Dir Upper.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

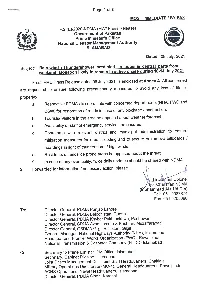

08 July 2021, Is Enclosed at Annex A

Page 1 of3 MOST IMMEDIATE/BY FAX F.2 (E)/2020-NDMA (MW/ Press Release) Government of Pakistan Prime Minister's Office National Disaster Management Authority ISLAMABAD NDMA Dated: 08 July, 2021 Subject: Rain-wind / Thundershower predicted in upper & central parts from weekend (Monsoon likely to remain in active phase during 10-14 July 2021 concerned Fresh PMD Press Release dated 08 July 2021, is enclosed at Annex A. All measures to avoid any loss of life or are requested to ensure following precautionary property: FWO and a. Respective PDMAs to coordinate with concerned departments (NHA, obstruction. C&W) for restoration of roads in case of any blockage/ . Tourists/Visitors in the area be apprised about weather forecast C. Availability of staff of emergency services be ensured. Coordinate with relevant district and municipal administration to ensure d. mitigation measures for urban flooding and to secure or remove billboards/ hoardings in light of thunderstorm/ high winds the threat. e. Residents of landslide prone areas be apprised about In case of any eventuality, twice daily updates should be shared with NDMA. f. 2 Forwarded for information / necessary action, please. Lieutenant Colonel For Chainman NDMA (Muhammad Ala Ud Din) Tel: 051-9087874 Fax: 051 9205086 To Director General, PDMA Punjab Lahore Director General, PDMA Balochistan, Quetta Director General, PDMA Khyber Pukhtunkhwa, Peshawar Director General, SDMA Azad Jammu & Kashmir, Muzaffarabad Director General, GBDMA Gilgit Baltistan, Gilgit General Manager, National Highways Authority -

Politics of Nawwab Gurmani

Politics of Accession in the Undivided India: A Case Study of Nawwab Mushtaq Gurmani’s Role in the Accession of the Bahawalpur State to Pakistan Pir Bukhsh Soomro ∗ Before analyzing the role of Mushtaq Ahmad Gurmani in the affairs of Bahawalpur, it will be appropriate to briefly outline the origins of the state, one of the oldest in the region. After the death of Al-Mustansar Bi’llah, the caliph of Egypt, his descendants for four generations from Sultan Yasin to Shah Muzammil remained in Egypt. But Shah Muzammil’s son Sultan Ahmad II left the country between l366-70 in the reign of Abu al- Fath Mumtadid Bi’llah Abu Bakr, the sixth ‘Abbasid caliph of Egypt, 1 and came to Sind. 2 He was succeeded by his son, Abu Nasir, followed by Abu Qahir 3 and Amir Muhammad Channi. Channi was a very competent person. When Prince Murad Bakhsh, son of the Mughal emperor Akbar, came to Multan, 4 he appreciated his services, and awarded him the mansab of “Panj Hazari”5 and bestowed on him a large jagir . Channi was survived by his two sons, Muhammad Mahdi and Da’ud Khan. Mahdi died ∗ Lecturer in History, Government Post-Graduate College for Boys, Dera Ghazi Khan. 1 Punjab States Gazetteers , Vol. XXXVI, A. Bahawalpur State 1904 (Lahore: Civil Military Gazette, 1908), p.48. 2 Ibid . 3 Ibid . 4 Ibid ., p.49. 5 Ibid . 102 Pakistan Journal of History & Culture, Vol.XXV/2 (2004) after a short reign, and confusion and conflict followed. The two claimants to the jagir were Kalhora, son of Muhammad Mahdi Khan and Amir Da’ud Khan I. -

Deforestation in the Princely State of Dir on the North-West Frontier and the Imperial Strategy of British India

Central Asia Journal No. 86, Summer 2020 CONSERVATION OR IMPLICIT DESTRUCTION: DEFORESTATION IN THE PRINCELY STATE OF DIR ON THE NORTH-WEST FRONTIER AND THE IMPERIAL STRATEGY OF BRITISH INDIA Saeeda & Khalil ur Rehman Abstract The Czarist Empire during the nineteenth century emerged on the scene as a Eurasian colonial power challenging British supremacy, especially in Central Asia. The trans-continental Russian expansion and the ensuing influence were on the march as a result of the increase in the territory controlled by Imperial Russia. Inevitably, the Russian advances in the Caucasus and Central Asia were increasingly perceived by the British as a strategic threat to the interests of the British Indian Empire. These geo- political and geo-strategic developments enhanced the importance of Afghanistan in the British perception as a first line of defense against the advancing Russians and the threat of presumed invasion of British India. Moreover, a mix of these developments also had an impact on the British strategic perception that now viewed the defense of the North-West Frontier as a vital interest for the security of British India. The strategic imperative was to deter the Czarist Empire from having any direct contact with the conquered subjects, especially the North Indian Muslims. An operational expression of this policy gradually unfolded when the Princely State of Dir was loosely incorporated, but quite not settled, into the formal framework of the imperial structure of British India. The elements of this bilateral arrangement included the supply of arms and ammunition, subsidies and formal agreements regarding governance of the state. These agreements created enough time and space for the British to pursue colonial interests in Ph.D. -

Pdf 325,34 Kb

(Final Report) An analysis of lessons learnt and best practices, a review of selected biodiversity conservation and NRM projects from the mountain valleys of northern Pakistan. Faiz Ali Khan February, 2013 Contents About the report i Executive Summary ii Acronyms vi SECTION 1. INTRODUCTION 1 1.1. The province 1 1.2 Overview of Natural Resources in KP Province 1 1.3. Threats to biodiversity 4 SECTION 2. SITUATIONAL ANALYSIS (review of related projects) 5 2.1 Mountain Areas Conservancy Project 5 2.2 Pakistan Wetland Program 6 2.3 Improving Governance and Livelihoods through Natural Resource Management: Community-Based Management in Gilgit-Baltistan 7 2.4. Conservation of Habitats and Species of Global Significance in Arid and Semiarid Ecosystem of Baluchistan 7 2.5. Program for Mountain Areas Conservation 8 2.6 Value chain development of medicinal and aromatic plants, (HDOD), Malakand 9 2.7 Value Chain Development of Medicinal and Aromatic plants (NARSP), Swat 9 2.8 Kalam Integrated Development Project (KIDP), Swat 9 2.9 Siran Forest Development Project (SFDP), KP Province 10 2.10 Agha Khan Rural Support Programme (AKRSP) 10 2.11 Malakand Social Forestry Project (MSFP), Khyber Pakhtunkhwa 11 2.12 Sarhad Rural Support Program (SRSP) 11 2.13 PATA Project (An Integrated Approach to Agriculture Development) 12 SECTION 3. MAJOR LESSONS LEARNT 13 3.1 Social mobilization and awareness 13 3.2 Use of traditional practises in Awareness programs 13 3.3 Spill-over effects 13 3.4 Conflicts Resolution 14 3.5 Flexibility and organizational approach 14 3.6 Empowerment 14 3.7 Consistency 14 3.8 Gender 14 3.9. -

Old Habits, New Consequences Old Habits, New Khalid Homayun Consequences Nadiri Pakistan’S Posture Toward Afghanistan Since 2001

Old Habits, New Consequences Old Habits, New Khalid Homayun Consequences Nadiri Pakistan’s Posture toward Afghanistan since 2001 Since the terrorist at- tacks of September 11, 2001, Pakistan has pursued a seemingly incongruous course of action in Afghanistan. It has participated in the U.S. and interna- tional intervention in Afghanistan both by allying itself with the military cam- paign against the Afghan Taliban and al-Qaida and by serving as the primary transit route for international military forces and matériel into Afghanistan.1 At the same time, the Pakistani security establishment has permitted much of the Afghan Taliban’s political leadership and many of its military command- ers to visit or reside in Pakistani urban centers. Why has Pakistan adopted this posture of Afghan Taliban accommodation despite its nominal participa- tion in the Afghanistan intervention and its public commitment to peace and stability in Afghanistan?2 This incongruence is all the more puzzling in light of the expansion of insurgent violence directed against Islamabad by the Tehrik-e-Taliban Pakistan (TTP), a coalition of militant organizations that are independent of the Afghan Taliban but that nonetheless possess social and po- litical links with Afghan cadres of the Taliban movement. With violence against Pakistan growing increasingly indiscriminate and costly, it remains un- clear why Islamabad has opted to accommodate the Afghan Taliban through- out the post-2001 period. Despite a considerable body of academic and journalistic literature on Pakistan’s relationship with Afghanistan since 2001, the subject of Pakistani accommodation of the Afghan Taliban remains largely unaddressed. Much of the existing literature identiªes Pakistan’s security competition with India as the exclusive or predominant driver of Pakistani policy vis-à-vis the Afghan Khalid Homayun Nadiri is a Ph.D. -

Causes of Deforestation and Climatic Changes in Dir Kohistan

CORE Metadata, citation and similar papers at core.ac.uk Provided by International Institute for Science, Technology and Education (IISTE): E-Journals Journal of Pharmacy and Alternative Medicine www.iiste.org ISSN 2222-5668 (Paper) ISSN 2222-4807 (Online) Vol. 3, No. 2, 2014 Research Article Causes of deforestation and climatic changes in Dir Kohistan Muhammad Tariq1*, Muhammad Rashid2, Wajid Rashid3 1Department of Environmental Sciences, Shaheed Benazir Bhutto University, Sheringal Dir Upper, Pakistan 2School of Pharmacy, The University of Faisalabad, Faisalabad, Pakistan 3Department of Environmental Sciences, University of Swat, Pakistan *E-mail of the corresponding author: [email protected] Accepted Date: 22 May 2014 akistan is on 2nd position among those countries, where deforestation rate is very high. The current work is design to highlight the facts, real causes and impacts of deforestation and forest degradation in P “Dir Kohistan” of K.P.K Pakistan, by incorporating the view of local people through a questionnaire. According to this survey about 83% of the local people are dependent on these forests and contribute to deforestation in one of different ways regardless of any rule regulation. The current study shows that the extensive deforestation in the mention area occurs for household needs (cooking, furniture, heating, earning etc). Another growing cause is the cutting of these forests for livestock purposes. Along this the nonscientific grazing is a key point in the deforestation. Unemployment and poverty is another attractive factor in the degradation of these forests. However the role of black marketing and role of stake holders on these forests should not be neglected in deforestation. -

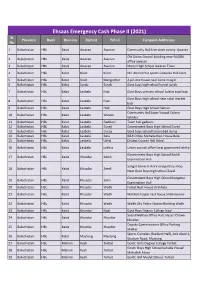

UPDATED CAMPSITES LIST for EECP PHASE-2.Xlsx

Ehsaas Emergency Cash Phase II (2021) Sr. Province Bank Division Distrcit Tehsil Campsite Addresses No. 1 Balochistan HBL Kalat Awaran Awaran Community Hall Live stock colony Awaran Old Union Council building near NADRA 2 Balochistan HBL Kalat Awaran Awaran office awaran 3 Balochistan HBL Kalat Awaran Awaran Model High School Awaran Town 4 Balochistan HBL Kalat Kalat Kalat Mir Ahmed Yar sports Complex Hall kalat 5 Balochistan HBL Kalat Kalat Mangochar A private house near Jame masjid 6 Balochistan HBL Kalat Surab Surab Govt boys high school hostel surab 7 Balochistan HBL Kalat Lasbela Hub Govt Boys primary school Adalat road hub Govt Boys high school near sabzi market 8 Balochistan HBL Kalat Lasbela Hub hub 9 Balochistan HBL Kalat Lasbela Hub Govt Boys High School Sakran Community Hall Jaam Yousuf Colony 10 Balochistan HBL Kalat Lasbela Winder Winder 11 Balochistan HBL Kalat Lasbela Gaddani Town hall gaddani 12 Balochistan HBL Kalat Lasbela Dureji Government Boys High School Dureji 13 Balochistan HBL Kalat Lasbela Dureji Govt boys school hasanabad dureji 14 Balochistan HBL Kalat Lasbela Bela B&R Office Mohalla Rest House Bela 15 Balochistan HBL Kalat Lasbela Uthal District Council Hall Uthal 16 Balochistan HBL Kalat Lasbela Lakhra Union council office local goverment lakhra Government Boys High School Karkh 17 Balochistan HBL Kalat Khuzdar Karkh Examination Hall Sangat General store and poltary shop 18 Balochistan HBL Kalat Khuzdar Zeedi Near Govt Boys high school Zeedi Government Boys High School Norgama 19 Balochistan HBL Kalat Khuzdar Zehri Examination Hall 20 Balochistan HBL Kalat Khuzdar Wadh Forest Rest House Drakhala 21 Balochistan HBL Kalat Khuzdar Wadh Mohbat Faqeer rest house Shahnoorani 22 Balochistan HBL Kalat Khuzdar Wadh Wadh City Police Station Building Wadh 23 Balochistan HBL Kalat Khuzdar Naal Govt Boys Degree College Naal Social Welfare Office Hall, Hazari Chowk 24 Balochistan HBL Kalat Khuzdar Khuzdar khuzdar. -

Ehsaas Emergency Cash Payments

Consolidated List of Campsites and Bank Branches for Ehsaas Emergency Cash Payments Campsites Ehsaas Emergency Cash List of campsites for biometrically enabled payments in all 4 provinces including GB, AJK and Islamabad AZAD JAMMU & KASHMIR SR# District Name Tehsil Campsite 1 Bagh Bagh Boys High School Bagh 2 Bagh Bagh Boys High School Bagh 3 Bagh Bagh Boys inter college Rera Dhulli Bagh 4 Bagh Harighal BISP Tehsil Office Harigal 5 Bagh Dhirkot Boys Degree College Dhirkot 6 Bagh Dhirkot Boys Degree College Dhirkot 7 Hattain Hattian Girls Degree Collage Hattain 8 Hattain Hattian Boys High School Chakothi 9 Hattain Chakar Boys Middle School Chakar 10 Hattain Leepa Girls Degree Collage Leepa (Nakot) 11 Haveli Kahuta Boys Degree Collage Kahutta 12 Haveli Kahuta Boys Degree Collage Kahutta 13 Haveli Khurshidabad Boys Inter Collage Khurshidabad 14 Kotli Kotli Govt. Boys Post Graduate College Kotli 15 Kotli Kotli Inter Science College Gulhar 16 Kotli Kotli Govt. Girls High School No. 02 Kotli 17 Kotli Kotli Boys Pilot High School Kotli 18 Kotli Kotli Govt. Boys Middle School Tatta Pani 19 Kotli Sehnsa Govt. Girls High School Sehnsa 20 Kotli Sehnsa Govt. Boys High School Sehnsa 21 Kotli Fatehpur Thakyala Govt. Boys Degree College Fatehpur Thakyala 22 Kotli Fatehpur Thakyala Local Govt. Office 23 Kotli Charhoi Govt. Boys High School Charhoi 24 Kotli Charhoi Govt. Boys Middle School Gulpur 25 Kotli Charhoi Govt. Boys Higher Secondary School Rajdhani 26 Kotli Charhoi Govt. Boys High School Naar 27 Kotli Khuiratta Govt. Boys High School Khuiratta 28 Kotli Khuiratta Govt. Girls High School Khuiratta 29 Bhimber Bhimber Govt. -

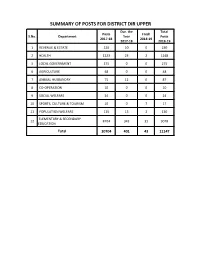

SUMMARY of POSTS for DISTRICT DIR UPPER Dur

SUMMARY OF POSTS FOR DISTRICT DIR UPPER Dur. the Total Posts Fresh S.No. Department Year Posts 2017-18 2018-19 2017-18 2018-19 1 REVENUE & ESTATE 220 10 0 230 2 HEALTH 1223 23 2 1248 5 LOCAL GOVERNMENT 275 0 0 275 6 AGRICULTURE 48 0 0 48 7 ANIMAL HUSBANDRY 75 12 0 87 8 CO-OPERATION 10 0 0 10 9 SOCIAL WELFARE 24 0 0 24 10 SPORTS, CULTURE & TOURISM 10 0 7 17 11 POPULATION WELFARE 115 13 2 130 ELEMENTARY & SECONDARY 12 8704 343 32 9078 EDUCATION Total 10704 401 43 11147 DISTRICT DIR UPPER Dur. the Total Posts Fresh Fund DDO Description Designation BPS Year Posts 2017-18 2018-19 2017-18 2018-19 DP21C09 Revenue & DP6136 Deputy Commissioner Dir Deputy Commissioner 19 1 1 Estate Upper DP21C09 Revenue & DP6136 Deputy Commissioner Dir Additional Deputy Commissioner 18 1 1 Estate Upper DP21C09 Revenue & DP6136 Deputy Commissioner Dir District Officer (Finance & 18 1 1 Estate Upper Planning) DP21C09 Revenue & DP6136 Deputy Commissioner Dir Accounts Officer 17 1 1 Estate Upper DP21C09 Revenue & DP6136 Deputy Commissioner Dir Additional Assistant 17 1 1 Estate Upper Commisisoner (Revenue) DP21C09 Revenue & DP6136 Deputy Commissioner Dir Additional Assistant 17 3 3 Estate Upper Commissioner DP21C09 Revenue & DP6136 Deputy Commissioner Dir Assistant Commissioner 17 3 3 Estate Upper DP21C09 Revenue & DP6136 Deputy Commissioner Dir Finance Officer 17 1 1 Estate Upper DP21C09 Revenue & DP6136 Deputy Commissioner Dir Planning Officer 17 1 1 Estate Upper DP21C09 Revenue & DP6136 Deputy Commissioner Dir Private Secretary 17 1 1 Estate Upper DP21C09 Revenue -

Audit Report on the Accounts of District Council and Municipal Committees, Dir Upper

AUDIT REPORT ON THE ACCOUNTS OF DISTRICT COUNCIL AND MUNICIPAL COMMITTEES, DIR UPPER AUDIT YEAR 2015-16 AUDITOR GENERAL OF PAKISTAN i TABLE OF CONTENTS ABBREVIATIONS AND ACRONYMS .................................................................. iii PREFACE ................................................................................................................... iv PREFACE ................................................................................................................... iv EXECUTIVESUMMARY ........................................................................................... v SUMMARY OF TABLES & CHARTS .................................................................. viii I Audit Work Statistics ............................................................................... viii II Audit Observations classified by Categories ........................................... viii III Outcome Statistics ....................................................................................... ix IV Irregularities reported ................................................................................... x V Cost- Benefit ................................................................................................. x CHAPTER 1 ................................................................................................................. 1 1.1 District Council and Municipal Committees Dir Upper ................................... 1 1.1.1 Introduction ............................................................................................... -

Ichthyofaunal Diversity of River Panjkora, District Dir Lower, Khyber Pakhtunkhwa Abstract Introduction

The Journal of Animal & Plant Sciences, 25(3 Supp. 2) 2015 Special Issue Page: 550-563 Hasan et al., ISSN: 1018-7081 J. Anim. Plant Sci. 25 (3 Supp. 2) 2015 ICHTHYOFAUNAL DIVERSITY OF RIVER PANJKORA, DISTRICT DIR LOWER, KHYBER PAKHTUNKHWA Z. Hasan1*, S. Ullah1, S. B. Rasheed1, A. Kakar2 and N.Ali1 1Department of Zoology, University of Peshawar, Pakistan 2Department of Zoology, University of Balochistan, Quetta, Pakistan *Corresponding Author’s Email: [email protected] ABSTRACT The study was conducted to determine the fish diversity in River Panjkora, Dir Lower from April to September 2012. A total of 781 individuals of fish representing 25 species, belonging to five families were caught during the study period. The fish fauna in the river was dominated by species belonging to the family Cyprinidae (49.93%) followed by Nemacheilidae (27.52%). Families Channidae, Sisoridae and Mastacembelidae constituted 10.88%, 10.37% and 1.28% respectively. Most dominant species were Crossocheilusdiplocheilus(15.492%) followed by Garragotyla (15.1%) and Cyprinuscarpio (8.194%). These species were abundant especially during the months of May and July. Ctenopharyngodonidella (Family: Cyprinidae), Triplophysamicrops (Family: Nemacheilidae)andSchisturamacrolepis (Family: Nemacheilidae) were the least existing species with 0.128%, 0.512% and 1.152% abundance respectively. Physico-chemical parameters of water were also monitored, mean values of which were as follows; temperature (21.275°C), pH (7.325), dissolved Oxygen (8.975mg/L), electric conductivity (201.675µs/cm), total dissolved solid (127.912 mg/L), total suspended solid (129.857 mg/L), total hardness (118.75mg/l), free CO2(4.3 mg/L), turbidity (1.34NTU), salinity (0.0075 mg/L), Ca hardness (77.5mg/L), Mg hardness(43.25mg/L), Sodium(5.1mg/L), Potassium(2.825mg/L), total alkalinity (98mg/L), Chloride (15.93mg/L) and nitrates (0.035mg/L). -

S.No ID.No Inst Name Tehsil Class Beds Locality Status 1 347006 BHU

DISTRICT DIR UPPER Basic Health Units S.No ID.No Inst Name Tehsil Class Beds Locality Status 1 347006 BHU Ganori Dir 1 Ganori Functional 2 347007 BHU Hatan Dara Dir 1 Ganori Functional 3 347009 BHU Kair Dara Dir 1 Bibyaware Functional 4 347010 BHU Darora Dir 1 Darora Functional 5 347011 BHU Battal Dir 1 Palam Functional 6 347013 BHU Jabbar Dir 1 Jabbar Functional 7 347014 BHU Sawni Dir 1 Sawni Functional 8 347016 BHU Ganshal Dir 1 Sawni Functional 9 347017 BHU Qulandi Dir 1 Qulandi Functional 10 347018 BHU Doug Mina Dir 1 Doug Dara Functional 11 347019 BHU Dobando Dir 1 Qulandi Functional 12 347025 BHU Janbatti Barawal 1 Shahi kot Functional 13 347026 BHU Bilachand Barawal 1 Darikand Functional 14 347027 BHU Shahikot Barawal 1 Darikand Functional 15 347028 BHU Bin payen Barawal 1 Shahi kot Functional 16 347031 BHU Bari kot Kalkot 1 Barikot Functional 17 347032 BHU Kalkot Kalkot 1 Kalkot Functional 18 347033 BHU Thall Kalkot 1 Kalkot Functional 19 347034 BHU Gwaldi Kalkot 1 Gwaldi Functional 20 347037 BHU Dislawar Wari 1 Dislawar Functional 21 347038 BHU Bara Dara Wari 1 Kotkay Functional 22 347039 BHU Daskore Bala Wari 1 Wari Functional 23 347040 BHU Pataw Wari 1 Kotkay Functional 24 347041 BHU Karo Dara Wari 1 Akhagram Functional 25 347042 BHU Kakad Wari 1 Wari Functional 26 347043 BHU Jillare Wari 1 Chappar Functional 27 347044 BHU Nasir Abad Wari 1 Chappar Functional 28 347045 BHU Sundal Wari 1 Sundal Functional 29 347046 BHU Nehag Bandi Wari 1 Nihag Bandi Functional 30 347047 BHU Malanga Wari 1 Dislawar Functional Barawal 1 Functional