 respectively. According to the statistics from China Association of Automobile Manufacturers, in the first nine months of 2020, the sales volume of automobiles in China was 17.116 million units. The Group continued to strengthen its competitiveness in technology, products, brands and globalization to boost the overall sales volume. The Group’s total sales volume of automobiles in the first three quarters reached 680,690 units, further accelerating its market penetration of automobiles. -

Annual Report

(a joint stock company incorporated in the People's Republic of China with limited liability) H Share Stock Code: 2333 A Share Stock Code: 601633 2 019 ANNUAL REPORT * For identification purpose only IMPORTANT NOTICE I. The Board, the Supervisory Committee and the directors, supervisors and senior management of the Company warrant that the contents of this annual report are true, accurate and complete and do not contain any false representations, misleading statements or material omissions, and jointly and severally take legal liability for its contents. II. All the directors of the Company attended the Board meeting. III. Deloitte Touche Tohmatsu Certified Public Accountants LLP has issued the standard audited report for the Company without qualified opinion. The financial information in the annual report was prepared in accordance with China Accounting Standards for Business Enterprises and the relevant laws and regulations. IV. Wei Jian Jun, person-in-charge of the Company, Liu Yu Xin, person-in-charge of the accounting affairs and Lu Cai Juan, person-in-charge of the accounting department (head of the accounting department), declare that they warrant the truthfulness, accuracy and completeness of the financial report in this annual report. V. Proposal of profit distribution or capitalization of capital reserve during the Reporting Period reviewed by the Board As audited by Deloitte Touche Tohmatsu Certified Public Accountants LLP, the net profit of the Group and net profit attributable to shareholders of the Company in 2019 amounted to RMB4,530,732,870.30 and RMB4,496,874,893.92 respectively. The Company proposed to declare a cash dividend of RMB2,281,817,250.00, (representing RMB0.25 per share) (tax inclusive) to the shareholders of the Company for the year ended 31 December 2019. -

長 城 汽 車 股 份 有 限 公 司 Great Wall Motor Company Limited

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. 長 城 汽 車 股 份 有 限 公 司 * GREAT WALL MOTOR COMPANY LIMITED (a joint stock company incorporated in the People’s Republic of China with limited liability) (Stock code: 2333) ANNOUNCEMENT OF INTERIM RESULTS FOR THE SIX MONTHS ENDED 30 JUNE 2020 The board of directors (the “Board”) of Great Wall Motor Company Limited (the “Company”) is pleased to announce the unaudited interim results of the Company and its subsidiaries for the six months ended 30 June 2020. This announcement, containing the full text of the 2020 Interim Report of the Company, is prepared with reference to the relevant requirements of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited in relation to preliminary announcements of interim results. Printed version of the Company’s 2020 Interim Report will be delivered to the Company’s shareholders and will also be available for viewing on the websites of Hong Kong Exchanges and Clearing Limited at www.hkexnews.hk and of the Company at www.gwm.com.cn. By order of the Board Great Wall Motor Company Limited Xu Hui Company Secretary * For identification purpose only IMPORTANT NOTICE I. The Board, the Supervisory Committee and the directors, supervisors and senior management of the Company warrant that the information in this interim report is true, accurate and complete and does not contain any false representations, misleading statements or material omissions, and severally and jointly take legal liability for its contents. -

GREAT WALL MOTOR COMPANY LIMITED (A Joint Stock Company Incorporated in the People’S Republic of China with Limited Liability) (Stock Code: 2333)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. 長 城 汽 車 股 份 有 限 公 司 * GREAT WALL MOTOR COMPANY LIMITED (a joint stock company incorporated in the People’s Republic of China with limited liability) (Stock code: 2333) ANNOUNCEMENT OF INTERIM RESULTS FOR THE SIX MONTHS ENDED 30 JUNE 2019 The board of directors (the “Board”) of Great Wall Motor Company Limited (the “Company”) is pleased to announce the unaudited interim results of the Company and its subsidiaries for the six months ended 30 June 2019. This announcement, containing the full text of the 2019 Interim Report of the Company, is prepared with reference to the relevant requirements of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited in relation to preliminary announcements of interim results. Printed version of the Company’s 2019 Interim Report will be delivered to the Company’s shareholders and will also be available for viewing on the websites of Hong Kong Exchanges and Clearing Limited at www.hkexnews.hk and of the Company at www.gwm.com.cn. By order of the Board Great Wall Motor Company Limited Xu Hui Company Secretary * For identification purpose only IMPORTANT NOTICE I. The Board, the Supervisory Committee and the directors, supervisors and senior management of the Company warrant that the information in this interim report is true, accurate and complete and does not contain any false representations, misleading statements or material omissions, and severally and jointly take legal liability for its contents. -

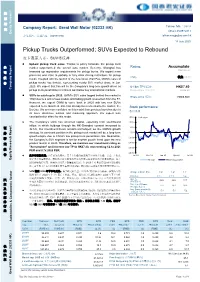

Pickup Trucks Outperformed; Suvs Expected to Rebound 皮卡跑赢大市,SUV将反弹

股 票 研 [Table_Title] Company Report: Great Wall Motor (02333 HK) Toliver Ma 马守彰 究 (852) 2509 5317 Equity Research 公司报告: 长城汽车 (02333 HK) [email protected] 14 July 2020 [Table_Summary] Pickup Trucks Outperformed; SUVs Expected to Rebound 皮卡跑赢大市,SUV将反弹 Upbeat pickup truck sales. Thanks to policy tailwinds, the pickup truck [Table_Rank] 公 market outperformed the overall auto market. Recently, Shanghai has Rating: Accumulate Maintained loosened up registration requirements for pickup trucks. We expect more 司 Report provinces and cities to partially or fully relax driving restrictions for pickup 评级: 收集 (维持) 报 trucks. Coupled with the launch of the new Great Wall Pao, GWM’s sales of 告 pickup trucks has thrived, representing nearly 50% market share in Jun. 2020. We expect that this will be the Company’s long-term growth driver as 6[Table_Price-18m TP目标价] : HK$7.40 Company pickup truck penetration in China is well below key international markets. Revised from 原目标价: HK$6.00 SUVs to catch up in 2H20. GWM’s SUV sales lagged behind the market in Share price 股价: HK$6.650 1H20 due to a lack of new models and fading growth momentum from the F7. However, we expect GWM to come back in 2H20 with two new SUVs expected to be launched. One has already been unveiled to the market, the Stock performance Da Gou. We are more confident on this model than previous launches due to 股价表现 its more distinctive outlook and marketing approach. We expect less [Table_QuotePic] cannibalization effect for this model. 30.0 % of return The Company’s stock has attracted capital, especially from southbound 20.0 inflow, in which holdings through the HK-Shanghai connect increased to 10.0 证 32.6%. -

Interim Report

(A joint stock company incorporated in the People's Republic of China with limited liability) H Share Stock Code: 2333 A Share Stock Code: 601633 2019 INTERIM REPORT * For identification purpose only IMPORTANT NOTICE I. The Board, the Supervisory Committee and the directors, supervisors and senior management of the Company warrant that the information in this interim report is true, accurate and complete and does not contain any false representations, misleading statements or material omissions, and severally and jointly take legal liability for its contents. II. Director(s) absent from the Board meeting Position of the Name of the Reasons for being director(s) absent from director(s) absent from absent from the Board meeting the Board meeting the Board meeting Representative Director Yang Zhi Juan Work commitment Wang Feng Ying III. This interim report of the Company has not been audited. The financial information in this interim report was prepared in accordance with China Accounting Standards for Business Enterprises and the relevant laws and regulations. IV. Wei Jian Jun, person-in-charge of the Company, Liu Yu Xin, person-in-charge of the accounting affairs and Lu Cai Juan, person-in-charge of the accounting department (head of the accounting department), declare that they warrant the truthfulness, accuracy and completeness of the financial report in this interim report. V. Proposal of profit distribution or capitalisation of capital reserve during the Reporting Period considered by the Board None VI. Risks relating to forward-looking statements √ Applicable □ Not applicable Forward-looking statements, such as future plans described in this report do not constitute an actual commitment of the Company to investors. -

3D Cars Models Catalogue (On September 30, 2021)

3D cars models catalogue (on September 30, 2021) Abarth 001 Abarth 205a Vignale berlinetta 1950 AC Shelby Cobra 001 AC Shelby Cobra 427 1965 002 AC Shelby Cobra 289 roadster 1966 003 Shelby Cobra Daytona 1964 004 AC 3000ME 1979 Acura 001 Acura TL 2012 001 ATS GT 2021 002 Acura MDX 2011 003 Acura ZDX 2012 004 Acura NSX 2012 005 Acura RDX 2013 006 Acura RL 2012 007 Acura NSX convertible 2012 008 Acura ILX 2013 009 Acura RLX 2013 010 Acura MDX Concept 2014 011 Acura RSX Type-S 2005 012 Acura TLX Concept 2015 013 Acura Integra 1990 014 Acura MDX 2003 015 Acura Vigor 1991 016 Acura TLX 2014 017 Acura ILX (DE) 2016 018 Acura TL 2007 019 Acura Integra coupe 1991 020 Acura NSX 2016 021 Acura Precision 2016 022 Acura CDX 2016 023 Acura NSX EV 2016 024 Acura TLX A-Spec 2017 025 Acura MDX Sport Hybrid 2017 026 Acura RLX Sport Hybrid SH-AWD 2017 027 Acura MDX Sport Hybrid with HQ interior 2017 028 Acura RLX Sport Hybrid SH-AWD with HQ interior 2017 029 Acura RDX Prototype 2018 030 Acura ILX A-spec 2019 031 Acura MDX 2014 032 Acura MDX RU-spec 2014 033 Acura RDX RU-spec 2014 034 Acura Type-S 2019 035 Acura NSX 1990 036 Acura RDX A-spec 2019 037 Acura ARX-05 DPi 2018 038 Acura RDX 2006 039 Acura MDX A-Spec 2018 040 Acura TLX Type S 2020 041 Acura TLX A-Spec 2020 042 Acura MDX A-Spec US-spec 2021 AD Tramontana 001 AD Tramontana C 2007 Adler 001 Adler Trumpf Junior Sport Roadster 1935 AEC 001 AEC Routemaster RM 1954 002 AEC Routemaster RMC 1954 Aermacchi 001 Aermacchi Chimera 1957 Aeromobil 001 Aeromobil 3.0 2014 Agrale 001 Agrale 10000 Chassis Truck -

Social Responsibility Report CONTENTS Issued by Great Wall Motor Company Limited Since 2011

(a joint stock company Incorporated in the People's Republic of China with limited liability) H Share Stock Code: 2333 A Share Stock Code: 601633 2020 Corporate, Social and Responsibility Report * For identification purpose only About This Report I. REPORTING PERIOD This report is the 10th annual corporate social responsibility report CONTENTS issued by Great Wall Motor Company Limited since 2011. This report covers the period from 1 January 2020 to 31 December 2020, with certain information extending to the previous or Only when There is No Retreat Making Innovations in Smart Advocating a Green Culture subsequent years where appropriate. will There be a Way Out Travel for Prosperity II. SCOPE OF REPORT Chairman’s Statement ................2 Product Responsibility ..............25 Environmental Responsibility .....53 The scope of report covers the Company and its subsidiaries. Some contents involve Baoding Great Wall Holdings Co., Ltd and its subsidiaries. Please refer to the annual report of Great Wall Motor Rock the World with Our Company Limited for detailed corporate information. Taking Root in Great Wall ESG Reporting Guide ...............60 GIFT (Green Intelligent Future Motor III. CONTENTS OF REPORT Technology), the Core Values Responsibility for Employees .....44 This report discloses the Company’s information on economic, Feedback Form ........................65 social and environmental performance indicators, social of Anti-corruption, Honesty, responsibility and sustainable development in 2020. Innovation, Changes, Sharing -

Morning Research Focus Table of Contents 目录

股 票 研 Research 究 [Table_Title] Equity Research Department Morning Research Focus 13 February 2020 [Table_Summary] Table of Contents 目录 Focus 今 News Focus 新闻焦点 晨 Industry and Company Focus 行业和公司焦点 焦 Research Great Wall Motor (02333HK): Vehicles Sales Decreased 28.2% YoY in January 2020 点 长城汽车 : 年 月汽车销量同比下跌 (02333HK) 2020 1 28.2% Morning Latest Reports 最新报告摘要 Company EPS Code Title TP Chg Rating Chg Name Est.Change? 代码 标题 目标价 z 评级 变动 公司名称 盈利预测是否改变 Flash Note: MoF Urges Early Infrastructure Release of New Local Government -- Outperform -- N Sector 证 Debt of RMB848 Billion for 2020 告 快讯:财政部要求提前下达 2020 年新增 券 基建行业 -- 跑赢大市 -- 否 地方政府债务限额人民币 8,480 亿元 研 报 究 究 Appendices :Chinese Version of the Industry and Company Focus, Latest Reports. 报 研 后附:行业和公司焦点,最新报告摘要中文版。 告 券 Equity Research Report 证 HSI Performance HSCEI Performance 16,000 35,000 33,000 14,000 31,000 29,000 12,000 27,000 25,000 10,000 23,000 21,000 8,000 19,000 17,000 6,000 Feb/19 May/19 Aug/19 Nov/19 Feb/20 Feb/19 May/19 Aug/19 Nov/19 Feb/20 Source: Bloomberg Source: Bloomberg Please subscribe GTJAI Research Wechat public account. Wechat ID: 国泰君安国际研究部 or scan the QR code. Research Report Database: (1) www.gtjai.com – “Research” – “Focus: Company”/”Research Highlights” (2) Bloomberg Report Page: RESP GJIR or NH GTJ 欢迎订阅国泰君安国际研究部微信公众号。 公众号账号:国泰君安国际研究部 也可扫右侧二维码关注。 研究报告库:(1) www.gtjai.com – “研究报告” – “公司点评”/“专题研究” (2) Bloomberg 报告页面: RESP GJIR 或 NH GTJ See the last page for disclaimer 1 of 6 Morning Research Focus 新闻焦点 [NewsTable_ NewsFocus]Focus The Federal Reserve will be forced to use large-scale asset purchases “aggressively” in a downturn, Chairman Jerome Powell said, as central bankers confront the dilemma of persistently low interest rates.